Plastic Pipes Market Size 2024-2028

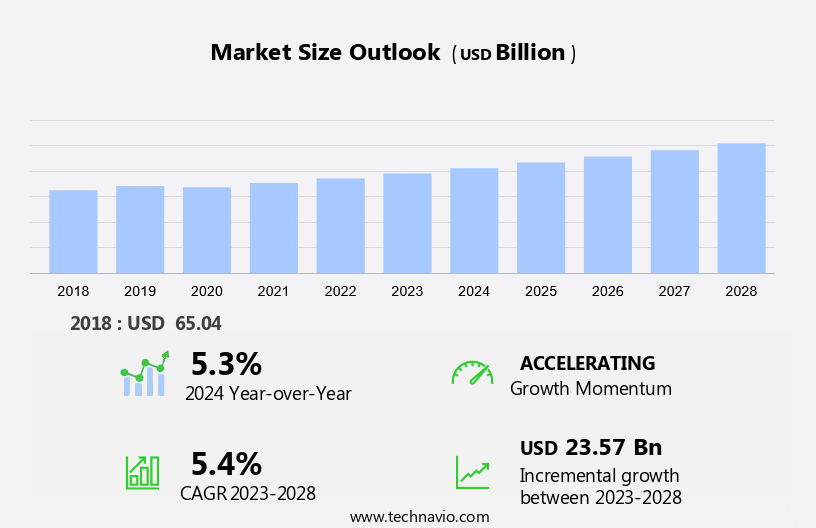

The plastic pipes market size is forecast to increase by USD 23.57 billion at a CAGR of 5.4% between 2023 and 2028.

- The market is experiencing significant growth due to several key factors. Firstly, the increasing construction activities in emerging economies are driving market expansion. In addition, the rising preference for anti-microbial pipes is contributing to market growth. However, the market is also facing challenges such as the fluctuating prices of raw materials used in plastic pipe production. These price fluctuations can impact the profitability of manufacturers and may lead to increased costs for end-users. Despite these challenges, the market is expected to continue growing due to its numerous advantages over traditional piping materials. The use of plastic pipes in various applications, including water supply, sewage, and natural gas transportation, is on the rise due to their durability, flexibility, and cost-effectiveness. The market is poised for steady growth In the coming years, with increasing demand from both developed and emerging economies.

What will be the Size of the Plastic Pipes Market During the Forecast Period?

- The market encompasses the production and supply of piping systems made from various plastic materials, including Polyvinyl Chloride (PVC), Polyethylene (PE), High-Density Polyethylene (HDPE), and Cross-Linked Polyethylene (PE-X), among others. This market plays a pivotal role in numerous industries, including water supply and sewage treatment, infrastructure investment, agriculture, and renewable energies. Plastic pipes are increasingly preferred due to their lightweight properties, resistance to corrosion, and durability.

- In the water supply sector, plastic pipes are used extensively for potable water transportation and distribution. In the context of sewage treatment, they facilitate efficient wastewater disposal. Plastic pipes also serve essential functions in agriculture, such as irrigation, and In the building and construction industry. The market is influenced by several trends, including extreme weather conditions, the growing demand for renewable energies, and the expansion of hydrogen networks. Plastic pipes are also employed as cable protection in power generation and chemical processing, as well as in food processing and water infrastructure. Overall, the market's growth is driven by the increasing demand for efficient, cost-effective, and sustainable piping solutions.

How is this Plastic Pipes Industry segmented and which is the largest segment?

The plastic pipes industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Material

- Polyvinyl chloride

- Polyethylene

- Polypropylene

- Others

- Application

- Water supply and distribution

- Sewage and drainage

- Gas distribution

- Agriculture

- Others

- Geography

- APAC

- China

- India

- Japan

- South Korea

- North America

- Canada

- US

- Europe

- Germany

- UK

- France

- Middle East and Africa

- South America

- APAC

By Material Insights

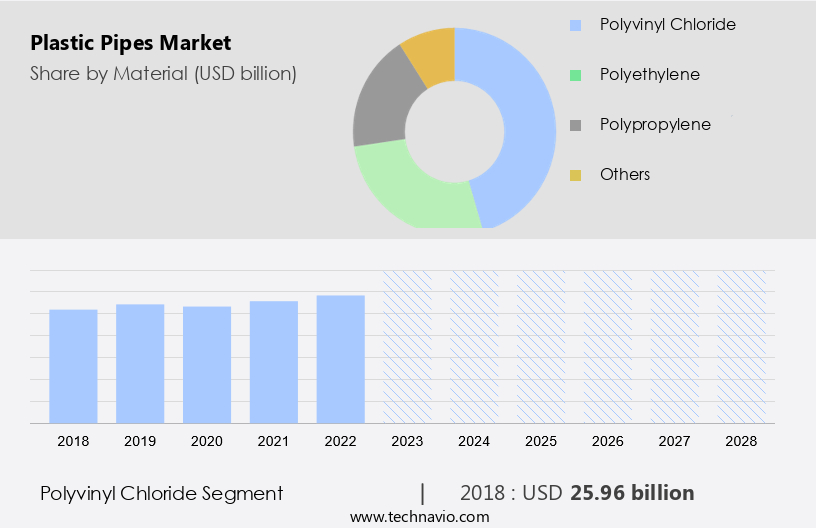

- The polyvinyl chloride segment is estimated to witness significant growth during the forecast period.

The market is driven by the widespread use of materials like Polyvinyl Chloride (PVC) and Polyethylene (PE) across various sectors. PVC, known for its durability, affordability, and versatility, is extensively used in water supply, sewage treatment, and pipeline projects. Its corrosion resistance, chemical resistance, and environmental stress tolerance make it ideal for applications in water and wastewater, agriculture, chemicals, and building and construction. PE, another key material, comes in various forms, including High-Density Polyethylene (HDPE), Low-Density Polyethylene (LDPE), and Cross-Linked Polyethylene (PE-X). PE pipes are valued for their lightweight properties, ease of installation, and non-reactive nature, making them perfect for use in water systems, power generation, chemical processing, food processing, and water infrastructure.

Furthermore, the market growth can be attributed to infrastructure investment, increasing water and wastewater demand, extreme weather conditions, renewable energies, hydrogen networks, and plastic cable protection. Additionally, the market is expanding in sectors like commercial and industrial, with applications in water supply systems, sewage systems, rainwater harvesting, wastewater management, water treatment plants, and wastewater treatment. The environmental impact of plastic pipes is a concern, but recycling and the use of recycled plastics and bioplastics are mitigating this issue.

Get a glance at the Plastic Pipes Industry report of share of various segments Request Free Sample

The polyvinyl chloride segment was valued at USD 25.96 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

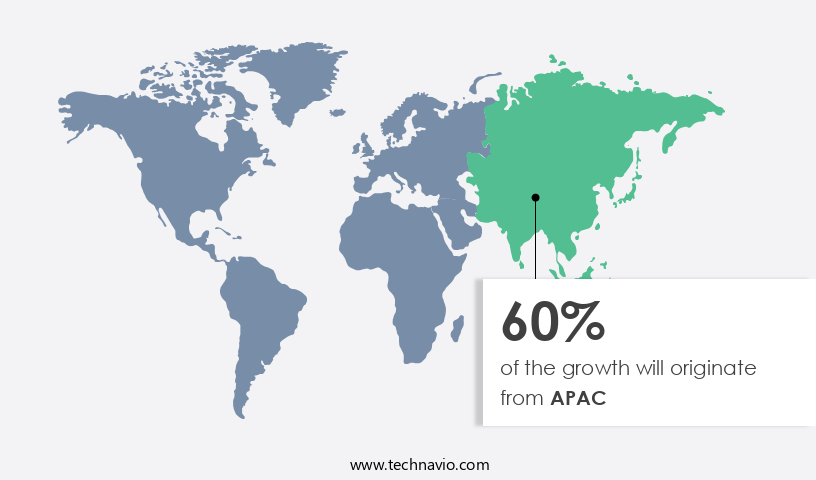

- APAC is estimated to contribute 60% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The Asia-Pacific (APAC) region's market is experiencing substantial growth due to the expanding construction sector in major countries like India and China. The Indian real estate industry is projected to grow from USD 200 billion in 2021 to USD 1 trillion by 2030, contributing 13% to the country's GDP by 2025. This growth encompasses various sectors, including residential, retail, hospitality, and commercial real estate, all requiring extensive infrastructure development. Plastic pipes are essential for plumbing, drainage, and other infrastructural applications In these sectors. In APAC, plastic pipe materials such as PVC, PE, PP, and others are widely used due to their lightweight properties, ease of installation, non-reactive nature, and corrosion resistance.

These pipes are crucial for water and wastewater applications, including potable water supply, sewage systems, rainwater harvesting, and wastewater treatment. Furthermore, plastic pipes are also utilized in agriculture, chemicals, renewable energies, hydrogen networks, plastic cable protection, and various industrial applications. The demand for plastic pipes is expected to continue growing due to infrastructure investment, water use in power generation and chemical processing, and food processing industries.

Market Dynamics

Our plastic pipes market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Plastic Pipes Industry?

Growing construction activities in emerging economies is the key driver of the market.

- The market is experiencing significant growth due to increasing infrastructure investment across various sectors. In pipeline projects for water supply and sewage treatment, plastic pipe materials such as PVC (Polyvinyl Chloride), PE (Polyethylene) including HDPE (High-Density Polyethylene) and LDPE (Low-Density Polyethylene), PP (Polypropylene), and others are favored for their durability, corrosion resistance, and ease of installation. The demand for plastic pipes is rising in the water and wastewater sector, as well as in agriculture, chemicals, and renewable energies, particularly for hydrogen networks and plastic cable protection. Additionally, extreme weather conditions and the growing need for water and wastewater disposal, rainwater harvesting, and wastewater management are further driving the market.

- The commercial and industrial sectors, including building and construction, power generation, chemical processing, food processing, and water infrastructure, are major consumers of plastic pipes due to their lightweight properties and non-reactive nature. The environmental impact of plastic waste, along with the growing need for recycling and the development of bioplastics, are also significant factors influencing the market.

What are the market trends shaping the Plastic Pipes Industry?

The growing popularity of anti-microbial pipes is the upcoming market trend.

- The market is experiencing significant growth due to the increasing adoption of plastic pipe materials, such as PVC, PE, PP, and others, in various pipeline projects for water supply and sewage treatment applications. Infrastructure investment in sectors like water and wastewater, agriculture, chemicals, renewable energies, hydrogen networks, and plastic cable protection is driving the demand for these pipes. Plastic pipes offer several advantages, including corrosion resistance, lightweight properties, ease of installation, and non-reactivity with water, making them a preferred choice over traditional materials. Additionally, extreme weather conditions and the growing need for efficient wastewater disposal and rainwater harvesting have further boosted the market.

- HDPE pipes are particularly popular for sewage systems due to their high strength and durability. The trend toward sustainability is also shaping the market, with the use of recycled plastics and bioplastics gaining traction. While the environmental impact of plastic pipes remains a concern, ongoing infrastructure development and the growing reliance of commercial and industrial sectors on water supply systems, power generation, chemical processing, and food processing are expected to continue driving market growth.

What challenges does the Plastic Pipes Industry face during its growth?

The fluctuating price of raw materials used in plastic pipe production is a key challenge affecting the industry growth.

- The market is influenced by various factors, primarily the prices of raw materials such as PE, PP, and PVC, which are derived from petrochemicals. These polymers are extensively used in pipeline projects for water supply, sewage treatment, and other applications, including agriculture, chemicals, renewable energies, hydrogen networks, plastic cable protection, and more. The volatility of crude oil prices significantly impacts the manufacturing costs and profit margins In the market. For instance, geopolitical tensions, like the full-scale invasion of Ukraine by Russia in H1 2022, led to a rise in crude oil prices, driving them to their highest inflation-adjusted level since 2014.

- Plastic pipes are preferred due to their corrosion resistance, lightweight properties, ease of installation, non-reactive nature, and suitability for various applications, such as water and wastewater, gas supply, building and construction, power generation, chemical processing, food processing, and water infrastructure. Additionally, plastic pipes are used in water treatment plants, wastewater management, sewage systems, rainwater harvesting, and wastewater treatment. Despite the challenges posed by fluctuating raw material prices, the market is expected to grow due to the increasing infrastructure investment and the demand for sustainable solutions in water and wastewater, agriculture, and other industries. The use of recycled plastics and bioplastics is also gaining traction, contributing to the market's growth and reducing the environmental impact.

Exclusive Customer Landscape

The plastic pipes market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the plastic pipes market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, plastic pipes market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Drainage Systems Inc.

- Aliaxis Holdings SA

- Astral Ltd.

- Chevron Phillips Chemical Co. LLC

- China Lesso Group Holdings Ltd.

- Georg Fischer Ltd.

- IPEX BRANDING INC.

- JM Eagle Inc

- Kubota Corp.

- NIBCO INC.

- Polypipe Ltd

- R C Plasto Tanks and Pipes Private Ltd

- RIFENG Enterprise Co Ltd

- Saudi Arabian Amiantit Co.

- Sekisui Chemical Co. Ltd.

- Tessenderlo Group NV

- Uponor Corp.

- Viega GmbH and Co. KG

- Wavin BV

- WL Plastics

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide range of applications, including water supply, sewage treatment, and various industries such as agriculture, chemicals, and building and construction. Plastic pipes offer several advantages over traditional materials, including corrosion resistance, lightweight properties, ease of installation, and non-reactive nature. In the realm of water and wastewater, plastic pipes have gained significant traction due to their ability to withstand extreme weather conditions and provide reliable infrastructure for potable water and wastewater disposal. These pipes are essential for infrastructure development in both the commercial and industrial sectors, ensuring the efficient transport of water and wastewater in various industries.

Moreover, plastic pipes play a crucial role in renewable energies, particularly in hydrogen networks and plastic cable protection. Their lightweight properties and non-reactive nature make them an ideal choice for these applications. In the water and wastewater sector, high-density polyethylene (HDPE) pipes have become a popular choice due to their durability and resistance to chemicals. HDPE pipes are extensively used in sewage systems and rainwater harvesting, making them a vital component of wastewater management and water infrastructure. The market also caters to the needs of various industries, including agriculture, chemicals, power generation, chemical processing, food processing, and building and construction.

Furthermore, the market is also influenced by the growing trend towards renewable energies and the need for reliable cable protection. The increasing adoption of hydrogen networks and the shift towards renewable energy sources is expected to drive demand for plastic pipes In these applications. Moreover, plastic pipes offer several environmental benefits, including the ability to be recycled and the use of bioplastics. Recycled plastics and bioplastics are gaining popularity due to their reduced environmental impact and sustainability.

|

Plastic Pipes Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

217 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.4% |

|

Market Growth 2024-2028 |

USD 23.57 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.3 |

|

Key countries |

China, US, India, Japan, Germany, UK, South Korea, Canada, Indonesia, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Plastic Pipes Market Research and Growth Report?

- CAGR of the Plastic Pipes industry during the forecast period

- Detailed information on factors that will drive the Plastic Pipes market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the plastic pipes market growth of industry companies

We can help! Our analysts can customize this plastic pipes market research report to meet your requirements.

RIA -

RIA -