Poland Prefabricated Buildings Market Size 2024-2028

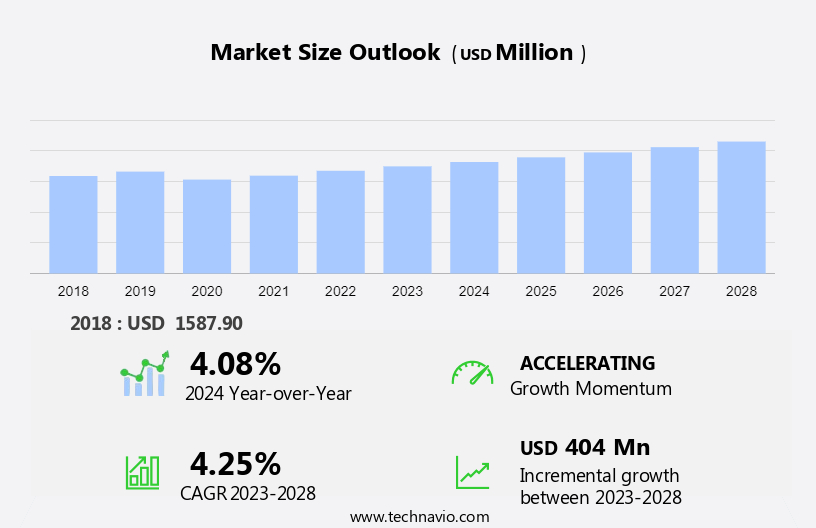

The Poland prefabricated buildings market size is forecasts to increase by USD 404 million growing at a CAGR of 4.25% between 2023 and 2028. Market market growth and trends is shaped by various factors, with notable impacts from shifting consumer preferences and economic considerations. The surge in demand for prefabricated houses in Poland underscores evolving housing trends and preferences, driving market expansion. Moreover, the cost savings associated with prefabricated buildings attract budget-conscious consumers, fostering demand and market growth. Additionally, the time efficiency offered by prefabricated methods accelerates project timelines, appealing to both developers and homeowners seeking faster occupancy. These combined factors propel the market forward, reflecting a convergence of economic incentives, technological advancements, and changing consumer needs. Understanding and adapting to these dynamics are essential for stakeholders to capitalize on emerging opportunities and navigate the evolving landscape of the prefabricated industry effectively.

What will be the Market Size During the Forecast Period?

Market Dynamics and Customer Landscape

In the realm of infrastructure investments, the market is experiencing significant growth due to modular construction and industrialization, key drivers of urbanization in developing nations. Government initiatives, such as business subsidies, and innovative construction methods, are fostering this trend. However, barriers to entry, including high upfront costs and time-consuming on-site procedures, persist. The market statistics indicate an economical solution to building operations in Poland, with prefabricated buildings offering reduced construction time and minimal waste, a crucial consideration in the context of environmental concerns. The negative environmental impact of traditional construction methods, including the generation of garbage from PVC and other materials, is a pressing issue. Green buildings, a contemporary approach, are gaining traction in Poland as a solution to these challenges. As emerging economies continue to urbanize, the market will remain a vital player in the industry. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

The rising demand for prefabricated houses in Poland is notably driving the market growth. The market is poised for growth, driven by increasing infrastructure investments, urbanization, and industrialization in developing nations. Modular construction, a key aspect of this market, is gaining popularity due to contemporary methods and the desire for convenience and security. Factors such as government initiatives, rising pay levels, and positive pricing trends are also contributing to this growth. However, barriers to entry include high upfront costs and building operations, as well as negative environmental perceptions. Market statistics indicate a shift towards innovative methods, such as combined systems and panel systems, which offer superior quality, quick production times, and adaptable designs.

Additionally, the use of green buildings, PVC, and public property subsidies is on the rise. The Canadian Minister of Parliament recently emphasized the importance of economical and efficient methods, further boosting the market. Despite challenges, such as waste and on-site procedures, the benefits of prefabricated buildings, including easy relocation and superior quality, make them an attractive option for businesses and residential sectors alike. Thus, such factors are expected to drive the growth of the market during the forecast period.

Significant Market Trend

Increasing demand for energy-efficient houses is an emerging trend in the market. The market is experiencing growth due to infrastructure investments and urbanization. Modular construction and industrialization are key drivers, with developing nations and government initiatives promoting their use. Prefabricated buildings are characterized by energy-efficient designs, including air-tightness, geothermal heat pumps (GHP), solar electric or photovoltaic (PV) systems, and passive solar design. Sustainable home features reduce waste and promote green buildings. Barriers to entry include building operations and costs, but innovative methods offer quick production times, simple services, and adaptable designs.

Emerging economies are expected to drive market statistics, with economic and easy relocation a significant advantage. Key components include PVC panels, cellular skeletons, and combined panel systems, offering superior quality and negative environmental benefits compared to traditional methods. Government subsidies and contemporary techniques, as discussed by the Canadian Minister in Parliament, are further boosting the market. Such factors are expected to contribute to the growth of the market during the forecast period.

Major Challenge Market

Rising labor cost in Poland is a major challenge impeding the market. In Poland, the sector is experiencing significant changes due to infrastructure investments and urbanization. The government has initiated various policies, including increasing the minimum wage by 15% and employer social insurance payments by 10%. These regulations have placed a heavier burden on smaller firms and self-employed persons. Prefabricated buildings and modular construction are gaining popularity as part of the industrialization trend. Developing nations, including Poland, are embracing innovative methods to meet the demands of contemporary methods. Barriers to entry for prefabricated buildings in Poland include high upfront costs and time-consuming on-site procedures. However, the benefits of using prefabricated buildings, such as quick production times, superior quality, and adaptable designs, outweigh the challenges. The Polish market for prefabricated buildings is growing, with emerging economies and market statistics showing an increase in demand. The construction industry is facing competition from other countries, such as Ukraine and Germany, which offer more profitable employment opportunities.

To remain competitive, businesses are turning to prefabricated buildings made of materials like PVC and green building systems. The Polish government is also offering subsidies to encourage the use of prefabricated buildings on public property. Despite the advantages of prefabricated buildings, challenges remain, including the negative environmental impact of construction waste and the need for simple services to support the industry. The Canadian Minister of Parliament recently discussed the potential of prefabricated buildings in the context of innovative construction and time and cost savings in building operations. The future of prefabricated buildings in Poland lies in the adoption of combined systems, such as skeleton, panel, and cellular systems, and the implementation of panel systems for quick and efficient production. Thus, such factors are expected to hinder the growth of the market during the forecast period.

Market Segmentation

By Material

The market share growth by the wood segment will be significant during the forecast period. The market in Poland is experiencing growth due to increasing infrastructure investments and urbanization. Modular construction, a key aspect of industrialization, is gaining popularity for its sustainability benefits. Developing nations and governments are initiating projects to promote green buildings, which are expected to drive the demand for prefabricated buildings. Wood, a primary material in prefabricated construction, offers numerous advantages. It is renewable, recyclable, and absorbs carbon dioxide. Industrialization of wood generates lower greenhouse gas emissions than other materials. Prefabricated buildings made of wood also require less energy for processing and have quick production times. Barriers to entry in the market include high upfront costs and on-site procedures.

Get a glance at the market contribution of the End User segment Request Free Sample

The wood segment was valued at USD 779 million in 2018. However, the benefits of contemporary construction, such as superior quality, adaptable designs, and easy relocation, outweigh these challenges. Government initiatives, such as subsidies for businesses and public property, are encouraging the adoption of prefabricated buildings. Market statistics indicate that the prefabricated buildings industry is growing, with emerging economies leading the way. The Canadian Minister of Infrastructure and Communities, speaking before Parliament, emphasized the importance of innovative methods in reducing time, costs, and building operations. The use of PVC and combined systems, such as panel and cellular systems, is becoming more common in prefabricated buildings due to their superior quality and simple services. Despite the advantages, there are concerns about the negative environmental impact of prefabricated buildings, particularly in terms of construction waste and the use of non-renewable materials. However, the trend towards green buildings and the use of renewable resources, such as wood, is expected to mitigate these concerns. In summary, the market in Poland is growing due to infrastructure investments, urbanization, and government initiatives. The use of renewable resources, such as wood, and innovative methods, such as panel systems, is driving the industry forward. However, concerns about construction waste and the use of non-renewable materials must be addressed to ensure the long-term sustainability of the industry. Hence, such factors are expected to drive the growth of the wood segment in the Poland market during the forecast period.

Who are the Major Market Companies?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Budizol Sp. z o.o. S.K.A.?????? - The company offers prefabricated buildings which are made with modern reinforced concrete and wooden parts.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

- ALHO Holding GmbH

- Unimex Group

- Berkeley Group

- Bouygues Construction SA

- CONTAINEX Container Handelsgesellschaft m.b.H.

- DFH Haus Gmbh

- Fertighaus WEISS GmbH

- ilke homes Ltd.

- KLEUSBERG GmbH and Co KG

- Laing O Rourke

- MABUDO Sp. z o.o

- Moelven Industrier ASA

- PEPEBE Wloclawek

- Prologis Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Segment Overview

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Million" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments.

- Material Outlook

- Wood

- Concrete

- Steel

- Others

- Type Outlook

- Permanent

- Relocatable

- Application Outlook

- Residential

- Commercial

- Industrial

You may also interested in below market reports:

-

Prefabricated Construction Market: Analysis APAC, Europe, North America, Middle East and Africa, South America - US, China, Japan, Germany, France - Size and Forecast

-

US Modular Construction Market: by Application and Type - Forecast and Analysis

-

Precast Concrete Market: Analysis APAC, Europe, North America, South America, Middle East and Africa - US, China, India, Germany, France - Size and Forecast

Market Analyst Overview

The market is experiencing significant growth, driven by factors such as government spending on sustainable infrastructure development and the demand for energy-efficient houses in urban areas. As a developing economy with rapid population growth, Poland is increasingly adopting modular systems and sustainable construction processes to meet housing demands efficiently. Prefabricated construction modules, including lightweight ceramic houses and customized prefabricated wooden structures, are gaining popularity due to their cost-effectiveness and swift construction timelines. This trend is supported by advancements in modular construction technology, which ensure quality control and reduce on-site labor shortages.

Moreover, key technological trends include the use of ground source heat pumps and photovoltaic systems in passive solar structures, enhancing energy efficiency and reducing overall energy consumption. The market landscape depends on Residential prefabricated construction, Lockdowns, Non-residential prefabricated construction, and Other non-residential prefabricated construction. The market also benefits from the integration of smart construction technologies and smart robots, which streamline production processes and enhance productivity in factory-like settings. Despite challenges such as material costs and the need for heavy machinery, the market in Poland offers high-end, customized solutions for residential and non-residential applications. Infrastructural reforms and advanced prefabricated technologies continue to drive the sector forward, catering to diverse needs from affordable housing to commercial real estate and hospitality projects.

The market faces challenges such as a lack of awareness, high initial investments, and the requirement for heavy and sophisticated machines. The market landscape depends on the Contractors, Construction companies, Quarantine sectors, Turnkey housing solutions, Developing economies, Prefabricated constructions, Prefabricated panels, Factory-like setting, Construction site, Non-residential buildings, Environmentally friendly construction method, Site disturbance, Affordable construction, Weather control, Supervision control. However, advancements in supply chain integration and the availability of interior turnkey solutions are enhancing efficiency. This sector appeals to private housing developers, startups, and collaborative workplaces in developing cities, despite space limitations. Various construction systems like cellular, panel, large slab components, skeleton, and combined systems cater to diverse needs in residential and non-residential prefabricated construction. These solutions offer flexibility and durability, addressing the growing demand for efficient and sustainable building methods in Poland's evolving real estate landscape.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

137 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.25% |

|

Market growth 2024-2028 |

USD 404 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.08 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ALHO Holding GmbH, Berkeley Group, Bouygues Construction SA, Budizol Sp. z o.o. S.K.A., CONTAINEX Container Handelsgesellschaft m.b.H., DFH Haus Gmbh, Fertighaus WEISS GmbH, ilke homes Ltd., KLEUSBERG GmbH and Co KG, Laing O Rourke, MABUDO Sp. z o.o, Moelven Industrier ASA, PEPEBE Wloclawek, Prologis Inc., Segezha Group, Skanska AB, Styrobud Gorno, thomas participations GmbH, UNIHOUSE SA, and Unimex Group |

|

Market dynamics |

Parent market analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for market forecast period. |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting of the market between 2024 and 2028

- Precise estimation of the size of the market size and its contribution to the parent market

- Accurate predictions about upcoming market trends and analysis and changes in consumer behavior

- Growth of the market industry across Poland

- Thorough market growth analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive market analysis and report on the factors that will challenge the market research and growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -