Post Quantum Cryptography Market Size 2026-2030

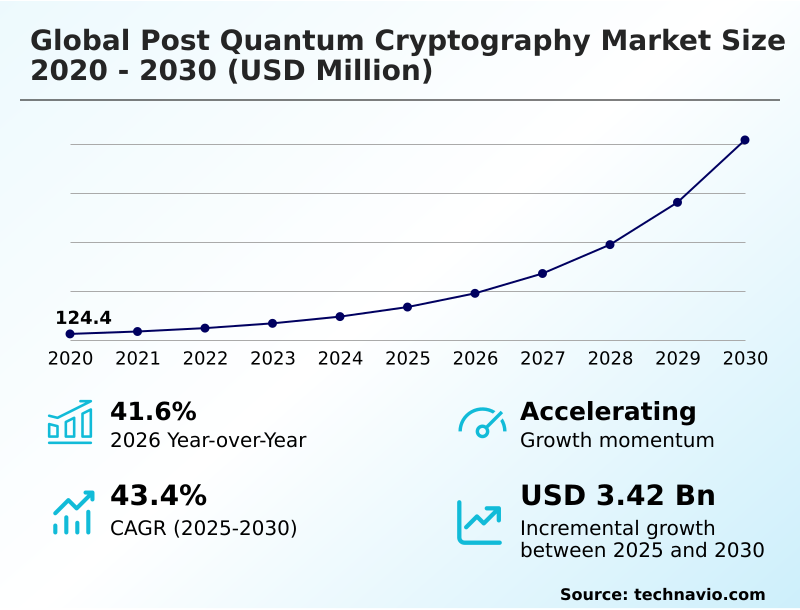

The post quantum cryptography market size is valued to increase by USD 3.42 billion, at a CAGR of 43.4% from 2025 to 2030. Escalating threat of quantum computing will drive the post quantum cryptography market.

Major Market Trends & Insights

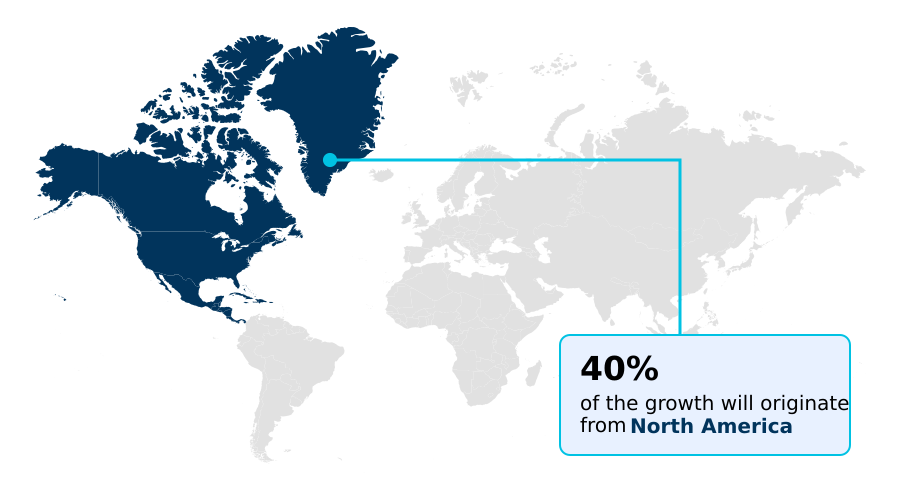

- North America dominated the market and accounted for a 40.3% growth during the forecast period.

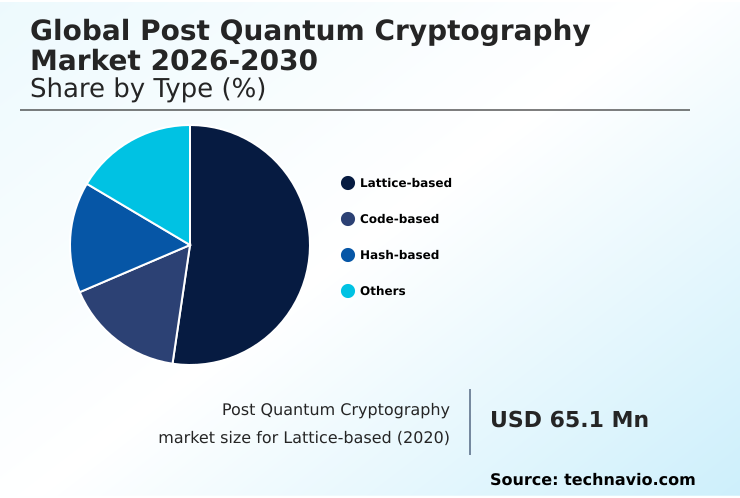

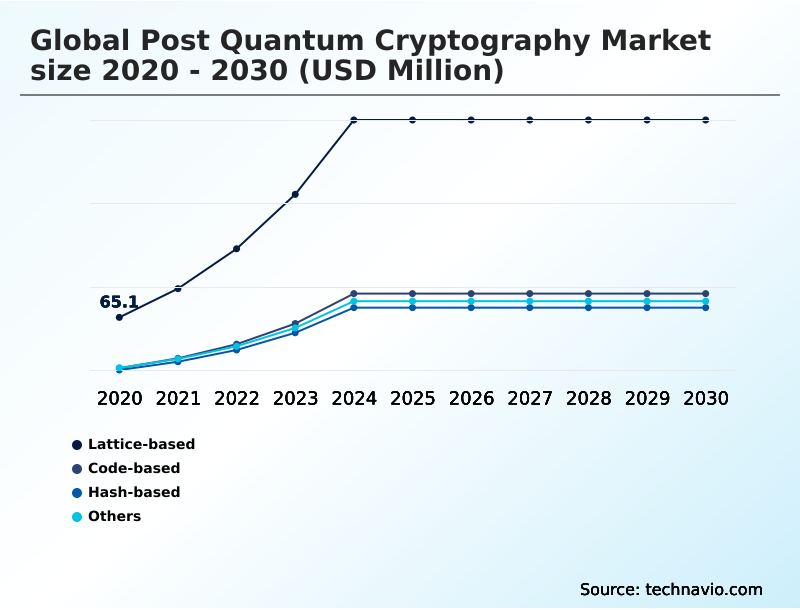

- By Type - Lattice-based segment was valued at USD 239.5 million in 2024

- By Component - Software segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.97 billion

- Market Future Opportunities: USD 3.42 billion

- CAGR from 2025 to 2030 : 43.4%

Market Summary

- The post quantum cryptography market is defined by the urgent need to develop and deploy new cryptographic systems secure against the threat posed by quantum computers. Current public key encryption standards are vulnerable to attacks from a cryptographically relevant quantum computer, rendering vast amounts of secured data insecure.

- This has catalyzed a global effort, led by bodies overseeing NIST PQC standardization, to develop quantum-resistant algorithms based on diverse mathematical problems, including lattice-based cryptography, code-based cryptography, and hash-based signatures. The primary driver is the need for long-term data security, particularly for sectors with sensitive information like government, finance, and healthcare, who face the 'harvest now, decrypt later' threat.

- A key trend is the move toward crypto-agility, enabling systems to transition to new cryptographic primitives without complete overhauls. For instance, a financial institution must plan a PQC migration strategy to protect decades of transaction archives, which involves integrating standardized PQC algorithms into legacy systems while managing performance overhead.

- This transition is complex, necessitating significant investment in PQC implementation services and skilled personnel to ensure a secure digital future. The adoption of a hybrid cryptographic approach often serves as an interim solution.

What will be the Size of the Post Quantum Cryptography Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Post Quantum Cryptography Market Segmented?

The post quantum cryptography industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Lattice-based

- Code-based

- Hash-based

- Others

- Component

- Software

- Services

- Hardware

- Application

- Network security

- Cloud security

- Application security

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Type Insights

The lattice-based segment is estimated to witness significant growth during the forecast period.

The market is segmented by type, component, application, and geography. Within the type segment, lattice-based cryptography has emerged as a foundational technology due to its robust security and efficiency.

These quantum-resistant algorithms, built on computationally hard lattice problems, offer a strong balance of performance and protection against the quantum computing threat. This makes them suitable for diverse cryptographic primitives, including key encapsulation mechanism and digital signatures.

The NIST PQC standardization process has further solidified their prominence, selecting specific lattice-based schemes for widespread adoption. This endorsement has driven integration into secure boot process and transport layer security protocols.

Implementations have demonstrated that while some performance overhead exists, optimizations can mitigate impact, with certain PQC-enabled hardware showing only a 15% increase in power consumption during intensive operations, a manageable trade-off for achieving forward secrecy.

This underpins the importance of crypto-agility.

The Lattice-based segment was valued at USD 239.5 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Post Quantum Cryptography Market Demand is Rising in North America Get Free Sample

The geographic landscape of the post quantum cryptography market is led by North America, which accounts for over 40% of the incremental growth, driven by US-led NIST PQC standardization efforts and substantial investment in quantum-safe VPN and cloud security with PQC.

This region is home to key vendors developing PQC hardware accelerators and quantum-resistant libraries. Europe is also a significant market, focusing on digital sovereignty and collaborative research into a crypto-agility framework.

The APAC region is experiencing the fastest growth, with a CAGR of 44.3%, propelled by major investments from China, Japan, and South Korea in developing indigenous quantum-resistant authentication and securing network security protocols.

These nations see post-quantum key exchange and quantum-proof encryption as vital for economic and national security, fostering a competitive environment for innovation in PQC algorithm selection.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the transition to post-quantum cryptography requires a detailed strategic roadmap, as migrating legacy systems to PQC is a complex undertaking with significant operational implications. A primary concern is the performance impact of PQC on networks, as some quantum-resistant algorithms have larger key and signature sizes compared to their classical counterparts.

- This necessitates a thorough cost analysis of PQC migration projects to balance security with efficiency. Comparing lattice-based and code-based PQC schemes reveals trade-offs in performance and key size, influencing their suitability for different applications. The challenges of PQC adoption in enterprises are further compounded by the existing talent gap in post-quantum cryptography expertise, making external support essential.

- Organizations are increasingly adopting a hybrid approach for PQC transition, which allows for gradual integration and mitigates risks associated with new PQC algorithms. This strategy is critical for PQC for securing IoT and OT environments, where resource constraints demand careful planning.

- The role of NIST in PQC standardization provides a crucial foundation, but developing a PQC crypto-agility roadmap is the responsibility of each organization. This roadmap must address quantum-safe digital identity management and the integration of PQC with existing security ecosystems.

- Ultimately, securing long-term data archives with PQC is paramount to counter the threat of Shor's algorithm to RSA and ensure PQC compliance and regulatory mandates.

What are the key market drivers leading to the rise in the adoption of Post Quantum Cryptography Industry?

- The escalating threat that quantum computing poses to current encryption standards is the foremost driver of market growth.

- The primary driver is the escalating quantum computing threat, which renders current public key encryption vulnerable and necessitates a shift to quantum-resistant algorithms.

- This has created an urgent need for long-term data security to counter the 'harvest now, decrypt later' scenario, where adversaries store encrypted data to decrypt later with a cryptographically relevant quantum computer.

- In response, government initiatives and the NIST PQC standardization process are providing a clear roadmap for adoption, fueling investment in PQC for critical infrastructure and financial services.

- This top-down push for quantum-proof encryption de-risks the migration process for enterprises, which are now actively pursuing PQC migration strategy development and quantum risk assessment to safeguard data that requires protection for decades.

What are the market trends shaping the Post Quantum Cryptography Industry?

- The accelerated pace of standardization efforts, coupled with the increasing issuance of government mandates for adoption, is a prominent trend shaping the market's trajectory.

- Key trends are reshaping the market, led by accelerated government mandates and the finalization of standardized PQC algorithms. This clarity is driving a pragmatic shift toward the adoption of a hybrid cryptographic approach, blending classical algorithms with new quantum-resistant libraries to ensure a secure transition.

- This layered strategy mitigates risks associated with the relative novelty of post quantum key exchange protocols. Another significant trend is the seamless integration of PQC for IoT devices into existing ecosystems, with vendors embedding quantum-safe VPN capabilities and quantum-resistant authentication directly into hardware.

- This approach simplifies crypto-agility, but a skills gap remains a hurdle, with less than 5% of professionals feeling prepared for PQC implementation services.

What challenges does the Post Quantum Cryptography Industry face during its growth?

- The inherent complexity and substantial cost associated with migrating existing infrastructures represent a significant challenge to market adoption.

- Significant challenges temper the pace of adoption, primarily the complexity and cost of a full PQC migration strategy. Transitioning from legacy systems requires a complete inventory of all cryptographic primitives and extensive testing, a daunting task for large organizations.

- The PQC performance overhead is another concern; some quantum-resistant algorithms demand more resources, with benchmark studies showing that certain implementations can increase power consumption by 15% in embedded systems, impacting PQC for IoT devices.

- Furthermore, a severe talent shortage, with less than 5% of cybersecurity professionals feeling fully prepared, complicates PQC algorithm selection and deployment, increasing reliance on specialized PQC implementation services to achieve a secure and efficient transition.

Exclusive Technavio Analysis on Customer Landscape

The post quantum cryptography market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the post quantum cryptography market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Post Quantum Cryptography Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, post quantum cryptography market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Expertise is demonstrated through advanced, quantum-resistant key management and data encryption services integrated within a scalable cloud environment, ensuring long-term information security.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Cisco Systems Inc.

- Cloudflare Inc.

- Google Cloud

- IDEMIA France SAS

- Infineon Technologies AG

- Intel Corp.

- IBM Corp.

- Microsoft Corp.

- NEC Corp.

- NXP Semiconductors NV

- Palo Alto Networks Inc.

- Qualcomm Inc.

- Quantinuum Ltd.

- STMicroelectronics NV

- Thales Group

- Toshiba Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Post quantum cryptography market

- In August 2024, the United States Cybersecurity and Infrastructure Security Agency (CISA) issued a directive requiring federal agencies to develop and begin implementing plans for migrating to post-quantum cryptography.

- In September 2024, a major web browser provider updated its experimental features to include an option for hybrid Transport Layer Security (TLS) connections, combining X25519 with CRYSTALS-Kyber for key exchange.

- In October 2024, a prominent enterprise identity and access management (IAM) company announced that its next-generation platform would natively support quantum-resistant authentication protocols.

- In May 2025, a major operating system developer announced the planned integration of the SPHINCS+ signature scheme for securing future software updates, ensuring the integrity of distributed code.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Post Quantum Cryptography Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 43.4% |

| Market growth 2026-2030 | USD 3417.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 41.6% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The post quantum cryptography market is rapidly maturing from theoretical research into practical deployment, driven by the existential quantum computing threat to modern public key encryption. The industry-wide shift toward adopting quantum-resistant algorithms is now a strategic imperative. This transition involves more than just swapping cryptographic primitives; it requires a deep commitment to crypto-agility and a redesign of security architectures.

- Boardroom decisions are increasingly focused on risk mitigation strategies, such as adopting hybrid cryptography, which blends classical and post-quantum methods to ensure a seamless security posture during the multi-year migration. Key technologies like lattice-based cryptography and hash-based signatures, now part of the NIST PQC standardization, are being integrated into key exchange protocols and digital signatures.

- However, performance remains a key consideration, with some hardware security modules experiencing up to a 15% increase in power consumption, influencing hardware selection for secure boot process and firmware signing.

- The goal is to achieve forward secrecy without compromising operational efficiency, a challenge that requires careful planning to guard against both side-channel attacks and future quantum threats from a cryptographically relevant quantum computer.

What are the Key Data Covered in this Post Quantum Cryptography Market Research and Growth Report?

-

What is the expected growth of the Post Quantum Cryptography Market between 2026 and 2030?

-

USD 3.42 billion, at a CAGR of 43.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Lattice-based, Code-based, Hash-based, and Others), Component (Software, Services, and Hardware), Application (Network security, Cloud security, Application security, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating threat of quantum computing, Migration complexity and cost

-

-

Who are the major players in the Post Quantum Cryptography Market?

-

Amazon.com Inc., Cisco Systems Inc., Cloudflare Inc., Google Cloud, IDEMIA France SAS, Infineon Technologies AG, Intel Corp., IBM Corp., Microsoft Corp., NEC Corp., NXP Semiconductors NV, Palo Alto Networks Inc., Qualcomm Inc., Quantinuum Ltd., STMicroelectronics NV, Thales Group and Toshiba Corp.

-

Market Research Insights

- The market's dynamics are shaped by a strategic push toward quantum-safe communication, driven by the need to secure critical infrastructure and ensure long-term data security. Organizations are actively pursuing a PQC migration strategy, balancing the adoption of standardized PQC algorithms with practical implementation challenges.

- This transition is not without friction; benchmark studies show that some PQC hardware accelerators can lead to a 15% increase in power consumption in embedded systems, a key consideration for PQC for IoT devices.

- Furthermore, a significant talent gap persists, with less than 5% of cybersecurity professionals feeling fully equipped to manage a migration, highlighting the critical need for PQC implementation services and quantum risk assessment. The adoption of a hybrid cryptographic approach offers a pragmatic path forward, allowing for a phased transition while providing robust security.

We can help! Our analysts can customize this post quantum cryptography market research report to meet your requirements.

RIA -

RIA -