Premium Chocolate Market Size 2024-2028

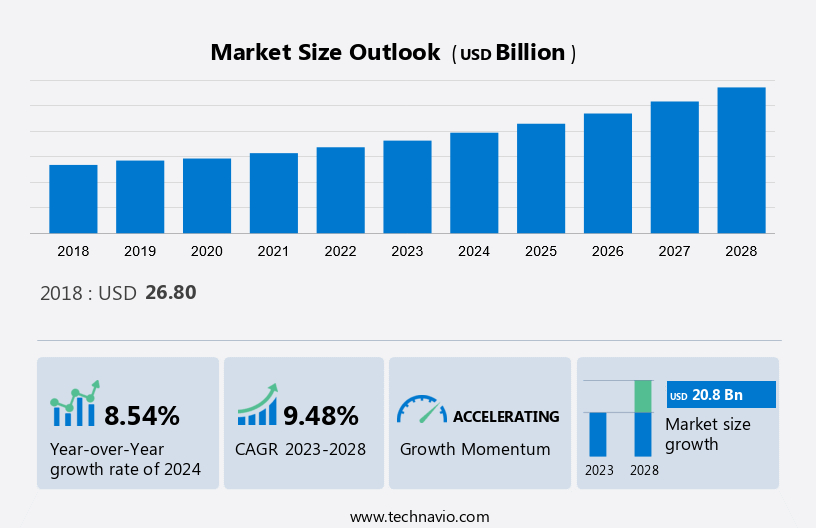

The Premium Chocolate Market size is forecast to increase by USD 20.8 billion, at a CAGR of 9.48% between 2023 and 2028. Market expansion hinges on various factors, notably the introduction of new products, heightened consumer engagement in the market, and the implementation of marketing strategies. New product launches inject innovation into the market, attracting consumer interest and driving demand for novel offerings. Additionally, increasing market indulgence, characterized by consumer willingness to explore diverse products and experiences, fosters market growth by expanding the consumer base and driving sales volume. The market thrives on exquisite ingredients like high-quality cocoa, gourmet salt, and luxurious packaging, elevating the consumer experience. With additional flavors such as almonds and raspberry pieces, brands like Purdys Chocolatier and Cadbury offer a range of indulgent options. Furthermore, effective marketing strategies play a pivotal role in creating brand awareness, communicating product benefits, and influencing consumer purchasing decisions. By leveraging innovative marketing approaches, businesses can enhance brand visibility, establish a stronger market presence, and capitalize on emerging opportunities for growth. Together, these factors contribute to the dynamic expansion of the market, shaping its trajectory and fostering competitiveness within the industry.

What will be the Size of the Market During the Forecast Period?

To learn more about this report, View Report Sample

Market Segmentation

Products like Lindor truffles and Guylian exemplify the richness and an upscale appearance, catering to discerning tastes with low sugar. Rising concerns for quality and taste drive product innovation and the creation of limited-edition chocolates, ensuring a premium offering in the chocolate confectionery landscape.

By Distribution Channel

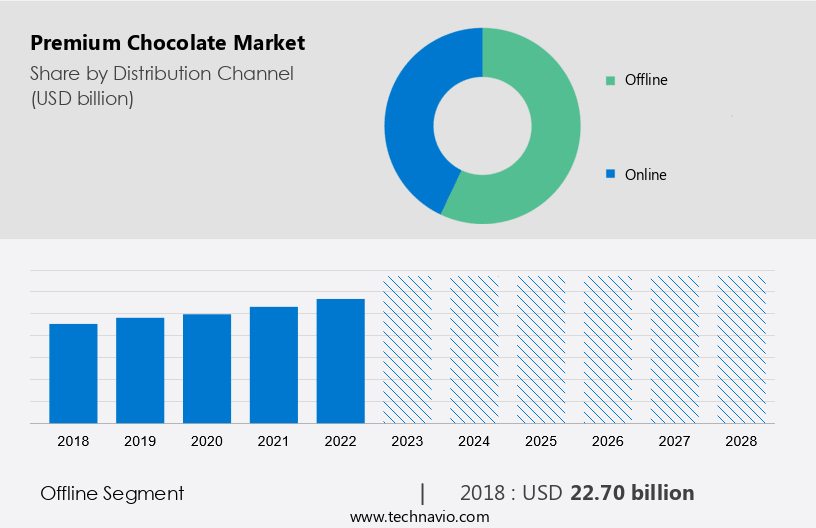

The market share by the offline segment will be significant during the forecast period. Offline sales channels include supermarket, hypermarkets, department stores, convenience stores, distributors, independent retailers, and specialty retailers. Popular supermarkets offering products include SPAR, Walmart, Meijer Inc., The Kroger Co. (Kroger), Carrefour, and Big Bazaar. Supermarkets and hypermarkets offer a wide variety of products from different brands, and consumers can easily select and purchase the desired product from these stores.

Get a glance at the market contribution of various segments View the PDF Sample

The offline segment was valued at USD 22.70 billion in 2018. Offline distribution channels such as supermarkets and hypermarket chains are focusing on expanding the number of stores around the world. Walmart, for example, has announced plans to open 300 new stores in China by 2024 as part of its global expansion policy. Such expansion of supermarket and hypermarket chains will improve customer access and increase sales of such products, driving the growth of the market during the forecast period.

By Region

For more insights on the market share of various regions Download PDF Sample now!

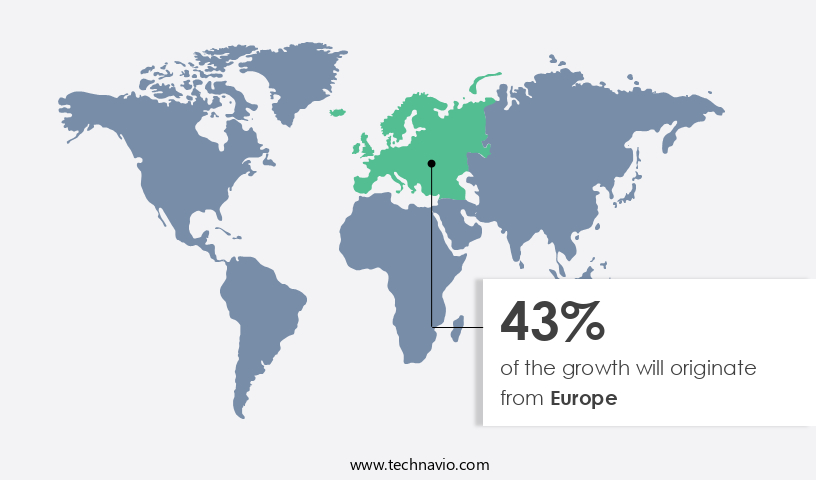

Europe is estimated to contribute 43% to the growth of the market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. In 2022, Europe had the highest per capita consumption of chocolate in the world. Consumers tend to prefer premium chocolates as they are popular as gifts for special occasions. Additionally, many chocolate manufacturers, such as Ferrero International SA, have their headquarters in the region. These factors are one of the main reasons why Europe holds the dominant share of the market. In Europe, demand is outpacing sales of private-label chocolate. This is mainly because consumers are willing to pay higher prices for higher quality, better packaging, and richer flavor than other chocolates. The UK, Belgium, Germany, and Switzerland are among the leading markets in Europe. Hence, such factors are driving the market in Europe during the forecast period.

Market Dynamics and Customer Landscape

In the market, consumers savor indulgent treats crafted from the finest ingredients like cocoa butter and premium cocoa, ensuring premium product with superior taste and texture for breakfast cereal like cookie dough. From classic favorites like chocolate bars to unique offerings such as Limited-edition chocolate and White chocolates, brands focuses on gourmet chocolates with premium textured and flavors like Berry Crunch. With meticulous attention to detail, these chocolates promise a luxurious experience that delights the senses and satisfies the most discerning palates. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

The increasing market indulgence is notably driving market growth. Chocolate consumption is associated with emotional aspects such as indulgence and enjoyment. The demand and popularity of this segment are growing rapidly with increasing knowledge and interest in unique and high-quality products. Moreover, the demand for higher-quality chocolate, including truffle chocolates, is growing faster than for other types of chocolate. With the increasing popularity of high-quality, the number of product launches in this category is increasing.

Further, the demand for chocolate with premium ingredients and labels is growing in almost every region of the world. France, England, Italy, Spain, and Germany are some of the countries with the highest demand. Consumers in these countries are willing to pay more for luxury goods. Most consumers buy premium chocolates as gifts. However, the purchase rate for personal use is also increasing. The love for these chocolates is growing more and more and is expected to grow even more in the future. Hence, such factors are driving the market during the forecast period.

Significant Market Trends

Support for sustainable cocoa production is a key trend influencing market growth. Ivory Coast and Ghana are the world's largest exporters of raw cocoa, accounting for around 60% of global exports in 2022. Cocoa is a major contributor to export earnings and is the main source of income for up to six million farmers in Côte d'Ivory and Ghana. At the same time, cocoa production faces challenges related to child labor, low incomes for local farmers, deforestation, and forest degradation. Cocoa growers and suppliers in African countries such as Côte d'Ivoire and Ghana are forced to sell their harvest of cocoa beans to middlemen who distort prices. In addition, several reports of child slavery have surfaced, pointing to farmers' plight and working conditions. To solve these problems, many major players have started to take initiatives by introducing sustainable cocoa production programs.

For example, the European Commission launched an initiative for more sustainable cocoa production. The actions taken by the European Commission are in line with the Commission's political priorities under the Green Deal and the Commission's 'zero tolerance' approach to child labor. It also builds on its June 2019 joint initiative in Côte d'Ivoire and Ghana on the lowest price of cocoa on the market. Such actions support the idea of sustainable cocoa production and boost the growth of the market during the forecast period.

Major Market Challenge

The threat from seasonal chocolates is challenging market growth. Seasonal chocolates are made for special occasions and are not available all year round. As such, seasonal chocolate purchases increase exponentially around the world during festivals and occasions such as Easter, Halloween, and Christmas. Easter is the perfect time to encourage seasonal chocolate purchases. Consumers buy seasonal chocolates for different seasonal occasions as gifts or to complement larger gifts for friends and family during festivals and holidays. Offering seasonal chocolates in a variety of price points, they serve as consumer impulse purchases and emergency or unscheduled gifts. Due to the rapid rise in the popularity of seasonal chocolates, players are benefiting from special holiday consumption.

For example, on White Day in Japan, men are encouraged to buy white chocolate for women. Players like Lindt and Lake Champlain Chocolates sell seasonal chocolates designed specifically for special occasions such as Mother's Day and Father's Day. Players such as Godiva, Gayle's Chocolates, and Zoe's Chocolate have dedicated Thanksgiving product lines that are very popular in regions such as North America and Europe. These special days offer simple gift options that don't confuse consumers' likes and dislikes, thus increasing overall sales of seasonal chocolates. Therefore, the threat of seasonal chocolates will impede the growth of the market during the forecast period.

Market Customer Landscape

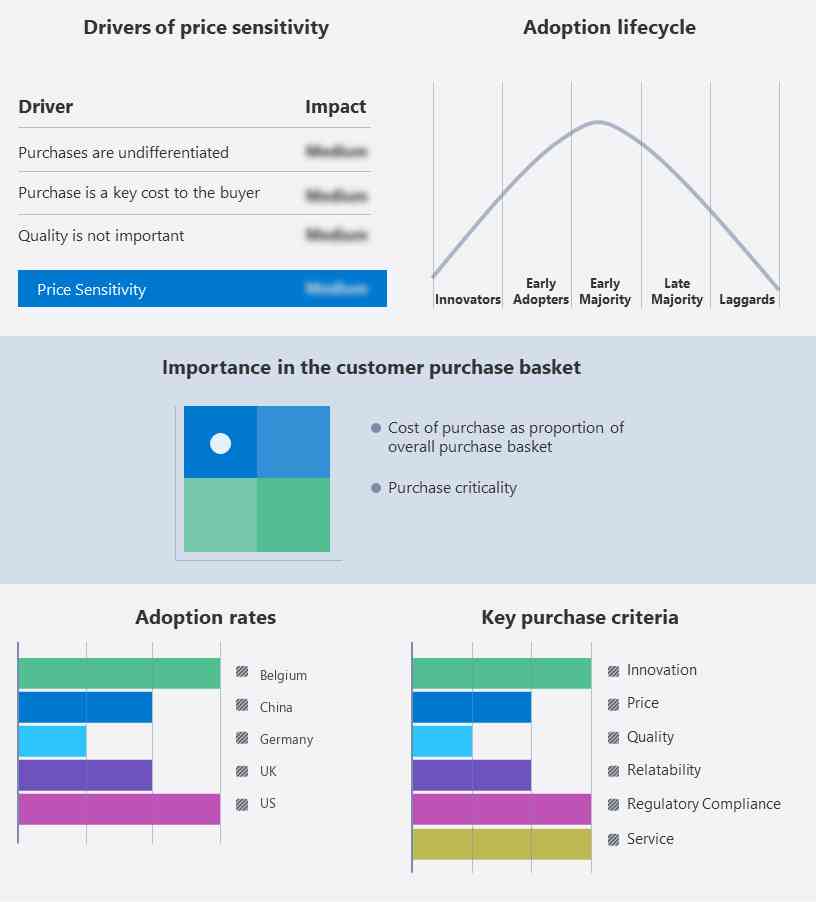

The report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Market Customer Landscape

Who are the Major Market Players?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Cargill Inc: The company offers different types of chocolate products such as milk chocolate, dark chocolate, white chocolate, and many more.

The report also includes detailed analyses of the competitive landscape of the market and information about 17 market companies, including:

- CEMOI Group

- Champlain Chocolate Co.

- Chocoladefabriken Lindt and Sprungli AG

- Ferrero International S.A.

- Hotel Chocolat Group plc

- Lotte Corp.

- Marks and Spencer Plc

- Mars Inc.

- Meiji Holdings Co. Ltd.

- Mondelez International Inc.

- Nestle SA

- Neuhaus NV

- Pierre Marcolini Group

- RICHART

- Savencia SA

- Teuscher Chocolates of Switzerland

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Segment Overview

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments.

- Distribution Channel Outlook

- Offline

- Online

- Product Outlook

- Dark premium chocolate

- White milk premium chocolate

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Brazil

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

Market Analyst Overview

In the realm of indulgence, premium chocolate stands out for its fusion of innovative flavors and luxury appeal. With a focus on healthier foods and lifestyle requirements, consumers are seeking out chocolates with advanced and cutting-edge fillings, such as crunchy hazelnuts and smooth materials, offering both texture and taste. Brands like ChoViva are gaining traction for their commitment to Fairtrade practices and transparent sourcing, resonating with chocolate aficionados who prioritize quality cocoa. The market experiences seasonal demand, especially during major holidays, where unique gift boxes filled with bitesized chocolates become sought-after items. To maintain a competitive edge, retailers are exploring unusual ingredients and irregular flavors, catering to the diverse consumer tastes of the millennial generation and beyond.

Further, in the market, connoisseurs seek more than just indulgence; they crave an experience. From luxury chocolate adorned in unique shapes to fine chocolates with creamy fillings, Milk, every aspect is meticulously crafted for the highest quality. Innovations like honey-infused, espresso-infused, and peanut butter-filled chocolates cater to diverse consumer habits. These treats aren't just delicious; they boast medical advantages due to their antioxidants and minerals content. However, moderation is key, as over intake may lead to chronic illnesses. With an eye on health, brands are incorporating cereals, grains, and blueberry or pomegranate infusions. Available at select retail outlets and even airport merchants, premium chocolates are made from cocoa rich and ordinary beans, transformed into delectable delights packaged in exquisite chocolate boxes.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.48% |

|

Market growth 2024-2028 |

USD 20.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.54 |

|

Regional analysis |

Europe, North America, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

Europe at 43% |

|

Key countries |

US, Germany, China, UK, and Belgium |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Cargill Inc., CEMOI Group, Champlain Chocolate Co., Chocoladefabriken Lindt and Sprungli AG, Ferrero International S.A., Hotel Chocolat, Lotte Corp., Marks and Spencer Group plc, Mars Inc., Meiji Holdings Co. Ltd., Mondelez International Inc., Nestle SA, Neuhaus NV, Pierre Marcolini Group, RICHART, Savencia SA, Teuscher Chocolates of Switzerland, The Hershey Co., Vosges Haut Chocolat Ltd., and Yildiz Holding AS |

|

Market dynamics |

Parent market analysis, Market forecasting, market report, market forecast, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting of the market between 2023 and 2028.

- Precise estimation of the market size and its contribution to the parent market

- Accurate predictions about upcoming market trends and analysis and changes in consumer behavior

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough market growth analysis of the market's competitive landscape and detailed information about companies

- Comprehensive market analysis and report on the factors that will challenge the market research and growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -