Printed Carton Market Size 2024-2028

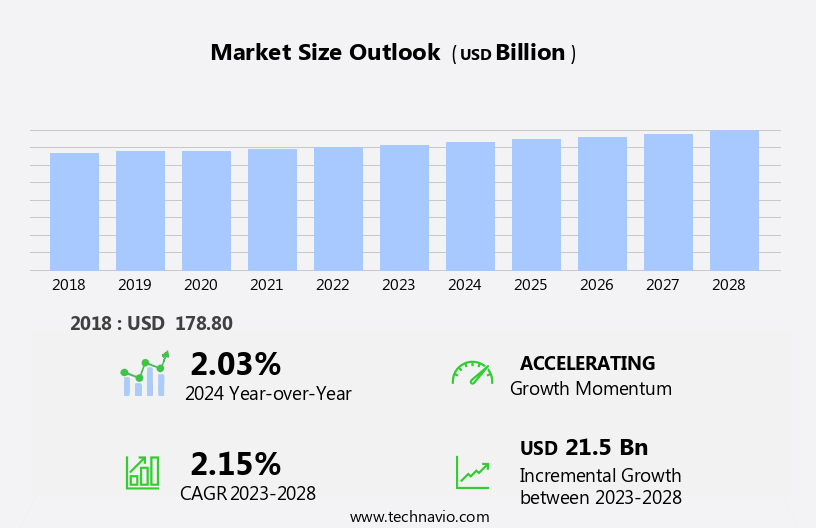

The printed carton market size is forecast to increase by USD 21.5 billion at a CAGR of 2.15% between 2023 and 2028.

- The market is experiencing significant growth, driven primarily by the expansion of organized retail and the increasing preference for eco-friendly packaging solutions. The organized retail sector's continuous expansion in both developed and emerging economies is fueling the demand for high-quality printed cartons. Additionally, the shift towards sustainable packaging solutions, including the use of eco-friendly inks, is gaining traction among consumers and manufacturers alike. However, the market is not without challenges. Regulations pertaining to the use of printed cartons, particularly those related to sustainability and food safety, are becoming increasingly stringent. Companies must ensure compliance with these regulations to maintain market presence and avoid potential penalties.

- To capitalize on the market opportunities and navigate these challenges effectively, businesses must stay informed of the latest trends and regulations and invest in innovative technologies and sustainable practices. By doing so, they can differentiate themselves from competitors and meet the evolving demands of consumers and regulatory bodies.

What will be the Size of the Printed Carton Market during the forecast period?

- The market in the United States is a dynamic and expansive industry, encompassing various sectors such as cosmetics, healthcare products, food, and homecare. Market growth is driven by factors including the increasing demand for sustainable and eco-friendly packaging solutions, the rise of e-commerce, and the ongoing trend towards personalized branding. Technologies like lithography, flexography, and digital printing are used to produce high-quality cartons for various substrates, including corrugated board, kraft board, and containerboard. Initial investments in setting up printing facilities can be substantial, but the potential for cost savings through economies of scale and the ability to cater to diverse industries make it an attractive investment.

- Products ranging from household essentials and electronics to spices and soups are all packaged in cartons, making this market a significant player in the packaging industry. Recycled materials are increasingly being used to reduce environmental impact, further fueling market growth.

How is this Printed Carton Industry segmented?

The printed carton industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Food and beverage

- Personal care and household

- Healthcare

- Others

- Product

- Corrugated carton

- Folding carton

- Geography

- APAC

- China

- India

- North America

- US

- Europe

- Germany

- UK

- South America

- Middle East and Africa

- APAC

By End-user Insights

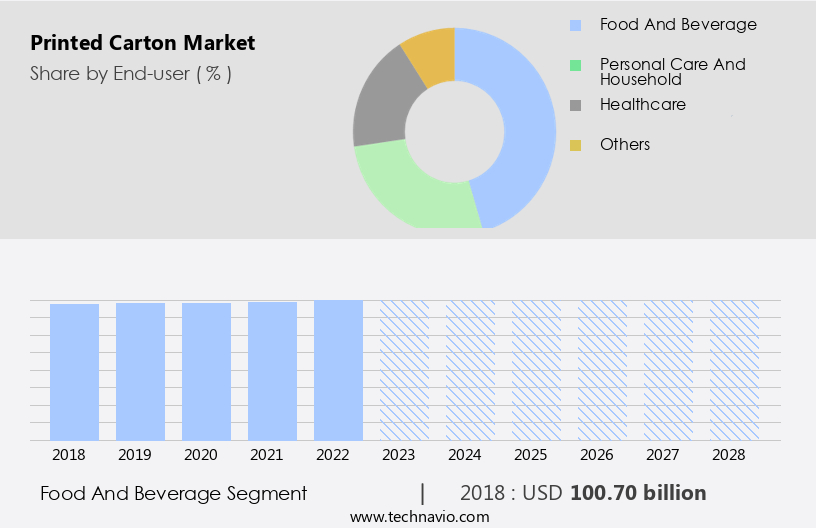

The food and beverage segment is estimated to witness significant growth during the forecast period.

The market is primarily driven by the food and beverage industry, which accounts for the largest market share. The increasing consumption of packaged food and beverages, including soups, cosmetics, electronics, spices, beverages, dairy products, and pharmaceuticals, is fueling the demand for printed cartons. Rigidity, moisture resistance, and shock resistance are essential features that make printed cartons an ideal choice for packaging these products. Printed cartons are used for various applications such as cereals, dry food, frozen food, candies and confectionery items, dairy products, refrigerated meat, wine, juices, beer, carbonated soft drinks, non-carbonated specialty beverages, and household essentials.

The changing consumer lifestyles and dietary preferences are leading to a rise in the demand for convenience and sustainability in packaging. Manufacturers are adopting advanced printing technologies like lithography, Flexography, and digital printing to enhance the identification and branding of their products. Sustainability is a crucial factor in the printing carton industry, with a focus on minimizing wastes and using recycled materials. The overall processed food industry's population base and natural supply of raw materials also contribute to the market's growth. Despite the environmental benefits of recyclable packaging, disposal methods, such as landfill activities, remain a concern for the industry.

The initial investments and operational costs associated with setting up printing facilities and the availability of alternative packaging solutions like plastic and glass containers are other challenges. However, the aseptic value and overall cost-effectiveness of printed cartons make them a preferred choice for many industries.

Get a glance at the market report of share of various segments Request Free Sample

The Food and beverage segment was valued at USD 100.70 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

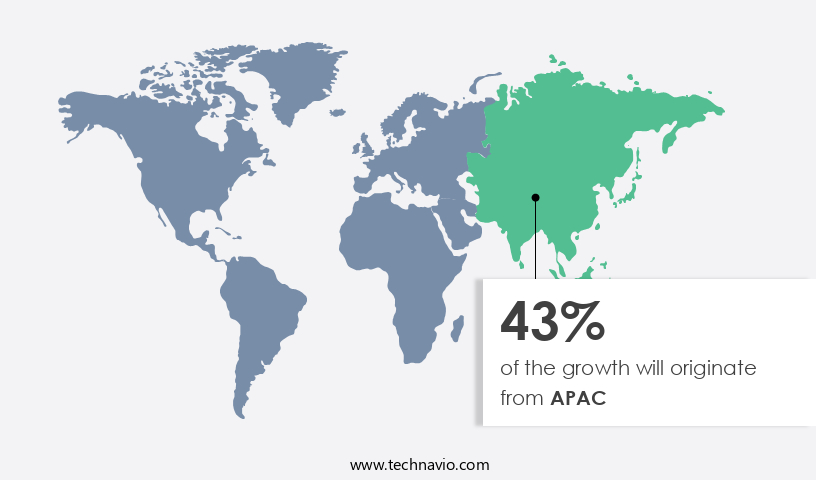

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market is driven by the increasing demand for efficient, shock-resistant, and moisture-resistant packaging solutions across various industries. Cosmetics, electronics, pharmaceuticals, homecare, and food sectors are significant contributors to the market's growth. APAC is expected to dominate the market due to its large population base and rising consumption of packaged foods, personal care products, and electronics. China, as a leading consumer in APAC, significantly influences market growth. The food industry, particularly in APAC, is a major consumer of printed cartons due to the increasing urbanization and changing consumer lifestyles. For instance, India's population grew from 1.353 billion in 2018 to 1.42 billion in 2022, leading to increased demand for various consumer goods.

Sustainability and minimizing wastes are key trends in the market, with an emphasis on recyclable packaging made from raw materials like kraft board, coated paper, and containerboard. Printing technologies like lithography, flexography, and digital printing are utilized to create branding and identification on these substrates. Initial investments in setting up printing facilities and operational costs are factors influencing product cost. The disposal method of printed cartons, either through landfill activities or combustion, is a concern for environmental sustainability.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Printed Carton Industry?

- Growth in organized retail is the key driver of the market.

- The organized retail sector, characterized by a large corporate entity managing a chain of retail stores, dominates retail sales in countries like the US, UK, and Canada. In this market, packaged products play a significant role. The US is currently the frontrunner in the global organized retail sector, with prominent players such as Walmart Inc., Costco Wholesale Corporation, Kroger Co., Home Depot Product Authority, LLC, Target Brands, Inc., and Amazon.Com. These companies have expanded their reach to emerging markets in Asia, the Middle East, and South America, contributing to the market's growth.

- The packaged goods sector benefits from this expansion as it caters to the increasing demand for convenience and consistency in developing economies. Organized retail's influence on the packaged products market is substantial, ensuring a steady demand for printed cartons as an essential component of product packaging.

What are the market trends shaping the Printed Carton Industry?

- Rising number of eco-friendly inks is the upcoming market trend.

- The packaging market is witnessing a shift towards eco-friendly solutions, with companies focusing on reducing carbon footprint and improving energy efficiency in their products. This trend is driven by increasing environmental regulations and policies in developed countries, including the US, UK, and Germany. Governments are updating standards for the printing ink industry to address sustainability concerns, with European printed packaging required to be EN 13432 certified for biodegradability and compostability.

- Companies are responding by using eco-friendly inks and new printing technologies to meet these demands. This focus on sustainability is set to shape the future of the packaging industry.

What challenges does the Printed Carton Industry face during its growth?

- Regulations pertaining to use of printed cartons is a key challenge affecting the industry growth.

- Printed cartons are subject to rigorous regulations during manufacturing and marketing. For instance, the British Retail Consortium (BRC) and the Institute of Packaging (IoP) have collaboratively established the BRC/IoP Global Standards for Packaging and Packaging Materials. Companies obtaining BRC/IoP certifications demonstrate that their packaging meets recognized quality and safety standards. Moreover, Good Manufacturing Practice (GMP) programs ensure compliance with regulations for food contact materials and products.

- Regulatory bodies, including the US FDA 21CFR174, mandate GMPs. Adherence to these regulations is crucial for manufacturers to maintain consumer trust and ensure product safety.

Exclusive Customer Landscape

The printed carton market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the printed carton market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, printed carton market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

All Packaging Co. - The company specializes in innovative printed carton solutions, utilizing IntriCut laser cutting and creasing technology for precision and efficiency. This advanced method ensures optimal product protection and enhanced branding capabilities. IntriCut's laser technology delivers precise cuts and creases, resulting in high-quality cartons that meet the industry's stringent standards. By combining technology and expertise, we provide our clients with superior carton solutions that exceed expectations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- All Packaging Co.

- Amcor Plc

- Ariba and Co.

- DS Smith Plc

- Guangzhou Yifeng Printing and Packaging Co. Ltd.

- Huhtamaki Oyj

- International Paper Co.

- Lithoflex Inc.

- Mondi Plc

- Nippon Paper Industries Co. Ltd.

- Pactiv Evergreen Inc.

- Quad Graphics Inc.

- Refresco Group BV

- Rengo Co. Ltd.

- Seaboard Folding Box Co. Inc.

- SIG Group AG

- Smurfit Kappa Group

- Tetra Laval SA

- WestRock Co.

- Winston Packaging

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a diverse range of industries, including cosmetics, electronics, food and beverages, pharmaceuticals, homecare, and personal care. The demand for cartons in these sectors is driven by various factors, such as the need for efficiency, shock resistance, and moisture resistance. Efficiency is a key consideration in the production and use of cartons. The ability to produce cartons quickly and cost-effectively is essential for businesses looking to minimize setup costs and maximize productivity. Lithography and flexography are common printing technologies used to produce high-quality cartons in large quantities. Sustainability is another important factor in the market. With increasing concerns over the environmental impact of packaging waste, there is a growing demand for recyclable and environmentally-friendly cartons.

Recycled materials, such as paperboard and kraft board, are popular choices due to their reduced carbon footprint and minimal disposal method. The electronics industry is a significant consumer of cartons, particularly for the packaging of sensitive components. Shock resistance and rigidity are crucial requirements for these applications, as the cartons must protect the electronics from damage during transportation and handling. The food and beverage sector also relies heavily on cartons for the packaging of various products, from soups and spices to dairy products and beverages. The use of aseptic value cartons has gained popularity in this industry due to their ability to maintain product freshness and extend shelf life.

The pharmaceutical and healthcare sectors also utilize cartons for the packaging of their products. Identification and branding are essential considerations in this industry, as the cartons must clearly convey important product information and maintain the required regulatory standards. The rise of disposable income and changing consumer lifestyles have led to an increase in demand for convenience products, such as ready-made meals and household essentials. This trend has resulted in a corresponding increase in the demand for cartons in the homecare and personal care sectors. The use of raw materials, such as liquid board and coated paper, plays a significant role in the production of cartons.

Initial investments in printing facilities and substrates can be substantial, but the long-term benefits, including cost savings and improved product availability, make it a worthwhile investment for businesses. The overall processed food market is a significant consumer of cartons, as the packaging helps maintain the tangibility and freshness of the products. The population base and natural supply of raw materials are important factors in the production and demand for cartons in this sector. Minimizing wastes and reducing the environmental impact of packaging is a priority for many businesses. Changing dietary trends and consumer preferences are driving the demand for cartons that are minimally processed and free from toxic waste.

In , the market is a dynamic and diverse industry that caters to various sectors, including cosmetics, electronics, food and beverages, pharmaceuticals, homecare, and personal care. The demand for cartons is driven by factors such as efficiency, sustainability, and consumer preferences. The use of advanced printing technologies and recycled materials is essential for businesses looking to minimize costs and reduce their environmental impact. The future of the market looks promising, with a focus on innovation, sustainability, and meeting the evolving needs of consumers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.15% |

|

Market growth 2024-2028 |

USD 21.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.03 |

|

Key countries |

US, China, Germany, India, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Printed Carton Market Research and Growth Report?

- CAGR of the Printed Carton industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the printed carton market growth of industry companies

We can help! Our analysts can customize this printed carton market research report to meet your requirements.

RIA -

RIA -