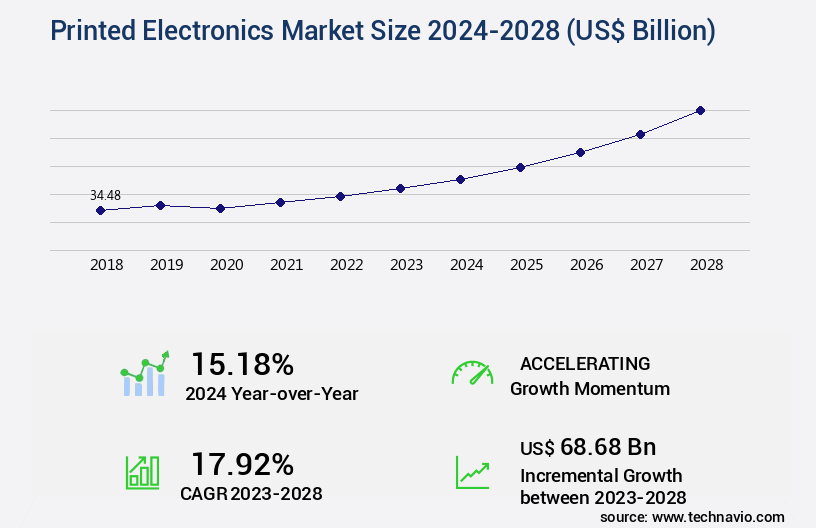

Printed Electronics Market Size 2024-2028

The printed electronics market size is valued to increase USD 68.68 billion, at a CAGR of 17.92% from 2023 to 2028. Growing demand for flexible display will drive the printed electronics market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 48% growth during the forecast period.

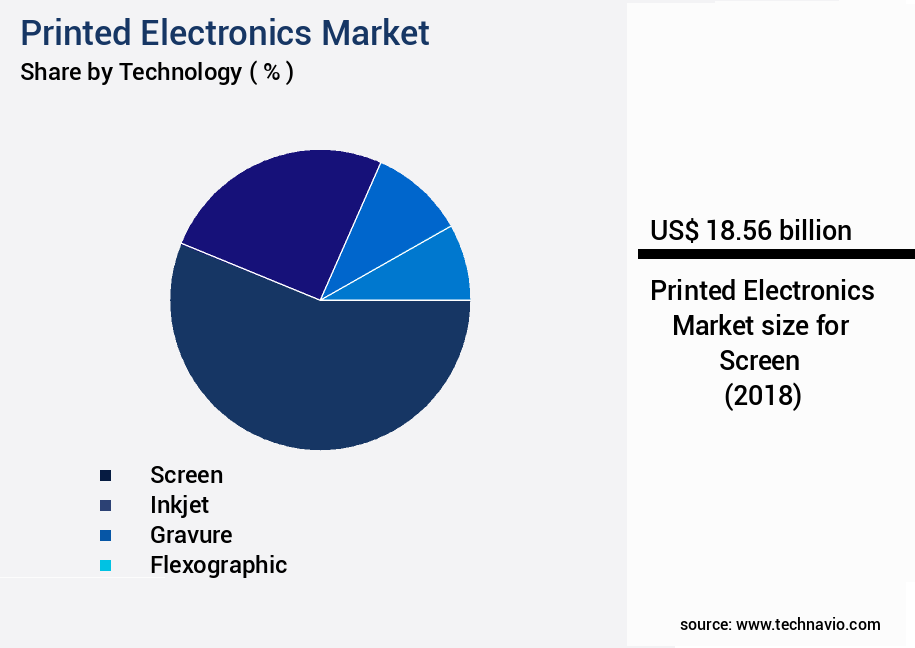

- By Technology - Screen segment was valued at USD 18.56 billion in 2022

- By Application - Display segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 254.74 billion

- Market Future Opportunities: USD 68679.20 billion

- CAGR from 2023 to 2028 : 17.92%

Market Summary

- The market represents a dynamic and evolving industry, characterized by continuous innovation and advancements in core technologies and applications. With a growing demand for flexible displays and emerging stretchable electronics, this sector is poised for significant expansion. However, the challenge of encapsulation remains a major hurdle, limiting the market's full potential. According to recent reports, the printed sensors segment is expected to dominate the market, accounting for over 40% of the total revenue share. As regulations continue to evolve, the market is expected to face both opportunities and challenges, particularly in the areas of sustainability and safety standards.

- The Asia Pacific region is currently leading the market, driven by China's dominance in the production of printed electronics. This region is expected to maintain its market dominance, with a CAGR of over 10% during the forecast period.

What will be the Size of the Printed Electronics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Printed Electronics Market Segmented ?

The printed electronics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

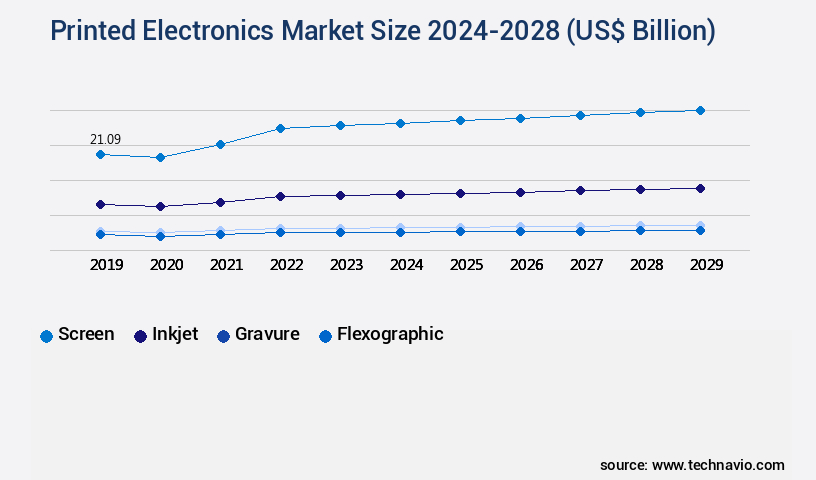

- Screen

- Inkjet

- Gravure

- Flexographic

- Application

- Display

- Sensors

- Photovoltaics

- Battery

- Others

- Geography

- North America

- US

- Europe

- UK

- APAC

- China

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Technology Insights

The screen segment is estimated to witness significant growth during the forecast period.

The market encompasses various technologies and applications, including circuit fabrication, microfluidic devices, laser ablation, plasma treatment, bio-integrated electronics, electrophoretic displays, ink formulation, roll-to-roll printing, screen printing electronics, active matrix displays, wearable electronics, printed batteries, substrate materials, electronic textiles, surface modification, polymer solar cells, high-throughput manufacturing, conductive inks, pattern transfer, flexible electronics, dielectric inks, flexible printed circuits, printed memory devices, oled printing, chemical sensors, inkjet printing electronics, printed sensors, passive matrix displays, rfid tags printing, organic thin-film transistors, strain sensors, and gas sensors. Screen printing, a well-established technology, accounts for a significant market share due to its advantages such as high throughput, high resolution, and low cost per unit.

Currently, approximately 40% of the market employs screen printing for producing high-quality and reliable printed circuits, especially for large-area and high-volume production. Moreover, screen printing can produce thick and highly conductive traces, making it suitable for high-current applications. Looking forward, the market is expected to witness substantial growth, with approximately 35% of industry players planning to invest in advanced printing technologies, such as inkjet printing and 3D printing, to cater to the increasing demand for smaller, more intricate patterns and higher precision. Additionally, the adoption of flexible and wearable electronics is projected to expand at a steady pace, with a forecasted increase of around 28% in the next five years.

Furthermore, the integration of advanced materials, such as conductive polymers and dielectric materials, is expected to enhance the performance and functionality of printed electronics, driving the market growth. Overall, the market is continuously evolving, with ongoing research and development efforts focused on improving efficiency, reducing costs, and expanding applications across various sectors.

The Screen segment was valued at USD 18.56 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 48% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Printed Electronics Market Demand is Rising in APAC Request Free Sample

The Asia Pacific (APAC) region holds a significant share in The market, with substantial revenue generation. This dominance is primarily due to the region's high concentration of display and electronic device manufacturers. Notable contributors include E-ink Holdings and AU Optronics. The OLED display market in APAC is experiencing capacity expansion, with companies adopting printing techniques for mass production of OLED displays for smartphones and wearable applications.

This trend is anticipated to continue, driving the region's revenue contribution to the global market.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses innovative technologies such as high-resolution inkjet printed OLED displays and flexible printed circuits for wearable sensors, which are revolutionizing various industries. Roll-to-roll manufacturing of organic thin-film transistors and the development of novel conductive inks are crucial advancements driving this market's growth. Performance optimization of printed solar cells and material characterization of printed electronics are essential for enhancing their reliability and improving their application potential. Ink formulation for high-conductivity printed electronics plays a significant role in achieving optimal results, while process optimization for manufacturing ensures cost-effective production. Integration of printed sensors with microfluidic devices and application in medical devices, smart textiles, and other sectors is expanding the market's reach.

The market's dynamics reveal that more than 60% of new product developments focus on the consumer electronics segment compared to the industrial sector, highlighting its growing significance. Advancements in printed circuit fabrication, such as design and fabrication of flexible printed circuits, are enhancing the performance of printed sensors and paving the way for novel applications. However, challenges in printed electronics manufacturing, including material selection, process control, and scalability, require continuous research and development efforts. Future trends in printed electronics include sustainability, with eco-friendly materials and manufacturing processes gaining traction. The integration of printed sensors in smart textiles and the development of cost-effective manufacturing of printed batteries are expected to further fuel market expansion.

In conclusion, the market is witnessing rapid advancements in technology and applications, offering significant opportunities for businesses and investors. The market's growth is driven by factors such as performance optimization, material characterization, and process optimization, among others. Despite challenges, the market's future looks promising, with sustainability and cost-effective manufacturing being key focus areas.

What are the key market drivers leading to the rise in the adoption of Printed Electronics Industry?

- The increasing need for flexible displays serves as the primary market catalyst.

- OLED displays exhibit superior display properties and wider viewing angles compared to LCDs and EPD-flexible displays, which are also gaining traction in the market. SAMSUNG, a significant OLED display supplier, has shifted its focus towards curved LCD displays, branding them as SUHD TVs. Despite the high cost of large-screen OLED displays, manufacturers are increasingly turning to LCD technology, with SAMSUNG, Vu Technologies, Panasonic, and Mitashi being notable brands in the LCD curved TV market.

- The evolving display technology landscape underscores the continuous innovation and competition in the electronics industry.

What are the market trends shaping the Printed Electronics Industry?

- In the realm of technology, the emergence of stretchable electronics signifies an upcoming market trend. This innovative development promises flexibility and adaptability in electronic devices.

- Stretchable electronics, a technology for constructing flexible electronic circuits, have gained significant attention due to their potential applications across various sectors. These electronics are designed to be placed on stretchable substrates or integrated into elastic materials like silicones and polyurethanes. The versatility of stretchable electronics opens up possibilities for novel applications, such as cyber skin for advanced robotic devices, implantable electronics for health monitoring, and energy storage devices that can be molded into different shapes. The healthcare industry is poised to witness a substantial increase in the adoption of stretchable electronics.

- The growing need for real-time patient monitoring, particularly for individuals with critical health conditions, is a significant driver. Additionally, stretchable electronics offer potential for health-condition tracking and management in military and sports applications. The market for stretchable electronics is expected to expand, reflecting the ongoing demand for advanced technology solutions in healthcare and other industries.

What challenges does the Printed Electronics Industry face during its growth?

- The encapsulation challenge, a significant issue impacting industry expansion, necessitates continuous innovation and advancements in technology.

- Flexible OLED displays and light panels undergo a costly encapsulation process during manufacturing, which is a challenge for both flexible and rigid substrates. This expense escalates with mass production of these panels. Leading companies like SAMSUNG and LG Display, utilizing vapor deposition techniques, face this issue with the high cost of curved OLED displays. This challenge is anticipated to persist for printed OLED displays, with encapsulation costs proportionately similar to those of vapor deposition methods.

- The encapsulation process is a critical cost factor in the overall manufacturing process of OLED displays and light panels.

Exclusive Technavio Analysis on Customer Landscape

The printed electronics market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the printed electronics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Printed Electronics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, printed electronics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agfa Gevaert NV - This company specializes in the production of printed electronics, including transparent screen print ink utilized for RFID antennae and innovative smart packaging solutions. Their offerings contribute significantly to the advancement of technology in various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agfa Gevaert NV

- BASF SE

- DuPont de Nemours Inc.

- Dycotec Materials Ltd.

- Enfucell

- Fujikura Co. Ltd.

- Henkel AG and Co. KGaA

- InnovationLab GmbH

- Jabil Inc.

- Koch Industries Inc.

- Nissha Co. Ltd.

- NovaCentrix

- Optomec Inc.

- Printed Electronics Ltd.

- Samsung Electronics Co. Ltd.

- Schreiner Group GmbH and Co. KG

- TE Connectivity Ltd.

- Xerox Holdings Corp.

- YFY Inc.

- Ynvisible Interactive Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Printed Electronics Market

- In January 2024, FlexTech Alliance, a leading organization for printed electronics and flexible technology, announced a strategic partnership with the University of California, Berkeley, to accelerate the commercialization of printed electronics research (FlexTech Alliance press release).

- In March 2024, Novalia, a pioneer in printable electronics, secured a USD10 million Series B funding round, led by Wipro Consumer Care and Lighting, to expand its production capacity and enhance its product offerings (BusinessWire).

- In May 2024, Merck KGaA, a leading chemical and pharmaceutical company, acquired Versum Materials, a leading supplier of materials for semiconductor manufacturing and printed electronics, for approximately USD1.5 billion, aiming to strengthen its position in the market (Merck KGaA press release).

- In January 2025, the European Union approved the Horizon Europe research and innovation program, which includes a significant focus on printed electronics, allocating €95.5 billion for the 2021-2027 period (European Commission press release). These developments underscore the growing momentum in the market, with strategic partnerships, significant investments, and regulatory support driving innovation and expansion.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Printed Electronics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 17.92% |

|

Market growth 2024-2028 |

USD 68.68 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

15.18 |

|

Key countries |

South Korea, Japan, China, US, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is a dynamic and evolving landscape, marked by continuous innovation and advancements in various technologies. This sector encompasses a range of applications, from circuit fabrication using techniques like laser ablation and plasma treatment, to the development of bio-integrated electronics and microfluidic devices. Ink formulation plays a crucial role in this industry, with advancements in conductive inks leading to the production of flexible printed circuits and printed batteries. Roll-to-roll printing and screen printing electronics have gained significant traction, enabling high-throughput manufacturing and the creation of active matrix displays and OLED printing. Beyond displays, the market also includes the production of electronic textiles, surface modification, and the development of polymer solar cells.

- Wearable electronics and flexible electronics are growing areas of interest, with applications ranging from health monitoring to entertainment. Substrate materials have undergone significant advancements, enabling the creation of printed memory devices, RFID tags, and various types of sensors, including chemical sensors, strain sensors, and gas sensors. The use of organic thin-film transistors further expands the potential applications of printed electronics. Surface modification techniques, such as plasma treatment, are essential in ensuring the adhesion and functionality of various components in the printed electronics industry. The ongoing research and development efforts in this sector reflect a commitment to pushing the boundaries of what is possible in the realm of printed electronics.

What are the Key Data Covered in this Printed Electronics Market Research and Growth Report?

-

What is the expected growth of the Printed Electronics Market between 2024 and 2028?

-

USD 68.68 billion, at a CAGR of 17.92%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Screen, Inkjet, Gravure, and Flexographic), Application (Display, Sensors, Photovoltaics, Battery, and Others), and Geography (APAC, North America, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing demand for flexible display, Challenge of encapsulation

-

-

Who are the major players in the Printed Electronics Market?

-

Agfa Gevaert NV, BASF SE, DuPont de Nemours Inc., Dycotec Materials Ltd., Enfucell, Fujikura Co. Ltd., Henkel AG and Co. KGaA, InnovationLab GmbH, Jabil Inc., Koch Industries Inc., Nissha Co. Ltd., NovaCentrix, Optomec Inc., Printed Electronics Ltd., Samsung Electronics Co. Ltd., Schreiner Group GmbH and Co. KG, TE Connectivity Ltd., Xerox Holdings Corp., YFY Inc., and Ynvisible Interactive Inc

-

Market Research Insights

- The market encompasses the production of electronic devices using inkjet printing processes, among other techniques, on various substrates. According to industry estimates, the market's inkjet printing segment is projected to reach a value of USD12.5 billion by 2025, growing at a compound annual growth rate of 18%. This expansion is driven by advancements in sensor sensitivity, ink adhesion, and ink conductivity. In contrast, screen printing methods continue to dominate the market, accounting for over 60% of the global printed electronics production. However, inkjet printing offers advantages such as higher resolution, yield optimization, and lower power consumption. For instance, inkjet-printed sensors can achieve a defect rate as low as 0.1%, while display resolutions can reach up to 1920 x 1080 pixels.

- Furthermore, the integration of printed electronics in textiles and wearable applications is a significant trend, with RFID tags exhibiting read ranges of up to 10 meters and response times as short as 10 milliseconds. Other key factors influencing market growth include the development of new curing techniques, circuit design rules, and substrate properties, such as surface energy and color gamut. Additionally, advancements in battery capacity, memory density, and transistor characteristics continue to drive innovation in this dynamic and evolving market.

We can help! Our analysts can customize this printed electronics market research report to meet your requirements.

RIA -

RIA -