Proton Pump Inhibitors (PPIs) Market Size 2025-2029

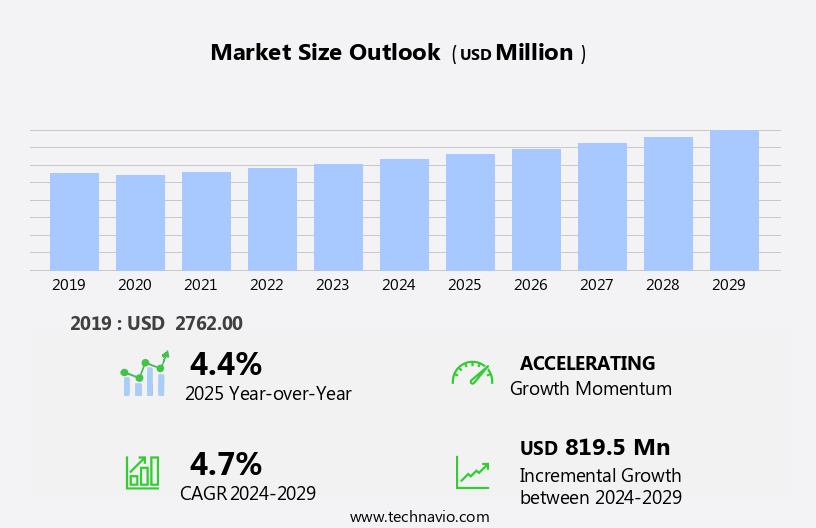

The proton pump inhibitors market size is forecast to increase by USD 819.5 million, at a CAGR of 4.7% between 2024 and 2029.

- The market is characterized by significant growth drivers and trends, as well as notable challenges. The expanding geriatric population is a key growth driver, as this demographic is more susceptible to gastroesophageal reflux disease and other conditions requiring long-term PPI therapy. Additionally, the increasing prevalence of gastric ulcers and other gastrointestinal disorders contributes to market expansion. However, the market faces challenges, including the rising number of lawsuits against PPIs due to potential side effects, such as kidney damage and increased risk of heart attacks. These lawsuits may lead to increased regulatory scrutiny and potential restrictions on PPI use, posing a significant threat to market growth.

- Companies operating in the PPI market must navigate these challenges by investing in research and development of safer alternatives, as well as implementing robust regulatory compliance strategies. By capitalizing on the growing demand for effective gastrointestinal treatments while addressing regulatory and legal hurdles, market participants can successfully capitalize on the opportunities and challenges presented in the PPI market.

What will be the Size of the Proton Pump Inhibitors (PPIs) Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

Proton pump inhibitors (PPIs) continue to play a significant role in the gastrointestinal therapeutics market due to their efficacy in treating various conditions, including peptic ulcer disease, gastroesophageal reflux disease (GERD), and Zollinger-Ellison syndrome. The market dynamics for PPIs are continually evolving, with ongoing research and development efforts focusing on addressing unmet needs and improving patient outcomes. In the realm of disease management, PPIs are increasingly being used in the context of smoking cessation and alcohol reduction to mitigate the negative effects of these habits on the gastrointestinal tract. Furthermore, the role of PPIs in managing conditions such as c difficile infection, elevated intra-abdominal pressure, and chronic kidney disease is a growing area of interest.

Brand-name PPIs dominate the market, but the introduction of generic alternatives and over-the-counter (OTC) medications has increased competition and driven down costs. Health technology assessment and cost-effectiveness analysis are crucial factors influencing market dynamics, with healthcare providers and primary care physicians seeking to optimize treatment algorithms and improve patient satisfaction. Clinical trials and treatment guidelines continue to shape the market, with a focus on addressing adverse events, drug interactions, and disease resistance. Patient education and lifestyle modifications, such as dietary changes and weight management, are essential components of effective PPI therapy. Quality of life and safety and efficacy remain key considerations in the PPI market, with ongoing efforts to improve patient adherence and address healthcare costs.

Healthcare providers and medical guidelines emphasize the importance of proper diagnosis and individualized treatment plans to ensure optimal outcomes for patients. The ongoing evolution of the PPI market is driven by a complex interplay of factors, including patient needs, healthcare costs, regulatory requirements, and technological advancements. The landscape is continually unfolding, with new developments and trends shaping the future of this dynamic market.

How is this Proton Pump Inhibitors (PPIs) Industry segmented?

The proton pump inhibitors (ppis) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- OTC PPIs

- Prescription PPIs

- Route Of Administration

- Oral

- Injectable

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- Middle East and Africa

- UAE

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

.

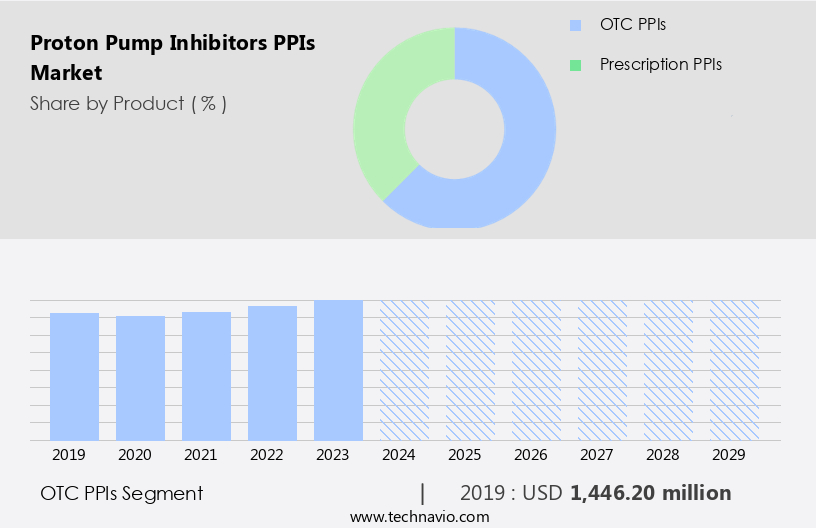

By Product Insights

The otc ppis segment is estimated to witness significant growth during the forecast period.

The market encompasses both prescription medications and over-the-counter (OTC) drugs, with the latter category gaining significant traction due to ease of access and affordability. OTC PPIs, such as PREVACID, NEXIUM, PRILOSEC, and Zegerid, are commonly used for treating frequent heartburn by decreasing stomach acid secretion. The US Food and Drug Administration (FDA) permits their use for up to 14 days per year. Peptic ulcer disease, acid reflux, and Zollinger-Ellison syndrome are among the conditions treated with PPIs. However, their use is not limited to these conditions, as they are also prescribed for other gastrointestinal disorders and for preventing gastric ulcers in critically ill patients.

Patient education plays a crucial role in ensuring proper use and adherence to PPI therapy. This is particularly important for patients with chronic conditions like chronic kidney disease, where long-term management is essential. In addition, lifestyle modifications, such as dietary changes and alcohol reduction, can help improve treatment outcomes and reduce the need for long-term PPI use. Health technology assessments , telemedicine and clinical trials are ongoing to evaluate the safety and efficacy of PPIs, as well as their cost-effectiveness compared to other treatment options. Treatment algorithms and medical guidelines are being developed to optimize PPI use and minimize potential adverse events, such as drug-induced liver injury, drug interactions, and antibiotic resistance.

Elevated intra-abdominal pressure and hiatal hernia can complicate PPI therapy, necessitating close monitoring and potential dose adjustments. Primary care physicians and healthcare providers are key players in managing PPI therapy and ensuring patient adherence, which is essential for optimal health outcomes. Despite the benefits of PPIs, concerns regarding their long-term use and potential adverse effects persist. These include drug resistance, delayed gastric emptying, and increased healthcare costs. Generic drugs offer a more affordable alternative, but patient satisfaction and safety and efficacy remain important considerations. Quality of life improvements and patient satisfaction are key drivers of PPI use, making it essential for healthcare providers to prioritize patient education and adherence to treatment guidelines.

The ongoing development of new treatment options and delivery methods, such as extended-release formulations and combination therapies, is expected to further shape the PPI market landscape.

The OTC PPIs segment was valued at USD 1446.20 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

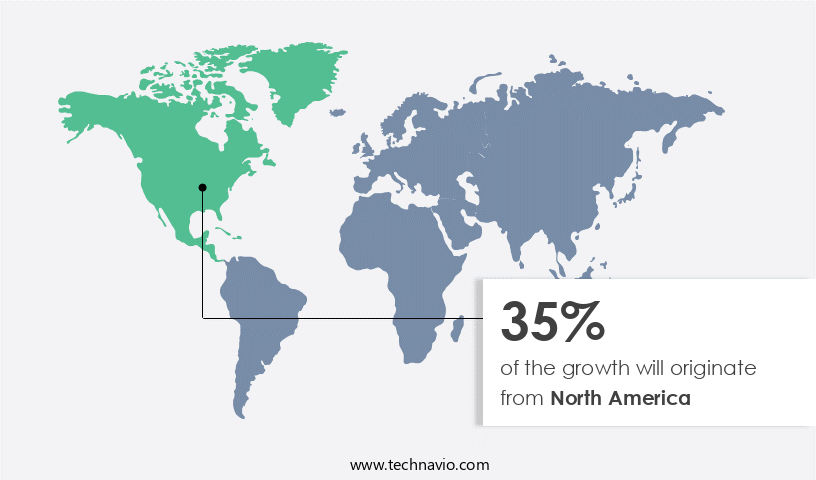

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is significantly driven by the presence of a large patient pool suffering from acid-related diseases. This population expansion is attributed to lifestyle factors such as increased alcohol and tobacco consumption and urban living. The region's market dominance is also due to the presence of major pharmaceutical companies offering both branded and generic PPIs, as well as a well-established regulatory framework for drug approval. Patient education plays a crucial role in disease management, with healthcare providers emphasizing the importance of adherence to treatment algorithms. Peptic ulcer disease, c difficile infection, and Zollinger-Ellison syndrome are among the conditions treated with PPIs.

However, safety and efficacy concerns, including drug-induced liver injury, drug interactions, and antibiotic resistance, necessitate continuous clinical trials and health technology assessments. Drug pricing and healthcare costs are significant factors influencing market dynamics. While prescription medications are essential for managing various gastrointestinal disorders, over-the-counter (OTC) medications and lifestyle modifications, such as dietary changes and acid reflux management, can also contribute to improved patient satisfaction and quality of life. Chronic conditions like chronic kidney disease and gastric motility disorders further fuel market growth. The integration of medical guidelines and clinical practice recommendations into primary care settings can enhance patient adherence and overall health outcomes.

However, challenges like delayed gastric emptying, drug resistance, and elevated intra-abdominal pressure necessitate ongoing research and innovation. Public awareness campaigns and patient education initiatives are vital for addressing the rising prevalence of gastrointestinal diseases. Healthcare providers play a pivotal role in ensuring patient safety and efficacy, while cost-effectiveness analysis and disease management strategies can help mitigate healthcare costs. In summary, the North American Proton Pump Inhibitors market is experiencing growth due to the presence of a large patient population, major pharmaceutical companies, and a well-established regulatory framework. Continuous innovation, patient education, and cost-effective strategies are essential for addressing the challenges associated with acid-related diseases and improving overall patient care.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Proton Pump Inhibitors (PPIs) Industry?

- The reformulation of drugs serves as the primary catalyst for market growth.

- Proton Pump Inhibitors (PPIs) are prescription medications widely used to treat conditions such as acid reflux and hiatal hernia. Primary care physicians often prescribe these drugs to improve health outcomes for patients. However, the use of PPIs is not without risks, including drug-induced liver injury and potential interactions with antibiotics that may contribute to antibiotic resistance. The market for PPIs is dynamic, with ongoing research and development efforts focused on enhancing drug efficacy through innovative formulations. Transdermal patches, extended-release formulations, and orally disintegrating tablets are some examples of drug delivery systems that increase patient compliance and bioavailability.

- Moreover, reformulation of marketed drugs presents an opportunity for pharmaceutical companies to extend their patent terms, delaying the entry of generic versions into the market. For instance, AstraZeneca and DAIICHI SANKYO Co. Ltd. (DAIICHI SANKYO) launched new formulations of the already marketed drug, NEXIUM, as 10 milligrams (mg) and 20 mg granules for suspension and sachets. These new formulations offer improved patient convenience and potential therapeutic advantages. Medical guidelines play a crucial role in the prescribing patterns of PPIs, ensuring their appropriate use and minimizing potential risks. Continuous monitoring of drug safety and efficacy is essential to maintain the trust and confidence of patients and healthcare providers in these essential medications.

What are the market trends shaping the Proton Pump Inhibitors (PPIs) Industry?

- The geriatric population is experiencing significant growth and represents an emerging market trend. This demographic shift presents numerous opportunities for businesses and industries catering to the unique needs of older adults.

- Proton pump inhibitors (PPIs) are commonly prescribed medications for conditions such as peptic ulcer disease, gastroesophageal reflux disease (GERD), and other acid-related disorders. The aging population is a significant driver for the PPI market due to the increased prevalence of these conditions with age. The relaxation of the lower esophageal sphincter, a valve that prevents stomach acid from flowing back into the esophagus, is a common issue in older adults, leading to heartburn and acid reflux. Furthermore, the slowing down of the digestive system with age can also contribute to acidity and the need for PPIs.

- Smoking cessation and lifestyle modifications are essential for managing acid-related disorders, but they may not always be sufficient. PPIs play a crucial role in treating these conditions and improving patients' quality of life. However, the use of PPIs is not without risks, including an increased risk of c difficile infection and potential interactions with other medications. Health technology assessments and clinical trials are essential for evaluating the safety and efficacy of PPIs and developing treatment algorithms. Patients must be educated on the proper use and potential side effects of these medications to maximize their benefits while minimizing risks.

- The PPI market is expected to continue growing due to the increasing prevalence of acid-related disorders and the need for effective treatments. Elevated intra-abdominal pressure, which can occur in various conditions such as obesity and certain surgeries, can also contribute to acid reflux and the need for PPIs. As such, ongoing research and innovation in the field of PPIs are essential to address the evolving needs of patients and improve their overall health outcomes.

What challenges does the Proton Pump Inhibitors (PPIs) Industry face during its growth?

- The rising number of lawsuits against PPIs poses a significant challenge to the industry's growth trajectory. This trend, which has gained momentum in recent times, could potentially hinder the expansion and profitability of companies operating in this sector.

- The market is currently facing legal challenges due to allegations of kidney injuries caused by these drugs. Plaintiffs have filed lawsuits against various PPI manufacturers, including Prevacid and Dexilant, accusing them of failing to adequately warn about the potential side effects of these drugs. The FDA requested the withdrawal of all ranitidine products in April 2020 due to the potential formation of N-Nitrosodimethylamine (NDMA) when stored at high temperatures, increasing the risk of kidney injuries. These incidents have raised concerns about the safety and efficacy of PPIs, particularly for patients with chronic kidney disease and other risk factors.

- Adverse events related to PPIs are not limited to kidney injuries. Some studies suggest a link between PPIs and weight gain, alcohol reduction, and disease management. However, the cost-effectiveness analysis of PPIs in managing these conditions is still under debate. Patient satisfaction with PPIs remains high, but safety concerns and potential long-term side effects may impact their long-term use. Dietary changes and lifestyle modifications are often recommended as alternatives to PPIs for managing conditions such as gastroesophageal reflux disease (GERD) and peptic ulcers. However, for patients with Zollinger-Ellison syndrome, PPIs remain the most effective treatment option.

- As the market evolves, manufacturers and healthcare providers must prioritize patient safety and efficacy while ensuring cost-effectiveness and addressing the concerns of regulatory agencies.

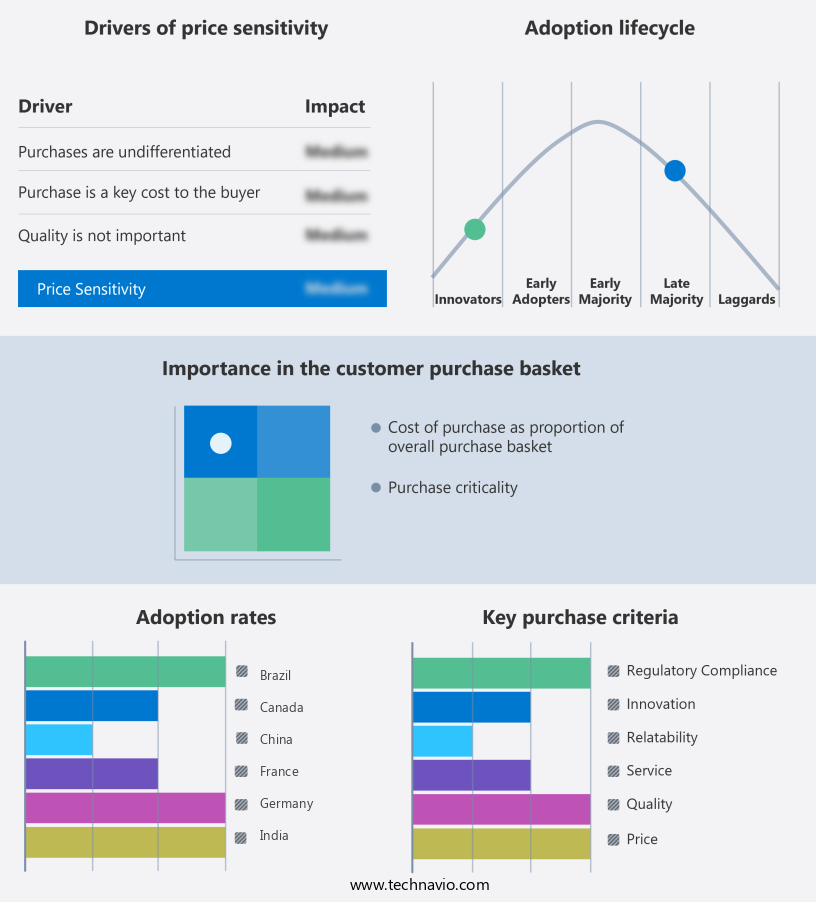

Exclusive Customer Landscape

The proton pump inhibitors (ppis) market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the proton pump inhibitors (ppis) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, proton pump inhibitors (ppis) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amgen Inc. - The company specializes in proton pump inhibitors, including LUMAKRAS, which function as effective gastric acid reducers. These inhibitors exhibit reduced concentrations of sotorasib, ensuring optimal therapeutic benefits. By utilizing advanced research and development techniques, the organization continues to innovate and deliver high-quality inhibitors to the market. These agents are essential in managing various gastrointestinal conditions, providing relief and promoting overall health.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amgen Inc.

- AstraZeneca Plc

- Aurobindo Pharma Ltd.

- Bausch Health Companies Inc.

- Bayer AG

- Cipla Inc.

- Dr Reddys Laboratories Ltd.

- Eisai Co. Ltd.

- Eli Lilly and Co.

- Glenmark Pharmaceuticals Ltd.

- Johnson and Johnson Inc.

- Perrigo Co. Plc

- Pfizer Inc.

- RedHill Biopharma Ltd.

- Sanofi SA

- Sun Pharmaceutical Industries Ltd.

- Takeda Pharmaceutical Co. Ltd.

- Teva Pharmaceutical Industries Ltd.

- The Procter and Gamble Co.

- Zydus Lifesciences Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Proton Pump Inhibitors (PPIs) Market

- In February 2023, AstraZeneca announced the US Food and Drug Administration (FDA) approval of their new Proton Pump Inhibitor (PPI), dexlansoprazole 30 mg delayed-release capsules, for the treatment of erosive esophagitis (EE). This expansion of dexlansoprazole's indication adds to AstraZeneca's strong presence in the PPI market (AstraZeneca Press Release, 2023).

- In July 2024, Pfizer and Merck & Co. Entered into a strategic collaboration to co-develop and commercialize Pfizer's experimental PPI, Pfizer's PF-06651620, in combination with Merck's Januvia (sitagliptin) for the treatment of gastroesophageal reflux disease (GERD). This partnership aims to leverage both companies' expertise and resources to address the unmet needs in the GERD market (Pfizer Press Release, 2024).

- In March 2025, Takeda Pharmaceuticals completed the acquisition of Shire Plc, which included Shire's gastrointestinal (GI) portfolio, including the PPI, lansoprazole. This acquisition significantly expanded Takeda's presence in the GI market, making it a major player in the PPI market (Takeda Press Release, 2025).

- In May 2025, the European Medicines Agency (EMA) granted a positive opinion for the extension of the indication of Protonix (pantoprazole) to include the treatment of pathological hypersecretory conditions associated with Zollinger-Ellison syndrome. This approval marks an important development in the PPI market, as Protonix is the first PPI to receive this indication in Europe (EMA Press Release, 2025).

Research Analyst Overview

- Proton pump inhibitors (PPIs) continue to dominate the gastrointestinal therapeutics market, with pharmaceutical research focusing on enhancing their therapeutic efficacy and safety. Big data analytics plays a pivotal role in PPIs market dynamics, enabling personalized medicine and therapeutic drug monitoring. In the realm of maintenance therapy, esophageal and gastric cancers, Barrett's esophagus, and other gastrointestinal disorders necessitate long-term management. Advancements in technology, such as impedance monitoring, radiofrequency ablation, and machine learning (ML), are revolutionizing the diagnosis and treatment of esophageal and gastric diseases. Minimally invasive procedures like laparoscopic surgery and upper endoscopy are increasingly preferred for their safety and efficacy.

- Pharmaceutical companies invest heavily in new drug discovery and development, employing AI and ML to accelerate the process. Precision medicine and clinical decision support systems facilitate tailored prophylactic therapy, ensuring optimal patient outcomes. In the realm of diagnostic procedures, barium swallow, PH monitoring, and esophageal stricture assessment remain essential for accurate diagnosis and treatment planning. As the need for more effective and less invasive therapeutic interventions grows, robotic surgery is emerging as a promising solution for complex gastrointestinal procedures.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Proton Pump Inhibitors (PPIs) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

199 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.7% |

|

Market growth 2025-2029 |

USD 819.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.4 |

|

Key countries |

US, Germany, China, Canada, UK, India, France, Japan, Brazil, and UAE |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Proton Pump Inhibitors (PPIs) Market Research and Growth Report?

- CAGR of the Proton Pump Inhibitors (PPIs) industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the proton pump inhibitors (ppis) market growth of industry companies

We can help! Our analysts can customize this proton pump inhibitors (ppis) market research report to meet your requirements.

RIA -

RIA -