Enjoy complimentary customisation on priority with our Enterprise License!

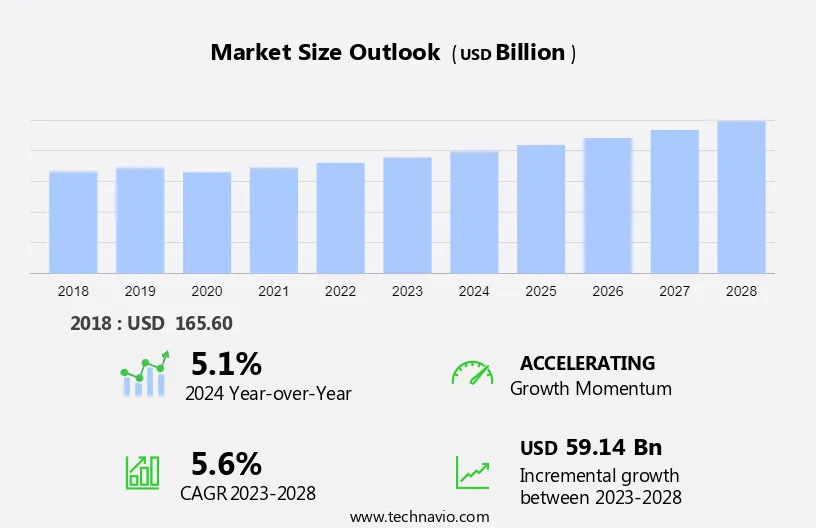

The public warehousing market size is forecast to increase by USD 59.14 billion, at a CAGR of 5.6% between 2023 and 2028. The growth rate of the market depends on several factors, such as the growing number of SMEs, increased focus on cutting logistics costs, and growing focus on last-mile delivery. Our report examines historical data from 2018-2022, besides analyzing the current and forecasted market scenario.

The rapid economic growth in APAC countries like India and China has fueled industrialization and trade, driving the need for efficient warehousing services. E-commerce growth has raised consumer expectations for speedy deliveries. CEVA Logistics S A provides a variety of public warehousing solutions including bonded/non-bonded, ambient, or temperature-controlled. Deutsche Bahn AG, through its subsidiary DB Schenker, also offers public warehousing solutions, catering to the region's evolving logistics needs.

Market Forecast 2023-2027

To learn more about this report, Request Free Sample

Our researchers studied the market research and growth data for years, with 2023 as the base year and 2023 as the estimated year, and presented the key drivers, trends, and challenges for the market.

Globally, the number of SMEs operating in the market is increasing. As SMEs are typically limited in terms of their financial capabilities and infrastructure, they generally opt for public warehouses to fulfill their warehousing and storage needs. Thus, as the number of SMEs increases, the demand for public warehouses is also likely to increase. As per the World Bank Group, SMEs represent about 90% of the businesses and more than half of the employment across the world. Formal SMEs account for two-fifths of the GDP of emerging economies. Due to government initiatives, such as exclusive economic zones for SMEs providing better credit facilities and reduced tax rates, SMEs have been able to flourish and have been growing even in volatile markets.

As a result of these activities, the number of SMEs has increased, resulting in the creation of numerous jobs and helping the global economy. Because these SMEs typically operate on a small scale and lack a well-established infrastructure, they rely on third parties to meet their transportation and logistics needs. Thus, these businesses frequently use public warehouses to keep costs low and avoid large capital expenditures that could negatively impact their cash flow. Public warehouses allow these SMEs to use as much space as and when required without investing in workforce and technology. Thus, the growth of SMEs across the world will continue to boost the growth of the global public warehousing market during the forecast period.

Multilevel warehouses are common in densely populated Asian cities such as Tokyo, Singapore, and Hong Kong, where dense populations and limited availability of land have made it a necessity. In the more developed countries such as the US, multistory warehouses are a nascent concept. This is largely due to the difficulty of providing industrial real estate in some of the country's most populous consumer regions. Developers have to deal simultaneously with chronic land scarcity as well as city development limitations imposed to alleviate traffic congestion in the country's major cities. For instance, in the coming years, the US will witness an increase in the number of multistory warehouses. Many of these warehouses will be in major urban areas, where there is a great demand for speedy delivery and convenience. Most construction activity is now taking place in New York, Seattle, San Francisco, and Washington, DC.

Moreover, the increasing use of e-commerce by retailers has also provided momentum to overall warehousing demand, thus making multistory warehousing a greater need. As the concept of multistory warehouses gains popularity, public warehousing vendors will have to leverage this new concept to increase their capacity and attract more companies to use public warehouses. Thus, the growing popularity of multistory warehousing will boost the growth of the global public warehousing market during the forecast period.

On-demand space availability is one of the major benefits of public warehousing. However, the limited space availability, especially during peak time in the sales cycle, has become a major challenge for companies in the global public warehousing market. During peak seasons, such as festivals or sale seasons, companies require additional space to store the excess volume of goods. This requirement for additional space may not be fulfilled due to limited space available in public warehouses, thus forcing companies to find alternatives. Moreover, finding additional space for warehousing is not only a time-consuming task but also increases the overall warehousing cost. This rise in cost is attributed to the increase in transportation costs as well as the amount spent on finding a warehouse that may be priced higher.

Hence, during peak seasons, companies compete for space, especially if the private and public warehouses have reached their maximum capacity. This becomes a challenge due to the short time frame that several companies, especially retailers, deal with during their seasonal sales cycles. This challenge of limited space availability is expected to hamper the growth of the global public warehousing market during the forecast period.

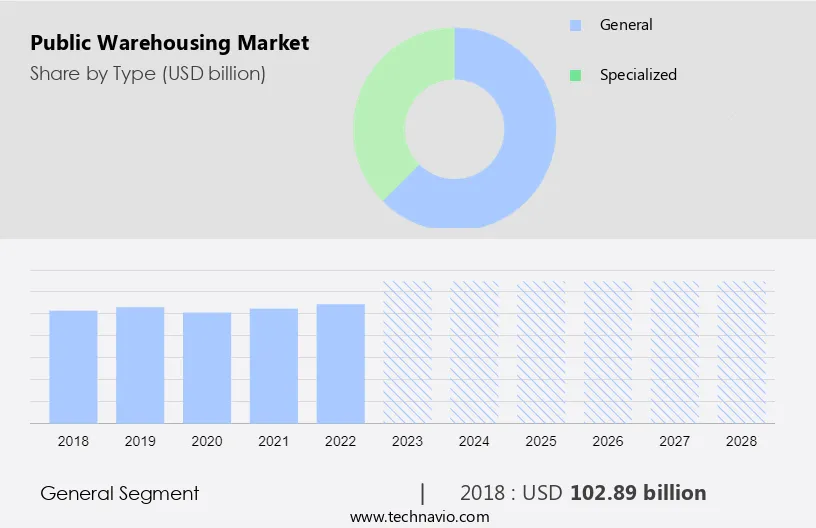

The general segment will account for a major share of the market's growth during the forecast period.? The general warehousing segment includes warehouses that are used to stockpile products and do not require any special handling equipment or temperature control. Apparel, manufacturing raw materials, industrial products, various non-perishable intermediate products, automobile components, and consumer staples are stored in these warehouses. These products do not require the temperature to be adjusted to lower levels; hence, no cold storage devices are required.

Customised Report as per your requirements!

The general segment was valued at USD 102.89 billion in 2018. Furthermore, companies that export goods to other countries may not have warehousing facilities in other countries, so they rely on third-party warehouses to avoid investing in their warehouse. Furthermore, as e-commerce sales have expanded, demand for consumer goods and products such as household goods, clothes, and utility products has increased, which requires general warehousing. Thus, these factors will drive the growth of the general segment and boost the global public warehousing market during the forecast period.

Based on application, the market has been segmented into manufacturing, consumer goods, retail, healthcare, and others. The manufacturing segment will account for the largest share of this segment. Public warehousing provides manufacturers with flexibility and scalability. Instead of committing to fixed warehouse space, manufacturers can scale their storage and distribution needs based on changes in production volumes or market demand. This flexibility is particularly beneficial for businesses with varying inventory levels. Public warehousing provides manufacturers with flexibility and scalability. Instead of committing to fixed warehouse space, manufacturers can scale their storage and distribution needs based on changes in production volumes or market demand. Thus, these factors will drive the growth of the manufacturing segment and impel the global public warehousing market during the forecast period.

For more insights on the market share of various regions Download Sample PDF now!

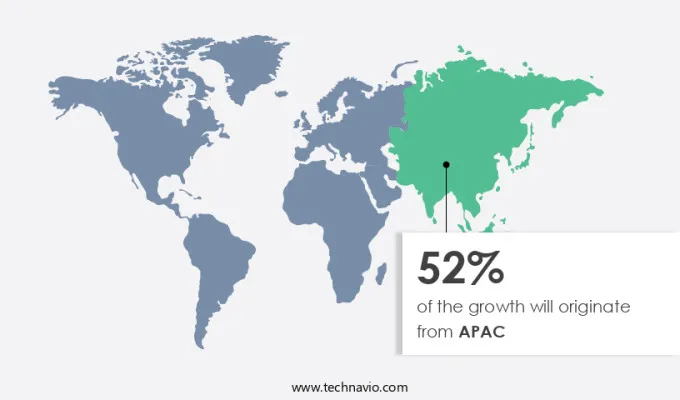

APAC is estimated to contribute 52% to the growth by 2027. Technavio's analysts have provided extensive insight into the market forecasting, detailing the regional trends and drivers influencing the market's trajectory throughout the forecast period. The rapid economic growth in many APAC countries, such as India and China, has led to increased industrialization and trade activities. This growth generates demand for warehousing services to store and distribute goods efficiently. With the rise of e-commerce, consumers in APAC have heightened expectations for faster and more reliable delivery services. Public warehousing plays a crucial role in achieving last-mile delivery efficiency.

Moreover, the ongoing infrastructure development projects in various APAC countries, such as India, including the development of logistics parks and transportation networks, contribute to the growth of the warehousing sector. Improved infrastructure enhances the efficiency of supply chain operations. For instance, in July 2023, the Ministry of Road, Transport and Highways (MoRTH) of India announced the development of 35 Multimodal Logistics Parks (MMLPs) under Bharatmala Phase 1. 6 MMLPs are undertaken by MoRTH in port cities namely Cochin (Kerala), Chennai (Tamil Nadu), Vishakhapatnam (Andhra Pradesh), Mumbai (Maharashtra), Kolkata (West Bengal), and Kandla (Gujarat). Higher consumer spending is another factor that has increased the demand for consumer goods and is ultimately driving the growth of goods manufacturing.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Agility Public Warehousing Co.: The company offers public warehousing solutions with recycle zones, solar panels, xeriscaping, and drought-tolerant plants.

We also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including:

K.S.C.P, CEVA Logistics S A, Deutsche Bahn AG, Deutsche Post AG, FedEx Corp., Fullers Logistics Ltd., GEODIS, Globe Express Services logistics and Shipping Co., Kenco Group Inc., Kuehne Nagel Management AG, NFI Industries Inc., Penske Corp., PiVAL International, Ryder System Inc., Saddle Creek Logistics Services, The China Fox Group Pty Ltd., United Parcel Service Inc., Warehouse Services Inc., Wincanton Plc, and XPO Inc.

Technavio market forecast the an in-depth analysis of the market and its players through combined qualitative and quantitative data. The analysis classifies companies based on their business approaches, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak, based on their quantitative data analysis.

The market analysis and report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028.

The public warehousing and storage services market is witnessing significant growth, driven by the increasing demand for storage of manufactured products and processed and frozen food products. The e-commerce industry, adopting an omnichannel model to cater to the rising online buying trend, requires efficient warehousing solutions. Despite the growth in online retail, offline stores continue to play a crucial role, especially in the big-ticket products segment. To meet these demands, supply chains are adopting advanced technologies such as GPS, RFID, and digital voice to enhance warehouse management systems. However, challenges persist, including the need for higher investment in advanced technologies, lack of awareness about common global standards, and the complexity of supply chain management (SCM), exacerbated by the globalization trend and bilateral free trade agreements like the North America Free Trade Agreement (NAFTA).

Morever, the International Association of Refrigerated Warehouses (IARW) and companies like Lineage Logistics are actively involved in the temperature-controlled market, offering services for refrigerated warehousing and storage for perishable products. These facilities include cold storage rooms, refrigerated warehouses, and services such as tempering, blast freezing, and modified atmosphere storage. The pharma sector benefits from these facilities, particularly for storing sensitive products like antibiotic liquids. As the demand for efficient storage solutions grows, the public warehousing market is expected to witness further growth, especially in segments such as food products, pharmaceuticals, and essential household goods. This growth underscores the importance of efficient logistics services and inventory management, particularly for SMEs looking to expand their operations.

|

Public Warehousing Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.6% |

|

Market Growth 2024-2028 |

USD 59.14 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.1 |

|

Regional analysis |

APAC, North America, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 52% |

|

Key countries |

US, China, India, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Agility Public Warehousing Co. K.S.C.P, CEVA Logistics S A, Deutsche Bahn AG, Deutsche Post AG, FedEx Corp., Fullers Logistics Ltd., GEODIS, Globe Express Services logistics and Shipping Co., Kenco Group Inc., Kuehne Nagel Management AG, NFI Industries Inc., Penske Corp., PiVAL International, Ryder System Inc., Saddle Creek Logistics Services, The China Fox Group Pty Ltd., United Parcel Service Inc., Warehouse Services Inc., Wincanton Plc, and XPO Inc. |

|

Market dynamics |

Parent market analysis, Market growth analysis inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by Application

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.