Quantum Cryptography Solutions Market Size 2024-2028

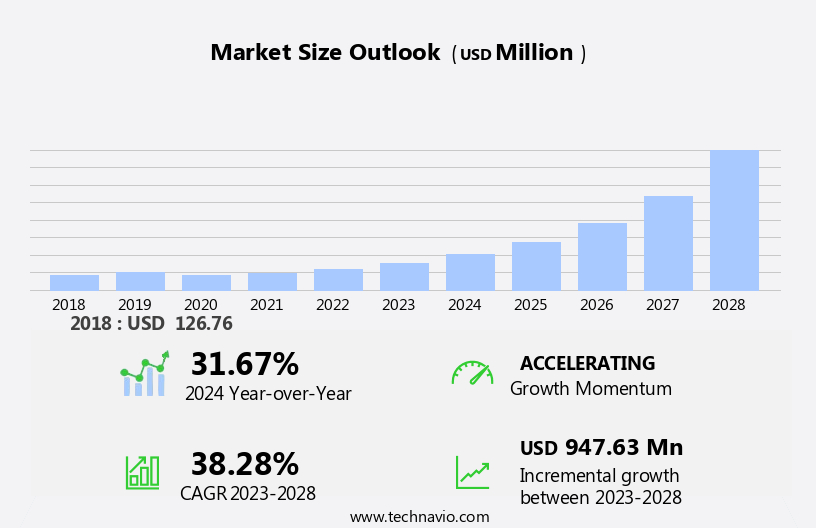

The quantum cryptography solutions market size is forecast to increase by USD 947.63 billion at a CAGR of 38.28% between 2023 and 2028.

- Quantum cryptography, a secure communication technology utilizing the principles of quantum mechanics, has gained significant attention due to its ability to prevent hacking, as photons, the quantum particles used, cannot be decoded without being detected. This market is witnessing notable growth trends, including the increasing number of ransomware attacks, such as the one on Colonial Pipeline, which underscores the need for secure digital communication solutions. companies are responding with organic and inorganic strategies, investing heavily in research and development and implementation costs to commercialize quantum cryptography technologies. Bitcoin and digital banking sectors are expected to be major adopters, as the need for secure transactions becomes increasingly crucial. The quantum cryptography market is poised for growth, with quantum key distribution (QKD) being a key technology driving this trend. Despite the high costs, the potential benefits of quantum cryptography in ensuring secure communication far outweigh the challenges.

What will be the Size of the Market During the Forecast Period?

- Quantum cryptography, a revolutionary approach to data security, is gaining significant attention in the ever-evolving cybersecurity landscape. This advanced security solution leverages the principles of quantum mechanics to provide unbreakable encryption, rendering traditional cryptographic methods obsolete. The core of quantum cryptography lies in the no-cloning theorem, which states that it is impossible to create an exact copy of an unknown quantum state. This theorem forms the basis for quantum key distribution (QKD), a process that enables secure sharing of cryptographic keys between two parties. Photons, elementary particles of light, play a pivotal role in quantum cryptography. They are used to encode and transmit information securely, ensuring that any attempt to intercept or eavesdrop on the communication is immediately detected. Mathematical algorithms, a crucial component of quantum cryptography, enable the encoding and decoding of quantum information.

- Quantum cryptography offers a promising solution, providing unbreakable encryption and ensuring data integrity. Hardware components, including receivers and electronic networking equipment, are essential for implementing quantum cryptography solutions. These components must be designed and manufactured with the highest standards to ensure optimal performance and security. The quantum computing industry is expected to grow exponentially, fueled by advancements in technology and increasing demand for secure data protection. As quantum computing capabilities advance, the need for quantum cryptography solutions becomes increasingly urgent. Investment in cybersecurity is on the rise, with organizations recognizing the importance of securing their digital assets.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Component

- Service

- Solution

- End-user

- Defense

- BFSI

- Government and public sector

- Telecom

- Others

- Geography

- North America

- US

- APAC

- China

- Japan

- Europe

- Germany

- UK

- Middle East and Africa

- South America

- North America

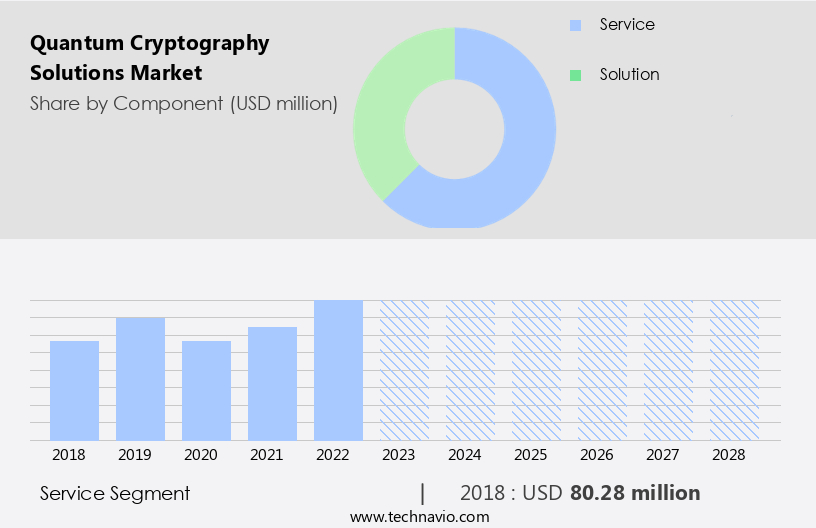

By Component Insights

- The service segment is estimated to witness significant growth during the forecast period.

In the current era of digital transformation, ensuring the security of sensitive data has become a top priority for government entities and public organizations. Quantum cryptography, with its advanced security capabilities, is gaining significant traction in this domain. This technology offers future-proof protection for official communication, both wired and wireless, between various governmental bodies, ministries, and regulatory authorities. For instance, ID Quantique's Centauris encryption solutions enable governments to securely transfer classified data across all networks using a single encryption platform. Quantum cryptography solutions have proven particularly valuable in securing data transfers during elections and backbone SAN connections. As the industry moves towards virtualization of servers, cloud computing services, and the BYOD trend, the need for quantum-safe standards becomes increasingly important.

Additionally, gateway antivirus, antispyware, and intrusion prevention systems must also be quantum-safe to protect against potential threats. Quantum cryptography solutions provide a quantum-safe future for secure data transfer and communication. Consulting and advisory firms and industry verticals are actively deploying and integrating these solutions to ensure their clients' data remains secure.

Get a glance at the market report of share of various segments Request Free Sample

The service segment was valued at USD 80.28 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

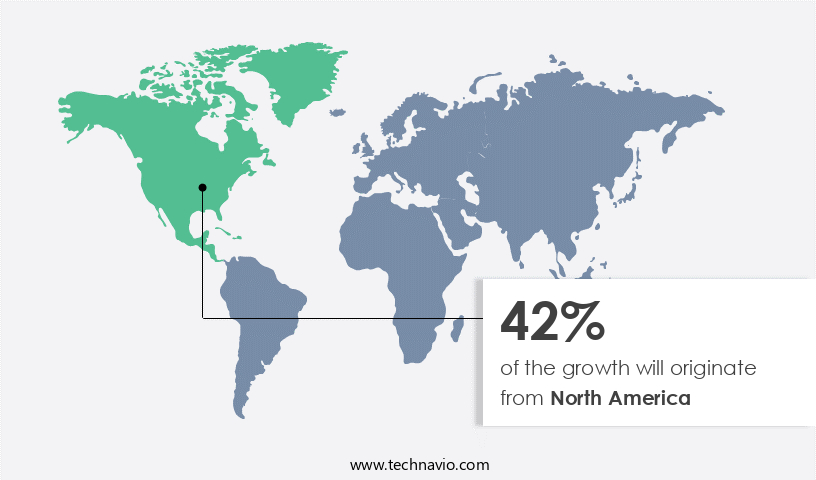

- North America is estimated to contribute 42% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In North America, the market for quantum cryptography solutions is experiencing significant growth due to the region's early adoption of advanced technologies such as cognitive computing and machine learning. This technological ecosystem, coupled with the extensive digitalization of both private and public sectors, necessitates strong cybersecurity and data management solutions. Quantum cryptography, with its unique ability to provide unbreakable encryption through the principles of quantum mechanics and the No-cloning theorem, is becoming increasingly sought after. Photons, the fundamental particles used in quantum key distribution, offer a level of security that is unattainable with traditional encryption technologies. As cyber threats continue to evolve, including quantum computing-based assaults, the demand for quantum cryptography solutions is expected to increase.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Quantum Cryptography Solutions Market?

Ability of photons not to be hacked assured by laws of QM is the key driver of the market.

- Quantum cryptography is a revolutionary security solution based on quantum mechanics, specifically quantum encryption through Quantum Key Distribution (QKD). Unlike traditional encryption approaches, quantum cryptography relies on the no-cloning theorem, which ensures the uniqueness of quantum states. Photons, the quantum particles used in quantum cryptography, transmit a single bit of data based on their quantum state. This method allows for the secure exchange of cryptographic keys, ensuring data privacy even with infinite computing power. The uncertainty principle in quantum mechanics introduces changes in the properties of quantum particles during transmission, making it impossible for eavesdroppers to observe and decode the information without being detected.

- The quantum computing industry's advancements necessitate cybersecurity infrastructure upgrades, leading to increased funding for quantum-safe encryption. Virtualization of servers, gateway antivirus, antispyware, intrusions, viruses, spyware, worms, Trojans, adware, keyloggers, filtering, and secret key protection are all areas where quantum cryptography solutions can provide enhanced security. In conclusion, quantum cryptography offers a quantum-safe future for secure communication, ensuring data privacy and protection against cyber threats, including those posed by quantum computing. As the world increasingly relies on digital technologies and communication networks, quantum cryptography solutions will play a crucial role in safeguarding sensitive information, such as intellectual property, health information, and financial transactions.

What are the market trends shaping the Quantum Cryptography Solutions Market?

Rising adoption of organic and inorganic strategies by vendors is the upcoming trend in the market.

- The market is experiencing significant growth due to the increasing threats from quantum computing-based assaults and the need for quantum-safe encryption. Quantum mechanics, specifically the No-cloning theorem, forms the basis of quantum cryptography, which uses photons to generate and distribute cryptographic keys. companies in this market are leveraging mathematical algorithms and advanced security measures, such as quantum network protocols and quantum internet infrastructure, to provide secure communication solutions. Banking, healthcare, financial transactions, intellectual property, and worldwide communication networks are some of the major industry verticals investing in quantum cryptography systems and QKD devices. Traditional encryption approaches, such as hardware and traditional cryptography, are becoming increasingly vulnerable to cyberattacks, making quantum cryptography solutions an attractive alternative.

-

The market is highly competitive, with players such as ID Quantique, Magiq Technologies, and Toshiba participating. The market is also witnessing the development of quantum-safe standards, such as Quantum Safe Standards, and the virtualization of servers and cloud computing services, which are expected to further drive market growth. Additionally, the BYOD trend, gateway antivirus, antispyware, and the increasing use of IoT devices are creating new opportunities for companies in the market. The market is expected to continue growing, driven by the need for secure communication and data protection in an increasingly digital world.

What challenges does Quantum Cryptography Solutions Market face during its growth?

High R&D and implementation costs related to quantum cryptography solutions is a key challenge affecting the market growth.

- Quantum cryptography solutions, which encompass quantum encryption and quantum key distribution (QKD), represent a significant investment for both companies and buyers. For companies, the costs are substantial due to ongoing research and development (R&D) and product innovation. With numerous key players actively pursuing product development and commercialization strategies, the quantum cryptography market is witnessing rapid evolution. The integration of quantum cryptography systems into satellite communications and free-space QKD is further driving up costs. From the buyer's perspective, the adoption of quantum cryptography solutions comes with a premium price tag. This is due to the complexity and specialized nature of the technology, which includes the use of photons and mathematical algorithms to generate and distribute cryptographic keys.

- However, the high costs associated with quantum cryptography solutions may limit their widespread adoption, particularly among small and medium enterprises (SMEs) and mobile devices. Despite the challenges, the quantum cryptography market is expected to grow, driven by the need for secure communication and the increasing threat of cyberattacks. The market is also being fueled by the development of quantum miniaturization, which is making quantum systems more accessible and cost-effective. The deployment and integration of quantum cryptography solutions in various industry verticals, including IT & Telecom, are expected to further drive market growth. In conclusion, the quantum cryptography market is witnessing significant investment from both companies and buyers due to the increasing need for secure communication and the threat of cyberattacks.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AUREA Technology

- Entrust Corp.

- Honeywell International Inc.

- HP Inc.

- Infineon Technologies AG

- International Business Machines Corp.

- IonQ Inc.

- ISARA Corp.

- MagiQ Technologies Inc.

- NuCrypt LLC

- PQ Solutions Ltd.

- QuNu Labs Inc.

- Quantum Xchange

- Qubitekk Inc.

- QuintessenceLabs Pty Ltd.

- RTX Corp.

- SK Telecom Co. Ltd.

- TOPTICA Photonics AG

- Utimaco GmbH

- Xiphera

- Toshiba Corp.

- Quantinuum Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Quantum cryptography, a revolutionary approach to encryption, leverages quantum mechanics to provide unbreakable security. Unlike traditional encryption methods, it relies on the no-cloning theorem and photons to generate and distribute cryptographic keys. Quantum key distribution (QKD) uses mathematical algorithms to ensure secure communication, protecting against cyber threats, including quantum computing-based assaults. Industries like banking, healthcare, and financial transactions heavily rely on encryption technologies to secure sensitive information. Quantum cryptography solutions offer advanced security measures against hacking and decoding attempts. These systems are vital for worldwide communication networks, including submarine fiber-optic cables and satellite communications. Quantum cryptography is essential for protecting intellectual property, network security, application security, and database security in IT & telecom industries.

Further, with the increasing threat of cyberattacks, quantum-safe encryption is becoming a priority. Artificial intelligence and advanced security measures are crucial components of a quantum-safe future. Quantum cryptography systems include QKD devices and quantum random number generators (QRNG), offering quantum-safe standards for securing digital technologies. Consulting and advisory services, deployment and integration, and industry verticals are key areas of focus for commercializing quantum cryptography. As digital technologies continue to evolve, so do the threats. Ransomware attacks, such as the Colonial Pipeline incident, and digital banking vulnerabilities require powerful security infrastructure. Quantum cryptography solutions offer a secure platform for conducting transactions and communication networks, protecting against viruses, worms, trojans, adware, keyloggers, and other malware.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

176 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 38.28% |

|

Market Growth 2024-2028 |

USD 947.63 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

31.67 |

|

Key countries |

US, Japan, China, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -