Quick Service Restaurants Market Size 2026-2030

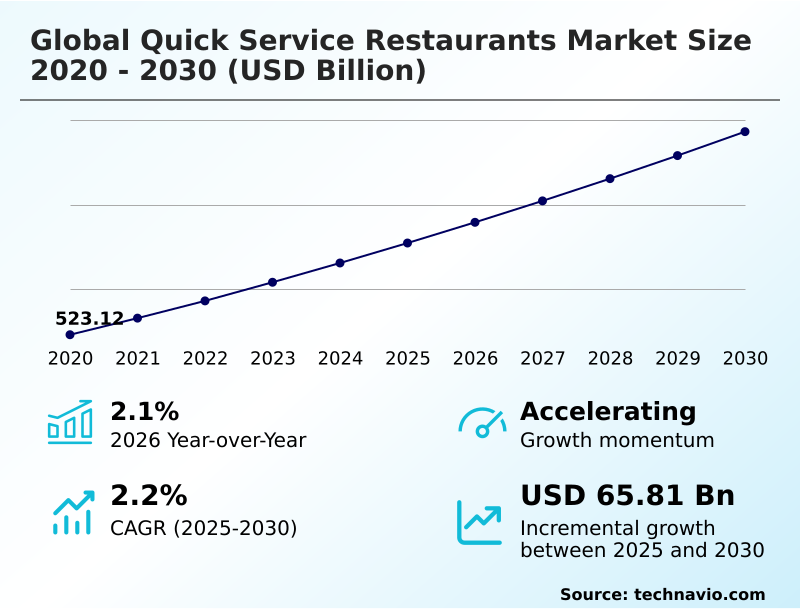

The quick service restaurants market size is valued to increase by USD 65.81 billion, at a CAGR of 2.2% from 2025 to 2030. Strategic mainstreaming of digital-first ecosystems and hyper-automation will drive the quick service restaurants market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 42.3% growth during the forecast period.

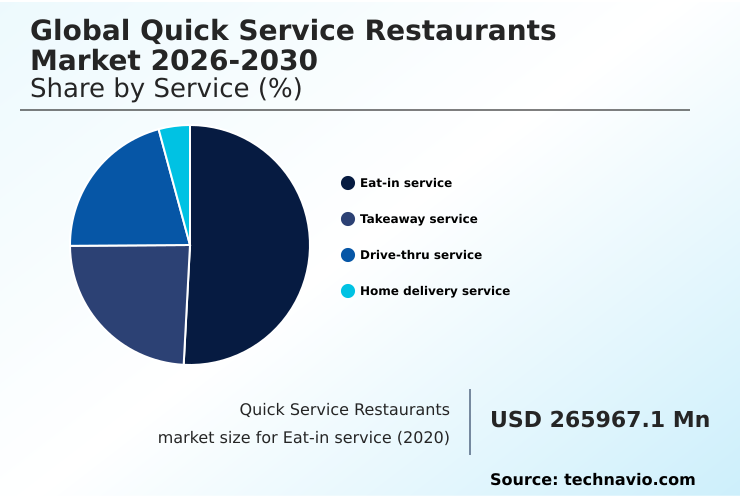

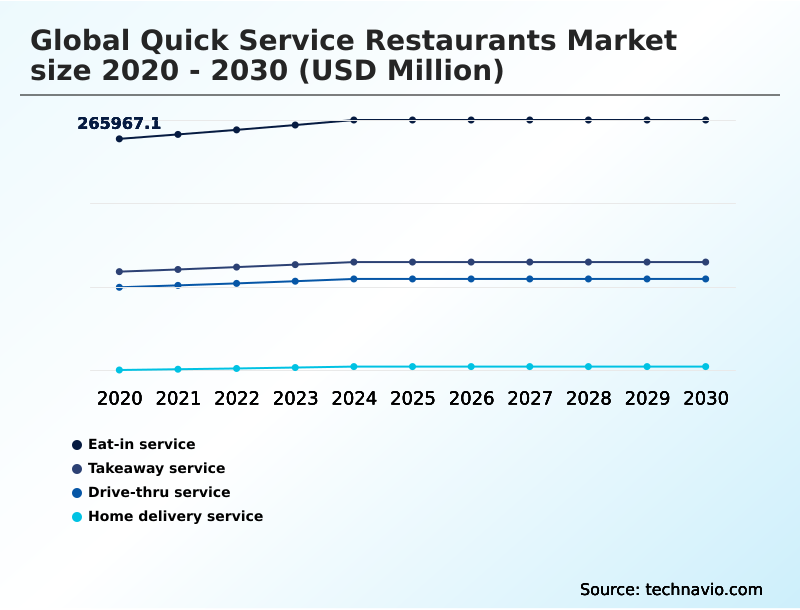

- By Service - Eat-in service segment was valued at USD 285.86 billion in 2024

- By Type - Chain segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 120.00 billion

- Market Future Opportunities: USD 65.81 billion

- CAGR from 2025 to 2030 : 2.2%

Market Summary

- The quick service restaurants market is defined by a fundamental shift toward digital-first ecosystems and operational simplification. As consumer lifestyles become increasingly compressed, the traditional value proposition of speed is now augmented by an expectation for seamless, technology-enabled interactions.

- This evolution is evident in the widespread adoption of artificial intelligence for drive-thru optimization, personalized loyalty platforms, and automated kitchen management systems that enhance throughput while reducing labor dependency.

- For instance, operators leverage predictive analytics to optimize supply chains, analyzing real-time sales data and local event schedules to forecast demand, thereby reducing food waste by over 15% and ensuring ingredient availability. This focus on data-driven efficiency is critical as the market navigates persistent labor shortages and rising input costs.

- The competitive landscape is further shaped by the proliferation of cloud kitchens and delivery-only formats, which allow brands to expand their geographic reach with reduced capital expenditure. Ultimately, the ability to balance price accessibility with ingredient quality and ethical sourcing will determine market leadership.

What will be the Size of the Quick Service Restaurants Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Quick Service Restaurants Market Segmented?

The quick service restaurants industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Service

- Eat-in service

- Takeaway service

- Drive-thru service

- Home delivery service

- Type

- Chain

- Independent

- Product type

- Burger and sandwich

- Pizza

- Asian cuisine

- Frozen desserts and ice cream

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Service Insights

The eat-in service segment is estimated to witness significant growth during the forecast period.

The eat-in service segment is transforming, pivoting from functional dining to experiences defined by hospitality-focused technology and premium design. Modern establishments integrate self-service kiosks and table-side mobile ordering, using a unified commerce platform to reduce queuing friction.

This shift toward operational self-optimization improves order accuracy by over 15%. High-traffic urban locations are adopting 'third place' concepts with comfortable seating to attract customers during off-peak hours.

The adoption of biometric authentication and frictionless payment methods at the point of sale is streamlining the checkout process, maintaining the speed advantage of the quick service model during high-volume periods.

These data-driven sustainability reporting measures are key for franchisee profitability and leveraging next-generation oven temperature controls.

The Eat-in service segment was valued at USD 285.86 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 42.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Quick Service Restaurants Market Demand is Rising in APAC Get Free Sample

The global quick service restaurants market exhibits a varied geographic landscape, with APAC emerging as the primary engine for incremental growth, contributing 42.3% of the total opportunity.

This region's momentum is fueled by rapid urbanization and a tech-savvy consumer base embracing mobile-first dining experiences and menu localization. In contrast, North America and Europe function as mature markets focused on operational self-optimization.

Here, the deployment of agentic artificial intelligence and autonomous back-of-house systems is standard, with AI-powered restaurant management solutions improving order fulfillment precision by over 12%.

These established regions prioritize workforce retention and are early adopters of reusable container programs and other zero-waste initiatives to meet stringent environmental stewardship standards.

Market Dynamics

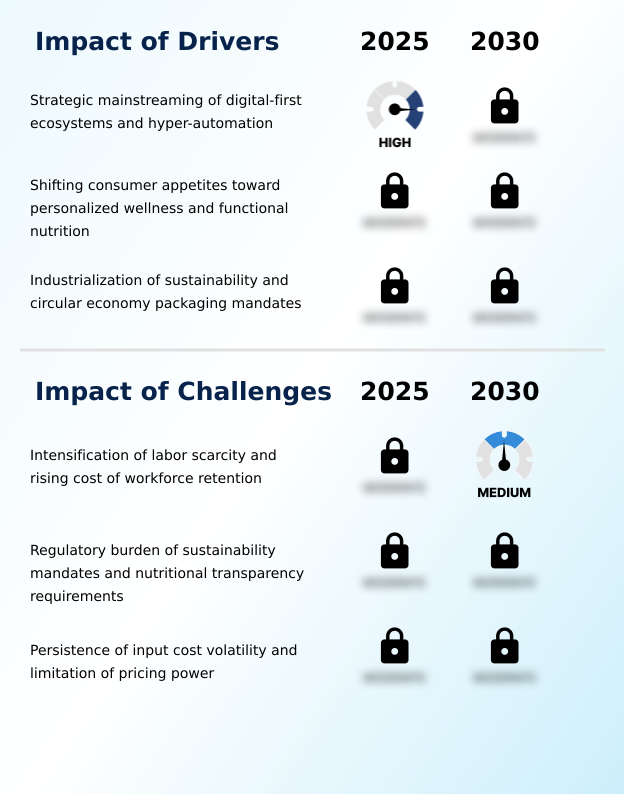

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The future of the Global Quick Service Restaurants Market 2026-2030 is being shaped by highly specific strategic imperatives. The industrialization of hyper-automation within drive-thru operations is no longer optional, with leaders achieving twice the throughput of competitors. This is complemented by the deployment of unified commerce platforms that create a seamless customer journey.

- Internally, the integration of agentic AI and autonomous operations, particularly automating order queues based on preparation complexity, is critical for efficiency. On the customer-facing side, the proliferation of hyper-personalized loyalty ecosystems that use geofencing for personalized drive-thru menus is driving retention.

- The strategic expansion of sustainable circularity is also paramount, involving everything from implementing reusable tableware for dine-in to integrating biomaterial-based soy sauce droppers. Success hinges on navigating the regulatory burden of sustainability mandates while managing input cost volatility and pricing power. This requires a balanced approach, from re-engaging guests with bundled offers to mitigating labor scarcity with automated kitchen tech.

- Firms that master the deployment of augmented makeline cobotic systems and the upgrade to next-generation espresso equipment will lead the market. The impact of GLP-1 medications on consumer appetites is also forcing a re-evaluation of menu strategies, pushing operators to use local pulses for plant-based options.

What are the key market drivers leading to the rise in the adoption of Quick Service Restaurants Industry?

- The strategic mainstreaming of digital-first ecosystems and the industrialization of hyper-automation are key drivers propelling market growth and operational resilience.

- A primary market driver is the transition to digital-first ecosystems and hyper-automation, particularly within drive-thru and carry-out channels.

- In labor-constrained markets, the requirement for AI-driven voice assistants and unified commerce platforms is mounting, as these systems can handle high-volume order processing with minimal human oversight, reducing order errors by up to 20%.

- The implementation of predictive analytics optimizes inventory levels and labor scheduling based on real-time demand forecasting. This focus on technology is coupled with the strategic evolution of consumer appetites toward personalized wellness and functional nutrition.

- AI-driven menu personalization, suggesting items based on health goals, is becoming standard.

- Furthermore, sustainability mandates and the rise of circular economy packaging solutions, such as strawless rPET lids, are compelling operators to adopt closed-loop waste management and data-driven sustainability reporting to enhance brand loyalty.

What are the market trends shaping the Quick Service Restaurants Industry?

- The market is undergoing a structural realignment, marked by the institutionalization of agentic AI and the deployment of autonomous back-of-house operations to enhance efficiency.

- The market is structurally realigning toward the institutionalization of agentic artificial intelligence and autonomous back-of-house operations. This move toward invisible AI is driven by labor shortages, with AI-driven kitchen managers prioritizing order queues based on preparation complexity, improving throughput during peak periods by up to 18%. This trend toward operational self-optimization enables the autonomous adjustment of staffing and inventory orders.

- The proliferation of hyper-personalized loyalty ecosystems and dynamic pricing models utilize real-time consumer data. Sophisticated customer relationship management platforms analyze order history to push tailored promotions, which has been shown to increase engagement by 15%. This shift toward precision value engineering, balancing premium innovation with targeted affordability, is critical.

- Sustainable circularity and plant-forward hybridization are also key, utilizing compostable packaging and hybrid burgers to reduce carbon footprints.

What challenges does the Quick Service Restaurants Industry face during its growth?

- A key market challenge is the intensification of labor scarcity, which is compounded by the rising costs associated with workforce retention and training.

- The market faces a critical challenge from a shrinking labor pool and escalating workforce retention costs, compelling investment in automated kitchen technologies and self-service kiosks. However, the high capital expenditure for these integrations, often representing over 20% of an independent operator's annual budget, creates significant financial barriers.

- Another major challenge is the escalating regulatory burden related to sustainability mandates and nutritional transparency requirements. Navigating a fragmented landscape of local health mandates and packaging bans on single-use plastics adds significant administrative overhead. Finally, the sustained volatility of raw material prices and consumer resistance to further price hikes, or input cost volatility, are compressing margins.

- The necessity to stabilize pricing, even as input costs remain unpredictable, creates an economic trap, forcing a reliance on a barbell menu strategy to balance value with profitability.

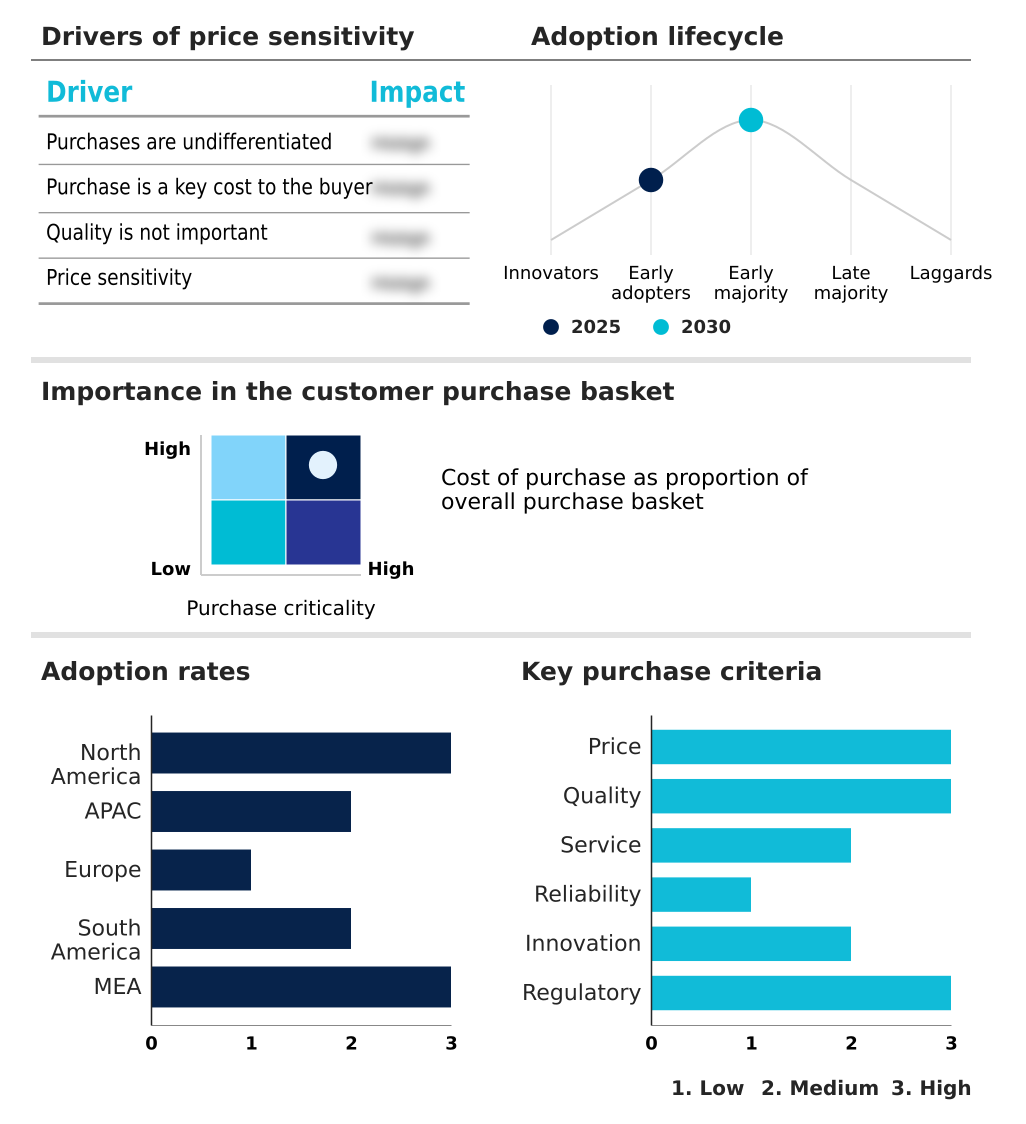

Exclusive Technavio Analysis on Customer Landscape

The quick service restaurants market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the quick service restaurants market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Quick Service Restaurants Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, quick service restaurants market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American Dairy Queen Corp. - An analyst view indicates a focus on specialized menus featuring fresh, high-quality ingredients delivered through a company-owned, fast-casual operational model, emphasizing food with integrity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Dairy Queen Corp.

- Carls Jr. Restaurants LLC

- Carrols Restaurant Group Inc.

- Chick fil A Inc.

- Chipotle Mexican Grill Inc.

- Dominos Pizza Inc.

- Greggs Plc

- Hardees Restaurants LLC

- Honeybee Foods Corp.

- Inspire Brands Inc.

- Jack in the Box Inc.

- Little Caesar Enterprises Inc.

- McDonald Corp.

- MOS Food Services Inc.

- Pret A Manger

- Restaurant Brands Inc.

- Starbucks Corp.

- The Wendys Co.

- YUM Brands Inc.

- Zaxbys Franchising LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Quick service restaurants market

- In September, 2024, Chipotle Mexican Grill Inc. announced the successful transition of its Autocado and Augmented Makeline cobotic systems into live restaurant environments, aimed at automating labor-intensive preparation tasks and improving throughput.

- In November, 2024, Datassential reported that Filipino cuisine emerged as the fastest-growing menu category in the United States, signaling a broader consumer shift toward unique and authentic global flavor profiles.

- In March, 2025, delivery aggregator Swiggy entered into a strategic partnership with Domino's Pizza Inc. in India to bolster its quick-service offerings, demonstrating increasing collaboration between tech platforms and established food chains.

- In April, 2025, Church Texas Chicken announced a significant global expansion with the launch of nine hundred new international sites, many featuring specialized beverage stations and regional bakery items to increase average order values.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Quick Service Restaurants Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 2.2% |

| Market growth 2026-2030 | USD 65805.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 2.1% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global quick service restaurants market is defined by a strategic pivot toward digital-first ecosystems and hyper-automation, where market leaders leverage smart restaurant formats. Dominant entities are institutionalizing AI-driven voice assistants and unified commerce platforms that prioritize mobile ordering and data-driven loyalty programs.

- The landscape is witnessing a massive technological overhaul, including the integration of agentic artificial intelligence for drive-thru ordering and autonomous back-of-house operations. This move to AI-powered restaurant management is a direct response to operational pressures and a core component of boardroom strategy, with capital expenditure for automated kitchen technologies and self-service kiosks directly tied to ESG compliance and profitability goals.

- Other firms are differentiating through technical innovation; for instance, successfully transitioning robotic kitchen assistants from pilot to live environments to automate labor-intensive tasks and improve peak service times by up to 30%.

- This competitive environment is further shaped by the digital expansion strategies of delivery-only formats and the growth of virtual brands, all increasingly reliant on integrated delivery platforms, predictive analytics, and hyper-personalized marketing through dynamic pricing models and digital menu boards to maintain consumer frequency.

- The adoption of high-performance sampling oscilloscopes and high-speed data transceivers underpins the reliability of these sprawling digital networks, from kitchen display systems to frictionless payment methods.

What are the Key Data Covered in this Quick Service Restaurants Market Research and Growth Report?

-

What is the expected growth of the Quick Service Restaurants Market between 2026 and 2030?

-

USD 65.81 billion, at a CAGR of 2.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Service (Eat-in service, Takeaway service, Drive-thru service, and Home delivery service), Type (Chain, and Independent), Product Type (Burger and sandwich, Pizza, Asian cuisine, Frozen desserts and ice cream, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Strategic mainstreaming of digital-first ecosystems and hyper-automation, Intensification of labor scarcity and rising cost of workforce retention

-

-

Who are the major players in the Quick Service Restaurants Market?

-

American Dairy Queen Corp., Carls Jr. Restaurants LLC, Carrols Restaurant Group Inc., Chick fil A Inc., Chipotle Mexican Grill Inc., Dominos Pizza Inc., Greggs Plc, Hardees Restaurants LLC, Honeybee Foods Corp., Inspire Brands Inc., Jack in the Box Inc., Little Caesar Enterprises Inc., McDonald Corp., MOS Food Services Inc., Pret A Manger, Restaurant Brands Inc., Starbucks Corp., The Wendys Co., YUM Brands Inc. and Zaxbys Franchising LLC

-

Market Research Insights

- The market's momentum is driven by a strategic pivot toward hyper-personalized loyalty ecosystems, where real-time demand forecasting and data-enabled risk management are standard. This approach moves beyond generic discounts, creating mobile-first dining experiences that have been shown to increase customer frequency by up to 20%.

- The implementation of a barbell menu strategy is critical for navigating input cost volatility, balancing high-margin premium items with value offerings. This requires sophisticated inventory tracking and nutritional innovation to maintain profitability. Furthermore, the integration of plant-based proteins and clean-label sourcing, now a baseline expectation, aligns with responsible consumption habits and broadens demographic appeal.

- Operators adopting these strategies report a 10% improvement in brand loyalty metrics.

We can help! Our analysts can customize this quick service restaurants market research report to meet your requirements.

RIA -

RIA -