Radiosurgery And Radiotherapy Robotics Market Size 2026-2030

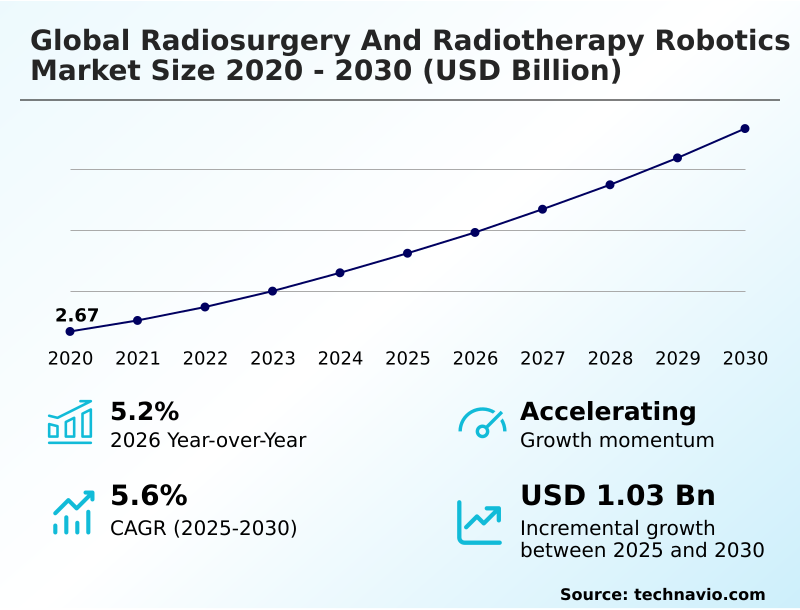

The radiosurgery and radiotherapy robotics market size is valued to increase by USD 1.03 billion, at a CAGR of 5.6% from 2025 to 2030. Increase in cancer cases and re-treatments will drive the radiosurgery and radiotherapy robotics market.

Major Market Trends & Insights

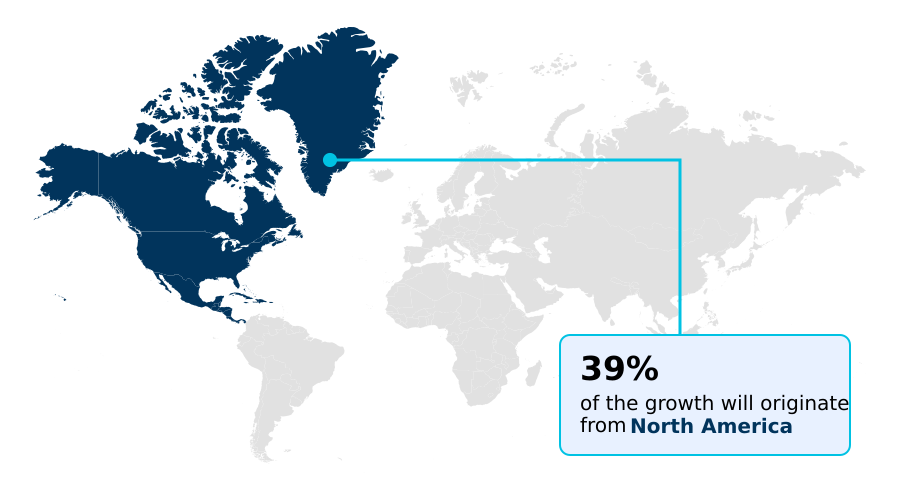

- North America dominated the market and accounted for a 38.6% growth during the forecast period.

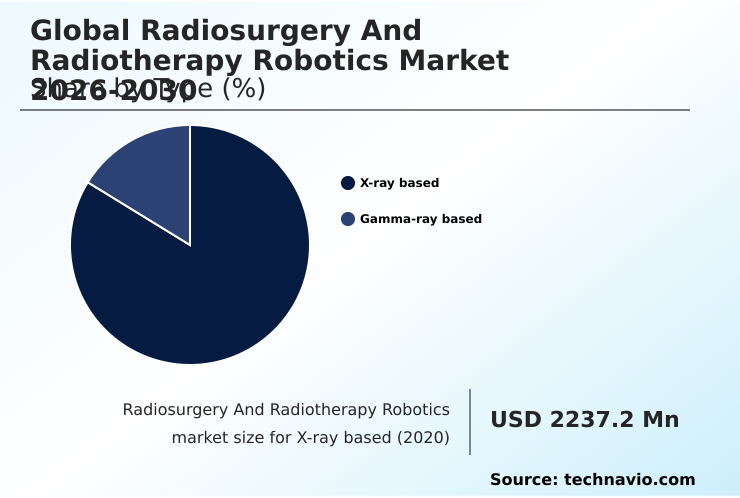

- By Type - X-ray based segment was valued at USD 2.62 billion in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.66 billion

- Market Future Opportunities: USD 1.03 billion

- CAGR from 2025 to 2030 : 5.6%

Market Summary

- The radiosurgery and radiotherapy robotics market is defined by a relentless drive for greater precision and efficiency in cancer care. This evolution is propelled by the rising incidence of cancer and the increasing demand for non-invasive tumor treatment options that minimize side effects and shorten recovery times.

- Key innovations center on advanced radiotherapy techniques, including stereotactic body radiation therapy and mr-guided radiotherapy, which rely on sophisticated motion management solutions and real-time tumor tracking to deliver ablative doses with sub-millimeter treatment accuracy.

- For instance, in a clinical scenario involving early-stage lung cancer, robotic systems with respiratory motion synchronization can precisely target the tumor as it moves, reducing radiation-induced toxicity to healthy lung tissue. This capability supports the trend of hypofractionated radiotherapy, allowing for shorter treatment courses.

- However, the high capital equipment procurement costs and the need for specialized oncology centers create significant adoption barriers, particularly in emerging economies. The market is also shaped by the ongoing development of alternative modalities like proton beam therapy systems, which challenge photon-based radiosurgery platforms to demonstrate superior cost-effectiveness and patient outcomes.

What will be the Size of the Radiosurgery And Radiotherapy Robotics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Radiosurgery And Radiotherapy Robotics Market Segmented?

The radiosurgery and radiotherapy robotics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- X-ray based

- Gamma-ray based

- End-user

- Hospitals

- Clinics

- Independent radiotherapy centers

- Application

- Lung cancer

- Prostate cancer

- Breast cancer

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Type Insights

The x-ray based segment is estimated to witness significant growth during the forecast period.

The X-ray-based segment, centered on linear accelerator technology, is foundational to the radiosurgery and radiotherapy robotics market. These systems are preferred for their operational versatility and for avoiding the logistical complexities of radioactive source management.

The integration of robotic arms and advanced couches enables non-isocentric beam delivery with sub-millimeter treatment accuracy, crucial for stereotactic body radiation therapy. Advanced platforms now incorporate real-time tumor tracking and motion management solutions to treat targets in mobile organs.

Innovations in adaptive radiotherapy planning allow for on-the-fly adjustments, with some systems demonstrating a 15% improvement in dose conformity to the target volume.

This capability, combined with hypofractionated radiotherapy schedules, enhances patient treatment throughput, making these systems a cost-effective cornerstone for specialized oncology centers.

The X-ray based segment was valued at USD 2.62 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

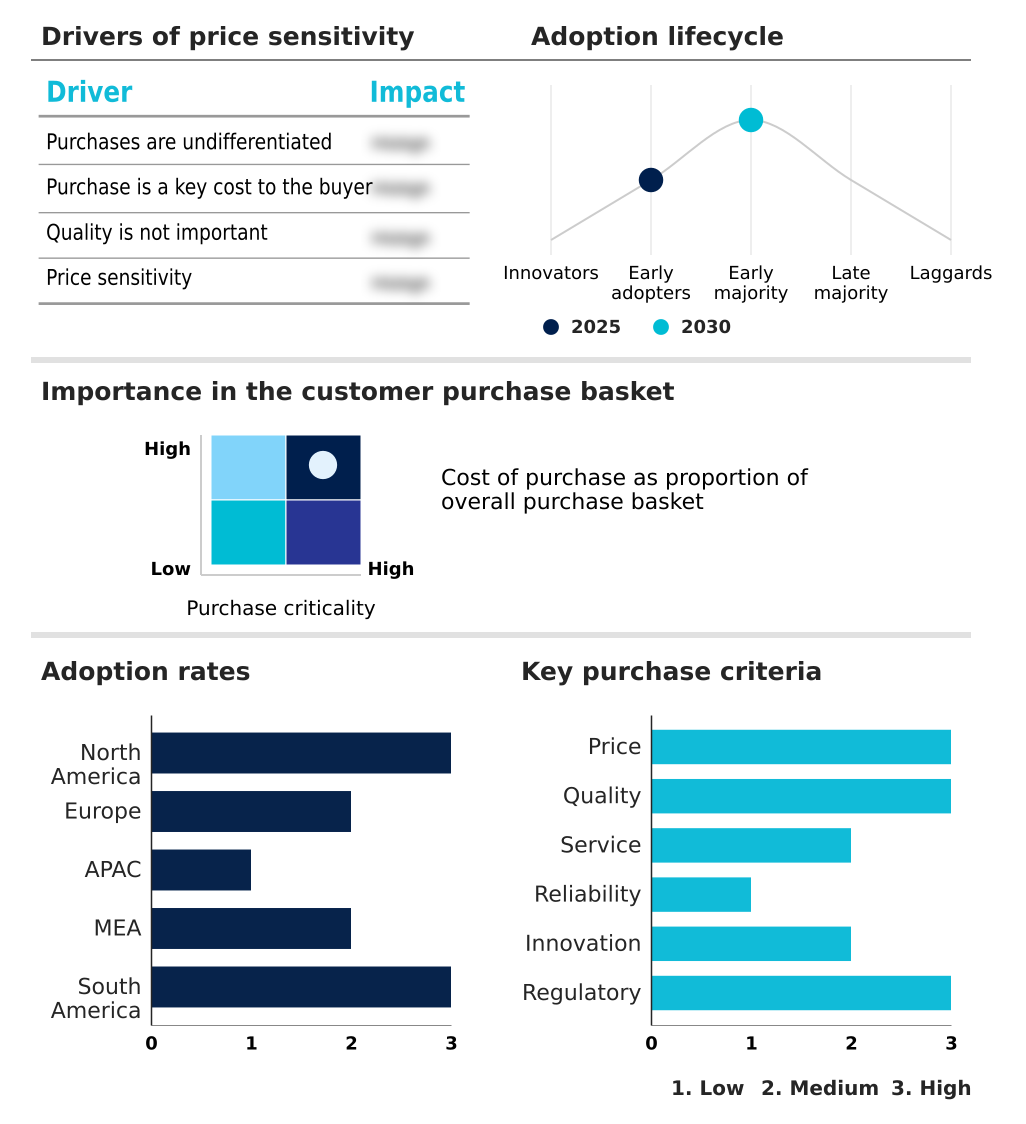

North America is estimated to contribute 38.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Radiosurgery And Radiotherapy Robotics Market Demand is Rising in North America Get Free Sample

The global geographic landscape is led by North America, which is projected to contribute 38% of the market's incremental growth, driven by its advanced healthcare infrastructure modernization and high adoption rate of precision oncology platforms.

Europe follows, with countries like Germany and the UK investing in linear accelerator technology and mr-guided radiotherapy. Meanwhile, the APAC region is the fastest-growing, with a CAGR of 6.6%, fueled by rising healthcare expenditure in China and India.

This growth supports the build-out of specialized oncology centers and the adoption of technologies like stereotactic ablative radiotherapy.

In contrast, adoption in South America and the Middle East and Africa is more fragmented, often limited to major urban centers and dependent on both public funding and private investment in capital equipment procurement for robotic cancer care.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the radiosurgery and radiotherapy robotics market is increasingly influenced by detailed evaluations of specific clinical applications and technologies. For example, the cost-effectiveness of robotic radiosurgery is a key consideration, with analyses often comparing LINAC SRS and Gamma Knife to determine the optimal platform for different intracranial indications.

- For extracranial targets, SBRT for early-stage lung cancer has become a standard of care, where effective motion management in prostate radiotherapy is crucial for minimizing toxicity. The complexity of adaptive planning for head and neck cancer highlights the need for advanced software and imaging.

- While proton therapy for pediatric tumors offers distinct advantages, the challenges in commissioning MR-LINAC systems can delay implementation. Improving workflow efficiency in radiosurgery centers is a constant goal, as is reducing toxicity with robotic SBRT to enhance patient outcomes with non-invasive SRS.

- The application of robotic radiotherapy for liver metastases is growing, though reimbursement policies for stereotactic radiosurgery remain a critical factor. Furthermore, the extensive training requirements for robotic radiotherapy and the need for rigorous quality assurance for robotic radiotherapy are significant operational considerations for healthcare providers.

- The integration of AI in treatment planning is seen as a pivotal step in managing the role of robotics in re-irradiation cases and improving overall treatment delivery.

What are the key market drivers leading to the rise in the adoption of Radiosurgery And Radiotherapy Robotics Industry?

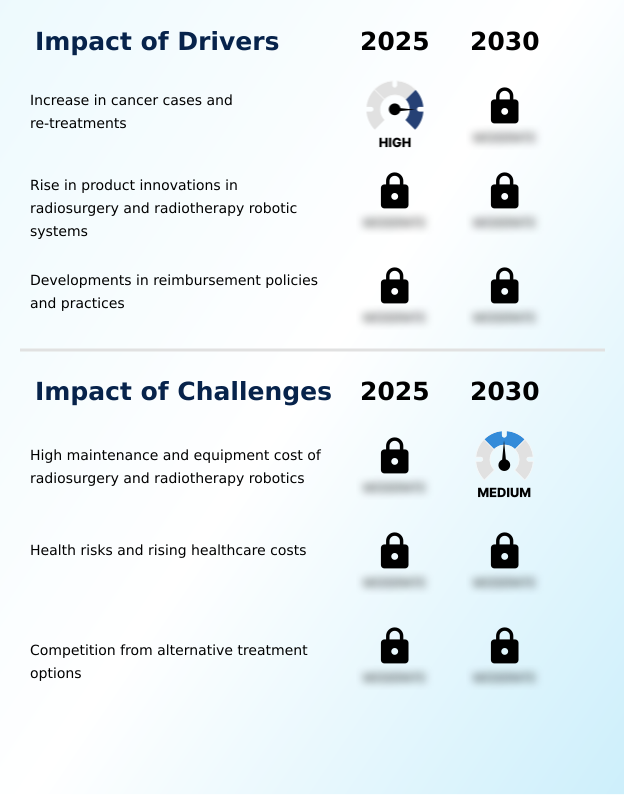

- The rising global incidence of cancer and a growing number of cases requiring retreatment are key drivers fueling the demand for advanced radiosurgery and radiotherapy solutions.

- Market growth is fundamentally driven by the rising global cancer incidence and the increasing demand for non-invasive tumor treatment options.

- Product innovations are reshaping the landscape, with a focus on integrating high-definition imaging and real-time tumor tracking into precision oncology platforms. This allows for the safe delivery of a higher therapeutic radiation dose.

- The development of more favorable reimbursement policies is also accelerating adoption, making advanced robotic cancer care more accessible.

- For instance, streamlined medical device regulation in key markets has reduced approval times by up to 30%, speeding the availability of new technologies.

- These factors combined are expanding the use of stereotactic body radiation therapy and other advanced modalities, meeting the needs of a growing patient population.

What are the market trends shaping the Radiosurgery And Radiotherapy Robotics Industry?

- The emergence of advanced radiotherapy treatments, such as intensity-modulated and image-guided therapies, represents a significant market trend. These innovations are enhancing treatment precision and overall patient safety.

- The market is advancing through the adoption of sophisticated technologies that enhance treatment precision and patient safety. Innovations like volumetric modulated arc therapy and image-guided radiotherapy are becoming standard, enabling high-precision radiation delivery to tumors while minimizing exposure to healthy tissue.

- The growing demand for extracranial radiosurgery applications is driving the development of robotic systems capable of sub-millimeter treatment accuracy for organs such as the liver and lung. This trend is supported by advanced radiotherapy techniques, with some centers reporting a 20% reduction in treatment-related side effects for complex cases.

- Furthermore, the integration of AI is optimizing radiation oncology workflow, leading to faster and more accurate radiosurgery treatment planning. This focus on both efficacy and efficiency is reshaping clinical treatment protocols globally.

What challenges does the Radiosurgery And Radiotherapy Robotics Industry face during its growth?

- The substantial equipment and maintenance costs associated with radiosurgery and radiotherapy robotics present a key challenge that can hinder widespread market adoption and growth.

- The high cost of capital equipment procurement and maintenance remains a significant barrier to market expansion, particularly in emerging economies with limited healthcare infrastructure modernization. Hospitals face substantial upfront investments, and recurring expenses for service and training further strain budgets.

- This financial pressure is compounded by competition from alternative treatments like brachytherapy and proton therapy, which are sometimes perceived as more cost-effective for certain indications. The complexity of these robotic systems also necessitates specialized expertise, creating a skills gap in some regions.

- Consequently, despite the proven benefits of high-precision radiation delivery, which can reduce certain long-term toxicities by 15%, cost and operational hurdles limit widespread adoption.

Exclusive Technavio Analysis on Customer Landscape

The radiosurgery and radiotherapy robotics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the radiosurgery and radiotherapy robotics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Radiosurgery And Radiotherapy Robotics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, radiosurgery and radiotherapy robotics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accuray Inc. - Key offerings include advanced robotic platforms for radiosurgery and radiotherapy, designed to deliver non-invasive, high-precision tumor treatments with enhanced accuracy and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accuray Inc.

- Advanced Oncotherapy plc

- Best Medical International Inc.

- Brainlab AG

- Elekta AB

- Hitachi Ltd.

- Mevion Medical Systems Inc.

- Mitsubishi Electric Corp.

- Neusoft Corp.

- Optivus Proton Therapy Inc.

- Panacea Medical Tech Pvt. Ltd.

- PMB Alcen

- ProTom Holding Corp.

- Siemens Healthineers AG

- Varian Medical Systems Inc.

- ViewRay Inc.

- ZAP Surgical Systems Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Radiosurgery and radiotherapy robotics market

- In May 2025, Elekta AB presented preliminary results from the ERECT clinical trial at the ESTRO annual congress, demonstrating that its 1.5T Elekta Unity MR-Linac significantly reduced erectile dysfunction in prostate cancer patients by enabling precise visualization and sparing of neurovascular structures.

- In July 2025, Elekta received U.S. FDA 510(k) clearance for its Leksell Gamma Knife radiosurgery system to treat refractory, intractable mesial temporal lobe epilepsy, expanding its application beyond traditional oncology.

- In September 2025, Varian, a Siemens Healthineers company, announced significant enhancements to its Halcyon treatment platform, including the PerfectKinetix Dynamic Couch and improved real-time imaging capabilities, designed to improve motion management and treatment accuracy.

- In November 2025, ZAP Surgical Systems Inc. received United States Food and Drug Administration 510(k) clearance and European CE certification for its ZAP Axon Radiosurgery Planning System, streamlining workflow for its vault-free cranial robotic radiosurgery platform.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Radiosurgery And Radiotherapy Robotics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.6% |

| Market growth 2026-2030 | USD 1027.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The radiosurgery and radiotherapy robotics market is characterized by intense technological competition, where leadership is defined by the ability to enhance clinical outcomes through superior precision. The field is advancing beyond incremental hardware updates toward integrated ecosystems that combine linear accelerator technology with sophisticated software for adaptive radiotherapy planning and real-time tumor tracking.

- Key differentiators include motion management solutions that enable complex procedures like stereotactic body radiation therapy and hypofractionated radiotherapy with exceptional accuracy. For instance, systems now feature fiducial-free tracking and respiratory motion synchronization, which are critical for neoadjuvant radiotherapy and treating mobile tumors. The adoption of mr-guided radiotherapy and biology-guided radiotherapy reflects a strategic shift toward personalized medicine.

- In this environment, boardroom decisions increasingly focus on investing in platforms that offer not just technical superiority in dose distribution optimization but also demonstrable improvements in patient throughput and reduced radiation-induced toxicity, with some providers reporting a 20% increase in treatment capacity after upgrading to the latest robotic platforms. This focus on verifiable ROI is shaping procurement strategies globally.

What are the Key Data Covered in this Radiosurgery And Radiotherapy Robotics Market Research and Growth Report?

-

What is the expected growth of the Radiosurgery And Radiotherapy Robotics Market between 2026 and 2030?

-

USD 1.03 billion, at a CAGR of 5.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (X-ray based, and Gamma-ray based), End-user (Hospitals, Clinics, and Independent radiotherapy centers), Application (Lung cancer, Prostate cancer, Breast cancer, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increase in cancer cases and re-treatments, High maintenance and equipment cost of radiosurgery and radiotherapy robotics

-

-

Who are the major players in the Radiosurgery And Radiotherapy Robotics Market?

-

Accuray Inc., Advanced Oncotherapy plc, Best Medical International Inc., Brainlab AG, Elekta AB, Hitachi Ltd., Mevion Medical Systems Inc., Mitsubishi Electric Corp., Neusoft Corp., Optivus Proton Therapy Inc., Panacea Medical Tech Pvt. Ltd., PMB Alcen, ProTom Holding Corp., Siemens Healthineers AG, Varian Medical Systems Inc., ViewRay Inc. and ZAP Surgical Systems Inc.

-

Market Research Insights

- The market dynamics are shaped by a strategic push toward value-based healthcare, where precision oncology platforms are critical. The adoption of advanced radiotherapy techniques is enabling some facilities to reduce average treatment times by up to 25%, directly boosting patient treatment throughput. This efficiency is paramount as capital equipment procurement decisions are increasingly scrutinized for return on investment.

- Furthermore, the integration of oncology informatics into the radiation oncology workflow improves clinical trial validation and protocol adherence, with some systems showing a 15% reduction in planning errors. This focus on verifiable outcomes and operational excellence defines the competitive landscape, pushing providers toward holistic robotic cancer care solutions that optimize every step of the cancer care continuum.

We can help! Our analysts can customize this radiosurgery and radiotherapy robotics market research report to meet your requirements.

RIA -

RIA -