Rheumatoid Arthritis Drugs Market Size 2024-2028

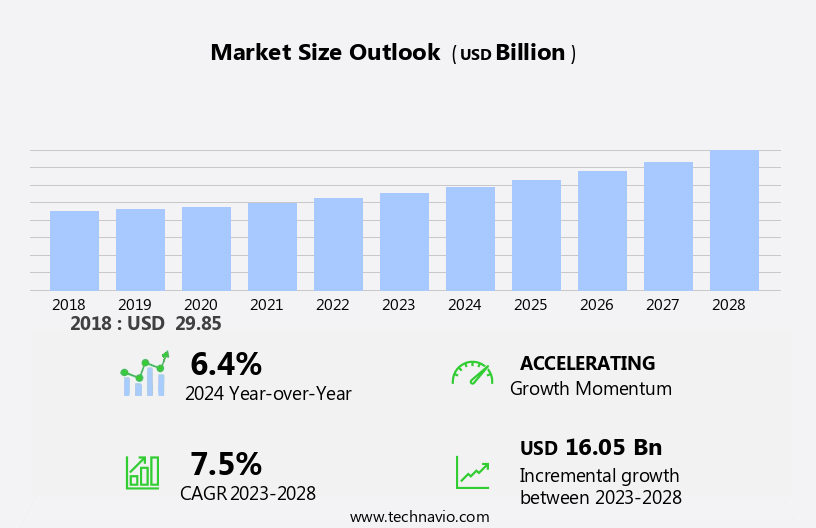

The rheumatoid arthritis drugs market size is forecast to increase by USD 16.05 billion at a CAGR of 7.5% between 2023 and 2028.

- The market is experiencing significant growth due to several economic and healthcare factors. The increasing number of RA cases and the focus on improving patient outcomes through early diagnosis and treatment are key drivers. Additionally, an increasing number of rheumatologists and health plans offering coverage for RA treatments are contributing to market growth. The market is evolving with the integration of biotech innovations and advanced analytics, which are helping to accelerate drug development and improve personalized treatment options for patients. However, challenges persist in the form of patient non-adherence to treatment, regulatory factors, and legal requirements. ISO management and environmental regulations are crucial considerations for chemical process professionals in the production of RA drugs. Compliance with these regulations and legal requirements can be costly and time-consuming, but failure to do so can result in significant consequences. Industry professionals need to stay informed of the latest regulatory and legal developments to ensure their organizations remain competitive and compliant.

What will be the Size of the Rheumatoid Arthritis Drugs Market During the Forecast Period?

- The market is witnessing significant advancements driven by the integration of technology and innovation in the pharmaceutical sector. The market is characterized by a focus on enhancing drug design, molecular modeling, and chemical analysis to develop effective treatments for RA. Chemistry plays a pivotal role in the development of RA drugs. Computer programs and molecular modeling are extensively used to simulate and analyze chemical reactions, enabling the design of new drugs with improved efficacy and reduced side effects. Molecular dynamics and quantum chemistry are advanced techniques that are gaining popularity in the industry due to their ability to provide insights into the behavior of molecules at the atomic level.

- Data management is another critical aspect of the RA drugs market. Digitalization and automation have led to the adoption of cloud computing for storing and analyzing large datasets. This enables researchers to access real-time data and collaborate with their colleagues, leading to faster and more efficient drug development. Remote monitoring and data analytics are also transforming the RA drugs market. These technologies enable real-time monitoring of patients and their response to treatment, allowing for personalized care and improved patient outcomes. Collaboration tools facilitate communication and information sharing among healthcare professionals, leading to better coordinated care and improved patient outcomes.

How is this Rheumatoid Arthritis Drugs Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Drug Class

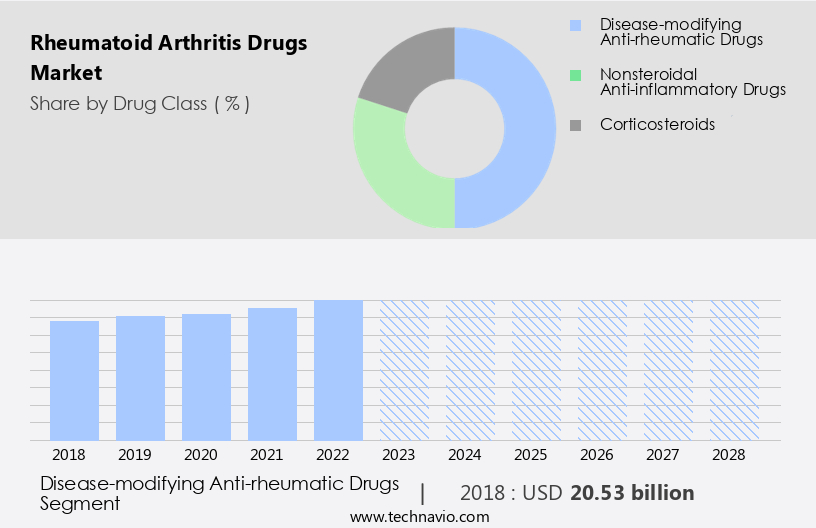

- Disease-modifying anti-rheumatic drugs

- Nonsteroidal anti-inflammatory drugs

- Corticosteroids

- Type

- Biologics

- Small Molecules

- Geography

- North America

- US

- Europe

- Germany

- UK

- France

- Asia

- China

- Rest of World (ROW)

- North America

By Drug Class Insights

- The disease-modifying anti-rheumatic drugs segment is estimated to witness significant growth during the forecast period. Investment in the research and development of disease-modifying anti-rheumatic drugs (DMARDs) for rheumatoid arthritis continues to be a priority in the pharmaceutical industry. DMARDs, such as methotrexate, sulfasalazine, leflunomide, etanercept, and infliximab, have proven to not only alleviate the symptoms of active rheumatoid arthritis but also influence the course of the disease and improve radiological outcomes. These drugs act at the cellular level to inhibit the immune system's inflammatory response. The use of advanced technologies like chemistry, computer programs, molecular modeling, chemical analysis, data management, and laboratory automation has significantly enhanced the innovation in the development of DMARDs. Early diagnosis and treatment with DMARDs are crucial in preventing the progression of rheumatoid arthritis and minimizing the risk of irreversible joint damage.

- When rheumatoid arthritis is diagnosed, initiating DMARD therapy is typically recommended. This proactive approach can slow or halt the disease's progression and reduce the likelihood of debilitating, persistent joint damage. The unique mechanisms of action of each DMARD make them effective in managing rheumatoid arthritis, making them essential components of treatment regimens. Investors and pharmaceutical companies are increasingly focusing on the development of DMARDs to address the unmet medical needs of rheumatoid arthritis patients. The market for these drugs is expected to grow steadily due to the increasing prevalence of rheumatoid arthritis and the need for effective treatment options.

Get a glance at the market report of share of various segments Request Free Sample

The Disease-modifying anti-rheumatic drugs segment was valued at USD 20.53 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

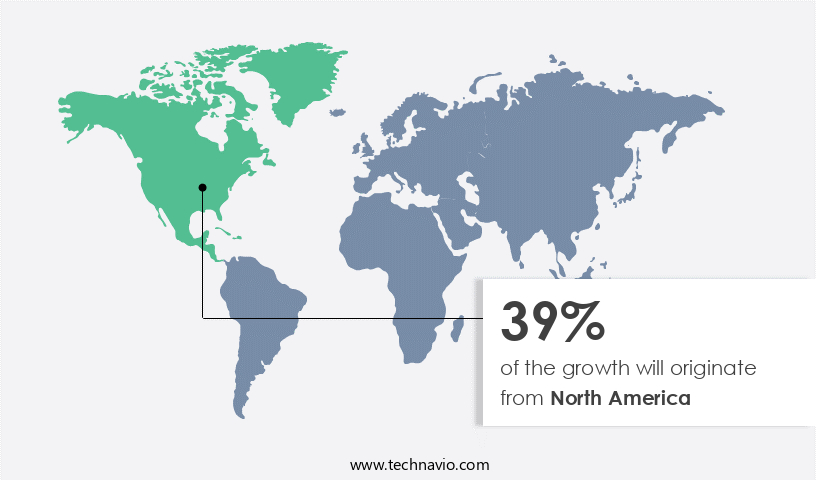

- North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

In North America, the market holds a substantial share due to the presence of major players. The market expansion will primarily be driven by the introduction of novel biologics during the forecast period. However, the adoption of biosimilars will not be observed within the given timeframe. In terms of best business practices, cost-effectiveness, data security, safety standards, environmental impact, process optimization, inventory management, supply chain visibility, and predictive analytics are crucial elements for market success. Ensuring these aspects are addressed will enable companies to maintain a competitive edge in the RA Drugs Market.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Rheumatoid Arthritis Drugs Industry?

- Rising cases of RA and a focus on increasing the number of rheumatologists is the key driver of the market. Rheumatoid Arthritis (RA) is a widespread condition affecting an estimated 17.6 million individuals worldwide, as reported by the National Library of Medicine. The global age-standardized prevalence rate of RA was 208.8 cases per 100,000 population in 2020. The significant number of RA cases is anticipated to fuel the expansion of the market. Furthermore, according to the Centers for Disease Control and Prevention, there is a pressing requirement to expand the healthcare workforce, specifically in the field of rheumatology.

- Rheumatologists, who specialize in diagnosing and managing joint, muscle, and bone diseases, are in high demand. This need for skilled healthcare professionals underscores the importance of the market. In the market, the integration of legacy software systems in the healthcare sector and the increasing disposable incomes of consumers are key factors driving the growth of the market. The use of specialty chemicals and petrochemicals in the production of these drugs is also a significant trend.

What are the market trends shaping the Rheumatoid Arthritis Drugs Industry?

- Health plan offerings for RA is the upcoming market trend. In the United States, the expense of managing Rheumatoid Arthritis (RA) continues to escalate, despite regulatory efforts to contain costs. The cost of popular RA treatments, such as HUMIRA and Enbrel, has risen significantly. For instance, the wholesale price of HUMIRA has nearly doubled, increasing by approximately 65% in the US market. Although non-biologic drugs like NSAIDs have lower prices, their long-term use can lead to substantial health burdens. The high cost of RA treatment is a significant concern for patients and healthcare providers.

- The escalating prices of RA drugs necessitate ongoing dialogue between stakeholders, including regulatory bodies, pharmaceutical companies, and healthcare providers, to find cost-effective solutions while ensuring the best possible patient care.

What challenges does the Rheumatoid Arthritis Drugs Industry face during its growth?

- Patient nonadherence to treatment is a key challenge affecting the industry growth. In the economic landscape of Rheumatoid Arthritis (RA) drug therapy, ensuring patient adherence to treatment is a significant challenge. According to research, approximately 30-80% of RA patients do not fully comply with their prescribed medication regimens. This non adherence can be attributed to various factors, including patients' beliefs about medication, self-medication, and altering dosages without consulting healthcare professionals. Treatment adherence is crucial for achieving the full therapeutic benefit of drugs. It encompasses the initiation of medication, adherence to the prescribed dosing schedule, and proper discontinuation. The chemical process of RA drug production must adhere to stringent regulatory and legal factors, including ISO management and environmental regulations.

- These requirements ensure the safety and efficacy of the drugs. As chemical professionals, it is essential to recognize the importance of patient adherence in the RA drug market. By addressing the root causes of nonadherence, such as improving patient education and communication, we can enhance the overall effectiveness of RA drug therapy. This, in turn, can lead to better patient outcomes and reduced healthcare costs. Maintaining a professional and formal tone, it is essential to acknowledge the importance of patient adherence in the RA drug market. Approximately 30-80% of RA patients do not fully comply with their prescribed medication regimens, which can be attributed to various factors, including patients' beliefs about medication, self-medication, and altering dosages without consulting healthcare professionals.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Amgen Inc.

- Astellas Pharma Inc.

- Bristol Myers Squibb Co.

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- Galmed Pharmaceuticals Ltd.

- Genor Biopharma Holdings Ltd.

- Gilde Healthcare

- Gilead Sciences Inc.

- GlaxoSmithKline Plc

- Johnson and Johnson

- Kangstem Biotech Co. Ltd.

- Novartis AG

- Oryn Therapeutics

- Pfizer Inc.

- Sanofi

- Sorrento Therapeutics Inc.

- Taisho Pharmaceutical Holdings Co. Ltd.

- UCB SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth due to the increasing prevalence of rheumatoid arthritis and the ongoing research and development in advanced technologies for drug design and manufacturing. The market is driven by innovation and investment in chemistry, computer programs, molecular modeling, and chemical analysis. Leading companies are focusing on digitalization and automation to enhance process optimization, inventory management, and supply chain visibility. Advanced technologies such as molecular dynamics, quantum chemistry, and digitalization are revolutionizing the industry by enabling remote monitoring, data analytics, collaboration tools, and cloud computing. These technologies offer scalability, flexibility, cost-effectiveness, data security, safety standards, and environmental impact reduction.

Moreover, the market is competitive, with companies adopting various pricing strategies to gain a competitive edge. Factors influencing the market include regulatory factors, legal requirements, and environmental regulations. Chemical professionals are increasingly focusing on ISO management and regulatory compliance to ensure the safety and efficacy of rheumatoid arthritis drugs. Despite the challenges of legacy software integration issues and the high cost of advanced technologies, the market is expected to grow significantly due to the increasing disposable incomes of consumers in the consumer goods, automobiles, and petrochemicals industries. The market is also driven by the potential for new drug discoveries and the increasing demand for specialty chemicals.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

162 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.5% |

|

Market growth 2024-2028 |

USD 16.05 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.4 |

|

Key countries |

US, UK, Germany, France, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Rheumatoid Arthritis Drugs Market Research and Growth Report?

- CAGR of the Rheumatoid Arthritis Drugs industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the rheumatoid arthritis drugs market growth of industry companies

We can help! Our analysts can customize this rheumatoid arthritis drugs market research report to meet your requirements.

RIA -

RIA -