Semiconductor Chip Packaging Market Size 2024-2028

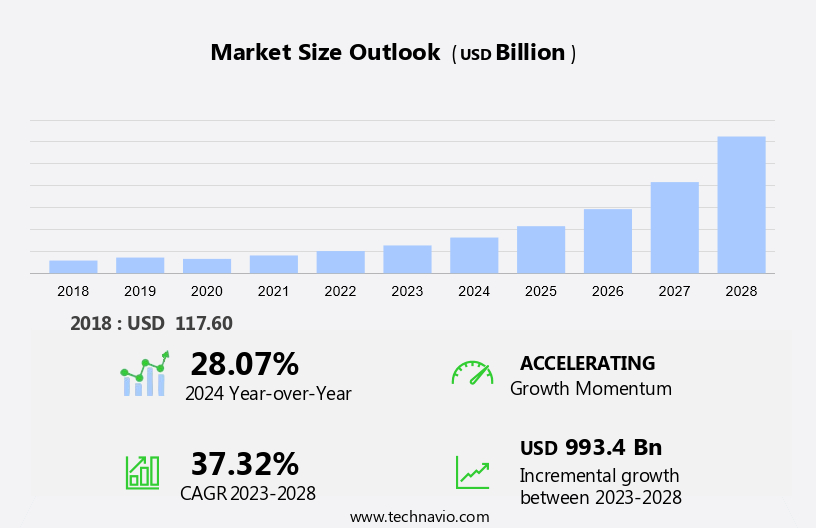

The semiconductor chip packaging market size is forecast to increase by USD 993.4 billion at a CAGR of 37.32% between 2023 and 2028. The market is experiencing significant growth due to the increasing demand for advanced semiconductor components in various industries. Integrated circuits are essential in technologies such as autonomous vehicles, laptops, smartwatches, and more. Packaging materials play a crucial role in protecting these sensitive components, ensuring electrical insulation and providing mechanical support. Key market trends include the adoption of display technologies and sensor technologies, which require advanced packaging solutions. The growing investment in lower technology nodes and fabrication facilities necessitates the development of new packaging materials and techniques. However, the high initial investment required for these advanced packaging solutions presents a challenge for market growth.

Moreover, in the market, the demand for semiconductor packaging is driven by the need for miniaturization, increased performance, and reliability in various applications. The integration of sensor technologies and display technologies in consumer electronics and automotive industries is expected to fuel market growth. The use of advanced materials, such as organic substrates and advanced interconnect technologies, is essential to meet the evolving demands of these industries. In summary, the market is experiencing growth due to the increasing demand for advanced semiconductor components in various industries. Packaging materials play a crucial role in protecting these components while ensuring electrical insulation and mechanical support.

The semiconductor packaging market is witnessing significant advancements due to the increasing demand for miniaturization, higher power densities, and improved thermal management in various sectors, including consumer electronics, automotive, and high-performance computing. In the consumer electronics segment, the growth is driven by the escalating demand for smartphones and tablets. Advanced packaging techniques, such as fan-out wafer-level packaging (FOWLP) and system-in-package (SiP), are increasingly being adopted to address the challenges of miniaturization and power efficiency in these devices. The electric vehicle (EV) and autonomous driving sectors are also fueling the semiconductor packaging market growth.

Moreover, advanced packaging solutions, like advanced interposers and 3D packaging, are essential for the integration of high-performance semiconductor components in EVs and autonomous driving systems. Artificial intelligence (AI) and the Internet of Things (IoT) are other significant applications contributing to the market expansion. High-frequency applications, such as 5G networks and satellite communications, also require advanced packaging techniques to ensure signal integrity and thermal management. High-performance computing and data processing applications, like supercomputers and data centers, necessitate advanced packaging solutions to address power densities and thermal management challenges. Integrated cooling mechanisms, such as micro-channel cooling and liquid cooling, are increasingly being used to maintain optimal operating temperatures.

Similarly, in the automotive sector, semiconductor packaging plays a crucial role in the development of advanced driver assistance systems (ADAS) and automotive electronics. Packaging materials, such as encapsulation resins, electrical insulation, and mechanical support, are essential for the production of lead frames and other critical components. Display technologies and sensor technologies also rely on advanced semiconductor packaging solutions. These applications require high reliability, low power consumption, and efficient thermal management to meet the evolving demands of the market. In conclusion, the semiconductor packaging market is experiencing continuous growth due to the increasing demand for miniaturization, higher power densities, and improved thermal management in various sectors, including consumer electronics, automotive, and high-performance computing.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

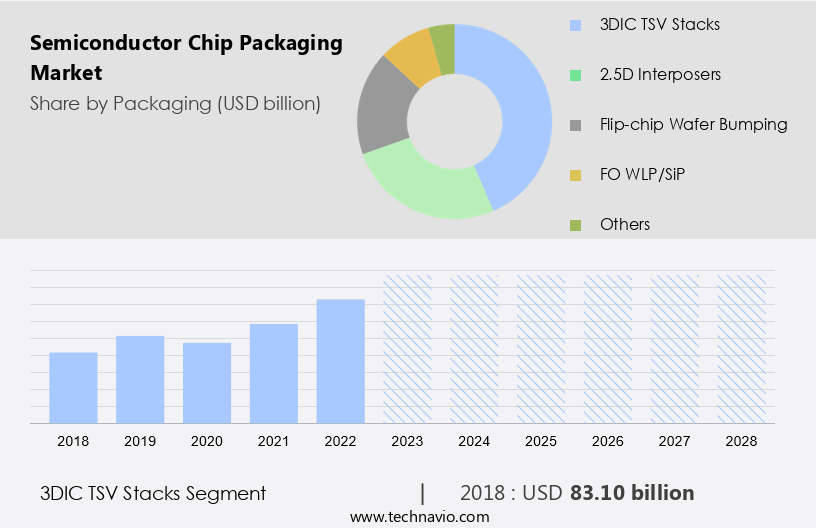

- Packaging

- 3DIC TSV stacks

- 2.5D interposers

- Flip-chip wafer bumping

- FO WLP/SiP

- Others

- End-user

- OSATs

- IDMs

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Europe

- South America

- Middle East and Africa

- APAC

By Packaging Insights

The 3DIC TSV stacks segment segment is estimated to witness significant growth during the forecast period. The semiconductor packaging market is experiencing significant growth due to the increasing demand for advanced technology in consumer electronics. Three-Dimensional Interconnect (3DIC) Through-Silicon Via (TSV) technology is a crucial solution for enhancing functionality, performance, and integration in high-end applications. This technology is particularly important for devices such as smartphones, tablets, electric vehicles, and those involved in autonomous driving, artificial intelligence, and the Internet of Things. The use of TSV platforms is gaining momentum due to the need for smaller form factors and cost reduction. In the future, this technology is expected to be utilized for applications including photonics and LED function integration.

Moreover, consequently, the demand for 3DIC TSV stacks is projected to increase, leading to market growth during the forecast period. Key industries driving this trend include consumer electronics, automotive, and industrial. 3DIC TSV technology is essential for memory applications, heterogeneous interconnection with CMOS Image Sensors (CIS), micro-electromechanical systems (MEMS), sensors, radio frequency (RF) filters, and performance applications.

Get a glance at the market share of various segments Request Free Sample

The 3DIC TSV stacks segment was valued at USD 83.10 billion in 2018 and showed a gradual increase during the forecast period.

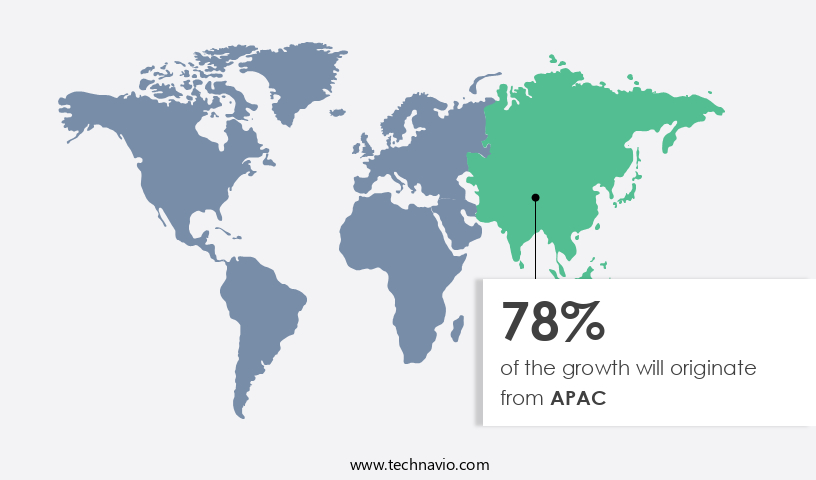

Regional Insights

APAC is estimated to contribute 78% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in the Asia Pacific (APAC) region is experiencing substantial growth due to the presence of numerous semiconductor manufacturing facilities. Leading semiconductor foundries, including Taiwan Semiconductor Manufacturing, United Microelectronics, Samsung, and Semiconductor Manufacturing International, are significantly contributing to the market expansion in APAC. These companies are investing heavily in the region to establish new fabrication plants. The increasing demand for electronic devices, particularly in countries like China, Japan, South Korea, and Taiwan, has led to significant growth in the APAC market.

Moreover, power densities and thermal management are critical considerations in semiconductor chip packaging, with integrated cooling mechanisms becoming increasingly important. Advanced chip designs, such as FinFET transistors and heterogeneous integration, are also driving market growth. The APAC market is witnessing significant growth due to the increasing demand for electronic devices, particularly in automotive electronics, advanced driver assistance systems, and infotainment systems. Semiconductor chip packaging plays a crucial role in ensuring signal integrity and thermal management for these advanced applications. The market is expected to continue its growth trajectory due to the ongoing innovation in semiconductor technology and the increasing demand for electronic devices in various industries.

Market Driver

Growing investment in fabrication facilities is the key driver of the market. The market is witnessing significant growth due to the increasing demand for smart devices, wearable technology, and the defense sector. Electromagnetic interference (EMI) and electromagnetic compatibility (EMC) are crucial factors driving the market's expansion, as plastic materials are increasingly used for IC packaging to ensure EMI shielding. The defense sector, fueled by military expenditure, is a major consumer of semiconductor chips, leading to increased demand for advanced packaging solutions. Densification is a key trend in the semiconductor industry, with companies investing in new fabrication facilities to increase production capacity.

According to Semiconductor Equipment and Materials International (SEMI), chipmakers are expected to invest over USD500 billion in 84 global facilities by 2024. This investment includes 23 new chipmaking facilities that started construction in 2021, followed by 33 in 2022 and 28 in 2023. The growing adoption of 5G technology and the Internet of Things (IoT) is further boosting the market. The rising demand for 3D NAND has created opportunities for supply chain members, including chipmakers, equipment manufacturers, and material suppliers. As the industry continues to evolve, companies must focus on providing advanced packaging solutions to meet the demands of the market.

Market Trends

Growing investments in lower technology nodes is the upcoming trend in the market. The semiconductor industry is witnessing significant advancements as manufacturers strive to create smaller, more efficient chips. Semiconductor foundries and Integrated Device Manufacturers (IDMs) are investing heavily in research and development to identify technologies that can support the production of smaller process nodes, adhering to Moore's law which predicts a doubling of transistors in integrated circuits every two years. To achieve high performance, scalability, and cost efficiency, semiconductor manufacturers are employing innovative technologies like Fin Field Effect Transistors (FinFET) and Fully Depleted Silicon on Insulator (FD-SOI). Moreover, the semiconductor packaging market is evolving rapidly, with a focus on advanced packaging solutions.

Moreover, leadframes, encapsulation resins, and thermal interface materials are essential components of semiconductor chip packaging. Product obsolescence and intellectual property concerns necessitate the adoption of advanced packaging technologies. Outsourcing of packaging processes and testing are also common practices in the industry. Machine learning algorithms are increasingly being used to optimize semiconductor manufacturing processes, including packaging. Small Outline Packages (SOP) and Surface Mount Technology (SMT) are popular packaging techniques for modern semiconductors. These packaging methods offer advantages such as reduced size, improved thermal management, and increased reliability. As the semiconductor industry continues to evolve, manufacturers must stay abreast of the latest packaging technologies and trends to remain competitive.

Market Challenge

High initial investment is a key challenge affecting the market growth. The market is witnessing significant transformation due to the increasing demand for advanced semiconductor components in various industries, including autonomous vehicles, laptops, smartwatches, and more. The manufacturing process of these components involves intricate packaging solutions, such as through-silicon via (TSV), stacked packaging, and micro-electromechanical systems (MEMS) packaging, which require advanced packaging materials for electrical insulation and mechanical support.

Furthermore, these materials and manufacturing processes are complex and time-consuming, leading to increased production costs. Moreover, the rapid advancements in display technologies and sensor technologies further add to the complexity of semiconductor manufacturing. As a result, semiconductor companies are investing heavily in efficient manufacturing equipment to keep up with the technological changes.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

3M Co.: The company offers semiconductor chip packaging such as 3M Heat Resistive Polyimide Tapes which are specially formulated for different high-temperature and chemical processes.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amkor Technology Inc.

- Applied Materials Inc.

- ASE Technology Holding Co. Ltd.

- ASMPT Ltd.

- ChipMOS TECHNOLOGIES INC.

- GlobalFoundaries Inc.

- Jiangsu Changdian Technology Co. Ltd.

- Kulicke and Soffa Industries Inc.

- Microchip Technology Inc.

- nepes Corp.

- Powertech Technology Inc.

- Skywater Technology

- SUSS MICROTEC SE

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Tokyo Electron Ltd.

- Unisem M Berhad

- UTAC Holdings Ltd.

- Veeco Instruments Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Semiconductor packaging plays a crucial role in the electronics industry, particularly in consumer electronics such as smartphones and tablets. Advanced packaging techniques, including system in package, miniaturization, 3D packaging, and organic substrates, are driving innovation in this market. The increasing adoption of artificial intelligence, the Internet of Things, and advanced technologies in consumer electronics, electric vehicles, autonomous driving, and telecommunications is fueling the demand for semiconductor packaging. Advanced packaging materials, such as advanced encapsulation resins, bonding wire, ceramic packages, and die attach materials, are essential for improving thermal and electrical performance. Traditional packaging methods, like flip chips, continue to be used in various applications, while new technologies like heterogeneous integration and finFET transistors are gaining popularity.

Moreover, the aerospace and defense sector also relies heavily on semiconductor packaging for high-reliability applications. Production-linked incentives and thermal management solutions, including integrated cooling mechanisms, are crucial considerations for this market. The semiconductor packaging market is also impacted by trends such as smart manufacturing, high-frequency applications, high-performance computing, data processing, and digitalization. Power densities, signal integrity, electromagnetic interference, and electromagnetic compatibility are critical factors in the design and production of advanced semiconductor components. The automotive electronics market, including advanced driver assistance systems, infotainment systems, and electric vehicles, is a significant growth area for semiconductor packaging. Plastic materials, lead frames, encapsulation resins, and thermal interface materials are essential components in this market.

Similarly, product obsolescence, intellectual property concerns, outsourcing, testing processes, machine learning, and small outline packages are some of the challenges facing the semiconductor packaging industry. Electronics manufacturing hubs and foreign investments are key drivers for market growth. In summary, the semiconductor packaging market is a dynamic and evolving industry, driven by technological advancements and the increasing adoption of electronics in various sectors, including consumer electronics, automotive, aerospace and defense, and telecommunications. Advanced packaging techniques, materials, and manufacturing processes are essential for addressing the challenges and opportunities in this market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 37.32% |

|

Market Growth 2024-2028 |

USD 993.4 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

28.07 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 78% |

|

Key countries |

China, US, Taiwan, Japan, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

3M Co., Amkor Technology Inc., Applied Materials Inc., ASE Technology Holding Co. Ltd., ASMPT Ltd., ChipMOS TECHNOLOGIES INC., GlobalFoundaries Inc., Jiangsu Changdian Technology Co. Ltd., Kulicke and Soffa Industries Inc., Microchip Technology Inc., nepes Corp., Powertech Technology Inc., Skywater Technology, SUSS MICROTEC SE, Taiwan Semiconductor Manufacturing Co. Ltd., Tokyo Electron Ltd., Unisem M Berhad, UTAC Holdings Ltd., and Veeco Instruments Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- A thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -