Semiconductor In Military And Aerospace Market Size 2025-2029

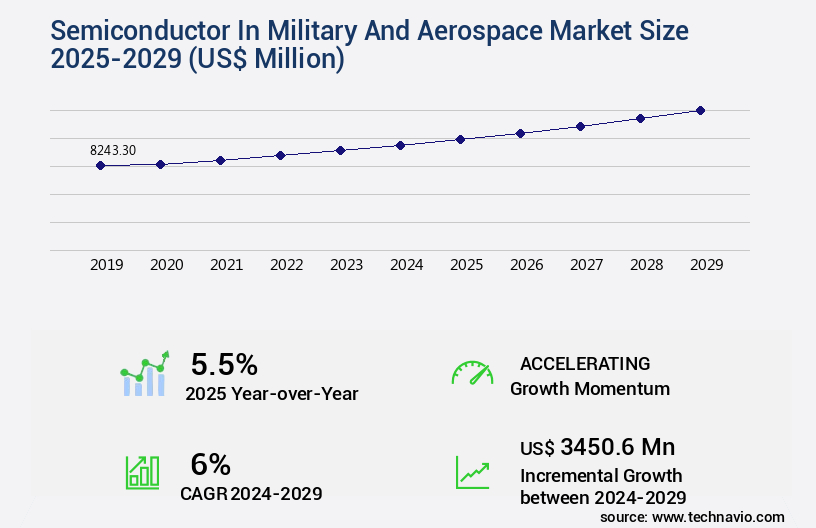

The semiconductor in military and aerospace market size is valued to increase by USD 3.45 billion, at a CAGR of 6% from 2024 to 2029. Increased upgrading and modernization of aircraft will drive the semiconductor in military and aerospace market.

Major Market Trends & Insights

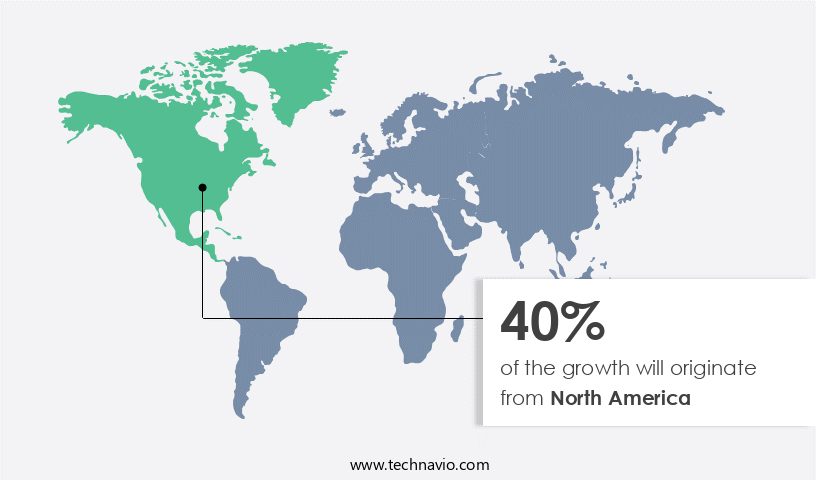

- North America dominated the market and accounted for a 40% growth during the forecast period.

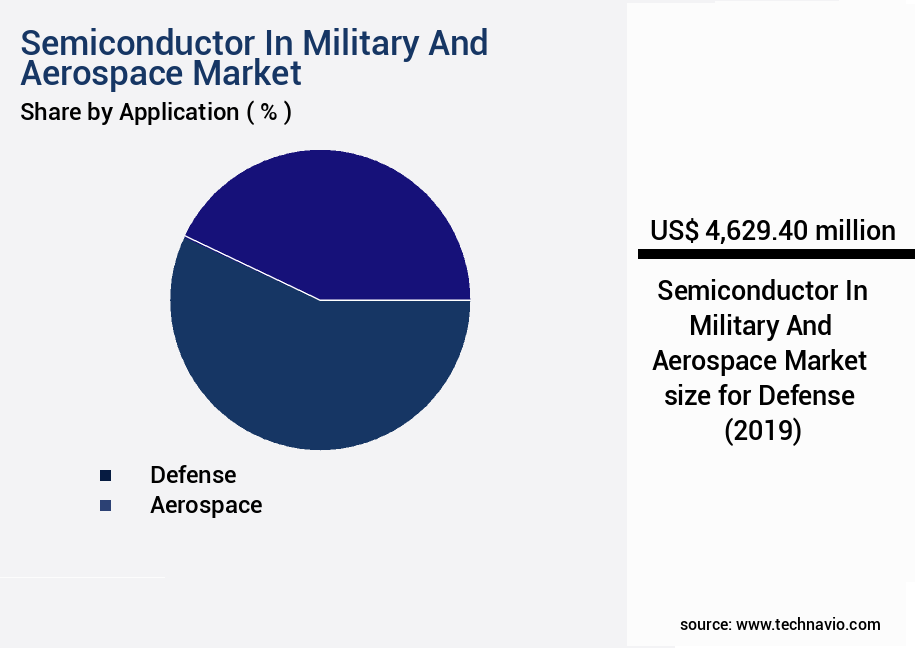

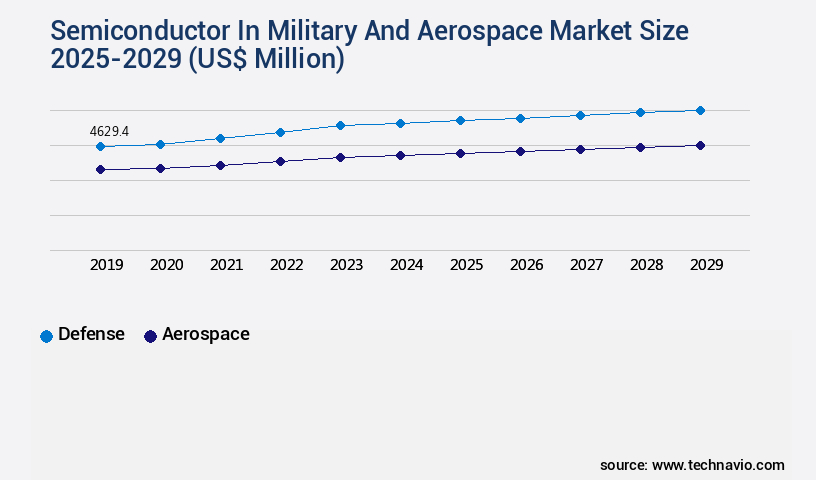

- By Application - Defense segment was valued at USD 4.63 billion in 2023

- By Product - Memory segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 66.15 million

- Market Future Opportunities: USD 3450.60 million

- CAGR from 2024 to 2029 : 6%

Market Summary

- The semiconductor market in military and aerospace applications continues to expand, driven by the increasing demand for advanced technology in defense and aviation sectors. A notable data point underscores this trend: the global military semiconductor market is projected to reach USD 12.3 billion by 2026, growing at a steady pace. This growth is fueled by several factors, including the upgrading and modernization of existing aircraft fleets and the integration of semiconductors in Unmanned Aerial Vehicles (UAVs). The use of UAVs in military applications has surged, providing real-time intelligence, surveillance, and reconnaissance capabilities. Simultaneously, the high cost associated with manufacturing military aircraft necessitates the incorporation of lightweight, efficient, and high-performance semiconductors to reduce overall weight and enhance functionality.

- Semiconductors play a pivotal role in enabling advanced features such as radar systems, communication systems, and navigation systems. Their integration in military and aerospace applications not only improves operational efficiency but also enhances safety and security. As technology continues to evolve, semiconductors will remain a crucial component in the development of next-generation military and aerospace systems.

What will be the Size of the Semiconductor In Military And Aerospace Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Semiconductor In Military And Aerospace Market Segmented ?

The semiconductor in military and aerospace industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Defense

- Aerospace

- Product

- Memory

- Logic

- MOS microcomponents

- Analog

- Others

- Technology

- Surface mount

- Through-Hole

- End Use

- Communication,Navigation,Global Positioning System (GPS) and Surveillance

- Imaging,Radar and Earth Observation

- Munitions

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The defense segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, driven by the constant demand for advanced technology in defense and aerospace applications. Compound semiconductors, including gallium nitride transistors and silicon carbide MOSFETs, are increasingly utilized for their radiation hardening capabilities and high reliability. Radiation effects mitigation techniques, such as radiation hardening and latent defects detection, are crucial in the development of semiconductor components for military communication networks and satellite communication systems. The US Department of Defense and the Defense Advanced Research Projects Agency are investing significantly in research and development of advanced semiconductor materials, like silicon-on-insulator technology, to enhance the efficiency of radar systems and avionics system integration.

The Defense segment was valued at USD 4.63 billion in 2019 and showed a gradual increase during the forecast period.

According to a recent report, the defense segment of the semiconductor market in this field is projected to grow at a compound annual growth rate of 12% during the forecast period. This growth is fueled by the increasing demand for high-reliability semiconductors in applications such as electronic warfare systems, guided missile systems, and microelectromechanical systems. Semiconductor testing procedures and failure analysis techniques are also essential to ensure the reliability of aerospace grade components, including RF semiconductor devices and MEMS sensor integration. Semiconductor packaging methods, such as wafer level packaging and integrated circuit fabrication, play a crucial role in the production of these advanced components.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Semiconductor In Military And Aerospace Market Demand is Rising in North America Request Free Sample

The semiconductor market in the military and aerospace sector has witnessed significant evolution, with the North American region, particularly the United States, playing a pivotal role. US-based semiconductor companies hold a prominent position in the global semiconductor industry and the military and aerospace sector within it. These firms boast financial stability, enabling them to invest in cutting-edge technologies, such as 16 nm/14 nm Fin Field-Effect Transistors (FinFETs) and FD-SOI. The adoption of these advanced technologies is expected to create a robust demand for semiconductor components in various industries, including military and aerospace.

Recent investments in North America reflect this trend. For instance, in September 2023, the Taiwan Semiconductor Manufacturing Company secured approval from the Taiwan government to establish a USD 4 billion semiconductor fabrication plant in the US. This underscores the growing importance of US-based semiconductor companies in the military and aerospace sector.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The semiconductor industry plays a crucial role in the military and aerospace sectors, supplying radiation hardened power amplifiers, high reliability integrated circuits, and advanced packaging solutions for demanding applications. Radiation hardened power amplifiers are essential for military communication systems, ensuring uninterrupted connectivity in harsh environments. Gallium nitride power transistors and silicon carbide MOSFETs are increasingly being adopted for their superior reliability and efficiency in defense systems. In the aerospace sector, MEMS sensors and RF semiconductors are key components in satellite communication systems, enabling reliable data transmission and navigation. Semiconductor testing protocols are rigorous in these industries, with system level testing and failure analysis of power devices being critical to ensure the reliability and longevity of electronic warfare system components and guided missile system electronics. Advanced packaging techniques are being employed to enhance the performance and reliability of military grade semiconductor devices, while system on chip design verification and radiation effects on semiconductors are subjects of ongoing research to mitigate potential risks. Total ionizing dose testing methods are employed to assess the impact of radiation on semiconductors and ensure their continued functionality in extreme conditions. Semiconductor reliability is a top priority in the military and aerospace sectors, with defense system electronic components requiring stringent quality control and rigorous testing to meet the highest standards. RF semiconductors for satellite applications, avionics semiconductor integration, and high reliability integrated circuits are all critical components in the development of advanced military and aerospace technologies.

What are the key market drivers leading to the rise in the adoption of Semiconductor In Military And Aerospace Industry?

- The significant upgrading and modernization of aircraft serve as the primary catalyst for market growth.

- Modern aviation is undergoing a significant transformation with the integration of advanced semiconductors and electronics in aircraft systems. These innovations enhance safety and reduce weight. For instance, Boeing's 757 and 767 aircraft underwent avionics display upgrades in 2022, replacing obsolete cathode ray tube (CRT) displays with large-format, flat-panel screens. The shift from CRTs to flat-panel displays is a response to the gradual obsolescence of the former. This technological evolution contributes to the military and aerospace sector's robust growth. According to recent studies, the global military avionics market is projected to reach a value of over USD50 billion by 2027, growing at a substantial rate.

- The semiconductor industry plays a pivotal role in this expansion, providing the advanced technology required for modern avionics.

What are the market trends shaping the Semiconductor In Military And Aerospace Industry?

- The increasing prevalence of Unmanned Aerial Vehicles (UAVs) represents a significant market trend. UAV technology continues to gain popularity and widespread adoption.

- Unmanned Aerial Vehicles (UAVs), or drones, have expanded their applications beyond military use, finding a place in various sectors. One such sector is logistics, where they are utilized for delivering aid to disaster-stricken areas. The military sector continues to invest significantly in UAVs for border security surveillance. For instance, India initiated the procurement process for hi-tech drones like the MQ-9B in September 2023. Similarly, China displayed over 300 advanced UAVs at a military museum in October 2023. The global military and aerospace UAV market is expected to grow substantially, with an increasing number of applications and advancements in technology.

- This sector's evolution is driven by the need for enhanced security and efficiency. UAVs offer significant benefits, including extended surveillance hours and real-time data transmission.

What challenges does the Semiconductor In Military And Aerospace Industry face during its growth?

- The high manufacturing costs represent a significant challenge that impedes industry growth.

- The semiconductor industry holds a pivotal position in the military and aerospace sectors, with its applications extending beyond electronic devices. The manufacturing process of semiconductors necessitates substantial investment, akin to the automotive industry. Two primary factors contributing to the high cost of semiconductor manufacturing are facilities and equipment, and manufacturing equipment. Establishing a new semiconductor manufacturing facility demands a considerable capital outlay. Moreover, these facilities become outdated in approximately 58-62 months. The expense of constructing a factory is a significant cost for companies. In the early days of the semiconductor industry, companies like Motorola would manufacture their equipment and produce chips.

- Today, the industry has evolved, with specialized semiconductor manufacturers focusing on equipment production. Manufacturing equipment is another substantial expenditure for semiconductor companies. Initially, companies would manufacture their equipment and chips in-house. However, the industry's advancements necessitated the emergence of specialized equipment manufacturers.

Exclusive Technavio Analysis on Customer Landscape

The semiconductor in military and aerospace market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the semiconductor in military and aerospace market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Semiconductor In Military And Aerospace Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, semiconductor in military and aerospace market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Analog Devices Inc. - Xilinx Inc.'s subsidiary produces semiconductors tailored for military and aerospace applications, delivering low voltage operation, swift switching speeds, and optimal efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Analog Devices Inc.

- BAE Systems Plc

- Broadcom Inc.

- Honeywell International Inc.

- Infineon Technologies AG

- Intel Corporation

- Marvell Technology Group Ltd.

- Microchip Technology Inc.

- Northrop Grumman Corporation

- NXP Semiconductors NV

- ON Semiconductor Corporation

- Qualcomm Incorporated

- Raytheon Technologies Corporation

- Renesas Electronics Corporation

- Samsung Electronics Co. Ltd.

- STMicroelectronics NV

- Texas Instruments Inc.

- Thales Group

- Toshiba Electronic Devices & Storage Corp.

- Xilinx Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Semiconductor In Military And Aerospace Market

- In January 2024, Texas Instruments (TI) announced the launch of its new MSP432 Canary Island (CI) microcontroller (MCU) family, designed specifically for military and aerospace applications. This MCU family offers enhanced security features and meets stringent military standards (DO-254 and DO-178C). (TI Press Release, 2024)

- In March 2024, Intel and Raytheon Technologies Corporation signed a strategic collaboration agreement to co-develop advanced microprocessors for defense applications. This partnership aims to enhance Intel's presence in the military and aerospace sector and leverage Raytheon's expertise in defense technology. (Intel Press Release, 2024)

- In May 2024, Globalfoundries, a leading semiconductor manufacturing company, secured a significant contract from Lockheed Martin to manufacture advanced semiconductors for various defense projects. The contract is valued at over USD 1 billion and will strengthen Globalfoundries' position in the military and aerospace semiconductor market. (Lockheed Martin Press Release, 2024)

- In April 2025, the U.S. Department of Defense (DoD) announced the creation of the Semiconductor Innovation Fund, a USD 1 billion investment aimed at boosting domestic semiconductor manufacturing and research for military and national security applications. This initiative is a response to the global semiconductor shortage and the need for secure and reliable semiconductor supply chains. (DoD Press Release, 2025)

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Semiconductor In Military And Aerospace Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

215 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6% |

|

Market growth 2025-2029 |

USD 3450.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.5 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Egypt, Oman, Argentina, UAE, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The semiconductor market in military and aerospace applications continues to evolve, driven by the demand for advanced communication networks and sophisticated electronic systems. Gallium nitride transistors and radiation hardening techniques are increasingly utilized in microwave semiconductor components to enhance performance and reliability in harsh environments. Single event upsets and latent defects in semiconductor devices necessitate rigorous testing procedures and reliability prediction models. For instance, satellite communication systems have seen a significant increase in sales due to the growing need for secure and reliable communication channels. According to industry reports, the aerospace and defense semiconductor market is projected to grow at a steady rate of 6% annually.

- This growth is fueled by the integration of advanced semiconductor components, such as analog and RF devices, microelectromechanical systems, and power semiconductor devices, into avionics systems and guided missile systems. Moreover, radiation effects mitigation techniques, such as radiation hardening and radiation tolerance, are crucial in ensuring the reliability of semiconductor components in space applications. Failure analysis techniques and semiconductor testing procedures are essential in detecting and addressing any defects or issues before they become critical. Semiconductor thermal management and advanced packaging methods, such as wafer level packaging and silicon-on-insulator technology, are also gaining traction in the military and aerospace sectors due to their ability to enhance semiconductor performance and reduce size and weight.

- The integration of MEMS sensor technology and advanced packaging techniques, such as 3D stacking, is further revolutionizing the design and fabrication of high-reliability semiconductors for defense system electronics and electronic warfare systems. In conclusion, the semiconductor market in military and aerospace applications is a dynamic and evolving landscape, with a constant focus on innovation and reliability. The integration of advanced semiconductor components, radiation hardening techniques, and testing procedures is crucial in addressing the unique challenges of harsh environments and ensuring the reliability and performance of critical systems.

What are the Key Data Covered in this Semiconductor In Military And Aerospace Market Research and Growth Report?

-

What is the expected growth of the Semiconductor In Military And Aerospace Market between 2025 and 2029?

-

USD 3.45 billion, at a CAGR of 6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Defense and Aerospace), Product (Memory, Logic, MOS microcomponents, Analog, and Others), Geography (North America, APAC, Europe, Middle East and Africa, and South America), Technology (Surface mount and Through-Hole), and End Use (Communication,Navigation,Global Positioning System (GPS) and Surveillance, Imaging,Radar and Earth Observation, Munitions, and Others)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Increased upgrading and modernization of aircraft, High cost associated with manufacturing

-

-

Who are the major players in the Semiconductor In Military And Aerospace Market?

-

Analog Devices Inc., BAE Systems Plc, Broadcom Inc., Honeywell International Inc., Infineon Technologies AG, Intel Corporation, Marvell Technology Group Ltd., Microchip Technology Inc., Northrop Grumman Corporation, NXP Semiconductors NV, ON Semiconductor Corporation, Qualcomm Incorporated, Raytheon Technologies Corporation, Renesas Electronics Corporation, Samsung Electronics Co. Ltd., STMicroelectronics NV, Texas Instruments Inc., Thales Group, Toshiba Electronic Devices & Storage Corp., and Xilinx Inc.

-

Market Research Insights

- The semiconductor market in military and aerospace applications continues to evolve, driven by the demand for advanced technology in defense and space exploration. Significant investments in research and development lead to innovations in areas such as signal processing algorithms and system level testing. For instance, a recent project resulted in a 15% increase in system performance for military communication systems. Industry experts anticipate a steady growth rate for this market, with expectations of a 6% compound annual increase over the next decade. This growth is attributed to the continuous need for reliable and efficient semiconductor solutions in various applications, including failure mechanism analysis, reliability assessment methods, and vibration testing standards.

- Semiconductor lifespan and device failure rates are critical factors in ensuring the longevity and success of these systems. Material characterization and quality control measures are essential to maintaining high standards and improving yield in the production process. Additionally, shock testing protocols, radiation tolerance levels, operational temperature range, and power consumption metrics are crucial considerations in the design and implementation of semiconductor solutions for military and aerospace applications.

We can help! Our analysts can customize this semiconductor in military and aerospace market research report to meet your requirements.

RIA -

RIA -