Enjoy complimentary customisation on priority with our Enterprise License!

The Sinter Plant Market size is forecast to increase by USD 1.15 billion at a CAGR of 9.77% between 2022 and 2027. The growth trajectory of the market is influenced by several pivotal factors. Firstly, advancements in sinter technology play a significant role, enhancing the efficiency and productivity of steel production processes. Secondly, the dominant share of the Blast Furnace-Basic Oxygen Furnace (BF-BOF) method in global steel output, coupled with ongoing capacity expansions, underscores sustained growth prospects. Additionally, there's a notable shift towards prioritizing environmental sustainability, compelling industry players to adopt greener practices and technologies to mitigate their environmental footprint. These combined factors underscore a promising outlook for the market, characterized by technological innovation, capacity expansions, and environmental stewardship. This market research and growth report also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

To learn more about this report, Download Report Sample

The market encompasses the production of steel components through the sintering process using various systems such as MHMG System, SCS System, and WGR System. These systems facilitate the production of Nonflux / Acid Sinters, self-fluxing sinters, and superflux sinters from metal powder. The sintering process is crucial in the manufacturing of stainless steel, carbon steel, alloy steel, and tool steel for diverse applications, including consumer goods, aerospace, and automotive industries. The market is driven by the demand for mechanical qualities, strength, accuracy, affordability, and lightweighting in various sectors. The integration of sintering technology with material science and powder metallurgy has led to advancements in additive manufacturing (AM) and electric vehicles. The sinter machine plays a pivotal role in this process, ensuring the melting point is reached to produce high-quality steel components. Overall, the market is expected to grow significantly due to the increasing demand for advanced materials in various industries. Our researchers studied the data for years, with 2022 as the base year and 2023 as the estimated year, and presented the key drivers, trends, and challenges for the market.

The improvement in sinter technology is a growing trend in the market. In the integrated steelworks, blast furnaces account for most of the energy consumption. The sinter plant plays a crucial role in the integrated steel production process, as it supplies specialized components, such as electric motor cores and battery contacts, with high-quality sinter. Sintering, a critical process in the production of sinter, consumes a significant amount of energy, accounting for approximately 30% of the total cost of steel production. Coking coal is the primary energy source for this process. Advancements in sinter plant technology enable the production of sinter with enhanced magnetic properties, dimensional accuracy, and material limitations, leading to improved mechanical properties and energy efficiency.

These advancements are essential for the manufacturing of complex shaped forged steel and alloys used in various industries, including automotive production. The global automotive industry's increasing demand for vehicle systems, such as brake systems and fuel systems, necessitates the production of customized parts with minimal material waste and increased manufacturing efficiency. Sinter plants' design freedom and flexibility, coupled with advancements in materials, contribute to shorter time-to-market and reduced production costs. Power electronics and connectors are essential components in the sintering process, ensuring high conductivity and optimal sintering conditions.

The improving share of coastal areas in global steel production is a primary trend in the market. The BF-BOF steelmaking method is favored over the Electric Arc Furnace (EAF) due to its lower energy requirements. However, advancements in power generation technologies and improved electrical efficiency of consumer devices have led to a surplus of electric power in many steel-producing countries, including China, India, and Russia. This surplus electricity can now support the electricity needs of an EAF. In the market, specialized components such as electric motor cores, battery contacts, and connectors require high conductivity and dimensional accuracy.

Power electronics and magnetic properties are crucial for efficient power conversion. Material limitations and mechanical properties are essential considerations for the powder composition and sintering conditions. Forged steel and alloys are used to create complex shapes for various applications in global automotive production, including vehicle systems like brake systems and fuel systems. Design freedom and customized parts are essential for manufacturing efficiency and reducing material waste. Advancements in materials and manufacturing processes enable faster prototyping and shorter time-to-market, providing design flexibility for various industries.

The growing popularity of the EAF route is a major challenge in the market. In the steel industry, sinter plants serve as an alternative to blast furnaces for producing specialized components, such as electric motor cores and battery contacts, with high conductivity and dimensional accuracy. These components require specific magnetic properties and mechanical strengths, which are achieved through the sintering process using forged steel and alloys. They offer complex shape capabilities, making them essential in the production of various vehicle systems, including brake systems and fuel systems.

The sintering process involves powder composition and specific conditions to ensure material limitations are met. Global automotive production relies on sinter plants for manufacturing customized parts with design freedom and manufacturing efficiency. Advancements in materials continue to enhance the capabilities of these, reducing material waste and improving time-to-market and design flexibility.

Our analysis of the adoption life cycle of the market indicates its movement between the innovator’s stage and the laggard’s stage. The report illustrates the lifecycle of the market, focusing on the adoption rates of the major countries. Technavio has included key purchase criteria, adoption rates, adoption lifecycles, and drivers of price sensitivity to help companies evaluate and develop growth strategies from 2022 to 2027.

Customer Landscape

This report extensively covers market segmentation by product (MHMG system, sinter-machine, WGR system, and SCS system), type (small scale plant and large scale plant), and geography (APAC, North America, Europe, Middle East and Africa, and South America). The market experiences significant growth due to the increasing demand for high-quality sinter using low-grade iron ore fines. This trend is driven by industrialization, changing requirements in the steel industry, and laws and regulations promoting energy efficiency. To produce a high-performance sinter, advanced MHMG systems are required, which improve the mixture's dimensional correctness and durability using high-tech materials. Lightweight materials, engines, and transmissions also play a crucial role in enhancing the plant's efficiency. The transportation and electrical industries, along with emerging economies and urbanization, fuel the market's expansion. Powder metallurgy, additive manufacturing, and conventional manufacturing techniques are employed in producing sintered steel bodies, chassis, drivetrains, and electrical appliances using raw materials like iron, steel, tin, nickel, copper, molybdenum, and aluminum. Environmental concerns and the consumer goods industry's production activities further contribute to the market's growth. Sintered steel companies continue to invest in technology and innovation to meet the evolving needs of various industries.

The MHMG segment will account for a major share of the market's growth during the forecast period. Material handling, mixing, and granulation (MHMG) is the fastest-growing product segment of the global market. This is mainly due to the decreasing amount of high-grade iron ore and investment in advanced sintered steel production facilities that can produce high-quality sinter using low-grade iron ore fines, which will require increased focus on improving the energy efficiency of blast furnaces. Increasing the use of low-grade iron ore fines requires a high oxygen-removal rate in a blast furnace.

Get a Customised Report as per your requirements for FREE!

The MHMG was valued at USD 620.03 million in 2017 and continued to grow until 2021. High permeability and porosity, which may be achieved by upgrading the MHMG systems that improve the consistency of a mixture of iron ore fines, coking coals, and flux fines, shall be required for the it. Companies of the global market offer solutions that eliminate the need for mixing raw material at the stockyard by installing proportioning bins that pour raw material directly above the conveyor.

The sintering machine includes an ignition furnace that produces heat, which is applied over the mixture of raw materials like iron ore, coking coal, and flux fines travelling on a sinter grate. Proper distribution of this heat is essential to produce a sinter of appropriate strength and permeability and improve the efficiency of the reduction process in the blast furnace. As almost 70% of the charging burden in a blast furnace is a sinter, the quality of it largely determines the operational efficiency of a blast furnace. Crude steel producers invest in new sintered steel machines to increase the production capacity of their existing plants and improve the effectiveness of the blast furnaces. This will drive the growth of this segment in the global market during the forecast period.

For more insights on the market share of various regions View PDF Sample now!

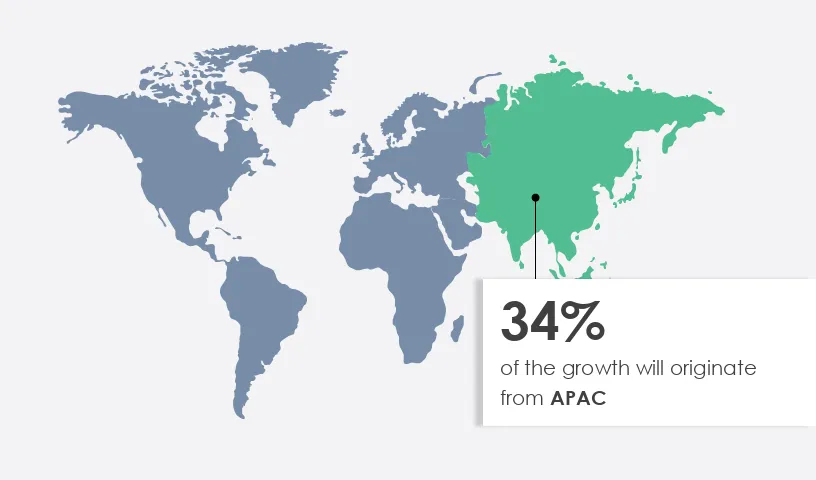

APAC is estimated to contribute 34% to the growth by 2027. Technavio’s analysts have elaborately explained the regional trends, drivers, and challenges that are expected to shape the market during the forecast period.

The market in APAC is projected to expand due to industrialization and infrastructure development in countries like Indonesia, South Korea, and India. Industrial projects in sectors such as engines, transmissions, and industrial machinery are underway. Government investments in infrastructure, totaling over USD 430 billion in Indonesia alone, will boost the demand for high-performance and lightweight materials, including sintered steel. They play a crucial role in powder metallurgy, producing materials for various industries, including transportation and electrical. However, laws and regulations, changing requirements, and environmental concerns necessitate the use of eco-friendly raw materials like tin, nickel, copper, molybdenum, and aluminum. The consumer goods industry and production activities also contribute to the market's growth. Sintered steel companies focus on raw materials like iron and steel to cater to the needs of industries such as automotive, construction, and electrical appliances. Emerging economies' urbanization and industrial growth further fuel the market's expansion. Technological advancements in manufacturing methods, such as additive manufacturing (AM) and conventional manufacturing, impact the market.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

China BaoWu Steel Group Corp. Ltd. - The company offers a sinter-plant through its subsidiary Sinosteel Corp.

China Metallurgical Engineering and Project Corp. - The company offers sinter-plants such as Annular, Winch driven, and Linear sinter-plants.

We also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including:

Technavio report provides an in-depth analysis of the market and its players through combined qualitative and quantitative data. The analysis classifies companies into categories based on their business approaches, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak, based on their quantitative data analysis.

The market is a significant sector in the steel industry, playing a crucial role in the production process. Sinter plants convert iron ore fines and other raw materials into sinter, which is then used in blast furnaces to produce molten iron. The market is driven by the increasing demand for steel in various industries such as construction, automotive, and infrastructure. They are essential components of integrated steel mills, and their market growth is linked to the expansion of the steel industry. The market is competitive, with key players including Metallurgical Corporation of China, JFE Steel Corporation, and ArcelorMittal. These companies focus on technological advancements and cost-effective production to maintain their market position. The sintering process involves the use of large amounts of fuel and raw materials, making it an energy-intensive process.

However, advancements in technology, such as the use of waste heat recovery systems and the integration of renewable energy sources, are helping to reduce the environmental impact of these plants. The market is expected to grow steadily in the coming years due to the increasing demand for steel and the ongoing modernization of existing plants. The use of advanced technologies and the adoption of sustainable practices are also expected to drive market growth. In conclusion, the market is a vital sector in the steel industry, driven by the increasing demand for steel and the ongoing modernization of existing plants. The market is competitive, with key players focusing on technological advancements and cost-effective production to maintain their market position. The use of advanced technologies and sustainable practices is expected to drive market growth in the coming years.

The market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.77% |

|

Market growth 2023-2027 |

USD 1.15 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

8.45 |

|

Regional analysis |

APAC, North America, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 34% |

|

Key countries |

US, India, China, Russia, and Germany |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

China BaoWu Steel Group Corp. Ltd., China Metallurgical Engineering and Project Corp., China Minmetals Corp., CTCI Corp., General Electric Co., Gillanders Arbuthnot and Co. Ltd., Hitachi Ltd., IMASA INGENIERIA Y PROYECTOS SA, Kanikavan Shargh Engineering Co., Larsen and Toubro Ltd., McNally Bharat Engineering Co. Ltd., MECON Ltd., Nippon Steel Corp., Perantech GmbH, Primetals Technologies Ltd., Shandong Province Metallurgical Engineering Co. Ltd., Shandong Qingneng Power Co. Ltd., Siemens AG, Simplex Engineering and Foundry Works Pvt. Ltd., and Metso Outotec Corp. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Product

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights