Blast Furnaces Market Size 2024-2028

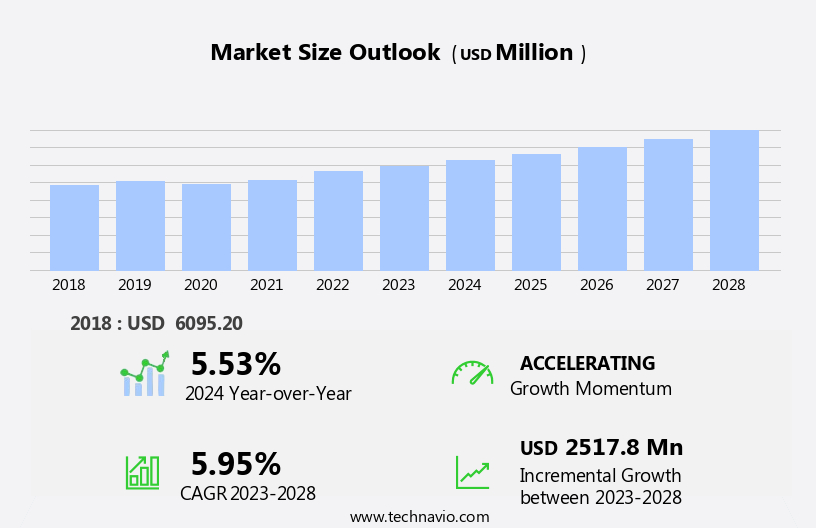

The blast furnaces market size is forecast to increase by USD 2.52 billion, at a CAGR of 5.95% between 2023 and 2028.

- The market is driven by the substantial installed base of blast furnaces, which continues to serve as a significant asset for steel production. This established infrastructure forms the backbone of the iron and steel industry, fueling demand for blast furnaces. Simultaneously, the rising popularity of steel mini mills poses a trend in the market, as these facilities offer cost advantages and increased flexibility compared to traditional integrated steel mills. However, the market faces challenges, including the need for energy efficiency and environmental sustainability. The increasing focus on reducing carbon emissions and minimizing waste is compelling blast furnace manufacturers to innovate and adopt advanced technologies.

- Additionally, the volatile raw material prices and intense competition further complicate the market landscape, necessitating strategic planning and operational agility for market participants. Companies seeking to capitalize on the opportunities in this market must stay abreast of technological advancements, optimize energy usage, and navigate the complex regulatory environment.

What will be the Size of the Blast Furnaces Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The blast furnace market is characterized by its continuous evolution and dynamic nature, with various interconnected elements shaping its landscape. Hot metal production remains a key focus, with blast furnace efficiency a critical factor in optimizing output. The sintering process, which precedes blast furnace operation, plays a pivotal role in ensuring consistent coke quality. Stack gas cleaning, a crucial aspect of blast furnace maintenance, addresses environmental regulations, reducing carbon emissions and improving fuel consumption. Blast furnace reline and automation are ongoing concerns, with advancements in technology driving efficiency and reducing costs. Coke production, a primary fuel source, is influenced by raw material costs and the mining and processing industry.

Blast furnace design and blast furnace lining are essential considerations in maximizing production capacity and minimizing energy consumption. Pig iron production, a key output of the blast furnace, is integral to steel rolling and various casting processes. The metals market, influenced by steel production costs and steel price volatility, impacts the demand for blast furnace operation. The global steel industry is undergoing significant changes, with Electric arc furnaces, direct reduced iron, and tuyere injection gaining popularity. Agglomeration technologies, refractory materials, and ironmaking slag are essential components in maintaining blast furnace operation and safety. Blast furnace optimization, burden management, and iron ore blending are ongoing concerns for industrial equipment manufacturers.

The mining and processing industry, machinery manufacturing, and scrap metal recycling all play crucial roles in the blast furnace market's intricate ecosystem.

How is this Blast Furnaces Industry segmented?

The blast furnaces industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Revamping projects

- Capacity additions

- Type

- Hot blast ovens

- Cold blast blowers

- Geography

- North America

- US

- Europe

- Russia

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

.

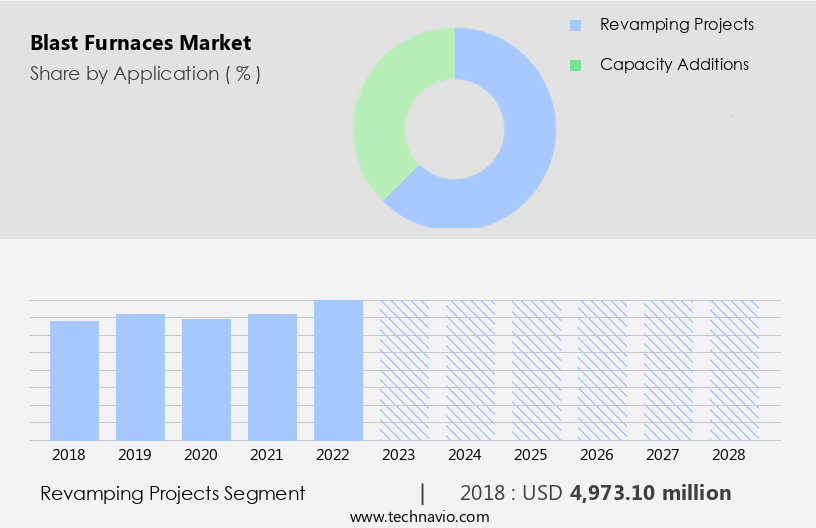

By Application Insights

The revamping projects segment is estimated to witness significant growth during the forecast period.

Amidst the global steel industry's overcapacity, there's a persistent drive for expansion in various regions. This trend is fueled by the employment opportunities the steel sector offers across its value chain. For instance, the US has imposed tariffs on imported steel from Canada, Mexico, China, and the EU to revive its domestic industry and generate employment. Moreover, the surge in steel prices since 2016 and the industry's rising profitability have further enticed producers to invest in new integrated steel plants. The overcapacity issue, which previously obstructed capacity development from 2013-2016, is gradually being addressed. China, for example, plans to reduce its production capacity to 1,000 million tons per annum (mtpa) by 2025-2026, down from 1,200 mtpa in 2015-2016.

Hot metal production remains a critical focus in the steel industry, with blast furnace efficiency, coke quality, and sintering process being essential factors. Blast furnace maintenance, reline, automation, and optimization are ongoing concerns to ensure optimal performance and reduce fuel consumption. Environmental regulations necessitate stack gas cleaning and carbon emissions reduction, while coke production and iron ore mining continue to influence raw material costs. Blast furnace technology, top gas recovery, electric arc furnaces, and direct reduced iron are shaping the industry's evolution. Machinery manufacturing, agglomeration technologies, mining and processing, and industrial equipment are integral to the steel industry's infrastructure.

Refractory materials, ironmaking slag, and casting processes are crucial components in the production of pig iron and steel. Energy consumption, steel rolling, and steel production costs are significant factors in the metals market's dynamics. Steel price volatility and metal fabrication are essential considerations for steel industry players. Safety remains a top priority, with blast furnace gas and safety regulations being key concerns. The steel industry's continued growth is influenced by global steel demand, iron ore blending, and scrap metal recycling.

The Revamping projects segment was valued at USD 4.97 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

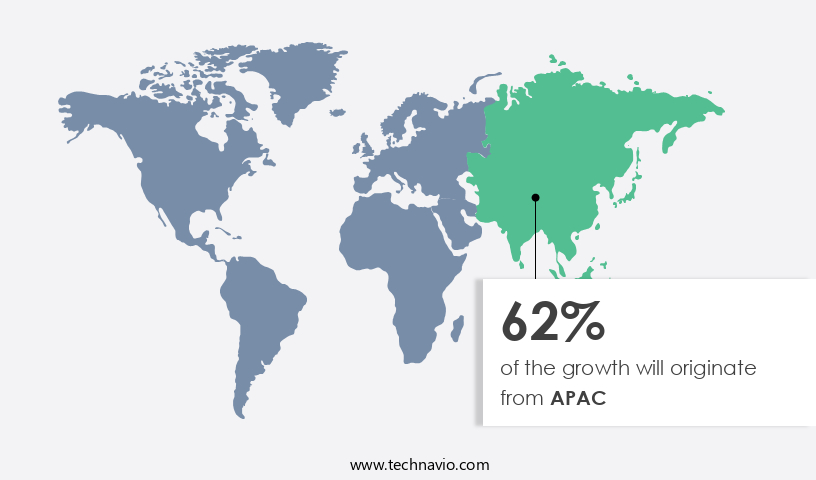

APAC is estimated to contribute 62% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the steel industry, Asia Pacific (APAC) is a significant market for blast furnace-based hot metal production. India and China are key contributors to this region's growth. India's infrastructure development, driven by its expanding urban population and affordable housing sector, will fuel the demand for steel. Additionally, the automobile industry's consistent growth in India will further increase steel consumption. To meet this rising demand, India aims to boost its steelmaking capacity by 175 million tonnes per annum (mtpa) between 2017 and 2030, as outlined in its National Steel Policy. Blast furnace efficiency is crucial for minimizing fuel consumption and reducing carbon emissions.

Sintering processes optimize the use of raw materials, while coke quality plays a vital role in blast furnace operation. Coke production and stack gas cleaning are essential aspects of blast furnace maintenance, which in turn influences blast furnace reline frequency. Blast furnace automation and optimization techniques, such as tuyere injection and blast furnace burden management, contribute to improved efficiency and productivity. Environmental regulations, including those related to carbon emissions, are driving the adoption of technologies like top gas recovery, electric arc furnaces, and direct reduced iron (DRI) production. Raw material costs, particularly for iron ore and coke, significantly impact blast furnace technology and steel production costs.

The steel industry's global demand, driven by various sectors like metal fabrication, construction, and manufacturing, influences the market dynamics. Mining and processing of iron ore, agglomeration technologies like iron ore pelletizing, machinery manufacturing, and refractory materials are essential components of the blast furnace ecosystem. Blast furnace design, lining, and safety are critical factors in ensuring efficient and sustainable iron production. Casting processes, including pig iron production and steel rolling, play a significant role in the overall steel industry value chain. Blast furnace gas, a byproduct of the process, can be utilized for energy generation. Steel price volatility, driven by factors like supply and demand imbalances, raw material costs, and geopolitical factors, impacts the market dynamics.

Scrap metal recycling is an essential aspect of the steel industry, contributing to resource efficiency and sustainability. The steel industry's continuous evolution is shaped by technological advancements, regulatory requirements, and market trends.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Blast Furnaces Industry?

- The substantial presence of blast furnaces in the market is the primary driving factor, given the vast installed base that significantly influences market growth.

- The global steel industry relies on two primary methods for producing crude steel: the Blast Furnace-Basic Oxygen Furnace (BF-BOF) route and the Electric Arc Furnace (EAF) route. Approximately 75% of the world's crude steel is produced via the BF-BOF process, with China, the world's leading producer, accounting for over 90% of its crude steel production through this method. Integrated steel plants employ the BF-BOF process, using iron ore and coking coal to create finished steel. In contrast, steel mini-mills predominantly use the EAF route, which relies on scrap metal and electricity. Despite the availability of scrap steel and affordable electricity in major steel-exporting countries like China, Germany, and Japan, the EAF route has not gained significant traction to meet the escalating steel demand from key industries such as construction, automobile, and equipment manufacturing.

- The BF-BOF process remains the preferred choice due to its ability to produce larger quantities of steel and its integration with the production of refractory materials and ironmaking slag, essential components in metal fabrication and casting processes. Moreover, blast furnace gas, a byproduct of the BF-BOF process, is utilized as a fuel source, contributing to industrial efficiency and sustainability. Blast furnace safety and continuous advancements in industrial equipment are crucial factors ensuring the longevity and competitiveness of this process in the steel industry.

What are the market trends shaping the Blast Furnaces Industry?

- Equipment-as-a-Service (EaaS) is gaining significant traction in the business world as the preferred model for acquiring and managing hardware and software solutions. This trend signifies a shift towards more flexible and cost-effective IT infrastructure solutions.

- Blast furnaces play a pivotal role in hot metal production within the integrated steel industry. Their efficiency significantly impacts the overall performance of a steel plant. To enhance operational efficiency and profitability, steel producers are increasingly entering into performance-based contracts with equipment companies. These contracts include the provision of hardware and services, with the companies bearing a significant portion of the equipment costs. The financial performance of the integrated steel plant determines the payments to the companies. Consequently, there is a growing emphasis on value-added services that optimize blast furnace efficiency. This includes the sintering process, coke quality management, stack gas cleaning, and blast furnace maintenance, such as relining and automation.

- Environmental regulations mandate reduced carbon emissions and fuel consumption, necessitating advancements in these areas. Effective implementation of these services can lead to improved coke production, reduced fuel consumption, and lower carbon emissions, making these investments worthwhile for steel producers.

What challenges does the Blast Furnaces Industry face during its growth?

- The rising prevalence of steel mini mills poses a significant challenge to the expansion of the industry, as these facilities increasingly disrupt traditional production methods and market dynamics.

- Blast furnaces are essential in the production of pig iron, a primary raw material for the global steel industry. This process, which involves the reduction of iron ore in a blast furnace, requires substantial capital investment due to the need for large-scale production to maintain competitive costs. However, blast furnace operations come with challenges, including frequent shutdowns for expensive relining processes and the costly and time-consuming start-up process. These factors necessitate high capacity utilization in integrated steel plants to achieve economies of scale. The global steel demand has historically experienced fluctuations, exposing integrated steel plant operators to potential profitability losses or even deficits when steel prices decline or demand for their output wanes.

- Blast furnace technology continues to evolve, with advancements such as tuyere injection, iron ore pelletizing, and agglomeration technologies aimed at improving efficiency and reducing costs. Top gas recovery and the use of direct reduced iron (DRI) are also gaining popularity in the industry. Machinery manufacturing companies continue to innovate, offering advanced solutions to enhance blast furnace performance and productivity. Despite these advancements, the industry faces challenges, including increasing raw material costs and the need to balance production with market demand.

Exclusive Customer Landscape

The blast furnaces market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the blast furnaces market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, blast furnaces market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ansteel Group Corp. Ltd. - This company specializes in the development and distribution of innovative sports products, catering to a global market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ansteel Group Corp. Ltd.

- China Metallurgical Engineering and Project Corp.

- Compagnie de Saint Gobain

- Danieli and C. Officine Meccaniche Spa

- Gillanders Arbuthnot and Co. Ltd.

- Heavy Engineering Corp. Ltd.

- IHI Corp.

- JP Steel Plantech Co.

- Krosaki Harima Corp.

- Larsen and Toubro Ltd.

- McNally Bharat Engineering Co. Ltd.

- MECON Ltd.

- Nippon Steel Corp.

- Noble Industrial Furnace Co. Inc.

- POSCO holdings Inc.

- Primetals Technologies Ltd.

- Qinhuangdao Qinye Heavy Industry Co. Ltd.

- Shandong Province Metallurgical Engineering Co. Ltd.

- Sinosteel Corp.

- SMS group GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Blast Furnaces Market

- In January 2024, ArcelorMittal, the world's leading steel and mining company, announced the successful start-up of a new blast furnace at its integrated steel mill in Ghent, Belgium. This modern furnace, with a capacity of 3.6 million tonnes per year, is expected to significantly enhance the company's European production capabilities and improve its competitiveness in the global steel market (ArcelorMittal Press Release, 2024).

- In March 2025, ThyssenKrupp AG and Tata Steel formed a strategic partnership to construct a greenfield blast furnace in Europe. The new facility, which will utilize the latest technologies to reduce carbon emissions, is expected to have an annual capacity of 6 million tonnes. This collaboration aims to strengthen the competitive position of both companies in the European steel market and contribute to the decarbonization of the industry (ThyssenKrupp AG Press Release, 2025).

- In May 2024, China Baowu Steel Group, the largest steel producer in China, completed the acquisition of a 51% stake in Shougang Conch Cement for approximately USD 3.4 billion. This strategic move allows Baowu to integrate the blast furnace operations of Shougang Conch Cement into its steel business, expanding its production capacity and enhancing its presence in the Chinese market (Reuters, 2024).

Research Analyst Overview

- The blast furnace market is experiencing significant advancements, driven by the integration of innovative technologies and processes. Automation in blast furnaces is a key trend, enhancing ironmaking process control and improving energy efficiency measures. Carbon capture technology and nanomaterials in steel are revolutionizing sustainable steel production, reducing emissions and enhancing steel quality. Blast furnace modeling and optimization are essential tools for steel industry innovation, enabling the development of new steel alloys and metal substitution. Smart steel, a new generation of advanced steelmaking technologies, is gaining traction, offering improved performance and cost savings. The circular economy is also influencing the market, with iron ore sintering and the use of additive manufacturing in steel production.

- Emerging steel applications, such as in the aerospace and automotive industries, are driving innovation and increasing demand. Despite these advancements, iron production costs remain a challenge, necessitating ongoing research and development in blast furnace lining life and process simulation. Overall, the future of ironmaking lies in the integration of these technologies and a continued focus on sustainability and efficiency.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Blast Furnaces Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.95% |

|

Market growth 2024-2028 |

USD 2517.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.53 |

|

Key countries |

China, India, US, Russia, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Blast Furnaces Market Research and Growth Report?

- CAGR of the Blast Furnaces industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the blast furnaces market growth of industry companies

We can help! Our analysts can customize this blast furnaces market research report to meet your requirements.

RIA -

RIA -