Small Molecule API Market Size 2024-2028

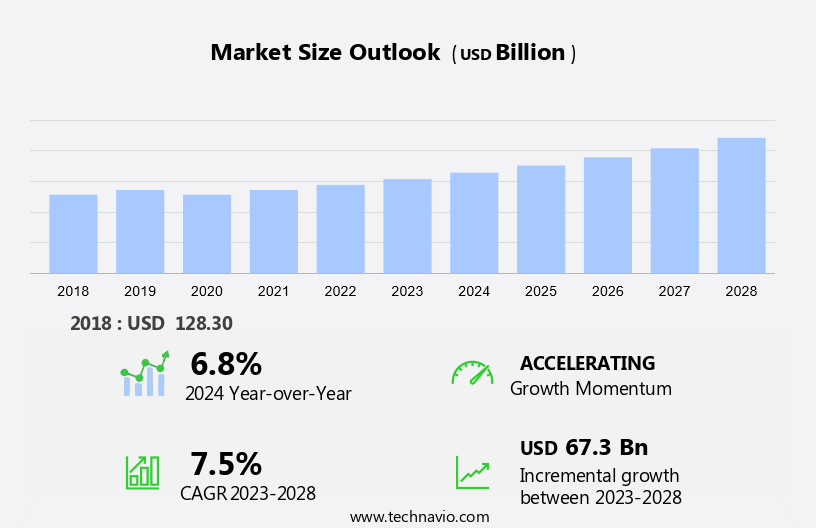

The small molecule API market size is forecast to increase by USD 67.3 billion at a CAGR of 7.5% between 2023 and 2028.

- The market is experiencing significant changes, driven by the shifting landscape of drug development and manufacturing. In developing countries, the small-molecule API manufacturing scenario is evolving, offering cost advantages to contract manufacturers. The increasing geriatric population is fueling demand for small molecule APIs in various therapeutic areas, including diabetes and cancer treatments.

- However, high investment costs and the risk of substantial financial losses are major challenges. Pharmaceutical companies are responding by adopting different manufacturing strategies, such as captive manufacturing and merchant manufacturing, to mitigate risks and optimize costs. Biologics and branded drugs continue to dominate the market, but the trend towards generic drugs is gaining momentum. This dynamic market requires continuous monitoring and strategic planning from industry players to stay competitive.

What will be the Size of the Market During the Forecast Period?

- The small molecule Active Pharmaceutical Ingredients (API) market is a significant segment within the pharmaceutical industry, supplying essential components for drug formulation in various therapeutic areas. This market is driven by several factors, including patent expiry of branded drugs, advancements in the drug development process, and the increasing demand for specialty medicines. Raw materials play a crucial role in the synthesis of APIs. Novel technologies, such as computational modeling and natural extraction, are being employed to improve the efficiency and sustainability of chemical synthesis. Contract manufacturers have been increasingly adopting these technologies to cater to the growing demand for APIs in the pharmaceutical sector.

- Additionally, the drug development process involves several stages, including discovery, development, and commercialization. The API stage is a critical component of this process, as it directly impacts the efficacy and safety of the final drug product. In the context of small molecule APIs, synthetic methods are widely used to produce these ingredients. The therapeutic areas that witness high demand for small molecule APIs include oncology, cardiovascular diseases, diabetes, and chronic diseases. The increasing prevalence of these diseases and the need for effective treatments have fueled the growth of the market. Biotechnology and natural extraction are alternative methods for producing APIs.

- Also, biotechnology involves the use of living organisms to produce therapeutic proteins and other complex molecules, while natural extraction is the process of extracting active compounds from natural sources. Both methods have their advantages and limitations and are used depending on the specific therapeutic area and the nature of the API. Branded drugs and generic drugs differ in their regulatory requirements and market positioning. Branded drugs are innovative treatments with patent protection, while generic drugs are copies of existing drugs with the same active ingredient but different branding and pricing. Captive manufacturing is a strategy employed by some pharmaceutical companies to ensure a consistent supply of APIs for their branded drugs. In conclusion, the market is a dynamic and evolving sector within the pharmaceutical industry. Patent expiry, advancements in the drug development process, and the increasing demand for specialty medicines are some of the key drivers of this market. The use of novel technologies, such as computational modeling and natural extraction, and the adoption of synthetic methods are essential to meet the growing demand for APIs in various therapeutic areas.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Deployment

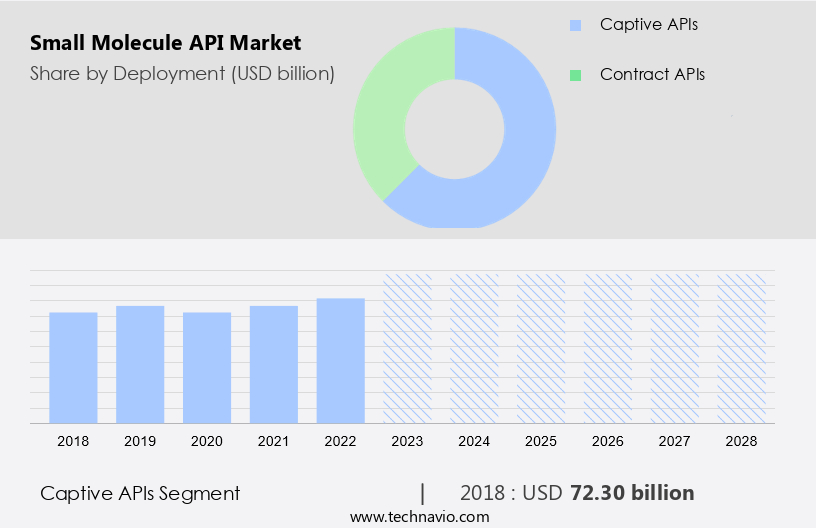

- Captive APIs

- Contract APIs

- Geography

- North America

- Canada

- US

- Asia

- China

- India

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- Italy

- Rest of World (ROW)

- North America

By Deployment Insights

- The captive APIs segment is estimated to witness significant growth during the forecast period.

The market experienced significant growth in 2023, with the captive API manufacturing segment holding the largest share. The expanding healthcare sector in the United States has fueled this growth, as there is a heightened emphasis on making healthcare services more accessible and affordable. This demand for affordable medicines has resulted in an increased need for low-cost small molecule APIs, which are essential for the production of finished drugs. In response, pharmaceutical companies are increasingly turning to Contract Manufacturing Organizations (CMOs) to outsource the manufacturing of either bulk actives or late-stage intermediates. This trend is particularly prominent in the therapeutic areas of chronic diseases, such as cancer and cardiovascular diseases, where the need for affordable treatments is particularly high.

To meet this demand, companies are utilizing various techniques, including chemical synthesis and natural extraction, as well as advanced tools like computational modeling and biotechnology. The market is expected to continue its growth trajectory in the coming years, driven by the increasing focus on developing new therapeutics and improving existing ones.

Get a glance at the market report of share of various segments Request Free Sample

The captive APIs segment was valued at USD 72.30 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

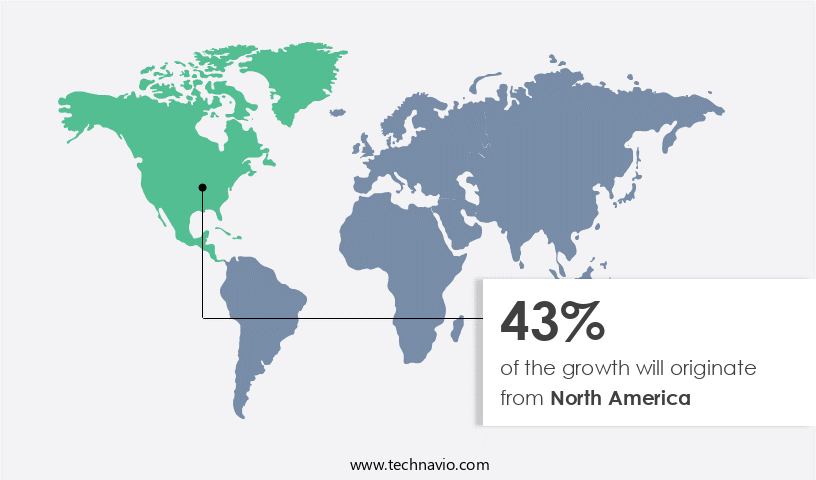

- North America is estimated to contribute 43% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The North American small molecule APIs market is projected to expand during the forecast period, driven by the region's significant player base involved in bulk manufacturing activities. However, the strict regulatory environment in the US and Canada has limited the market share of emerging companies in the global small molecule APIs market. Factors such as the increasing geriatric population in the US and the growing prevalence of chronic diseases are fueling the demand for small-molecule APIs in the region. Additionally, the US government's increased healthcare expenditure is driving the development and production of innovative small-molecule APIs, contributing to market growth.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Small Molecule API Market?

The evolving small-molecule API manufacturing scenario in developing countries is the key driver of the market.

- Small Molecule APIs, or active pharmaceutical ingredients, have become increasingly important in the drug development process as patent expiries on branded drugs create opportunities for contract manufacturers to produce these essential components. China and other emerging economies, such as India, have emerged as significant suppliers of raw materials for Small Molecule APIs due to their cost-effective manufacturing capabilities. In the late 1980s and early 1990s, Chinese manufacturers primarily focused on producing large volumes of low-cost drugs, mainly through fermentation and simple synthetic compounds.

- However, China's economic evolution and entry into the World Trade Organization have led to a more competitive environment for local drug manufacturers. As a result, there has been a shift towards custom manufacturing, which was once prohibited but is now seen as an efficient way to accelerate the learning curve for producing high-quality Small Molecule APIs for regulated markets. Novel technologies, such as Molnupiravir, are also driving demand for Small Molecule APIs in the development of specialty medicines.

What are the market trends shaping the Small Molecule API Market?

The increasing geriatric population is the upcoming trend in the market.

- The market in the United States is poised for growth due to the rising prevalence of chronic diseases among the aging population. As individuals age, they become more susceptible to conditions such as diabetes, cancer, and cardiovascular diseases. These health issues necessitate the development and production of small molecule APIs for the manufacturing of branded and generic drugs. Contract manufacturers play a crucial role in meeting the demand for these APIs.

- Additionally, they offer services ranging from captive manufacturing to merchant manufacturing, ensuring a steady supply of high-quality APIs for drug development. The focus on medication management for the elderly population, particularly those with comorbidities, is driving the need for effective and efficient production processes. In the US healthcare landscape, both branded and generic drugs are essential for managing chronic conditions. Small molecule APIs are the building blocks for these medications, making them a vital component of the pharmaceutical industry. With the increasing burden of chronic diseases, the demand for these APIs is expected to continue growing, offering significant opportunities for market participants.

What challenges does Small Molecule API Market face during the growth?

High investment costs and concerns of huge financial loss are key challenges affecting the market growth.

- Small-molecule Active Pharmaceutical Ingredients (APIs) are a crucial component of various therapeutics, including those used in biotech for targeted therapies in cardiology for cardiovascular conditions and oncology for cancer drugs. CDMOs (Contract Development and Manufacturing Organizations) play a significant role in the production of these APIs. India and China, with their low production costs, have experienced rapid growth in small-molecule API manufacturing. However, the high regulatory scrutiny in these countries, particularly in Asia, can result in quality issues due to the intense manufacturing pressure.

- Also, the US market for pharmaceuticals is highly regulated, ensuring proper development, approval, manufacturing, and commercialization of pharmaceutical products. The expansion of the generic industry and the global chemical and pharmaceutical industries have led to a substantial increase in the production of bulk actives outside the US. Despite the regulatory framework, the demand for small-molecule APIs continues to grow due to the increasing prevalence of chronic diseases. The biotech industry's focus on targeted therapies and the development of new cancer drugs further boosts the market's growth. CDMOs play a vital role in meeting this demand while maintaining the highest quality standards.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amneal Pharmaceuticals Inc.

- Aurobindo Pharma Ltd.

- Cambrex Corp.

- Cipla Inc.

- Corden Pharma International GmbH

- Dishman Carbogen Amcis Ltd.

- Dr Reddys Laboratories Ltd.

- Gilead Sciences Inc.

- GlaxoSmithKline Plc

- Johnson Matthey Plc

- Lonza Group Ltd.

- Merck KGaA

- Novartis AG

- Novasep Holding SAS

- Pfizer Inc.

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

- Thermo Fisher Scientific Inc.

- Viatris Inc.

- WuXi AppTec Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Small molecule APIs, or active pharmaceutical ingredients, play a crucial role in the pharmaceutical industry by serving as the essential components of various therapeutic medicines. The market is witnessing significant growth due to the patent expiry of several blockbuster drugs, leading to an increase in demand for alternative sources of these essential ingredients. The drug development process involves the synthesis of small molecule APIs through various methods such as chemical synthesis and natural extraction. Contract manufacturers specializing in CDMOs (Contract Development and Manufacturing Organizations) and CMOs (Contract Manufacturing Organizations) are key players in the production of small molecule APIs for pharmaceutical and biotech companies.

Moreover, novel technologies, such as computational modeling and targeted therapies, are being employed to discover new molecular entities (NMEs) and develop cost-effective drugs for chronic diseases, including cardiovascular conditions, cancer, and diabetes. These therapeutic areas continue to attract significant investment due to their high unmet medical needs. The production of small molecule APIs for specialty medicines, such as oncology drugs and cardiology treatments, requires specialized expertise and advanced technologies. Biotech companies are increasingly partnering with CDMOs to leverage their capabilities in synthetic and captive manufacturing for the production of these complex APIs. The healthcare system's focus on patient-centric care and personalized treatments is driving the demand for precision medicine and biosimilars. These trends are expected to shape the future of the market, as the industry continues to innovate and meet the evolving health needs of patients.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

159 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.5% |

|

Market growth 2024-2028 |

USD 67.3 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.8 |

|

Key countries |

US, Canada, China, Japan, India, UK, South Korea, Germany, Italy, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Asia, Europe, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -