Smart Railway Systems Market Size 2026-2030

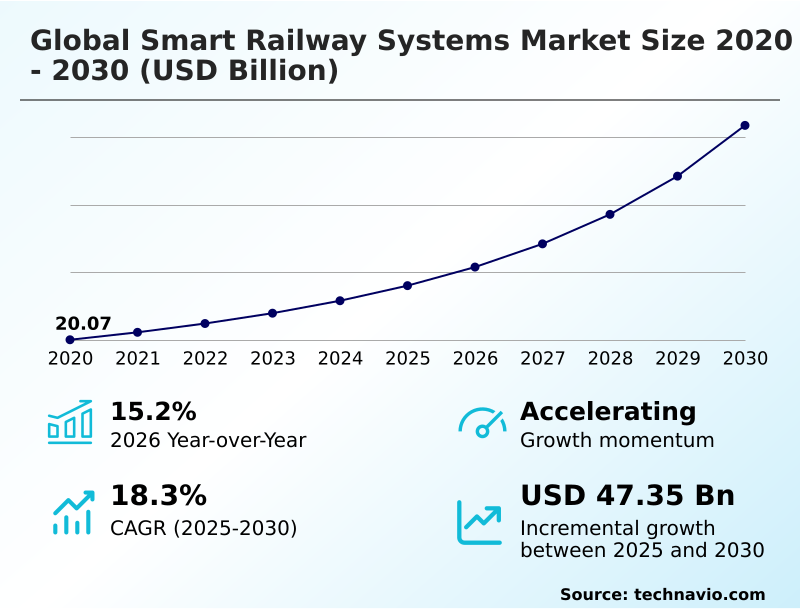

The smart railway systems market size is valued to increase by USD 47.35 billion, at a CAGR of 18.3% from 2025 to 2030. Unyielding imperative for enhanced safety and security protocols will drive the smart railway systems market.

Major Market Trends & Insights

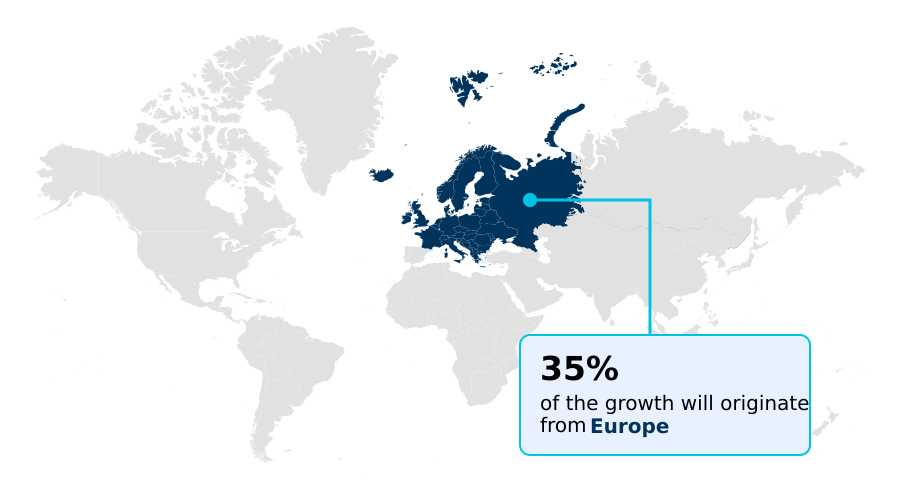

- Europe dominated the market and accounted for a 34.6% growth during the forecast period.

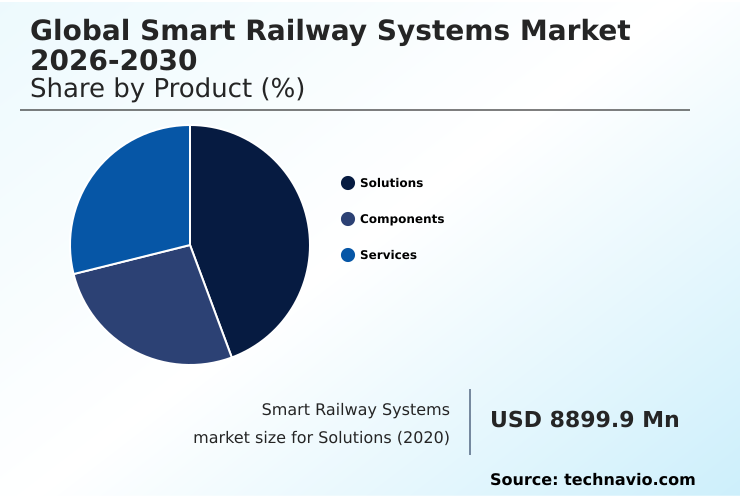

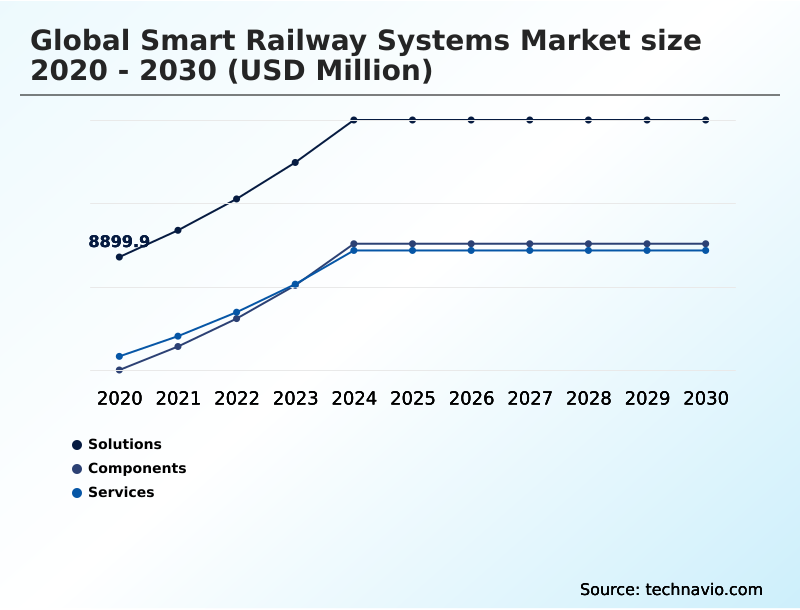

- By Product - Solutions segment was valued at USD 13.18 billion in 2024

- By Type - Passenger information system segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 63.34 billion

- Market Future Opportunities: USD 47.35 billion

- CAGR from 2025 to 2030 : 18.3%

Market Summary

- The smart railway systems market is undergoing a significant transformation, driven by the need to modernize rail infrastructure for greater efficiency, safety, and sustainability. This evolution is defined by the integration of advanced digital capabilities, including predictive maintenance platforms that utilize real-time data from extensive IoT sensor networks.

- A key focus is the shift to condition-based maintenance, which helps optimize asset performance and reduce lifecycle costs. For example, a freight operator can leverage onboard computing and trackside analytics to predict component failures in its rolling stock, scheduling repairs proactively to prevent service disruptions and enhance network reliability.

- While the adoption of technologies like digital twin and automated train control promises substantial benefits, the market must navigate challenges such as high initial investment costs and the need for robust interoperability standards to ensure seamless communication between legacy and modern systems.

- The progression is toward creating a fully interconnected, data-driven ecosystem that supports both operational excellence and a superior passenger journey.

What will be the Size of the Smart Railway Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Smart Railway Systems Market Segmented?

The smart railway systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Solutions

- Components

- Services

- Type

- Passenger information system

- Rail and freight OMS

- Smart ticketing system

- Rail analytics system

- Others

- Deployment

- On-premises

- Cloud

- Hybrid

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- Europe

By Product Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The solutions segment is central to the evolution of modern railways, providing the digital intelligence for a more connected and efficient network.

These integrated platforms enable advanced functionalities like condition-based maintenance and remote condition monitoring, shifting asset management from a reactive to a proactive model. Core offerings focus on enhancing operational control through real-time train tracking and sophisticated onboard computing.

By leveraging data for automated decision-making and intelligent traffic management, these systems are critical for network capacity enhancement.

For instance, the implementation of Mobility as a Service (MaaS) platforms has shown the potential to increase public transit integration by over 20%.

This supports the creation of a resilient transport infrastructure through proactive maintenance scheduling and seamless multimodal transport integration.

The Solutions segment was valued at USD 13.18 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 34.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Smart Railway Systems Market Demand is Rising in Europe Get Free Sample

The geographic landscape of the smart railway systems market is diverse, with regional priorities shaping technology adoption. In Europe, the focus remains on enhancing cross-border connectivity, with initiatives driving demand for standardized solutions.

North America prioritizes freight efficiency, with significant investment in Positive Train Control (PTC) and automated track inspection to optimize its vast supply chain logistics.

Meanwhile, APAC is the fastest-growing region, with an 19.2% growth rate fueled by new urban mobility ecosystem projects in megacities, where Communications-Based Train Control (CBTC) and advanced passenger information systems are standard.

These projects often include high-definition surveillance and video analytics software to manage passenger flow optimization.

For instance, the deployment of smart ticketing systems in major Asian metropolitan areas has simplified multimodal journeys for millions of commuters, supporting efforts to create a seamless passenger journey and a more integrated real-time operational view for transport authorities.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global push for modernizing rail transport is creating distinct opportunities across various applications, from urban transit to heavy-haul freight. Examining the benefits of CBTC in urban rail reveals how moving block signaling significantly enhances network capacity and service frequency, a critical factor for congested cities.

- Concurrently, the challenges of integrating legacy and new signaling systems remain a significant hurdle for brownfield projects. On high-speed lines, ETCS Level 3 implementation challenges revolve around ensuring flawless communication and data integrity for safe, high-speed operations.

- In the freight sector, the pursuit of efficiency is leading to explorations of autonomous heavy-haul freight benefits, where automation promises substantial cost savings and safety improvements. Central to all segments is the need for effective asset management, where IoT sensor applications for track maintenance and remote diagnostics for locomotive health are becoming standard.

- This data-driven approach, seen in the high predictive maintenance ROI for rolling stock, relies on rail analytics for service delay reduction and AI applications in railway network scheduling. As networks become more connected, addressing cybersecurity risks in automated train control and ensuring robust security solutions for rail operational technology are paramount.

- Operators adopting these advanced data-driven asset management strategies in railways have reported a reduction in critical failures that is over 50% greater than those relying on traditional scheduled inspections, showcasing the clear advantages of this technological shift.

What are the key market drivers leading to the rise in the adoption of Smart Railway Systems Industry?

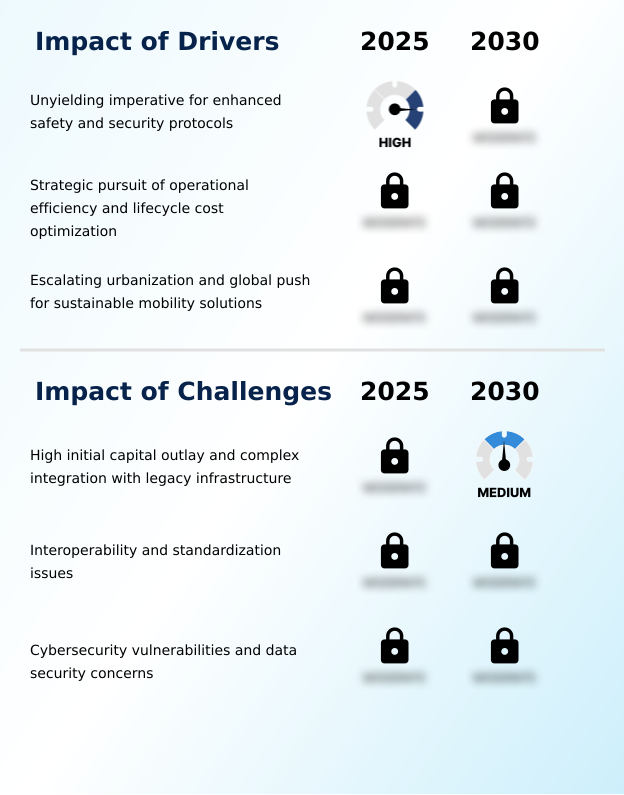

- The unyielding imperative for enhanced safety and security protocols across all facets of rail operations serves as a key driver propelling investment in smart railway systems.

- Market growth is fundamentally driven by the non-negotiable demands for enhanced safety and security, alongside the intense pressure for greater operational efficiency.

- Regulatory mandates compelling the adoption of systems like Positive Train Control (PTC) and the European Train Control System (ETCS) create a baseline for investment, with PTC adoption being credited with reducing certain accident types by over 40%.

- Concurrently, the pursuit of lifecycle cost optimization is fueling the deployment of smart asset management systems and digital signaling.

- These technologies provide a clear return on investment; for example, advanced traffic management systems (TMS) can increase network capacity by up to 20% without requiring new physical track.

- Furthermore, the global push for sustainable mobility solutions positions smart rail as a key enabler, with technologies like driver advisory systems (C-DAS) and regenerative braking optimization reducing energy consumption and supporting environmental goals.

What are the market trends shaping the Smart Railway Systems Industry?

- The convergence of the Internet of Things (IoT) and big data analytics represents a foundational trend, establishing a new operational standard for the industry. This integration enables a fundamental shift toward intelligent, data-driven management of railway assets and infrastructure.

- Key trends in the market are centered on creating intelligent, self-optimizing networks through the integration of digital technologies. The convergence of the Internet of Things (IoT), big data analytics, and artificial intelligence (AI) is enabling a shift toward predictive maintenance, where algorithms can forecast equipment failures with over 90% accuracy.

- This data-driven approach is further enhanced by digital twin technology, creating virtual replicas of physical assets for simulation and analysis. The advancement toward higher grades of automation, particularly Automatic Train Operation (ATO) and the use of the moving block principle in modern signaling, is also critical.

- These systems not only improve service reliability but have demonstrated energy savings of up to 15% on certain routes. The rollout of 5G for rail is set to accelerate these trends, providing the high-bandwidth connectivity needed for real-time data processing and advanced diagnostics.

What challenges does the Smart Railway Systems Industry face during its growth?

- The high initial capital outlay required for deployment, combined with the complexity of integrating new digital technologies with legacy infrastructure, presents a key challenge to market growth.

- The market faces significant challenges, primarily the high initial capital required for digital transformation in rail and the complexity of ensuring interoperability standards between new and legacy systems. Integrating next-generation signaling with older operational technology (OT) often requires bespoke solutions, elevating project costs and timelines.

- The cost to retrofit a single line with modern automated fare collection and centralized traffic control can consume over 50% of an upgrade budget. Furthermore, the increasing connectivity of rail systems creates a larger attack surface, making cybersecurity for rail a paramount concern.

- Recent data shows that cyber threats against critical infrastructure have risen by more than 75%, demanding substantial investment in secure communication links and high-availability systems to protect against potential disruptions and ensure the integrity of vital train control and management systems (TCMS) and wayside inspection systems.

Exclusive Technavio Analysis on Customer Landscape

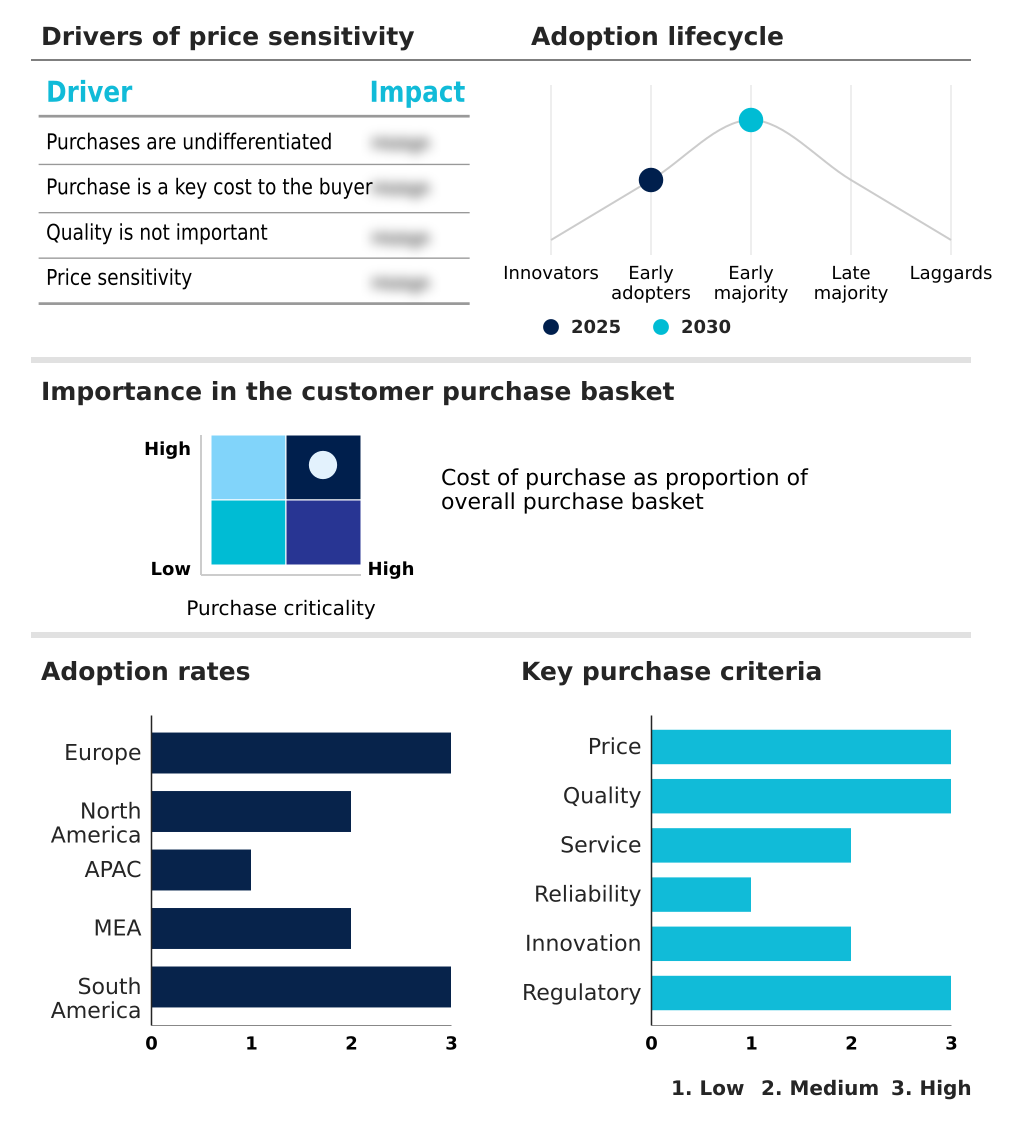

The smart railway systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smart railway systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Smart Railway Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, smart railway systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advantech Co. Ltd. - Specializes in comprehensive smart railway systems, offering digital depot management, advanced CBTC signaling, and train-to-train communication to facilitate automated operations and high-frequency metro services.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advantech Co. Ltd.

- ALSTOM SA

- CAF Group

- Cisco Systems Inc.

- CRRC Corp. Ltd.

- EKE Electronics Ltd.

- Hitachi Rail

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Indra Sistemas SA

- Kapsch TrafficCom AG

- Kyosan Electric Mfg. Co

- ORBCOMM Inc.

- Siemens AG

- Stadler Rail Ag

- Thales Group

- Toshiba Corp.

- Trimble Inc.

- Wabtec Corp.

- ZTE Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Smart railway systems market

- In November, 2024, Alstom secured a five-year Technical Support and Spare Part Supply Agreement with the Saudi Railway Company (SAR) to enhance the operational efficiency of the diesel locomotive fleet on a vital east-west freight corridor using its HealthHub predictive maintenance platform.

- In October, 2024, Televic GSP was chosen by Alstom to supply a complete, state-of-the-art Passenger Information System for 46 new trains for the Massachusetts Bay Transportation Authority (MBTA), featuring high-resolution displays and advanced audio announcement technology.

- In February, 2025, Deutsche Bahn awarded a major long-term contract to a consortium led by Siemens Mobility for the nationwide rollout of digital signaling technology (DSTW) and the European Train Control System (ETCS), a cornerstone project for digitalizing Germany's rail network to boost capacity and punctuality.

- In March, 2025, CG Power and Industrial Solutions Ltd. received a significant purchase order from Kinet Railway Solutions for a long-term supply agreement to provide critical railway components, including advanced propulsion kits and motors, for India's modern Vande Bharat trainsets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Smart Railway Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 318 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.3% |

| Market growth 2026-2030 | USD 47348.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.2% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The smart railway systems market is defined by a strategic transition from traditional mechanical operations to an intelligent, data-driven ecosystem. This shift is centered on the deployment of core technologies like Communications-Based Train Control (CBTC), European Train Control System (ETCS), and Positive Train Control (PTC) to create safer and more efficient networks.

- A pivotal trend is the adoption of digital twin technology, which allows operators to simulate, monitor, and manage physical assets in a virtual environment. For boardroom consideration, the decision to invest in a comprehensive predictive maintenance platform, powered by big data analytics and AI, fundamentally alters financial planning.

- It moves expenditures from unpredictable, costly emergency repairs to manageable, data-informed operational budgets, directly impacting long-term asset value. For instance, the implementation of advanced Automatic Train Operation (ATO) systems has demonstrated the capability to improve on-time performance by over 15%, a critical metric for both passenger satisfaction and operational viability.

- This evolution toward next-generation signaling and condition-based maintenance is reshaping the industry's approach to infrastructure management and service delivery.

What are the Key Data Covered in this Smart Railway Systems Market Research and Growth Report?

-

What is the expected growth of the Smart Railway Systems Market between 2026 and 2030?

-

USD 47.35 billion, at a CAGR of 18.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Solutions, Components, and Services), Type (Passenger information system, Rail and freight OMS, Smart ticketing system, Rail analytics system, and Others), Deployment (On-premises, Cloud, and Hybrid) and Geography (Europe, North America, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Unyielding imperative for enhanced safety and security protocols, High initial capital outlay and complex integration with legacy infrastructure

-

-

Who are the major players in the Smart Railway Systems Market?

-

Advantech Co. Ltd., ALSTOM SA, CAF Group, Cisco Systems Inc., CRRC Corp. Ltd., EKE Electronics Ltd., Hitachi Rail, Huawei Technologies Co. Ltd., IBM Corp., Indra Sistemas SA, Kapsch TrafficCom AG, Kyosan Electric Mfg. Co, ORBCOMM Inc., Siemens AG, Stadler Rail Ag, Thales Group, Toshiba Corp., Trimble Inc., Wabtec Corp. and ZTE Corp.

-

Market Research Insights

- The smart railway systems market is characterized by dynamic shifts toward data-driven decision-making and lifecycle cost optimization. The emphasis on operational efficiency is paramount, with operators achieving over a 20% reduction in unplanned downtime by adopting predictive asset management strategies.

- This move toward high-availability systems is complemented by a focus on the seamless passenger journey, where integrated ticketing and real-time information systems have contributed to a 10% increase in ridership in certain urban mobility ecosystems. Furthermore, enhanced safety and security measures, driven by strict regulatory compliance, remain a core pillar of investment.

- These advancements underscore a strategic pivot to resilient transport infrastructure, where intelligent traffic management and proactive maintenance scheduling are not just enhancements but essential components of modern railway operations, delivering measurable improvements in both performance and financial sustainability.

We can help! Our analysts can customize this smart railway systems market research report to meet your requirements.

RIA -

RIA -