Software Bill Of Materials (Sbom) Management Market Size and Growth Forecast 2026-2030

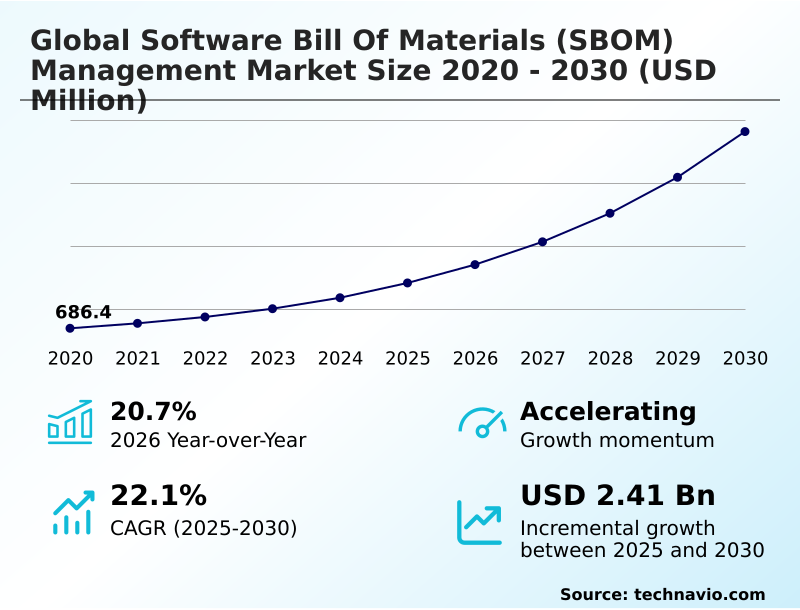

The Software Bill Of Materials (Sbom) Management Market size was valued at USD 1.41 billion in 2025 growing at a CAGR of 22.1% during the forecast period 2026-2030.

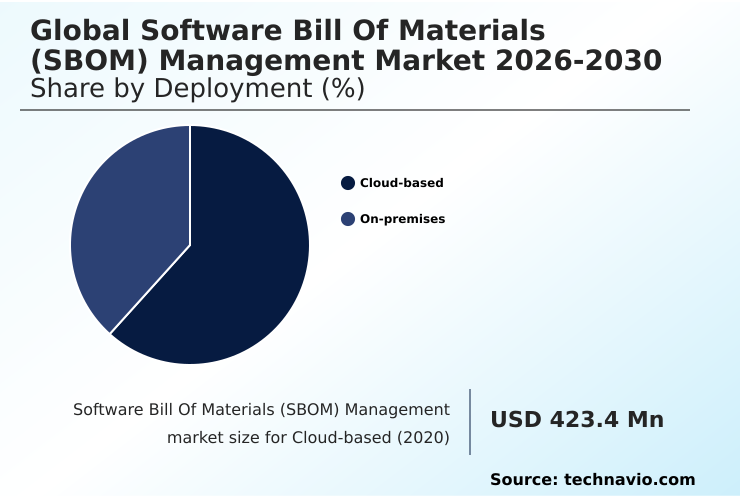

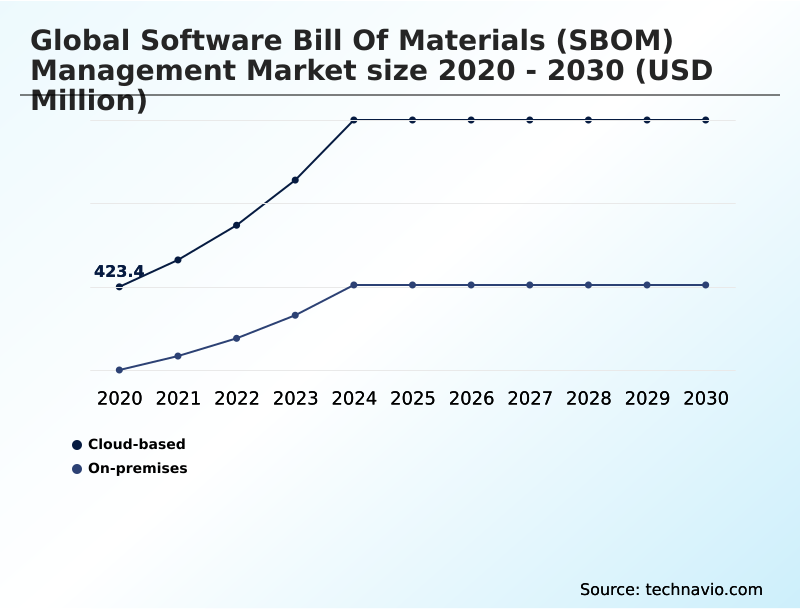

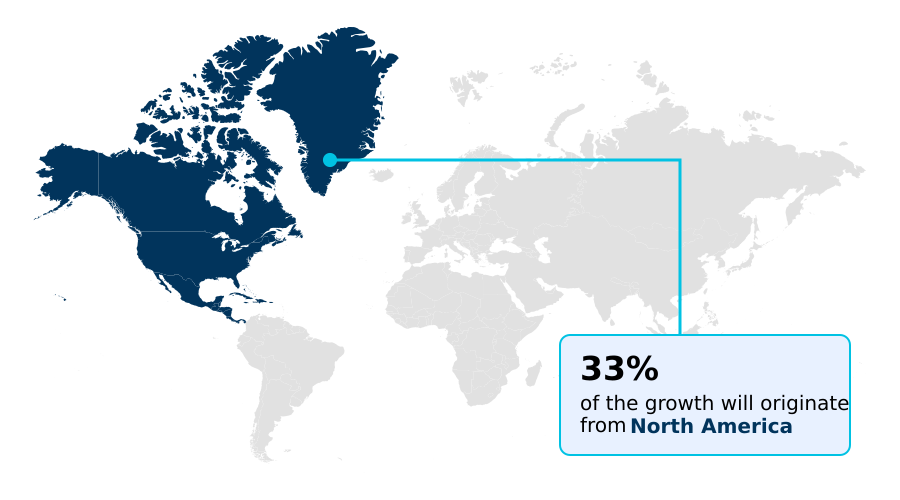

North America accounts for 33.4% of incremental growth during the forecast period. The Cloud-based segment by Deployment was valued at USD 745.2 million in 2024, while the Vulnerability and risk management segment holds the largest revenue share by Application.

The market is projected to grow by USD 3.13 billion from 2020 to 2030, with USD 2.41 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Software Bill Of Materials (Sbom) Management Market Overview

The software bill of materials (sbom) management market is fundamentally shaped by the escalating need for software component transparency amidst rising supply chain attacks. A key driver is the accelerated adoption of devsecops, which necessitates integrating automated security checks directly into the development lifecycle. This shift is particularly evident in regulated sectors; for instance, a medical device manufacturer implementing automated sbom generation ensures continuous compliance with FDA premarket submission guidelines, embedding vulnerability and risk management into its CI/CD pipeline. This proactive stance contrasts sharply with reactive measures, reflecting a broader industry transition toward managing software provenance and integrity from code inception. With North America accounting for over 33% of the market's incremental growth, regulatory pressure from bodies like CISA is setting a global benchmark. The adoption of AI-driven dependency analysis is further refining these processes, enabling more sophisticated threat intelligence integration and reducing the manual overhead associated with open-source license compliance and vulnerability disclosure policies.

Drivers, Trends, and Challenges in the Software Bill Of Materials (Sbom) Management Market

The imperative to secure digital infrastructure is pushing organizations to adopt comprehensive strategies for managing software supply chains. A critical factor is the EU Cyber Resilience Act, which mandates stringent transparency and security-by-design principles, making the implementation of sbom management platforms for automotive software and other critical systems a non-negotiable compliance task.

In a typical automotive OEM setting, leveraging automated sbom generation for ci/cd pipelines is essential to track components from hundreds of tier-one and tier-two suppliers, ensuring that every piece of code meets security and licensing requirements.

As procurement teams are now comparing sbom generation tools for enterprises, the focus is on platforms that offer not just generation but also continuous monitoring and vulnerability prioritization.

Enterprises are discovering that following best practices for sbom implementation, which includes integrating these tools with existing security information and event management systems, can reduce mean-time-to-remediate critical vulnerabilities by over 40% compared to manual tracking methods. The financial impact of sbom on software development costs is offset by reduced risk of breaches and streamlined compliance.

Understanding how to use sbom for vulnerability management becomes a core competency for security teams, who must manage the sbom lifecycle for open source components effectively. The benefits of sbom for developers include faster remediation and clearer guidance, fostering a more secure development culture.

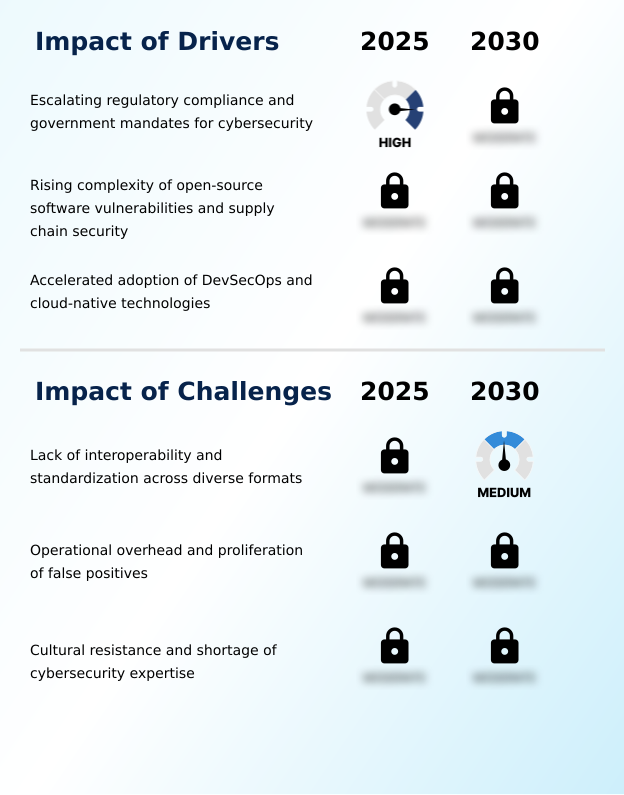

Primary Growth Driver: Escalating regulatory compliance requirements and government mandates for cybersecurity are a primary driver for the adoption of software bill of materials (SBOM) management solutions.

Regulatory pressure and the inherent risks of modern software development are the primary drivers of the software bill of materials (SBOM) management market.

Government mandates, particularly in North America, which commands a 33.37% share of the global market opportunity, have made software supply chain security a prerequisite for public sector contracts. This has forced organizations to adopt formal processes for software component verification.

The widespread use of open-source components has also made open-source vulnerability scanning an essential practice to mitigate risks from software supply chain attacks.

Furthermore, the accelerated adoption of devsecops and cloud-native development requires automated security solutions, making devsecops toolchain integration a critical driver for market growth as organizations seek to embed security without impeding development velocity.

Emerging Market Trend: The integration of artificial intelligence and machine learning for automated dependency analysis represents a key emerging trend. This enables proactive vulnerability prediction and prioritization of critical threats within complex software ecosystems.

Key trends are reshaping the software bill of materials (SBOM) management market, moving it beyond simple inventory creation toward dynamic risk management. The integration of AI-driven dependency analysis is central to this evolution, enabling security teams to perform automated remediation and prioritize threats with greater precision.

This shift is evident as the vulnerability and risk management application segment continues to hold the largest market share. Concurrently, there is a strong push for global standardization around formats like CycloneDX and SPDX, which facilitates better threat intelligence integration across disparate tools and supply chains.

This trend supports a more robust vulnerability disclosure policy, as clear, interoperable data is crucial for rapid communication and response. The market is increasingly focused on the entire sbom lifecycle management, transforming static documents into living inventories for continuous security.

Key Industry Challenge: The lack of interoperability and standardization across diverse documentation formats presents a significant challenge to seamless data exchange and market growth.

A significant challenge constraining the software bill of materials (SBOM) management market is the operational overhead caused by a lack of standardization and the prevalence of false positives. A recent report indicated that 40% of global enterprises struggle to reconcile disparate metadata formats, which impedes efforts toward automated sbom validation and creates significant friction in multi-vendor environments.

This lack of standardization is a critical structural issue. Additionally, security teams often face vulnerability fatigue from a high volume of alerts generated by vulnerability scanning tools, many of which lack the context to determine actual exploitability.

The global shortage of cybersecurity expertise, particularly in interpreting complex vulnerability cvss scores and managing open-source software risks, further exacerbates this challenge, limiting the effective adoption and utilization of advanced SBOM management platforms.

Explore Full Market Dynamics Analysis Request Free Sample

Software Bill Of Materials (Sbom) Management Market Segmentation

The software bill of materials (sbom) management industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Deployment Segment Analysis

The cloud-based segment is estimated to witness significant growth during the forecast period.

The cloud-based deployment model for software bill of materials (sbom) management dominates the market, accounting for approximately 64% of the total share in 2025.

This model's rapid adoption is driven by its inherent scalability and flexibility, which align with modern cloud-native workflows and the accelerated adoption of devsecops.

Organizations increasingly favor cloud solutions to centralize oversight of software components across distributed development teams without significant upfront capital expenditure. These platforms enable seamless automated sbom validation and threat intelligence integration, ensuring that security teams can perform continuous vulnerability discovery.

The software as a service (saas) delivery model is particularly attractive for enterprises requiring sophisticated tools for software supply chain security that can scale with their growing software portfolios and support global regulatory compliance frameworks.

The Cloud-based segment was valued at USD 745.2 million in 2024 and showed a gradual increase during the forecast period.

Software Bill Of Materials (Sbom) Management Market by Region: North America Leads with 33.4% Growth Share

North America is estimated to contribute 33.4% to the growth of the global market during the forecast period.

The geographic landscape of the software bill of materials (SBOM) management market is led by North America, which accounts for 33.37% of the market opportunity, largely due to stringent federal mandates that enforce software supply chain security.

This region sets the global standard for regulatory compliance frameworks and vulnerability disclosure policy.

Meanwhile, APAC is the fastest-growing region, with its market projected to expand at a 23.2% rate, fueled by rapid digitalization and the vast software development ecosystems in China and India.

Europe is also a significant market, driven by initiatives like the Cyber Resilience Act that compel organizations to adopt transparent practices such as using the cyclonedx format for interoperability.

This global divergence highlights a mature, regulation-driven market in the West versus a rapidly expanding, adoption-focused market in the East.

Customer Landscape Analysis for the Software Bill Of Materials (Sbom) Management Market

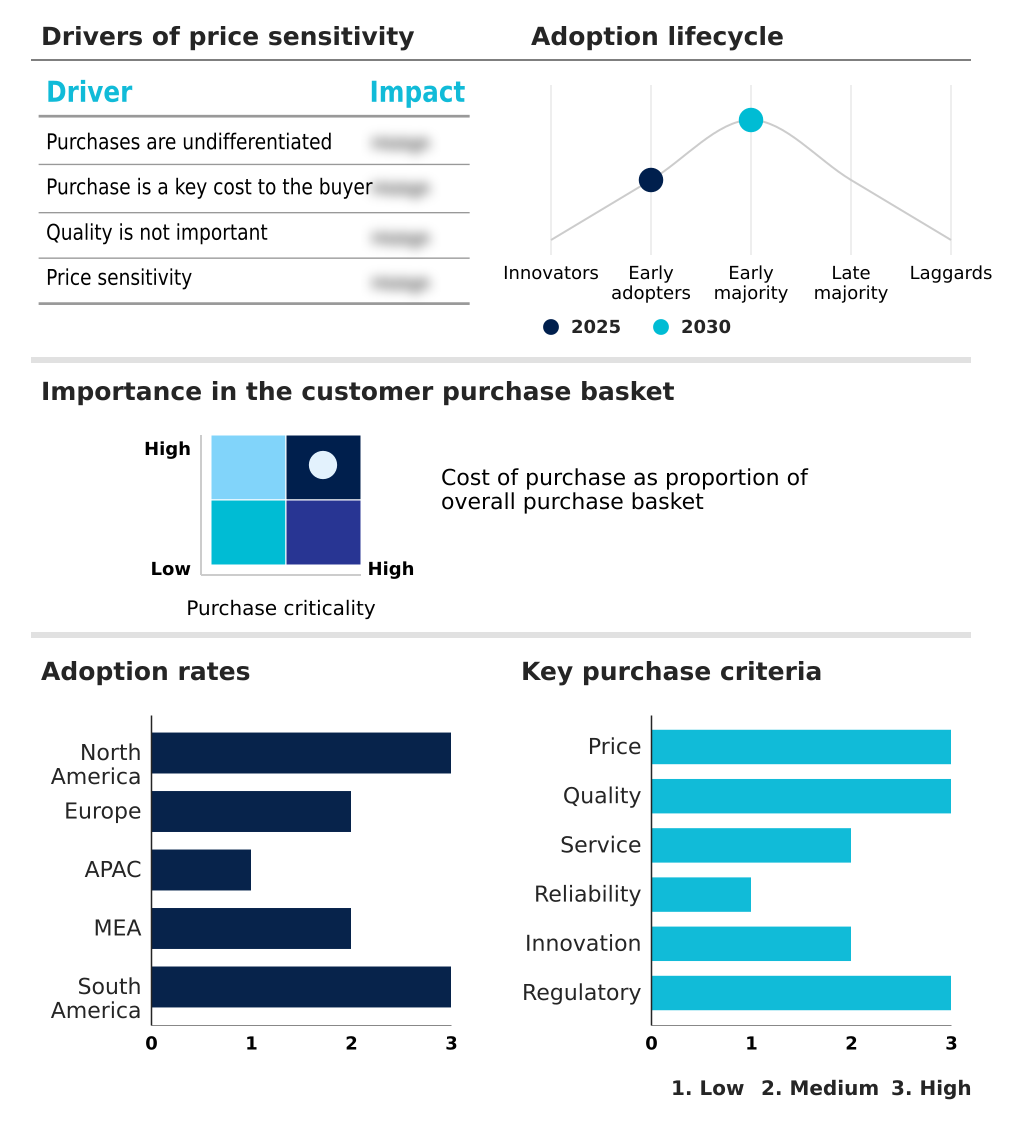

The software bill of materials (sbom) management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the software bill of materials (sbom) management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Software Bill Of Materials (Sbom) Management Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the software bill of materials (sbom) management market industry.

Anchore Inc. - Offerings center on deep container inspection and filesystem analysis to generate comprehensive component inventories for securing cloud-native applications and ensuring software component transparency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anchore Inc.

- Aqua Security Software Ltd.

- ArmorCode

- Chainguard

- Checkmarx Ltd.

- Codenotary

- Cybeats Technologies Inc.

- Finite State Inc.

- Flexera Software LLC

- FOSSA Inc.

- JFrog Ltd.

- Karamba Security Ltd.

- Mend.io

- Palo Alto Networks Inc.

- ReversingLabs

- ServiceNow Inc.

- Snyk Ltd.

- Sonatype Inc.

- Veracode Inc.

- Vigilant Ops

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Software Bill Of Materials (Sbom) Management Market

- In March 2025, Finite State Inc. released updated firmware analysis modules designed to enhance the security of critical infrastructure and embedded systems.

- In March 2025, Karamba Security Ltd. also launched updated firmware analysis modules, focusing on strengthening the security posture of IoT and automotive software.

- In February 2025, the International Organization for Standardization introduced a new protocol to facilitate the automated exchange of software bill of materials data across international borders.

- In March 2025, the US Department of Commerce published a comprehensive update to its minimum elements for a software bill of materials, mandating more stringent requirements for component origin identification.

Research Analyst Overview: Software Bill Of Materials (Sbom) Management Market

The software bill of materials (sbom) management market is maturing from a compliance-centric necessity to a strategic tool for proactive risk management. Boardroom decisions increasingly weigh the total cost of ownership of a comprehensive cloud native application protection platform (cnapp) against siloed software composition analysis (sca) tools, with a clear trend toward integrated solutions.

This shift is driven by the operational need for a single source of truth that supports not just vulnerability scanning but also advanced capabilities like vulnerability reachability mapping and zero-day vulnerability response. Adherence to standards like ISO/IEC 5230 for open-source license compliance is no longer optional but a baseline for vendor qualification.

With year-over-year market growth hitting 20.7%, investment is accelerating in technologies that automate and secure the entire software lifecycle. The rise of immutable ledger technology for ensuring code provenance tracking further underscores the market's move toward verifiable, end-to-end software supply chain security and robust devsecops toolchain integration.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Software Bill Of Materials (Sbom) Management Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 22.1% |

| Market growth 2026-2030 | USD 2408.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 20.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, China, India, Japan, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Software Bill Of Materials (Sbom) Management Market: Key Questions Answered in This Report

-

What is the expected growth of the Software Bill Of Materials (Sbom) Management Market between 2026 and 2030?

-

The Software Bill Of Materials (Sbom) Management Market is expected to grow by USD 2.41 billion during 2026-2030, registering a CAGR of 22.1%. Year-over-year growth in 2026 is estimated at 20.7%%. This acceleration is shaped by escalating regulatory compliance and government mandates for cybersecurity, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, and On-premises), Application (Vulnerability and risk management, Compliance and governance management, and SBOM generation and discovery), End-user (Software developers, DevOps and CI teams, Security teams, Compliance and risk officers, and Government and regulated industries) and Geography (North America, Europe, APAC, Middle East and Africa, South America). Among these, the Cloud-based segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, Middle East and Africa and South America. North America is estimated to contribute 33.4% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, China, India, Japan, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is escalating regulatory compliance and government mandates for cybersecurity, which is accelerating investment and industry demand. The main challenge is lack of interoperability and standardization across diverse formats, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Software Bill Of Materials (Sbom) Management Market?

-

Key vendors include Anchore Inc., Aqua Security Software Ltd., ArmorCode, Chainguard, Checkmarx Ltd., Codenotary, Cybeats Technologies Inc., Finite State Inc., Flexera Software LLC, FOSSA Inc., JFrog Ltd., Karamba Security Ltd., Mend.io, Palo Alto Networks Inc., ReversingLabs, ServiceNow Inc., Snyk Ltd., Sonatype Inc., Veracode Inc. and Vigilant Ops. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Software Bill Of Materials (Sbom) Management Market Research Insights

The market dynamics for software bill of materials (SBOM) management are heavily influenced by the push for greater software component transparency, driven by an increase in sophisticated software supply chain attacks. As organizations grapple with third-party software risk management, the adoption of standardized formats like Software Package Data Exchange (SPDX) becomes critical for interoperability.

The market's shift toward cloud-based solutions is pronounced, with this segment projected to be nearly double the size of on-premises deployments by 2025. In practice, security teams are leveraging open source vulnerability scanning and software composition analysis within the CI/CD pipeline to automatically identify and flag risks, moving from periodic audits to continuous security assurance and effective vulnerability management.

We can help! Our analysts can customize this software bill of materials (sbom) management market research report to meet your requirements.

RIA -

RIA -