Software-defined Vehicle (SDV) Market Size 2026-2030

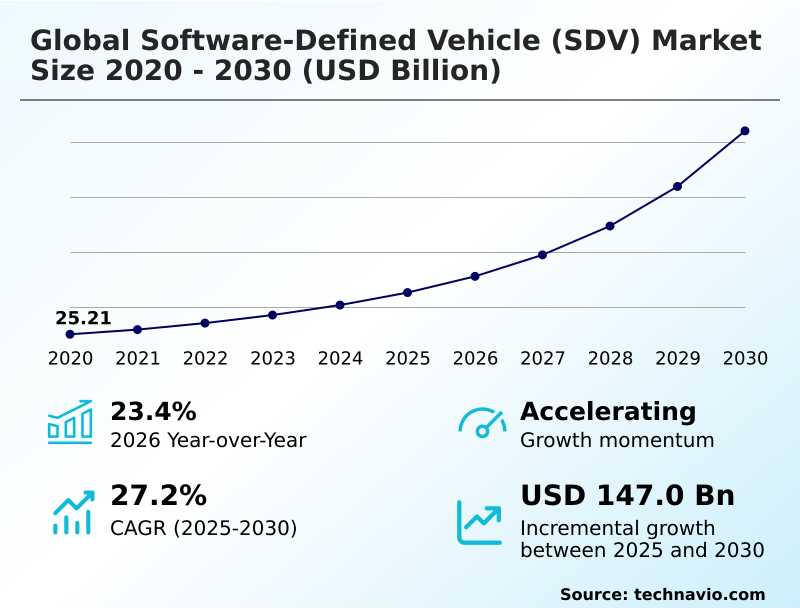

The software-defined vehicle (sdv) market size is valued to increase by USD 147.00 billion, at a CAGR of 27.2% from 2025 to 2030. Increasing demand for autonomous vehicles will drive the software-defined vehicle (sdv) market.

Major Market Trends & Insights

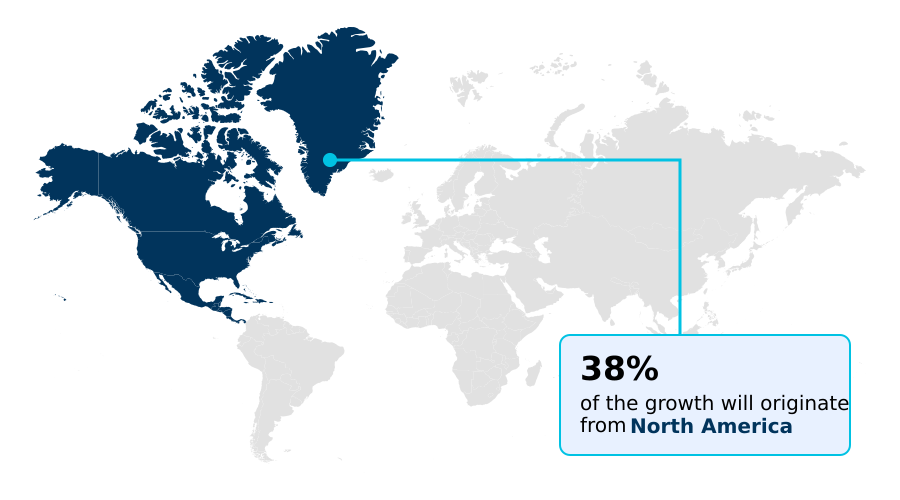

- North America dominated the market and accounted for a 38.4% growth during the forecast period.

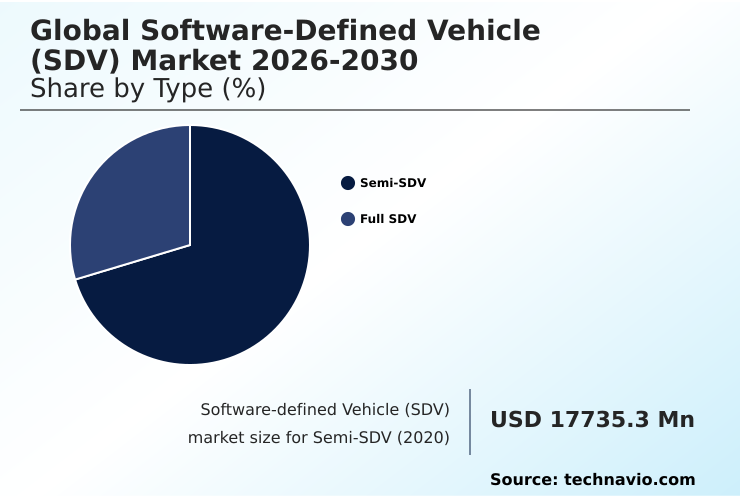

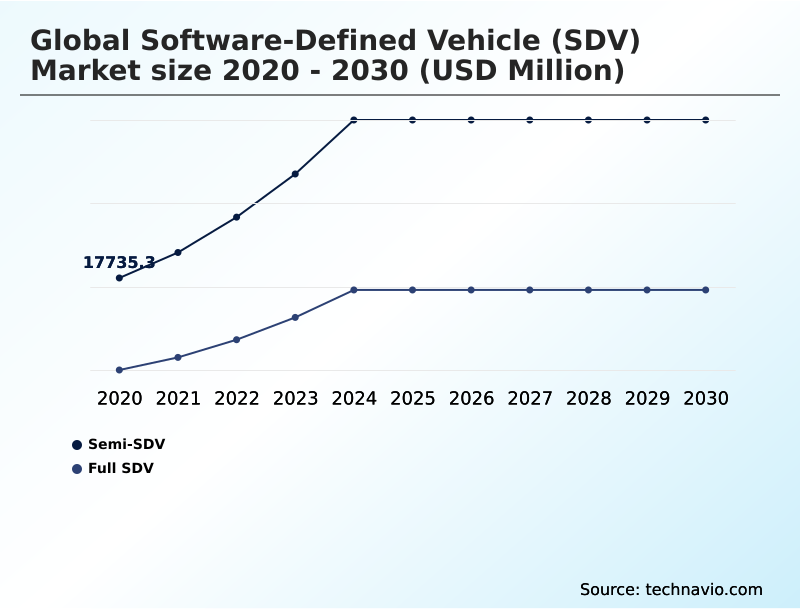

- By Type - Semi-SDV segment was valued at USD 35.35 billion in 2024

- By Vehicle Type - Passenger cars segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 184.90 billion

- Market Future Opportunities: USD 147.00 billion

- CAGR from 2025 to 2030 : 27.2%

Market Summary

- The software-defined vehicle (SDV) market represents a fundamental transformation, shifting the basis of automotive value from mechanical engineering to software innovation. This evolution is driven by consumer demand for connectivity and personalization, mirroring experiences with consumer electronics. Vehicles are becoming dynamic platforms capable of receiving over-the-air updates that enhance performance, safety, and infotainment features throughout the vehicle's lifecycle.

- A key business scenario involves fleet management, where predictive maintenance algorithms analyze real-time vehicle data to forecast component failures, reducing downtime and optimizing operational efficiency. However, this transition introduces significant challenges, including managing immense software complexity and ensuring robust cybersecurity against remote threats.

- The industry's move toward centralized E/E architecture and high-performance computing is essential for enabling advanced driver-assistance systems and paving the way for full autonomy, fundamentally redefining mobility and creating new revenue streams through on-demand services.

What will be the Size of the Software-defined Vehicle (SDV) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Software-defined Vehicle (SDV) Market Segmented?

The software-defined vehicle (sdv) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Semi-SDV

- Full SDV

- Vehicle type

- Passenger cars

- Commercial vehicles

- Application

- Powertrain control

- Advanced driver-assistance systems (ADAS)

- Infotainment and connectivity

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- Japan

- South Korea

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The semi-sdv segment is estimated to witness significant growth during the forecast period.

The semi-software-defined vehicle segment represents a critical transitional phase in the industry's E/E architecture transformation. This category is characterized by a domain-controlled architecture, where a domain controller unit manages distinct functionalities.

While it represents consolidation from legacy designs, the software-hardware decoupling is incomplete, limiting the scope of over-the-air updates. These updates are often restricted to non-critical systems like in-vehicle infotainment, impacting less than 30% of the vehicle’s functional domains.

This approach allows manufacturers to introduce subscription-based features and connected car services without a complete overhaul, balancing innovation with existing vehicle lifecycle management strategies.

The focus remains on progressing toward a true software-first development model through incremental advances in embedded software development.

The Semi-SDV segment was valued at USD 35.35 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Software-defined Vehicle (SDV) Market Demand is Rising in North America Get Free Sample

The geographic landscape is highly dynamic, with North America expected to command approximately 38% of the market's incremental growth. This region's leadership is fueled by intense competition and strong consumer adoption of new technologies.

Europe follows, contributing around 28% of the growth, driven by stringent regulations and deep automotive engineering expertise. The APAC region, securing about 26%, is the fastest-growing area, led by China's massive market scale and rapid innovation.

A key enabler is the move toward a zonal architecture, which simplifies vehicle-to-everything communication. This transition is supported by the adoption of automotive grade linux and advanced vehicle virtualization techniques.

These regional dynamics highlight a global push toward creating a comprehensive digital thread for automotive manufacturing.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The transition to the software-defined vehicle introduces profound complexity in managing software complexity in SDVs. The core challenge lies in the effective decoupling of software from hardware, a task central to achieving true modularity. The role of middleware in SDV platforms is therefore critical, providing the abstraction layer that enables independent development cycles and seamless integration.

- For commercial vehicles, adopting an SDV architecture for commercial vehicles promises significant operational gains through OTA updates for powertrain control and predictive maintenance in electric vehicles. However, ensuring cybersecurity in centralized vehicle computers is a non-negotiable requirement, governed by rigorous industry standards.

- The impact of 5G on V2X communication is transformative, enabling real-time data exchange for enhanced safety and traffic efficiency. This connectivity underpins the HPC platform for autonomous driving, which processes immense data streams. The industry is also exploring new business models, such as the subscription model for in-car features and on-demand ADAS feature activation via software.

- To manage this evolution, automakers are leveraging the benefits of virtual ECU testing and creating a digital twin for vehicle simulation, achieving development cycles that are more than 50% faster than traditional methods. The vehicle OS impact on development is profound, dictating everything from application deployment to system-wide security.

- Strategic decisions around SOA for cross-domain communication and the use of an automotive hypervisor for mixed-criticality systems are essential for ensuring functional safety in zonal architectures. The migration from domain to zonal architectures and the AI integration in smart cockpits represent the next frontier in this technological shift, which is further complicated by the challenges of software-hardware decoupling.

- A robust cloud platform for HD mapping is also a prerequisite for advancing autonomous capabilities.

What are the key market drivers leading to the rise in the adoption of Software-defined Vehicle (SDV) Industry?

- The increasing demand for autonomous vehicles is a key market driver, necessitating advanced, centrally managed software-defined vehicle architectures to process complex environmental data.

- Market growth is being driven by the architectural shift toward high-performance computing and a centralized E/E architecture. This enables the development of an intelligent vehicle platform capable of supporting mobility-as-a-service business models.

- The use of middleware layer abstraction is critical, allowing for a software-defined powertrain that can be optimized for efficiency, leading to a 10% improvement in energy consumption in certain use cases.

- The adoption of cloud-native automotive software, coupled with continuous integration/continuous deployment pipelines, has been shown to reduce development and validation cycles by up to 25%.

- A sophisticated AI-driven mobility platform relies on this infrastructure to process data from sensor fusion algorithms, paving the way for more advanced autonomous capabilities and connected services.

What are the market trends shaping the Software-defined Vehicle (SDV) Industry?

- The integration of advanced safety technologies within luxury vehicles is a prominent market trend, driven by escalating consumer demand for enhanced protection and stricter safety regulations.

- Key market trends are reshaping the in-vehicle experience and operational capabilities. The vehicle operating system is becoming the central nervous system, enabling a sophisticated smart cockpit technology and a next-generation user experience. This platform supports an in-vehicle app marketplace, allowing for feature-on-demand activation and continuous value delivery.

- The integration of advanced driver-assistance systems is evolving, with data-driven vehicle development enabling performance improvements of over 20% through software updates. Automakers are leveraging the AUTOSAR adaptive platform to manage the complexity of these systems. Furthermore, predictive maintenance algorithms are gaining traction, capable of reducing unplanned downtime by up to 30%.

- This shift toward an AI-defined vehicle is not just about features but about creating an adaptable, intelligent mobility platform.

What challenges does the Software-defined Vehicle (SDV) Industry face during its growth?

- A significant challenge affecting industry growth is the decline in automotive production caused by the global shortage of mission-critical semiconductor chips.

- Significant challenges stem from rising system complexity and stringent safety requirements. Adherence to ISO 26262 functional safety and UN R155 cybersecurity standards necessitates a robust automotive cybersecurity framework and a secure automotive software stack. The introduction of zonal security concepts and the use of an automotive hypervisor are critical for isolating safety-critical functions from other domains.

- The sheer volume of code, which has increased by over 100% in recent vehicle generations, escalates development and validation costs. Managing this intricate web of software component management through virtual ECU simulation and other advanced tools is essential, as failure to do so can increase post-launch patch deployments by over 50%.

- The underlying automotive ethernet and real-time operating system must also be secured to prevent vulnerabilities.

Exclusive Technavio Analysis on Customer Landscape

The software-defined vehicle (sdv) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the software-defined vehicle (sdv) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Software-defined Vehicle (SDV) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, software-defined vehicle (sdv) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arm Ltd. - A diverse range of companies, from semiconductor manufacturers to embedded software specialists and major Tier-1 suppliers, provide critical solutions for the evolving automotive ecosystem.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arm Ltd.

- Arorian Technologies GmbH

- BlackBerry Ltd.

- Bluekei Solutions Pvt.Ltd.

- Continental AG

- ETAS GmbH

- Expleo Group SAS

- Keysight Technologies Inc.

- Larsen and Toubro Ltd.

- MulticoreWare Inc.

- NCC Group Plc

- NTT DATA Corp.

- NXP Semiconductors NV

- Real-Time Innovations Inc.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Siemens AG

- u blox AG

- Vector Informatik GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Software-defined vehicle (sdv) market

- In May 2025, BlackBerry Ltd expanded its QNX hypervisor capabilities by launching QNX Hypervisor 8.0, a new embedded virtualization solution designed to streamline and accelerate development across automotive and IoT systems.

- In January 2025, Intel announced its expanded automotive technology portfolio, including an adaptive control solution and a virtual development environment with AWS to help automakers transition to electric and software-defined vehicles.

- In June 2024, NXP Semiconductors NV introduced its S32 CoreRide platform, offering automakers a unified approach to manage hardware, software, and safety functions for software-defined vehicle development.

- In May 2024, BlackBerry Ltd and ETAS GmbH expanded their partnership to jointly market a solution aimed at accelerating the development of safety-critical functions for next-generation software-defined vehicles.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Software-defined Vehicle (SDV) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 27.2% |

| Market growth 2026-2030 | USD 146995.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 23.4% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, Japan, South Korea, India, Indonesia, Australia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Morocco |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is centered on the shift to a centralized E/E architecture, which serves as the foundation for innovation. This architectural change enables a complete software-hardware decoupling, facilitated by middleware layer abstraction and a dedicated vehicle operating system. Such a setup is crucial for deploying an advanced AI-driven mobility platform and sophisticated smart cockpit technology.

- Key functionalities like over-the-air updates and predictive maintenance algorithms depend on this software-centric approach. From a boardroom perspective, this transformation directly impacts long-term revenue strategy, moving from one-time sales to continuous monetization through subscription services. The adoption of service-oriented architecture and an automotive hypervisor is critical for managing system complexity.

- Ensuring compliance with ISO 26262 functional safety and UN R155 cybersecurity standards during embedded software development is paramount, with a focus on high-performance computing to run complex sensor fusion algorithms. This approach has led to a 30% reduction in diagnostic resolution times, showcasing tangible operational improvements.

- The entire ecosystem, from the automotive digital twin and automotive ethernet to the domain controller unit and real-time operating system, is being re-engineered.

What are the Key Data Covered in this Software-defined Vehicle (SDV) Market Research and Growth Report?

-

What is the expected growth of the Software-defined Vehicle (SDV) Market between 2026 and 2030?

-

USD 147.00 billion, at a CAGR of 27.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Semi-SDV, and Full SDV), Vehicle Type (Passenger cars, and Commercial vehicles), Application (Powertrain control, Advanced driver-assistance systems (ADAS), Infotainment and connectivity, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for autonomous vehicles, Decline in automotive production due to global shortage of semiconductor chips

-

-

Who are the major players in the Software-defined Vehicle (SDV) Market?

-

Arm Ltd., Arorian Technologies GmbH, BlackBerry Ltd., Bluekei Solutions Pvt.Ltd., Continental AG, ETAS GmbH, Expleo Group SAS, Keysight Technologies Inc., Larsen and Toubro Ltd., MulticoreWare Inc., NCC Group Plc, NTT DATA Corp., NXP Semiconductors NV, Real-Time Innovations Inc. , Robert Bosch GmbH, Samsung Electronics Co. Ltd., Siemens AG, u blox AG and Vector Informatik GmbH

-

Market Research Insights

- The market is defined by a strategic E/E architecture transformation, where OEMs pursue software-first development to deliver a next-generation user experience. This shift enables new business models centered on subscription-based features and continuous integration/continuous deployment pipelines, which can accelerate feature rollout by up to 40%.

- The adoption of cloud-native automotive software and intelligent vehicle platforms supports this evolution, providing the backbone for advanced connected car services. Managing the complex automotive software stack is a critical focus, with successful integration leading to a 25% improvement in diagnostic accuracy.

- As the industry moves toward the AI-defined vehicle, the focus on a cohesive software component management strategy becomes paramount for sustaining innovation and market differentiation.

We can help! Our analysts can customize this software-defined vehicle (sdv) market research report to meet your requirements.

RIA -

RIA -