India Solar Power Market Size 2026-2030

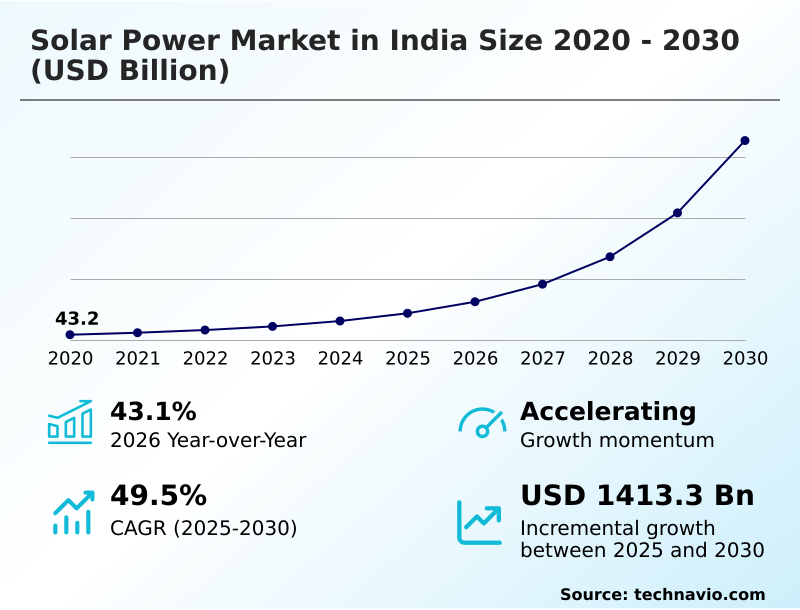

The india solar power market size is valued to increase by USD 1413.3 billion, at a CAGR of 49.5% from 2025 to 2030. Supportive government policies and strategic national initiatives will drive the india solar power market.

Major Market Trends & Insights

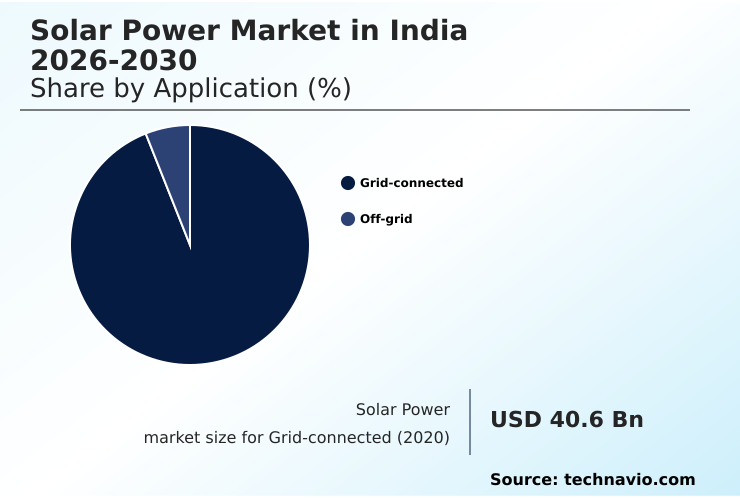

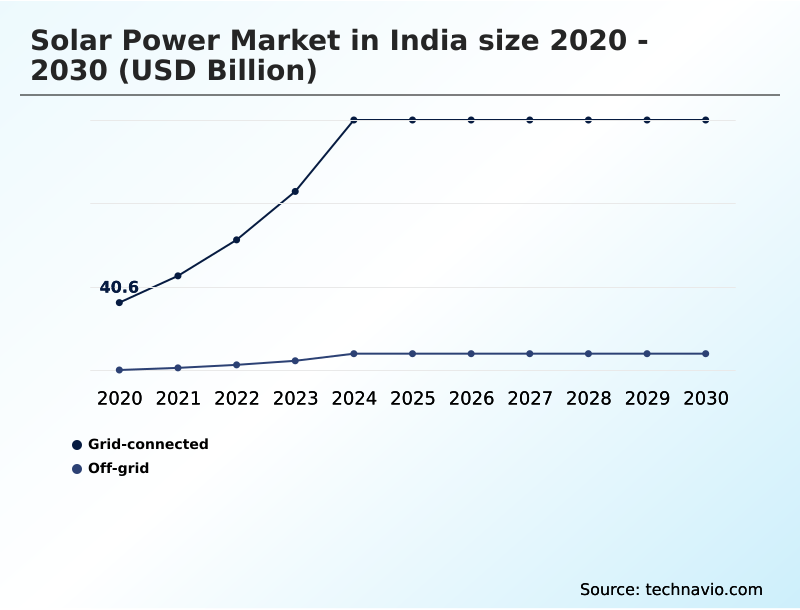

- By Application - Grid-connected segment was valued at USD 143.6 billion in 2024

- By End-user - Utility segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1588.7 billion

- Market Future Opportunities: USD 1413.3 billion

- CAGR from 2025 to 2030 : 49.5%

Market Summary

- The solar power market in India is undergoing a period of exceptional expansion, driven by a strong government commitment to decarbonization and energy security. This growth is underpinned by the increasing economic competitiveness of photovoltaic technology, which has positioned solar as a mainstream energy source.

- Key trends include a strategic push for domestic solar module manufacturing to reduce import reliance and the rapid adoption of rooftop solar installations by residential and commercial users. For instance, businesses are increasingly leveraging onsite solar generation to lower operational electricity costs and meet corporate sustainability mandates, optimizing their energy procurement strategies.

- However, the market faces significant hurdles, including the need for substantial upgrades to grid infrastructure to handle intermittent renewable power and the complexities associated with land acquisition for large utility-scale projects. Addressing these challenges is critical to sustaining the market's growth trajectory and achieving the nation's ambitious clean energy targets.

What will be the Size of the India Solar Power Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the India Solar Power Market Segmented?

The india solar power industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Grid-connected

- Off-grid

- End-user

- Utility

- Rooftop

- Technology

- Photovoltaic systems

- Concentrated solar power

- Geography

- APAC

- India

- APAC

By Application Insights

The grid-connected segment is estimated to witness significant growth during the forecast period.

The grid-connected segment is the primary component of the solar power market in India, driven by utility-scale projects and distributed rooftop solar installations.

These systems, integral to the national energy strategy, benefit from supportive regulatory mechanisms like renewable purchase obligations and competitive solar tariff auctions.

The development of extensive solar park infrastructure with shared resources de-risks large investments, attracting significant capital for solar EPC services.

Technological advancements toward high-efficiency module technology, including TOPCon solar cells, are enhancing the economic viability for both large solar farms and smaller systems.

Widespread adoption is further enabled by structured power purchase agreements, although effective integration requires robust grid stability solutions to manage the intermittent nature of solar energy, which represents over 95% of new capacity additions.

The Grid-connected segment was valued at USD 143.6 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A strategic analysis of the market reveals several interconnected dynamics shaping investment and operational decisions. The impact of PLI scheme on solar manufacturing is profound, catalyzing a domestic ecosystem, yet supply chain risks in solar component imports persist, particularly for upstream materials.

- While advancements in high-efficiency solar modules, such as comparing TOPCon and heterojunction cell efficiency, promise better yields, the operational challenges of floating solar farms and land acquisition bottlenecks for solar parks remain significant hurdles. The economic viability of solar-plus-storage projects is improving, but this is closely tied to the challenges of grid integration for solar power.

- Utility-scale solar project financing models are evolving to de-risk investments, while financial incentives for commercial solar adoption are driving growth in the C&I segment. The regulatory framework for power purchase agreements and the role of virtual power purchase agreements are critical for large-scale corporate procurement.

- The cost-effectiveness of rooftop solar installations is bolstered by favorable net metering policy impact on residential solar, yet the debate between photovoltaic systems vs concentrated solar power continues, especially regarding the viability of concentrated solar power with thermal storage.

- Furthermore, the role of solar in green hydrogen production, the benefits of agrivoltaics for farmers, and the development of off-grid solar solutions for rural electrification represent significant long-term growth avenues. Technological shifts in the solar inverter market are also pivotal, with some advanced systems improving energy conversion by over 3% compared to older models.

What are the key market drivers leading to the rise in the adoption of India Solar Power Industry?

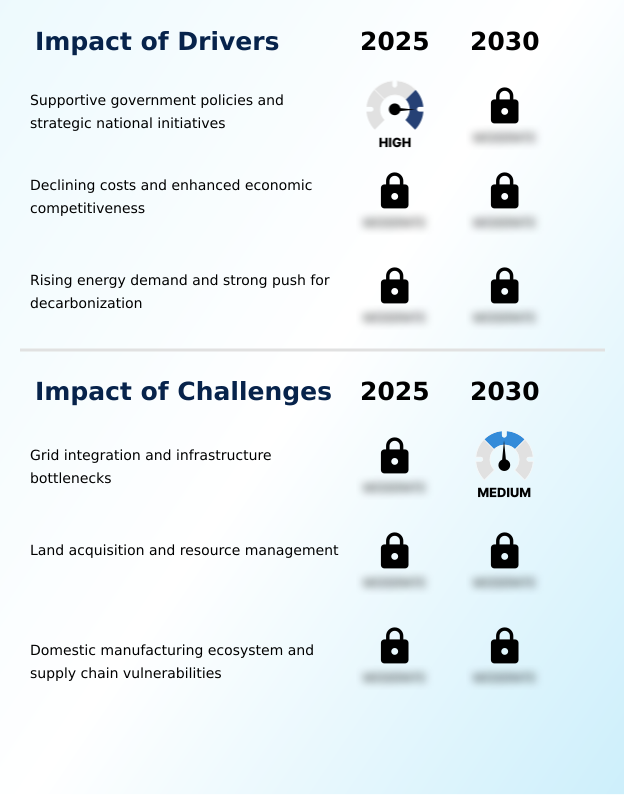

- Supportive government policies and strategic national initiatives function as a primary driver, fostering a stable and attractive environment for investment in the market.

- Market growth is propelled by a convergence of supportive policies and powerful economic drivers. Proactive government frameworks, including net metering policies and domestic content requirements, create a stable investment climate.

- The sharp decline in the levelized cost of energy, with solar tariff auctions consistently reaching record lows, makes concentrated solar power more competitive. This has spurred an increase of over 200% in corporate green energy procurement in recent years.

- Surging energy demand from a rapidly industrializing economy, coupled with a national commitment to decarbonization, provides a strong, long-term demand signal.

- The financial attractiveness of solar water pumps and thermal energy storage investments is further enhanced by innovative green project financing models.

What are the market trends shaping the India Solar Power Industry?

- A prominent trend influencing the market is the explosive growth in domestic solar module manufacturing. This strategic expansion is catalyzed by government policies aimed at achieving energy sector self-reliance.

- Key trends are reshaping the solar power market in India, led by the rapid expansion of the domestic manufacturing ecosystem. This strategic push, fueled by government incentives, is reducing reliance on imports and fostering local production of PV modules and balance of system components. Another significant trend is the surge in decentralized power generation, with rooftop solar installations growing exponentially.

- This is democratizing energy access, enabling consumers to achieve savings of up to 40% on electricity bills. The integration with the emerging green hydrogen production economy is also creating a new demand frontier for solar power, with projects now being designed to power electrolyzer capacity.

- This synergy supports the decarbonization of hard-to-abate sectors, enhancing the overall value proposition of solar energy.

What challenges does the India Solar Power Industry face during its growth?

- The challenge of integrating large-scale renewable capacity with existing grid infrastructure, coupled with transmission bottlenecks, poses a significant constraint on market growth.

- Despite rapid growth, the solar power market in India grapples with significant operational and infrastructural challenges. The land acquisition process for solar trackers and thin-film solar cells is a major bottleneck, with procedural delays often extending project timelines by over 12 months.

- Inadequate grid infrastructure leads to frequent solar power curtailment, with some resource-rich regions reporting energy losses of up to 15% during peak generation hours, undermining the financial viability of solar investments. Furthermore, while monocrystalline silicon assembly is growing, the solar supply chain logistics remain vulnerable due to heavy reliance on imported upstream components like polycrystalline silicon.

- These persistent issues in the renewable energy service company pose a strategic risk to the market's long-term stability and growth ambitions.

Exclusive Technavio Analysis on Customer Landscape

The india solar power market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the india solar power market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of India Solar Power Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, india solar power market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Offers vertically integrated solutions from giga-scale solar module manufacturing to the execution of utility-scale renewable energy projects, ensuring end-to-end value chain control.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Adani Group

- Azure Power Global Ltd.

- Huawei Technologies Co. Ltd.

- JA Solar Technology Co. Ltd.

- juwi AG

- Larsen and Toubro Ltd.

- Mahindra and Mahindra Ltd.

- Reliance Industries Ltd.

- ReNew Energy Global Plc

- SMA Solar Technology AG

- Sungrow Power Supply Co. Ltd.

- Sunsure Energy

- Suzlon Energy Ltd.

- Tata Power Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in India solar power market

- In April, 2025, the Ministry of New and Renewable Energy announced the fourth tranche of its Production Linked Incentive scheme, earmarking funds to promote domestic manufacturing of high-efficiency TOPCon and Heterojunction solar cells.

- In August, 2025, a leading Indian conglomerate announced the commissioning of the country's first large-scale grid-connected solar-plus-storage facility in Gujarat, designed to provide dispatchable power.

- In March, 2025, the Solar Energy Corporation of India concluded an auction for a 2-gigawatt interstate transmission system-connected solar project, which resulted in record-low winning tariffs.

- In May, 2025, a prominent non-governmental organization, in partnership with a financial institution, launched a program to deploy over 50,000 solar home systems across tribal communities in central India.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Solar Power Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 176 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 49.5% |

| Market growth 2026-2030 | USD 1413.3 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 43.1% |

| Key countries | India |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The solar power market in India is defined by a rapid transition toward energy self-sufficiency and decarbonization, a shift that is compelling boardroom-level strategic recalculations. The aggressive implementation of the production linked incentive is central to this, forcing companies to re-evaluate supply chain dependencies and capital allocation for domestic solar module manufacturing.

- This move towards vertical integration, encompassing everything from polysilicon and wafer production to solar cell technology, is a direct response to geopolitical risks. Vertically integrated firms have demonstrated up to a 20% reduction in project cost overruns linked to import disruptions.

- Investment in solar EPC services is increasingly focused on deploying high-efficiency module technology like bifacial solar panels and heterojunction technology. The market's architecture is also changing, with a growing emphasis on hybrid renewable projects that combine photovoltaic technology with energy storage systems to provide ancillary grid services and round-the-clock renewable power.

- This requires sophisticated solar asset management and energy yield analysis to ensure financial viability, especially with ongoing solar power curtailment issues.

What are the Key Data Covered in this India Solar Power Market Research and Growth Report?

-

What is the expected growth of the India Solar Power Market between 2026 and 2030?

-

USD 1413.3 billion, at a CAGR of 49.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Grid-connected, and Off-grid), End-user (Utility, and Rooftop), Technology (Photovoltaic systems, and Concentrated solar power) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Supportive government policies and strategic national initiatives, Grid integration and infrastructure bottlenecks

-

-

Who are the major players in the India Solar Power Market?

-

ABB Ltd., Adani Group, Azure Power Global Ltd., Huawei Technologies Co. Ltd., JA Solar Technology Co. Ltd., juwi AG, Larsen and Toubro Ltd., Mahindra and Mahindra Ltd., Reliance Industries Ltd., ReNew Energy Global Plc, SMA Solar Technology AG, Sungrow Power Supply Co. Ltd., Sunsure Energy, Suzlon Energy Ltd. and Tata Power Co. Ltd.

-

Market Research Insights

- The market's dynamism is driven by compelling economic incentives and evolving procurement strategies. The adoption of open access solar frameworks allows commercial and industrial entities to reduce energy costs by over 30% compared to grid tariffs.

- Simultaneously, the deployment of battery energy storage systems in conjunction with solar is improving project viability, with solar-plus-storage tenders demonstrating the potential for round-the-clock renewable power at competitive rates. The focus on captive power plants is also growing, as industrial users seek energy independence, a trend that improves their operational resilience by 25% during periods of grid instability.

- These shifts are fostering a more decentralized power generation landscape, supported by innovative project financing models.

We can help! Our analysts can customize this india solar power market research report to meet your requirements.

RIA -

RIA -