Stationary Emission Control Catalyst Market Size 2024-2028

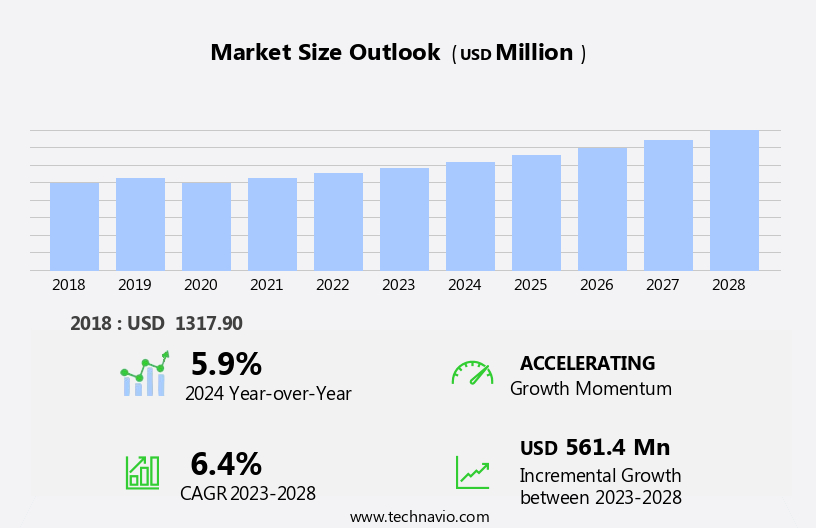

The stationary emission control catalyst market size is forecast to increase by USD 561.4 million at a CAGR of 6.4% between 2023 and 2028.

- The market is driven by stringent emission control regulations and the growing importance of adding catalytic converters to reduce car emissions. Regulatory bodies worldwide are imposing increasingly rigorous standards to limit industrial emissions, creating a significant demand for effective stationary emission control catalysts. This trend is further fueled by the increasing awareness of environmental concerns and the need to minimize air pollution. However, high maintenance costs associated with stationary emission control catalysts pose a challenge to market growth. The complex nature of these catalysts and the need for regular replacement or refurbishment can lead to significant expenses for businesses.

- Supply chain inconsistencies also temper growth potential, as the availability and reliability of raw materials can impact production and delivery schedules. Companies seeking to capitalize on market opportunities must focus on developing cost-effective catalysts with extended lifetimes and reliable supply chains. By addressing these challenges, they can effectively navigate the market landscape and meet the evolving needs of their customers.

What will be the Size of the Stationary Emission Control Catalyst Market during the forecast period?

- The market is experiencing significant activity and trends as businesses prioritize energy efficiency and regulatory compliance. Catalytic combustion systems, including lean NOx traps, play a crucial role in reducing harmful emissions, enhancing air quality, and promoting sustainable development. Catalyst formulation and synthesis are key areas of focus, with researchers exploring catalyst composition, catalyst loading, and catalyst surface area to improve catalyst efficiency and activity. Energy efficiency is a major concern, with process optimization and renewable energy integration becoming essential for cost-effective solutions. Catalyst aging and deactivation mechanisms are also under scrutiny to extend catalyst life and minimize environmental impact.

- Emission management strategies incorporate air quality monitoring and emission monitoring equipment to ensure continuous compliance with environmental protection regulations. Catalyst pore size and catalyst selectivity are critical factors in clean technology applications, as they influence the catalyst's ability to effectively reduce various pollutants. Overall, the market is driven by the need for effective, cost-effective, and sustainable emission reduction solutions.

How is this Stationary Emission Control Catalyst Industry segmented?

The stationary emission control catalyst industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Honeycomb catalyst

- Plate catalyst

- Corrugated catalyst

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

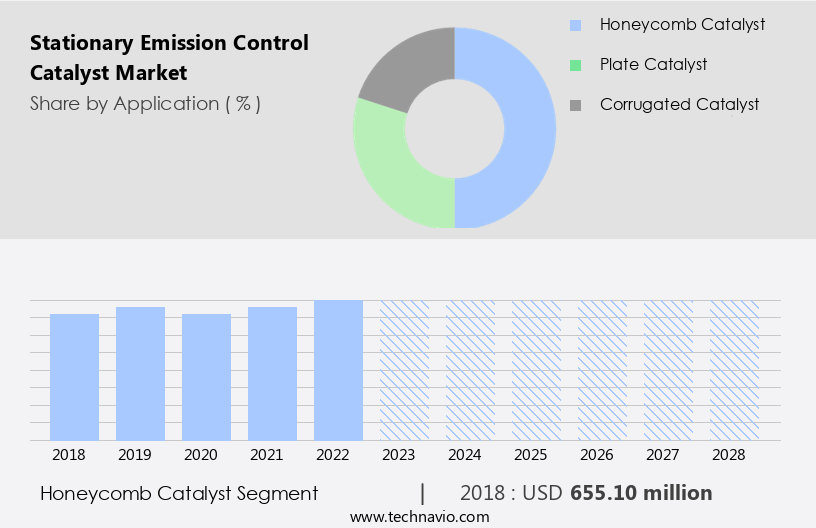

The honeycomb catalyst segment is estimated to witness significant growth during the forecast period.

In the realm of emission control, stationary sources continue to prioritize the reduction of sulfur dioxide, particulate matter, nitrogen oxides, and volatile organic compounds. Three-way catalysts, a critical component in this endeavor, facilitate co-oxidation and NOx reduction during waste incineration and internal combustion engine processes. Emission monitoring plays a pivotal role in ensuring environmental compliance, with catalyst characterization and emission testing essential for catalyst optimization and performance assessment. Catalyst development encompasses various technologies, including ceramic monoliths and metallic open-pore foams as catalyst supports. Honeycomb catalysts, made of ceramic or metallic blocks with hexagonal, triangular, or square channels, offer benefits such as low pressure drop, simplified scalability, homogeneous flow, and low axial mixing.

Their low thermal expansion, thermal conduction, and high thermal shock resistance make them suitable for heat recovery applications. Gas turbines and industrial processes, including chemical manufacturing, cement production, and power generation, rely on catalytic converters to treat exhaust gases and minimize greenhouse gas emissions. Catalyst regeneration and deactivation are crucial aspects of emission control, with catalyst replacement a necessary part of the lifecycle. Selective catalytic reduction and catalytic oxidation processes employ precious metals to enhance catalyst performance and adhere to stringent emission standards. Catalyst modeling and simulation enable the prediction of catalyst behavior under various conditions, ensuring durability and optimal design.

Catalyst durability and air quality remain key concerns, with EPA regulations driving the market's evolution towards more efficient and effective emission control solutions.

The Honeycomb catalyst segment was valued at USD 655.10 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

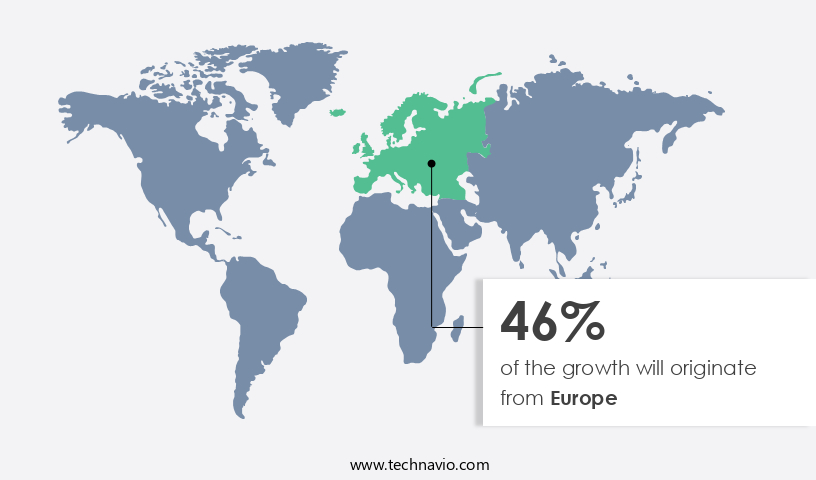

Europe is estimated to contribute 46% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is witnessing significant growth due to increasing regulations aimed at reducing hazardous emissions from industrial processes and power generation. In Europe, stringent emission standards, such as EURO 6 for light vehicles and EURO 5 and EURO 6 for heavy vehicles, have driven the demand for energy-efficient catalysts. The European Union (EU) has committed to reducing emissions by 40% by 2030 as part of its 2030 climate and energy framework and its contribution to the Paris Agreement. Sulfur dioxide, particulate matter, nitrogen oxides, and volatile organic compounds are among the pollutants targeted for reduction. Three-way catalysts and selective catalytic reduction systems are commonly used for co-oxidation and NOx reduction, respectively.

Waste incineration and cement production are significant stationary sources of emissions, requiring catalytic solutions for NOx and SO2 reduction. Catalyst development continues to focus on improving catalyst performance, durability, and regeneration to meet evolving emission standards. Gas turbines and internal combustion engines also utilize catalytic converters for emission control. Catalyst design, optimization, and modeling are crucial aspects of catalyst technology to enhance catalyst efficiency and reduce catalyst deactivation and poisoning. Catalytic oxidation and hydrocarbon oxidation catalysts play a vital role in air pollution control. The market trends reflect the ongoing efforts to minimize greenhouse gas emissions and improve air quality.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Stationary Emission Control Catalyst market drivers leading to the rise in the adoption of Industry?

- Stringent emission control regulations serve as the primary driver for market growth in this industry.

- The global market for stationary emission control catalysts is experiencing significant growth due to the increasing concern for air quality and the implementation of stricter emission standards. Industrial processes, particularly in sectors like cement production, contribute significantly to environmental pollution through the release of harmful gases. To mitigate these emissions, stationary emission control catalysts are utilized, which use precious metals to convert pollutants into less harmful substances. The demand for these catalysts is escalating as industries strive to comply with emission regulations and reduce their carbon footprint. Moreover, the need for catalyst optimization and regeneration is crucial to ensure their durability and prevent catalyst poisoning.

- In the context of gas turbines, the use of stationary emission control catalysts is essential to meet stringent emission norms and improve overall efficiency. Catalyst modeling and design play a vital role in enhancing the performance and longevity of these catalysts. The market's growth is further driven by the rising awareness of the importance of clean air and the increasing focus on sustainable industrial practices.

What are the Stationary Emission Control Catalyst market trends shaping the Industry?

- The growing importance of catalytic converters in reducing car emissions is a significant market trend. These devices play a crucial role in minimizing harmful exhaust gases, making them an essential component in modern automobiles.

- The market is witnessing significant growth due to the increasing need to minimize emissions from power generation and industrial processes. Advanced catalytic technologies, such as catalyst simulation, catalytic oxidation, and selective catalytic reduction (SCR), are being adopted to address environmental concerns and comply with EPA regulations. Catalytic converters play a crucial role in removing hydrocarbons, carbon monoxide, and nitrogen oxides produced by internal combustion engines. In the industrial sector, stationary sources, including power plants and manufacturing units, are implementing these catalytic systems to reduce their carbon footprint. Automotive manufacturers and industrial players are investing in research and development to create new and advanced catalytic systems, such as two-way and three-way catalytic converters, to enhance the overall performance and efficiency of emission control catalysts.

- Precious metals, such as platinum, palladium, and rhodium, are commonly used in these catalytic systems due to their high catalytic activity. By utilizing these advanced technologies, industries and automotive sectors can effectively address air pollution control and contribute to a cleaner environment.

How does Stationary Emission Control Catalyst market faces challenges face during its growth?

- The significant expense related to maintaining stationary emission control catalysts poses a major challenge to the industry's growth trajectory.

- Stationary emission control catalysts play a crucial role in reducing harmful pollutants such as sulfur dioxide, particulate matter, and volatile organic compounds from industrial processes and waste incineration. The global market for these catalysts is driven by stringent regulations mandating the reduction of NOx emissions. Three-way catalysts, in particular, are widely used for co-oxidation of NOx, CO, and hydrocarbons in the exhaust gases of internal combustion engines. However, the adoption of stationary emission control catalysts comes with challenges. The high initial investment required for the installation of these systems is a significant barrier. Moreover, the catalysts have a finite lifespan in the flue gas, necessitating periodic replacement.

- Contamination and plugging during operation can also impact the catalyst's performance. Despite these challenges, the market for stationary emission control catalysts is expected to grow due to the increasing focus on reducing greenhouse gas emissions and improving air quality. Catalyst development is ongoing to enhance catalyst lifespan, improve efficiency, and reduce the amount of ammonia slips. Emission monitoring technologies are also advancing to provide real-time data, enabling operators to optimize catalyst performance and minimize emissions.

Exclusive Customer Landscape

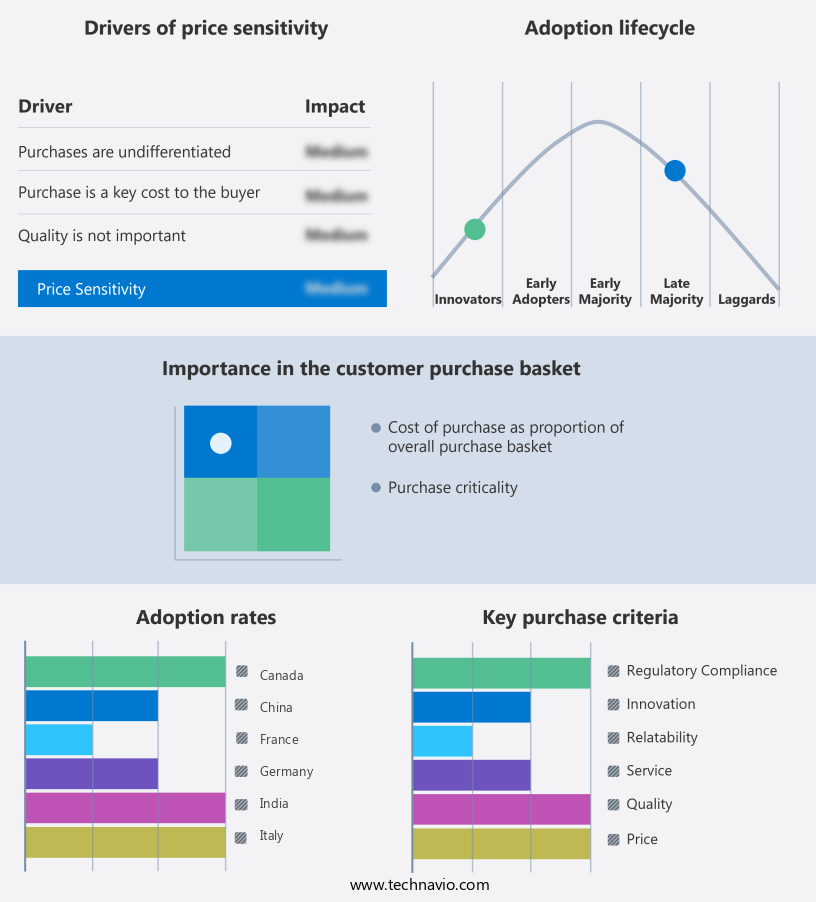

The stationary emission control catalyst market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the stationary emission control catalyst market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, stationary emission control catalyst market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AeriNOx Inc. - The company specializes in stationary emission control catalysts, designed to minimize pollutants in power generation processes. Our advanced catalysts effectively reduce harmful emissions, contributing to improved air quality and regulatory compliance. Through continuous research and development, we deliver innovative solutions that enhance efficiency and durability, ensuring optimal performance for our clients in the power industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AeriNOx Inc.

- BASF SE

- Bosal Nederland BV

- Cataler Corp.

- CDTi Advanced Materials Inc.

- Clariant International Ltd

- CORMETECH Inc.

- Corning Inc.

- DCL International Inc.

- Ecopoint Inc.

- Heraeus Holding GmbH

- Hitachi Zosen Corp.

- INTERKAT Catalyst GmbH

- Johnson Matthey Plc

- Nett Technologies Inc.

- Shell plc

- Solvay SA

- Tenneco Inc.

- Umicore SA

- Zeolyst International

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Stationary Emission Control Catalyst Market

- In February 2024, Haldor Topsoe, a leading Danish catalyst and process technology company, announced the launch of its new SCR (Selective Catalytic Reduction) catalyst, named Topsoe Select Catalyst 360. This innovative catalyst is designed to reduce nitrogen oxides (NOx) emissions by up to 95% in industrial applications, surpassing the current market standards (Topsoe Press Release, 2024).

- In July 2025, BASF Corporation and Siemens Energy AG entered into a strategic partnership to jointly develop and commercialize emission control technologies. The collaboration aims to integrate BASF's catalysts with Siemens Energy's power generation systems, providing comprehensive solutions to reduce emissions from power plants (BASF Press Release, 2025).

- In September 2024, Johnson Matthey, a global specialty chemicals company, completed the acquisition of the emission control catalyst business of U.S.-based Catalytic Solutions Inc. This acquisition significantly expanded Johnson Matthey's presence in the North American market and strengthened its position as a leading supplier of emission control technologies (Johnson Matthey Press Release, 2024).

- In March 2025, the European Union passed the Fit for 55 package, which includes new regulations to reduce greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels. The package includes stricter emission standards for various sectors, including industry, which is expected to drive demand for advanced emission control catalysts (European Commission Press Release, 2025).

Research Analyst Overview

The market is characterized by its continuous evolution and dynamic nature, driven by the ongoing unfolding of market activities and evolving patterns. Catalyst simulation plays a crucial role in optimizing catalyst performance for various applications, including power generation and air pollution control. EPA regulations have been instrumental in shaping the market, with stringent emission standards driving the demand for advanced catalytic technologies. Catalytic oxidation processes, such as hc oxidation and NOx reduction, are essential in controlling emissions from industrial processes and power generation. Precious metals, including platinum, palladium, and rhodium, are commonly used in catalysts for their catalytic properties.

However, the high cost of these metals and the need for their efficient utilization are ongoing challenges. Catalyst durability and regeneration are critical factors in maintaining optimal performance and minimizing catalyst replacement. Industrial processes, such as cement production, require robust catalysts to withstand high temperatures and corrosive environments. Catalyst design and optimization are ongoing areas of research to improve catalyst efficiency and reduce greenhouse gas emissions. Gas turbines and stationary sources are significant contributors to air pollution and are subject to strict emission regulations. Catalytic converters are used to treat exhaust gases, with emission monitoring and testing essential to ensure environmental compliance.

Catalyst characterization and modeling are essential tools in understanding catalyst behavior and optimizing catalyst design. Catalyst deactivation and poisoning are ongoing challenges in the market, with catalyst durability and regeneration crucial to maintaining optimal performance. The market is expected to continue evolving as new technologies and regulations emerge, with a focus on reducing emissions and improving efficiency.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Stationary Emission Control Catalyst Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.4% |

|

Market growth 2024-2028 |

USD 561.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.9 |

|

Key countries |

US, Germany, China, UK, Japan, France, India, Canada, Italy, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Stationary Emission Control Catalyst Market Research and Growth Report?

- CAGR of the Stationary Emission Control Catalyst industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, APAC, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the stationary emission control catalyst market growth of industry companies

We can help! Our analysts can customize this stationary emission control catalyst market research report to meet your requirements.

RIA -

RIA -