Enjoy complimentary customisation on priority with our Enterprise License!

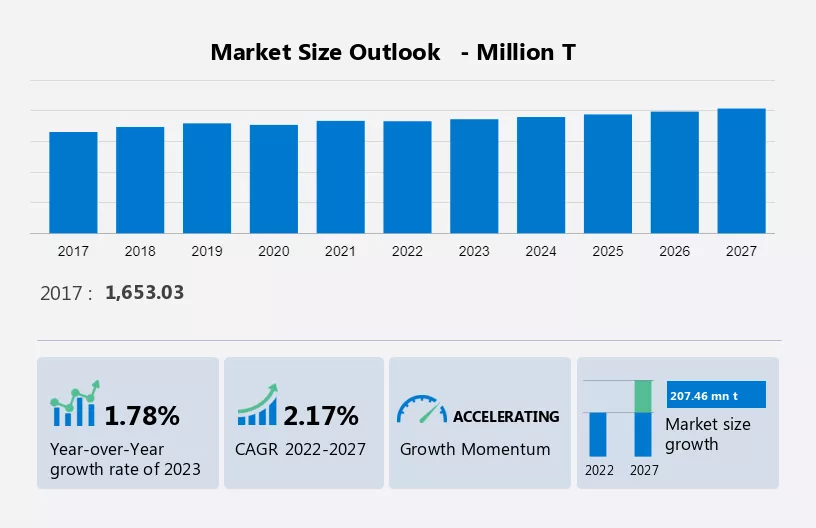

The steel market size is estimated to grow by 207.46 million tons at a CAGR of 2.17% between 2022 and 2027. Market growth relies on several factors, including an increase in the consumption of high-strength steel, its corrosion resistance, excellent mechanical properties, and the growing demand from the construction sector. These elements drive the expansion of the market, catering to diverse industries' needs for durable and high-performance materials. High-strength steel's ability to withstand harsh conditions and provide structural integrity makes it a preferred choice in construction and other sectors requiring robust materials. With the construction industry's steady growth and the increasing demand for high-strength, corrosion-resistant materials, the market for high-strength steel is expected to experience significant expansion in the coming years, reflecting its importance in various industrial applications.

It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report consists of historic market data from 2017 to 2021.

To learn more about this report, Download Report Sample

This report extensively covers market segmentation by end-user (construction, machinery, transportation, metal goods, and others), type (flat steel and long steel), and geography (APAC, Europe, North America, Middle East and Africa, and South America).

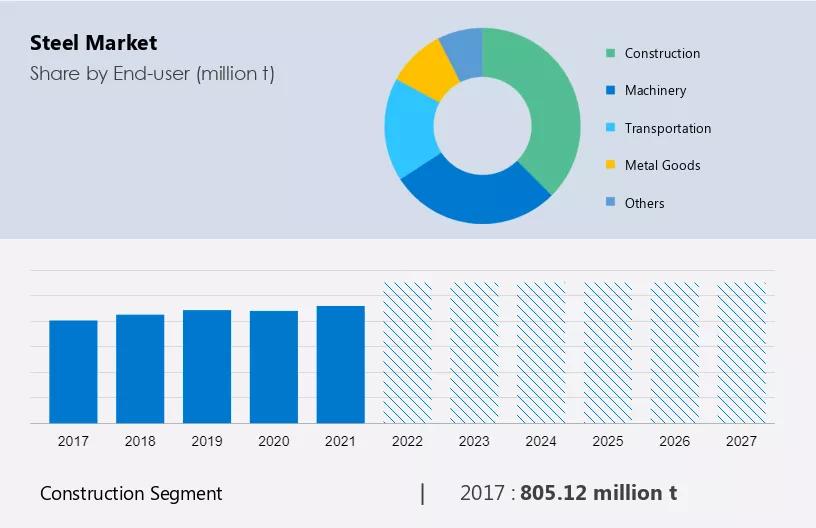

The market share growth by the construction segment will be significant during the forecast period. The market will experience significant growth in 2022, primarily driven by the construction industry. Pre-engineered metal buildings utilize steel for its strength and durability, making it an ideal choice for infrastructure development. Lightweight building materials, such as steel sheets and tubes, contribute to energy savings and reduce construction costs. The development of high-rise buildings, tech parks, roads, highways, and bridges across the world drives the growth of the global market.

Get a glance at the market contribution of various segments Request a PDF Sample

The construction segment was valued at 805.12 million t in 2017. Conventional casting processes and novel technologies continue to advance steel product innovation. Recycled metals play a crucial role in sustainability, while consumer safety and business risks influence market trends. Contractors rely on these for high-tolerance applications, including rail wheels, axles, and fish plates. Rapid urbanization and infrastructure investment necessitate steel demand for multifamily houses, single-family houses, upscale neighborhoods, metropolitan cities, office markets, and healthcare facilities. Raw materials like iron ore and coking coal fuel steelmaking, while carbon dioxide emissions and wastage remain key concerns. Collaborations between industry players and advancements in direct rolling practices further shape the market landscape. Hence, these factors are also expected to boost the global construction industry, which, in turn, will propel the growth of the market during the forecast period.

For more insights on the market share of various regions Request PDF Sample now!

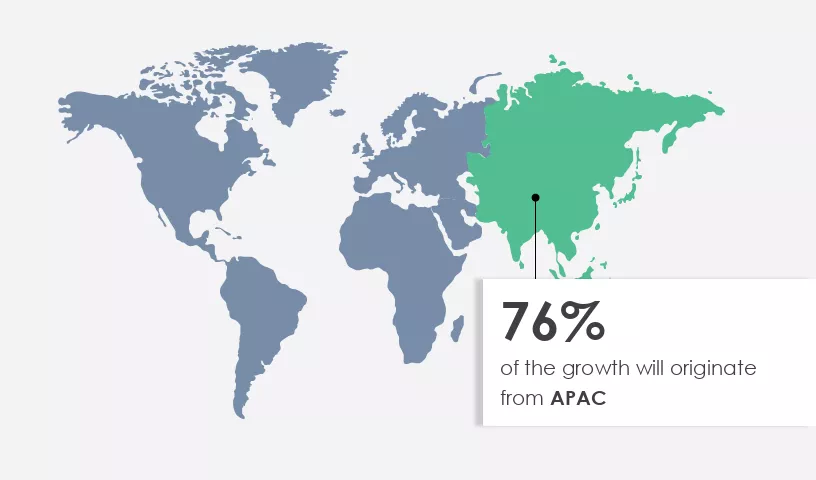

APAC is estimated to contribute 76% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in APAC is experiencing significant growth due to the increasing demand for conventional product forms such as automotive, transformers, beverage cans, housing materials, and industrial applications. This growth is driven by rapid industrialization and infrastructure development in countries like Indonesia, South Korea, and India. Government initiatives are also contributing to the expansion of the market. For instance, Indonesia's USD430 billion infrastructure investment plan includes over 60% spending on road, rail, and port projects. Steel is essential for various infrastructure projects, including underground transportation, gas, water, and overhead electrical wires, as well as cable protection. Its corrosion resistance and structural strength make it ideal for industrial structures, such as roofs and walls, panels, and large bridges. Additionally, steel's lightweight and ease of installation properties make it a popular choice for ready-made buildings, hassle-free construction of industrial and residential infrastructures, and HVAC control systems. The market is expected to continue growing, catering to various industries, including warehouses, and providing solutions for extreme weather conditions like snow, storms, and heavy rains.

In the dynamic market, pre-engineered metal buildings are a significant trend, utilizing lightweight building materials to promote energy savings. Conventional casting processes continue to dominate, but novel technologies, such as recycled metals, are gaining traction. Steel products, including tubes, are essential for various applications, from consumer safety in residential purposes like multifamily houses and single-family houses in upscale neighborhoods to non-residential purposes like offices in metropolitan cities and healthcare facilities. Steel demand is influenced by raw materials like iron ore and coking coal, steelmaking processes, and recycling. Collaborations between contractors and steel manufacturers are crucial for infrastructure investment in rapidly urbanizing areas. The steel industry faces business risks, including construction costs, carbon dioxide emissions, wastage, and contractual agreements. Cold-rolled steel undergoes recrystallization temperatures and surface finish processes to meet diverse market requirements. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The upsurge in consumption of high-strength steel is notably driving the market growth. The market for high-strength steel is experiencing growth due to its superior qualities, including high strength and ductility at both room and elevated temperatures. This steel is increasingly being used in various sectors, such as architectural, industrial, and consumer applications. Pre-engineered metal buildings and lightweight building materials are benefiting from high-strength steel's energy savings and affordability. In the construction industry, high-strain hardening ability and high tolerance are essential for contractors working with tubes, sheets, and other steel products.

Novel technologies and collaborations are driving innovation in conventional casting processes and recycled metals. Factors like rapid urbanization, infrastructure investment, and business risks are influencing the demand for high-strength steel in multifamily houses, single-family houses, upscale neighborhoods, metropolitan cities, office markets, healthcare, and more. Steelmaking relies on raw materials like iron ore and coking coal, and the demand for high-strength steel impacts steelmaking processes and carbon dioxide emissions. Cold-rolled steel and recrystallization temperatures are crucial factors in achieving the desired surface finish and properties. High-strength steel is also essential for various industries, including rail transportation, where it is used in rail wheels, axles, and fish plates. Direct rolling practices are employed to optimize the production of high-strength steel tubes. Hence, such factors will drive the growth of the global market during the forecast period.

The growing demand for steel and stainless steel scrap is an emerging trend in the market. The market is witnessing a shift towards the utilization of recycled metals, including scrap steel and stainless steel, due to their economic benefits and reduced environmental impact. Pre-engineered metal buildings and lightweight construction materials are key sectors driving the demand for steel products. Recycled metals contribute to energy savings and reduced carbon dioxide emissions, with an average of 2.9 metric tons of CO2 saved per metric ton of scrap steel. Steelmaking processes, such as conventional casting and novel technologies, use iron ore and steel or stainless-steel scrap as raw materials. Consumer safety, construction costs, and business risks are crucial considerations for contractors in the residential and non-residential sectors, including multifamily houses, single-family houses, upscale neighborhoods, metropolitan cities, and the office market.

Recycled metals play a significant role in infrastructure investment, particularly in the production of steel tubes, sheets, and other steel products, such as fish plates, rail wheels, axles, and cold-rolled steel. Collaborations between stakeholders, including steel producers, contractors, and governments, are essential for addressing the challenges of rapid urbanization and minimizing wastage. Steelmaking processes, including direct rolling practices and recrystallization temperatures, impact the surface finish and high tolerance requirements of steel products. The steel industry's focus on reducing carbon dioxide emissions, energy consumption, and water usage is crucial for its long-term sustainability. Thus, owing to the increasing demand for steel from various industries and the expansion of companies' production capacity, it is anticipated that the market in focus will grow during the forecast period.

Excess production capacity in the market are major challenge impeding the market. The market faces challenges due to excess production capacity, leading to low utilization ratios and oversupply. Factors such as low production costs, subsidies, and attractive financing contribute to unstructured capacity expansion. In the construction sector, pre-engineered metal buildings and lightweight building materials offer energy savings and consumer safety. Conventional casting processes and novel technologies are used to produce various steel products, including tubes and sheets, for residential and non-residential purposes.

Recycled metals reduce wastage and carbon dioxide emissions. Business risks and construction costs influence contractors' decisions. Collaboration and infrastructure investment are crucial in addressing rapid urbanization and meeting demand in metropolitan cities. Steelmaking relies on raw materials like iron ore and coking coal. Cold-rolled steel undergoes recrystallization at specific temperatures for high tolerance and surface finish. Steel tubes are used in rail wheels and axles, while fish plates and direct rolling practices ensure efficient production. Hence, technological advancements like these will likely hinder the global market in focus during the forecast period.

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Ansteel Group Corp. Ltd. - The company offers steel production, mining, ore dressing, sintering, ironmaking, steelmaking, rolling, coking and utility, and transportation products. The key offerings of the company include steel such as bridge steel, automotive steel, and others.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, robust, tentative, and weak.

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "million ton" for the period 2023 to 2027, as well as historical data from 2017 to 2022 for the following segments

In the dynamic market, various players engage in producing and trading of metals and building materials. The industry involves the production of consumentional and structural steel, as well as tubes and pipes. Lightweight materials, such as aluminum and carbon fiber, are also gaining popularity in the market. Engaging in marketing strategies is crucial for companies to gain a competitive edge. Marketing strategies include advertising, sales promotion, and personal selling. Companies may use various channels, such as social media, print media, and trade shows, to reach their target audience. The use of technology, such as CRM systems and automation tools, can help streamline marketing efforts and improve customer engagement.

Furthermore, the market is influenced by several factors, including economic conditions, technological advancements, and regulatory policies. Producers and consumers must navigate these factors to ensure the sustainability and growth of their businesses. The use of data and analytics is becoming increasingly important in the market. Companies can use data to gain insights into market trends, customer behavior, and production processes. This information can help inform marketing strategies and improve overall business performance. Innovation and sustainability are key drivers in the market. Companies that can offer eco-friendly and cost-effective solutions will be well-positioned to succeed in the industry. The use of renewable energy sources and recycled materials is becoming more common in steel production. In conclusion, the market is a complex and dynamic industry that requires effective marketing strategies to succeed. Companies must stay informed of market trends, customer needs, and regulatory policies to remain competitive. The use of technology, data, and sustainable practices can help companies differentiate themselves and thrive in the industry.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2022 |

|

Historic period |

2017 - 2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.17% |

|

Market growth 2023-2027 |

207.46 mn t |

|

Market structure |

USD Fragmented |

|

YoY growth 2022-2023(%) |

1.78 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 76% |

|

Key countries |

US, China, India, Japan, and Russia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Ansteel Group Corp. Ltd., ArcelorMittal SA, Baosteel Group Corp., Beijing Jianlong Heavy Industry Group Co. Ltd., Beijing Shougang Co. Ltd., China Baowu Steel Group Corp. Ltd., HBIS Group Co. Ltd., Hebei Jingye Group, Hyundai Steel Co., JFE Holdings Inc., JSW STEEL Ltd., Liuzhou Iron and Steel Co. Ltd., Nippon Steel Corp., NLMK Group, Nucor Corp., POSCO holdings Inc., Shagang Group Inc., Steel Authority of India Ltd., Tata Steel Ltd., and Benxi Steel Group Co. Ltd. |

|

Market dynamics |

Parent market analysis, market forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for market forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by End-user

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.