Enjoy complimentary customisation on priority with our Enterprise License!

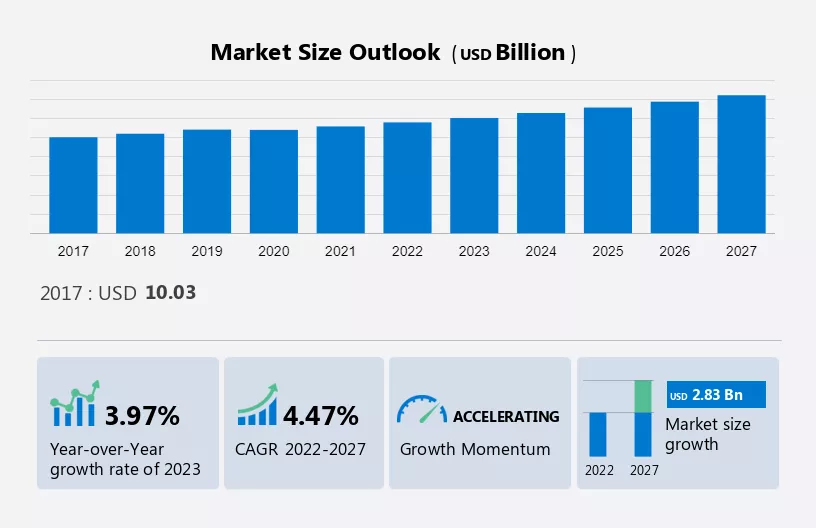

The Global Thin Film Material Market size is estimated to grow by USD 2.83 billion at a CAGR of 4.47% between 2022 and 2027. The growth of the market depends on several factors, including the increasing demand for consumer electronics, growing demand for architectural coatings, and growing demand for renewable energy. Thin film materials have been deposited in a very thin, uniform layer onto a substrate.

To learn more about this report, View Report Sample

consumer electronics is a key driving factor. The growing demand for consumer electronics is a major driver for the expansion of the thin film material industry. Thin film materials are utilized in various consumer electronic devices such as smartphones, laptops, and televisions to enhance their lightweight nature, compactness, and energy efficiency.

Thin film materials have diverse applications in consumer electronics, including display screens, touch screens, energy storage, and circuitry. They are used in the production of high-quality display screens like LCDs and OLEDs, providing excellent transparency and conductivity. Additionally, thin film materials play a crucial role in touch screen functionality, enabling accurate touch detection. They are also utilized in energy storage devices, such as lithium-ion batteries, offering improved energy density and cost-effectiveness. Furthermore, thin film materials like copper indium gallium selenide (CIGS) and silicon are employed in thin film solar cells, which can be integrated into consumer electronics devices to provide a renewable energy source. These factors contribute to the projected growth of the market in the forecast period.

The increased production efficiency is one of the major market trends. Increasing production efficiency is a prominent trend observed in the thin film material industry. To remain competitive and meet the growing demand for thin film materials, the industry is constantly seeking ways to enhance efficiency and reduce costs. One approach to improve production efficiency is through automation, such as the use of robotic systems. Automation not only enhances consistency but also reduces labor costs and increases material yield. Process optimization plays a crucial role in improving efficiency and reducing costs in thin film material production. Utilizing advanced deposition technologies like molecular beam epitaxy (MBE) and atomic layer deposition (ALD) can enhance scalability and efficiency. Material optimization is another key aspect of improving production efficiency. Developing new thin film materials with improved properties and lower costs, as well as optimizing existing materials, can contribute to higher efficiency and reduced production costs.

Additionally, equipment improvement is essential. Enhancing deposition systems and post-deposition processing equipment helps to achieve better production efficiency and cost reduction. By embracing these strategies, the thin film material industry drives innovation and growth, meeting the increasing demand for thin film materials. Continuously improving production efficiency and reducing costs ensure competitiveness in the global market throughout the forecast period.

Cost competitiveness is a major factor driving the market growth. The thin film material industry is actively focusing on increasing production efficiency to meet demand and stay competitive. Automation, process optimization, material enhancement, and equipment improvement are key approaches used. Automation improves consistency, reduces labor costs, and increases material yield. Process optimization involves utilizing advanced deposition technologies for scalability and efficiency. Material optimization entails developing new materials with improved properties and lower costs, as well as optimizing existing materials. Equipment improvement enhances production efficiency and reduces costs. These strategies drive innovation and growth, enabling the industry to meet the growing demand for thin film materials and maintain competitiveness in the global market.

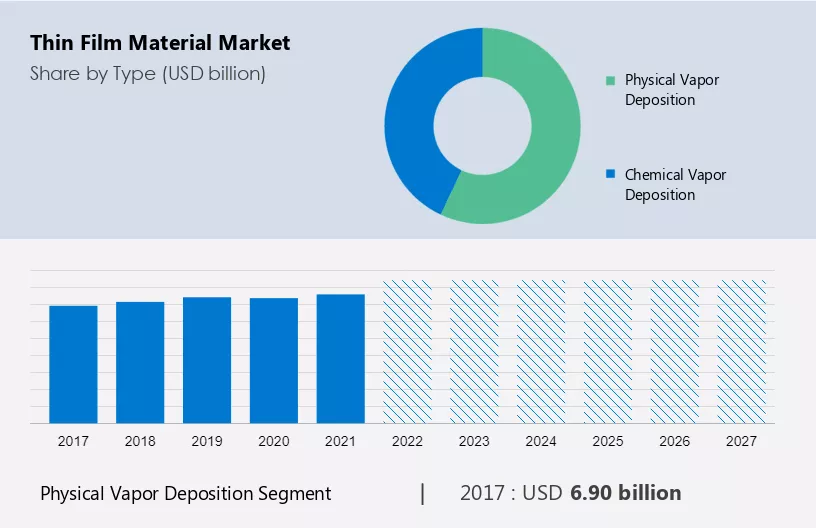

During the forecast period, the physical vapor deposition (PVD) segment is expected to experience substantial growth in market share. PVD is extensively utilized across multiple applications, including cutting tools, optics, decorative coatings, and electronic devices. Automation is enhancing PVD systems through the integration of robotics, advanced control systems, and process monitoring. Additionally, there is a rising trend in developing PVD systems capable of depositing thin films on large-area substrates.

Get a glance at the market contribution of various segments View Free PDF Sample

The physical vapor deposition segment was valued at USD 6.90 billion in 2017 and continued to grow until 2021. PVD is a thin film deposition process that uses physical means to transfer material from a source (typically a solid target) to a substrate, creating a thin, uniform film on the surface. The development of advanced coatings with unique properties such as high hardness, wear resistance, and low friction is a growing trend in PVD.

The application segment is categorized into the photovoltaic solar cell, mems, semiconductor, and electrical, and optical coating. Based on application, the photovoltaic solar cell holds the largest market share. A Photovoltaic (PV) solar cell is a device that converts sunlight into electrical energy through the use of a thin film of semiconducting material, typically silicon, deposited on a substrate. When sunlight hits the PV cell, it generates an electric field that separates positive and negative charges, resulting in an electric current. This current can power electrical devices or be stored in batteries for later use. Thin film photovoltaic (TFPV) solar cells are a type of PV cell that utilizes a thin film of photovoltaic material instead of bulky crystalline silicon. TFPV cells offer advantages such as lighter weight, increased flexibility, and cost-effectiveness. Various materials like cadmium telluride (CdTe), copper indium gallium selenide (CIGS), and amorphous silicon (a-Si) can be used to produce TFPV solar cells. The advancement of TFPV technology is an emerging trend in the solar energy industry, driven by the demand for more efficient, flexible, and affordable solar cells. Thin film photovoltaic technology has the potential to revolutionize the industry and serve as a clean and renewable energy source across various applications.

For more insights on the market share of various regions Download PDF Sample now!

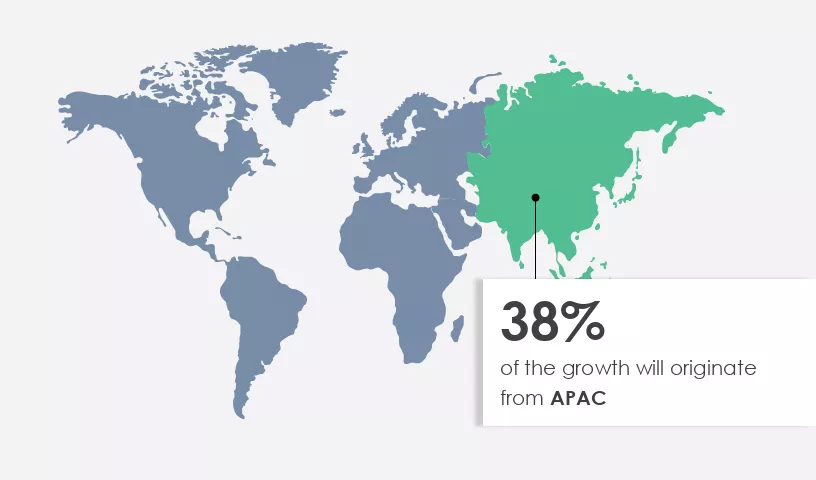

APAC is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The region plays a vital role in the thin film material industry, with increasing demand expected in the electronics, solar energy, and architectural coatings sectors. Factors such as the rising demand for electronic devices, renewable energy sources, and rapid industrialization in countries like China, Japan, and South Korea drive this growth. For instance, the APAC photovoltaic industry, led by China, exhibits a strong market for solar panels and cells, resulting in an increased demand for thin film photovoltaic cells.

The market growth analysis report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market research and growth report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market growth and forecasting report also includes detailed analyses of the competitive landscape of the market and information about 15 market Companies, including:

Qualitative and quantitative analysis of Companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize Companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize Companies as dominant, leading, strong, tentative, and weak.

The thin film material market is experiencing significant growth due to advancements in technology, leading to decreased weight and smaller size of products, while also enhancing their lifespan and introducing new features. These materials exhibit diverse electrical, optical, chemical, and mechanical properties, influenced by factors such as film density, morphology, and strength, along with their material composition. Driving factors include their application in photovoltaic solar cells, offering advanced characteristics compared to traditional silicon solar panels, contributing to the renewable energy sector and environmental sustainability by reducing greenhouse gases.

Companies like NICE Solar Energy GmbH are pioneering the development of CIGS thin film solar modules with high conversion efficiency rates, driving increased adoption in PV solar cell modules, 5G mobile communications, and semiconductors, addressing power consumption concerns and offering water resistance for prolonged use. Despite challenges like low efficiency and monocrystalline and polycrystalline structures, thin film materials find extensive use across various end-use industries, including the manufacturing of semiconductors, computer chips, and optical coatings, contributing to off-grid energy solutions and meeting the growing demand for electricity worldwide.

The market forecasting report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

|

Market Scope |

|

|

Market Report Coverage |

Details |

|

Page number |

155 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.47% |

|

Market growth 2023-2027 |

USD 2.83 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

3.97 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 38% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Ascent Solar Technologies Inc., AVANCIS GmbH, Cicor Management AG, Delta Optical Thin film AS, Hanergy Thin Film Power EME BV, Johanson Technology Inc., Kaneka Corp., Laird Performance Materials, Masdar, Moser Baer, Murata Manufacturing Co. Ltd., Samsung SDI Co. Ltd., Solar Frontier Europe GmbH, TDK Corp., Token Electronics Industry Co. Ltd., Trony Solar Holdings Co. Ltd., Viking Tech Corp., Vishay Intertechnology Inc., Wurth Elektronik GmbH and Co. KG, and Wuxi Suntech Power Co. Ltd. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by Application

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.