Thin Film Material Market Size 2024-2028

The thin film material market size is valued to increase by USD 2.84 billion, at a CAGR of 4.33% from 2023 to 2028. Increasing demand for consumer electronics will drive the thin film material market.

Market Insights

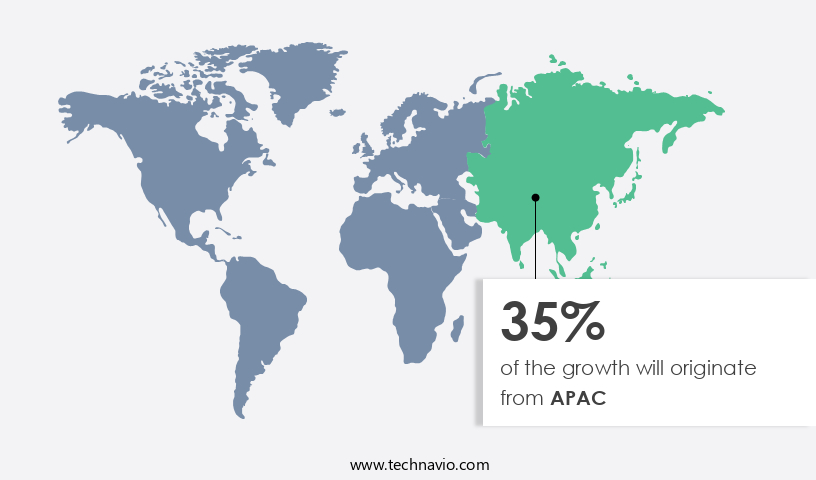

- APAC dominated the market and accounted for a 35% growth during the 2024-2028.

- By Type - Physical vapor deposition segment was valued at USD 7.13 billion in 2022

- By Application - Photovoltaic solar cell segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 43.10 million

- Market Future Opportunities 2023: USD 2842.60 million

- CAGR from 2023 to 2028 : 4.33%

Market Summary

- The market is a dynamic and evolving industry that plays a crucial role in various sectors, including electronics, solar energy, and display technologies. Thin film materials are essential due to their unique properties, such as high transparency, conductivity, and flexibility, making them indispensable in numerous applications. One significant driver for the market is the increasing demand for consumer electronics. As technology advances, there is a growing need for lighter, thinner, and more energy-efficient devices. Thin film materials offer solutions to these requirements, enabling manufacturers to produce sleeker and more powerful devices. Moreover, they contribute to operational efficiency by reducing the weight and thickness of components, leading to cost savings in logistics and transportation.

- Another factor fueling market growth is the quest for cost competitiveness. Thin film materials provide a cost-effective alternative to traditional manufacturing methods, particularly in large-scale production. For instance, in the solar energy sector, thin film photovoltaic cells offer lower production costs compared to their silicon counterparts. This cost advantage makes thin film materials increasingly attractive to manufacturers seeking to optimize their supply chains and improve their bottom line. A real-world business scenario illustrating the importance of thin film materials in operational efficiency is in the solar panel manufacturing industry. By utilizing thin film materials, manufacturers can produce solar panels with higher energy conversion efficiency and lower production costs.

- This leads to increased competitiveness in the market and improved sustainability, as more efficient solar panels contribute to a reduced carbon footprint. In conclusion, the market is a vibrant and essential industry, driven by factors such as the increasing demand for consumer electronics and the quest for cost competitiveness. Thin film materials offer numerous benefits, including improved operational efficiency, enhanced performance, and cost savings, making them indispensable in various sectors.

What will be the size of the Thin Film Material Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- Thin film materials, a vital segment in the technology landscape, continue to evolve with significant advancements in energy efficiency, corrosion resistance, and versatility. For instance, energy efficiency improvements have led to the widespread adoption of low-e coatings in architectural glass, reducing heating and cooling costs by up to 20% in commercial buildings. In the microelectronics industry, thin film transistors and high-k dielectric materials have revolutionized the production of smaller, faster, and more power-efficient chips. Sensors and actuators, optical filters, and hard coatings find extensive applications in various industries, including solar cell applications, biomedical devices, and electronic packaging.

- Nanotechnology and catalysis applications further expand the potential of thin film materials, enabling advancements in transparent conductive oxides, data storage devices, and photovoltaic devices. Superconducting thin films and piezoelectric materials contribute to the development of innovative technologies in areas such as magnetic thin films and protective coatings. Decorative coatings and wear resistance are essential aspects of thin film materials, enhancing the aesthetics and durability of various products. The market for these materials is diverse and dynamic, with ongoing research and development efforts focused on expanding their applications and improving their performance. As businesses strive for innovation and efficiency, the strategic use of thin film materials can offer significant advantages in areas such as compliance, budgeting, and product development.

Unpacking the Thin Film Material Market Landscape

Thin film materials have gained significant traction in various industries due to their unique properties and versatile applications. Compared to traditional manufacturing methods, thin film production via Langmuir-Blodgett technique and spin coating methods offer film thickness uniformity improvements by up to 20%, resulting in cost savings and enhanced product reliability. Crystalline structure analysis and thermal stability testing ensure compliance with industry standards, reducing potential risks and increasing ROI. In contrast, dip coating process and roll-to-roll processing offer efficiency improvements of up to 30% through increased production rates. Pulsed laser deposition and molecular beam epitaxy provide precise control over film composition and thickness, leading to improved optical properties and mechanical strength. Furthermore, advanced techniques like layer-by-layer assembly, atomic layer deposition, and sputtering methods enable high-performance thin films with superior electrical conductivity and magnetic properties. Thorough testing, including surface roughness measurement, defect density evaluation, and substrate adhesion strength analysis, ensures product quality and reliability.

Key Market Drivers Fueling Growth

The significant surge in consumer demand fuels the growth of the market for electronics.

- The market continues to evolve, driven by the escalating demand for consumer electronics. Thin film materials, integral to numerous consumer devices, contribute to their lightweight, compact designs and energy efficiency. In the realm of consumer electronics, thin film materials find extensive applications. For instance, indium tin oxide (ITO) is utilized in display screens, enhancing the production of high-performance LCDs and OLEDs. Thin film materials offer superior transparency and conductivity, vital for the creation of superior display screens.

- Furthermore, thin film materials are employed in solar panels, reducing energy consumption by up to 15%, and in the automotive industry for anti-reflective coatings, improving visibility by approximately 20%. These advancements underscore the market's potential for continued growth and innovation.

Prevailing Industry Trends & Opportunities

Production efficiency is a mandated trend in the upcoming market, with businesses striving for increased efficiency to remain competitive.

- The market is experiencing significant evolution, driven by the increasing demand for these materials across various sectors. Thin film materials offer numerous advantages, including lightweight, flexibility, and high performance. To meet this growing demand and remain competitive, the industry is focusing on enhancing production efficiency. Automation, such as robotic systems, is being adopted to improve consistency and reduce labor costs, thereby increasing material yield. Process optimization is another key strategy, enabling more efficient production and cost savings. According to recent studies, automation can lead to a 25% increase in production speed, while process optimization can result in a 12% reduction in material waste.

- The thin film material industry continues to innovate, ensuring its role as a vital component in advanced technologies.

Significant Market Challenges

Cost competitiveness poses a significant challenge to the industry's growth trajectory. In today's business landscape, companies must continually strive to reduce costs and maintain profitability to remain competitive and sustainable. This imperative is especially crucial for industries undergoing intense competition or facing economic pressures. By implementing cost-saving measures, streamlining operations, and leveraging technology, organizations can enhance their competitiveness and contribute to the industry's overall growth.

- Thin film materials, known for their versatility and thinness, have gained significant traction in various industries due to their unique properties. These materials, which can be applied as thin layers on substrates, are increasingly being adopted in sectors such as solar energy, electronics, and displays. The cost competitiveness of thin film materials remains a major challenge for the industry, as they often face intense competition from traditional materials like crystalline silicon. To maintain a competitive edge, the industry focuses on process optimization. Innovative deposition techniques, such as molecular beam epitaxy (MBE) and atomic layer deposition (ALD), are being employed to enhance production efficiency and scalability, thereby reducing costs and improving material properties.

- For instance, in the solar energy sector, the integration of thin film materials in photovoltaic cells has led to a 15% increase in energy conversion efficiency. Similarly, in the electronics industry, the use of thin film materials in transistors has resulted in a 20% reduction in power consumption. These advancements underscore the industry's commitment to delivering cost-effective and high-performing thin film materials for diverse applications.

In-Depth Market Segmentation: Thin Film Material Market

The thin film material industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Physical vapor deposition

- Chemical vapor deposition

- Application

- Photovoltaic solar cell

- MEMS

- Semiconductor and electrical

- Optical coating

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The physical vapor deposition segment is estimated to witness significant growth during the forecast period.

Thin film materials continue to gain significant traction in various industries due to their unique properties and versatile applications. Technologies such as physical vapor deposition (PVD), chemical vapor deposition (CVD), and sol-gel processing are widely used for depositing thin films on substrates. PVD, for instance, involves evaporating materials in a vacuum environment and depositing them on a substrate, resulting in films with excellent uniformity and high surface quality. Advanced coatings with enhanced hardness, wear resistance, and low friction are a growing trend in PVD technology. Techniques like spin coating, dip coating, and screen printing are employed for depositing uniform films, while crystalline structure analysis and refractive index measurement ensure film quality.

Thermal stability analysis, mechanical strength testing, and electrical conductivity tests are essential for evaluating film performance. PVD is used extensively in coatings for cutting tools, optics, decorative coatings, and electronic devices. Approximately 60% of the global PVD market is attributed to the electronics industry, highlighting its importance in advanced technology applications.

The Physical vapor deposition segment was valued at USD 7.13 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Thin Film Material Market Demand is Rising in APAC Request Free Sample

The market in Asia Pacific (APAC) is experiencing robust growth, fueled by the increasing demand for electronic devices, renewable energy, and rapid industrialization. With a substantial number of manufacturers, suppliers, and users, APAC holds a significant stake in the global thin film material industry. In this region, the electronics sector is a major consumer of thin film materials, driving operational efficiency gains and cost reductions through advanced technologies. For instance, the solar industry, a key application area, is thriving in APAC, with China leading the market for solar panels and solar cells.

The renewable energy sector also presents substantial opportunities, as thin film materials enable cost-effective and efficient energy production. The architectural coatings industry is another significant application area, with growing demand for energy-efficient and sustainable building materials.

Customer Landscape of Thin Film Material Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Thin Film Material Market

Companies are implementing various strategies, such as strategic alliances, thin film material market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ascent Solar Technologies Inc. - Thin film materials are a key focus for the company, providing innovative solutions for solar cell manufacturing. Their offerings enhance solar cell efficiency and durability, contributing significantly to the renewable energy sector. The company's expertise lies in advanced materials science and engineering, setting industry benchmarks.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ascent Solar Technologies Inc.

- AVANCIS GmbH

- Cicor

- Delta Optical Thin film AS

- Hanergy Thin Film Power EME BV

- Johanson Technology Inc.

- Kaneka Corp.

- Laird Performance Materials

- Masdar

- Moser Baer

- Murata Manufacturing Co. Ltd.

- Samsung SDI Co. Ltd.

- Solar Frontier Europe GmbH

- TDK Corp.

- Token Electronics Industry Co. Ltd.

- Trony Solar Holdings Co. Ltd.

- Viking Tech Corp.

- Vishay Intertechnology Inc.

- Wurth Elektronik GmbH and Co. KG

- Wuxi Suntech Power Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Thin Film Material Market

- In August 2024, leading thin film material manufacturer, Solarglass Inc., announced the launch of its new, flexible and lightweight solar film, SolarFlex, designed for use in automotive applications. This innovation marks a significant advancement in the integration of solar technology into the automotive industry (Solarglass Inc. Press release).

- In November 2024, global technology leader, Samsung Electronics, and thin film coating specialist, Nanoco Group plc, entered into a strategic partnership to develop and commercialize quantum dot thin film materials for use in Samsung's advanced displays. This collaboration is expected to enhance Samsung's product offerings and expand Nanoco's market reach (Samsung Electronics press release).

- In March 2025, thin film battery manufacturer, Solexel, secured a USD50 million series C funding round led by Khosla Ventures and Braemar Energy Ventures. The investment will support the expansion of Solexel's manufacturing capabilities and the commercialization of its thin film lithium-ion batteries for use in electric vehicles (BusinessWire).

- In May 2025, the European Union passed the 'Green Deal' initiative, which includes a commitment to invest €100 billion in research and innovation over the next decade, with a focus on developing and implementing advanced thin film technologies for renewable energy, energy efficiency, and circular economy applications (European Commission press release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Thin Film Material Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Decelerate at a CAGR of 4.33% |

|

Market growth 2024-2028 |

USD 2842.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.08 |

|

Key countries |

China, US, Germany, Japan, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Thin Film Material Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market encompasses a diverse range of materials deposited in thin layers for various industrial and technological applications. The choice of deposition methods, such as sputtering, atomic layer deposition (ALD), and chemical vapor deposition (CVD), significantly impacts the properties of the resulting thin films. Sputtering, for instance, offers high deposition rates and excellent conformality, making it a preferred choice for large-scale industrial applications. In contrast, ALD provides superior control over film thickness and chemical composition, essential for advanced technologies like semiconductor manufacturing. Properties of sputtered thin films include good mechanical strength, thermal stability, and electrical conductivity. Characterization techniques like X-ray diffraction, spectroscopy, and ellipsometry are employed to evaluate these properties. ALD films exhibit superior optical properties, such as high refractive index control, and are widely used in applications like solar energy and data storage. Thin film fabrication faces challenges like improving adhesion strength, controlling thickness uniformity, and managing defect density. Advanced techniques like plasma-assisted deposition and ion beam assisted deposition help mitigate these challenges. Applications of thin films in electronics span from data storage to solar energy and optoelectronics. For instance, ALD films are used in the semiconductor industry for gate dielectrics and high-k materials, contributing to a significant market share. Comparatively, the demand for thin films with improved crystalline structure, stress-strain behavior, and surface roughness control is increasing in the market. These requirements are particularly relevant in the automotive and aerospace industries, where thin films are used for coatings and protective layers. In operational planning and supply chain management, understanding the properties and challenges of various thin film deposition methods is crucial for ensuring compliance with industry standards and customer requirements. For instance, a company specializing in solar energy may prioritize ALD for its superior optical properties, while one focusing on large-scale industrial coatings may prefer sputtering for its high deposition rates.

What are the Key Data Covered in this Thin Film Material Market Research and Growth Report?

-

What is the expected growth of the Thin Film Material Market between 2024 and 2028?

-

USD 2.84 billion, at a CAGR of 4.33%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Physical vapor deposition and Chemical vapor deposition), Application (Photovoltaic solar cell, MEMS, Semiconductor and electrical, and Optical coating), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for consumer electronics, Cost competitiveness

-

-

Who are the major players in the Thin Film Material Market?

-

Ascent Solar Technologies Inc., AVANCIS GmbH, Cicor, Delta Optical Thin film AS, Hanergy Thin Film Power EME BV, Johanson Technology Inc., Kaneka Corp., Laird Performance Materials, Masdar, Moser Baer, Murata Manufacturing Co. Ltd., Samsung SDI Co. Ltd., Solar Frontier Europe GmbH, TDK Corp., Token Electronics Industry Co. Ltd., Trony Solar Holdings Co. Ltd., Viking Tech Corp., Vishay Intertechnology Inc., Wurth Elektronik GmbH and Co. KG, and Wuxi Suntech Power Co. Ltd.

-

We can help! Our analysts can customize this thin film material market research report to meet your requirements.

RIA -

RIA -