Type 2 Diabetes Market Size 2026-2030

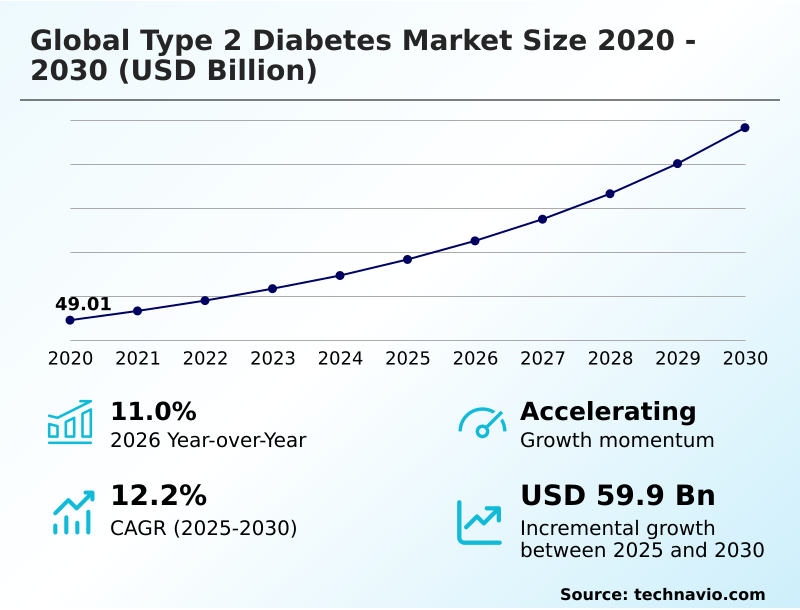

The type 2 diabetes market size is valued to increase by USD 59.90 billion, at a CAGR of 12.2% from 2025 to 2030. Integration of advanced medical devices and automated glycemic control will drive the type 2 diabetes market.

Major Market Trends & Insights

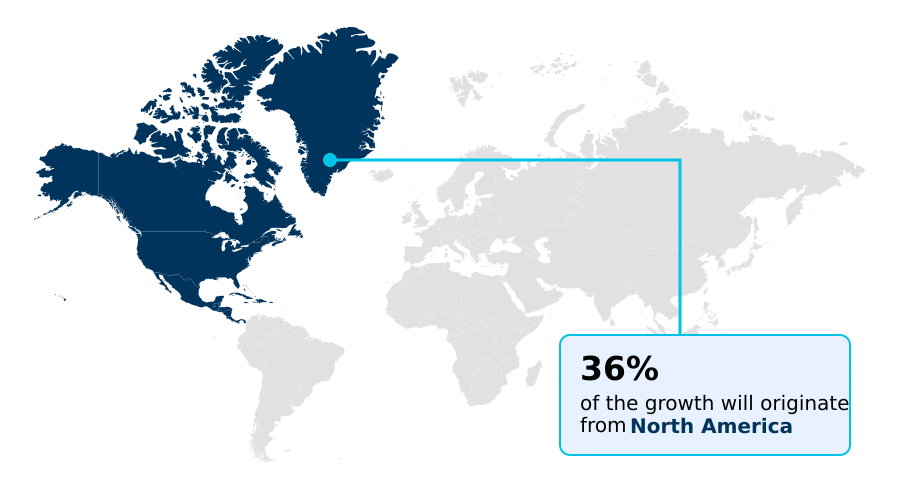

- North America dominated the market and accounted for a 35.9% growth during the forecast period.

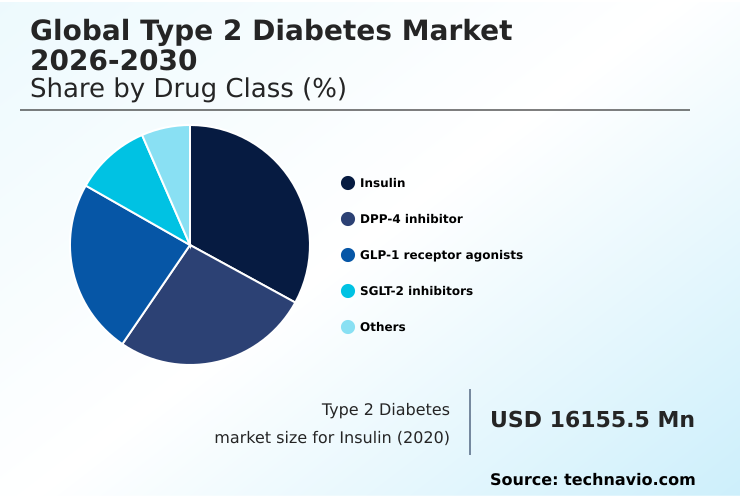

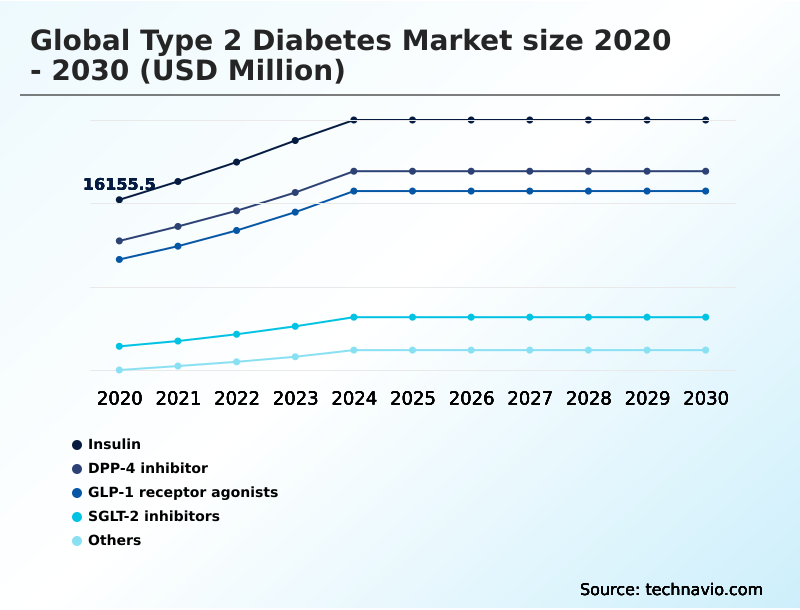

- By Drug Class - Insulin segment was valued at USD 22.22 billion in 2024

- By Distribution Channel - Retail pharmacies segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 87.50 billion

- Market Future Opportunities: USD 59.90 billion

- CAGR from 2025 to 2030 : 12.2%

Market Summary

- The type 2 diabetes market is defined by a persistent need for more effective therapies and management tools to address its growing prevalence. This complex metabolic disorder requires a multi-faceted approach, combining lifestyle adjustments with pharmacological intervention. Key market drivers include the rising rates of obesity and sedentary lifestyles, which are increasing the patient population globally.

- In response, the industry is innovating rapidly, with a significant trend toward personalized medicine and the integration of digital health technologies. For instance, healthcare systems are now leveraging predictive analytics to identify high-risk patients, allowing for targeted interventions that optimize resource allocation and prevent costly complications. This proactive management strategy exemplifies the shift from reactive treatment to preventive care.

- However, the high cost of novel therapies and challenges in patient adherence continue to shape the competitive landscape. As the market evolves, the focus remains on developing solutions that improve glycemic control while addressing related cardiovascular and renal comorbidities, ultimately enhancing the long-term quality of life for patients.

What will be the Size of the Type 2 Diabetes Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Type 2 Diabetes Market Segmented?

The type 2 diabetes industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Drug class

- Insulin

- DPP-4 inhibitor

- GLP-1 receptor agonists

- SGLT-2 inhibitors

- Others

- Distribution channel

- Retail pharmacies

- Hospital pharmacies

- Online pharmacies

- Delivery mode

- Oral

- Injectable

- Continuous glucose monitoring (CGM)

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Asia

- Rest of World (ROW)

- North America

By Drug Class Insights

The insulin segment is estimated to witness significant growth during the forecast period.

The insulin segment remains a foundational component of pharmacological intervention, evolving with the introduction of patient-centric alternatives like biosimilar insulin aspart. Emphasis is on improving subcutaneous infusion methods and developing advanced basal insulin formulation options to enhance patient adherence solutions.

While traditional formulations are prevalent, the market is shifting toward integrated systems that combine insulin delivery with continuous glucose monitoring.

This technological fusion is central to value-based care models, as automated systems can reduce hypoglycemic events by up to 18%, significantly improving safety and long-term outcomes for individuals requiring intensive glycemic management.

The Insulin segment was valued at USD 22.22 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Type 2 Diabetes Market Demand is Rising in North America Get Free Sample

The global landscape for the type 2 diabetes market is characterized by distinct regional dynamics in metabolic disorder management.

North America, driven by high adoption of digital health platforms and preventive care models, commands the largest share, accounting for over 35% of incremental growth.

The region's advanced healthcare infrastructure supports the widespread use of sophisticated therapies like oral semaglutide formulation and drugs targeting the glucose-dependent insulinotropic polypeptide pathway.

In contrast, Asia is the fastest-growing market, expanding at a rate of 13.0% due to rising disease prevalence and improving healthcare access.

This growth is fueled by the increased use of established drug classes like dipeptidyl peptidase-4 and sodium-glucose cotransporter-2 inhibitors, which offer effective and increasingly affordable treatment options.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic landscape of the global type 2 diabetes market 2026-2030 is increasingly focused on personalizing treatment pathways beyond simple glycemic management. A key consideration is understanding the impact of glp-1 agonists on weight management, a significant comorbidity for many patients. Concurrently, the proven benefits of sglt-2 inhibitors for heart failure are reshaping clinical guidelines, prioritizing agents with cardiovascular advantages.

- This has intensified the search for effective oral alternatives to injectable insulin therapies, aiming to improve convenience and long-term compliance. The challenge of managing glycemic variability with continuous glucose monitoring is being addressed through advanced analytics, which helps in reducing therapeutic inertia in diabetes care.

- From a strategic perspective, the role of digital health in improving patient adherence has become a critical performance metric for providers. Furthermore, the cost-effectiveness of automated insulin delivery systems is scrutinized twice as heavily in procurement decisions compared to five years ago.

- This shift also highlights challenges in cold-chain logistics for biologics and elevates the importance of tracking cardiovascular outcomes of new diabetes medications and successfully integrating cgm data into clinical practice to validate therapeutic value.

What are the key market drivers leading to the rise in the adoption of Type 2 Diabetes Industry?

- The integration of advanced medical devices and automated glycemic control systems is a key driver accelerating market expansion.

- Market growth is propelled by technological advancements and a deeper clinical understanding of chronic disease management.

- The integration of continuous glucose monitoring with automated glycemic control is a primary driver, with closed-loop systems demonstrating an ability to increase users' time in the optimal glucose range by over 20%.

- This data-driven approach, supported by real-world evidence, improves outcomes and aligns with value-based care. Another key driver is the expansion of therapies to provide cardiorenal benefits beyond glycemic control.

- Medications offering proven cardiovascular risk reduction are now prioritized in over 40% of new treatment plans for high-risk patients, reflecting a shift toward holistic health management and preventive care models.

What are the market trends shaping the Type 2 Diabetes Industry?

- The integration of artificial intelligence and predictive analytics is a key trend in chronic disease management. This evolution is reshaping patient care by enabling more proactive and personalized therapeutic strategies.

- Key trends are reshaping the market, driven by a convergence of technology and patient-centric care. The adoption of non-invasive formulations is accelerating, with advancements in oral delivery of complex biologics like glucagon-like peptide-1. These innovations, coupled with smart insulin pens, are improving convenience and driving better hemoglobin a1c reduction.

- The move toward decentralized healthcare, supported by telehealth consultations and specialized cold-chain logistics, ensures wider access to temperature-sensitive medications. This logistical enhancement is critical, as it supports a 40% increase in home delivery for injectable therapies. Furthermore, digital platforms leveraging AI have shown the potential to improve long-term adherence by up to 25% by providing personalized feedback and support.

What challenges does the Type 2 Diabetes Industry face during its growth?

- The escalating economic burden of advanced therapies and associated reimbursement hurdles present a key challenge to market growth.

- Significant challenges constrain market potential, primarily centered on economics, adherence, and manufacturing. High costs associated with novel pharmacological therapies, such as incretin mimetics and dual agonist therapies, create substantial reimbursement hurdles.

- This financial pressure is compounded by issues of therapeutic inertia, where studies show that nearly 50% of patients with suboptimal glycemic control do not receive timely treatment adjustments, necessitating better clinical decision support.

- Furthermore, ensuring supply chain resilience is a critical challenge, as manufacturing constraints for high-demand biologics have led to shortages affecting medication access for an estimated 1 in 5 patients in some regions, undermining therapeutic inertia mitigation efforts.

Exclusive Technavio Analysis on Customer Landscape

The type 2 diabetes market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the type 2 diabetes market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Type 2 Diabetes Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, type 2 diabetes market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Advanced medical devices and diagnostic products form the core of integrated solutions for chronic disease management and glucose monitoring.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AstraZeneca Plc

- Bayer AG

- Biocon Ltd.

- Boehringer Ingelheim GmbH

- Dexcom Inc.

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- Insulet Corp.

- Lupin Ltd.

- Medtronic Plc

- Merck and Co. Inc.

- MicroPort Scientific Corp.

- Novartis AG

- Pfizer Inc.

- Sanofi SA

- Sun Pharmaceutical Industries

- Takeda Pharmaceutical Ltd.

- Tandem Diabetes Care Inc.

- Terumo Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Type 2 diabetes market

- In October, 2024, Novo Nordisk secured a significant approval from the Food and Drug Administration of the United States for Rybelsus, an oral semaglutide formulation, to reduce the risk of major adverse cardiovascular events in adults with Type 2 diabetes and established cardiovascular disease.

- In February, 2025, Tandem Diabetes Care received clearance from the Food and Drug Administration of the United States for the use of its Control-IQ technology in adults living with Type 2 diabetes, expanding automated insulin delivery to a broader population.

- In March, 2025, Dexcom launched an upgraded digital interface that utilizes generative artificial intelligence to provide personalized lifestyle recommendations based on glucose fluctuations and historical data trends, enhancing its continuous glucose monitoring platform.

- In May, 2025, Amazon Pharmacy announced a major expansion of its specialized cold-chain logistics network, enabling same-day delivery of insulin and other refrigerated metabolic medications across more than twenty major metropolitan areas.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Type 2 Diabetes Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.2% |

| Market growth 2026-2030 | USD 59896.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 11.0% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, Russia, China, India, Japan, South Korea, Turkey, Indonesia, Brazil, Saudi Arabia, South Africa, Israel, Argentina, Egypt, UAE and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global type 2 diabetes market 2026-2030 is undergoing a fundamental transformation, shifting from a singular focus on glycemic control to holistic metabolic health management. This evolution prioritizes cardiovascular risk reduction and renal protection, compelling a strategic pivot in R&D budgeting toward dual agonist therapies and combination treatments.

- The integration of advanced technologies like continuous glucose monitoring and closed-loop systems for automated insulin delivery is becoming standard. Innovations in non-invasive formulations, including oral semaglutide formulation and other patient-centric alternatives, are addressing long-standing barriers to adherence. The development of next-generation pharmacological therapies, such as those targeting glucagon-like peptide-1 and sodium-glucose cotransporter-2, alongside biosimilar insulin aspart, is intensifying competition.

- However, therapeutic inertia remains a significant challenge, with studies showing that nearly 50% of adults with insufficient hemoglobin A1C reduction do not receive timely therapy adjustments. Success now hinges on creating integrated ecosystems that combine smart insulin pens and subcutaneous infusion technologies with data-driven insights to enable precise, automated glycemic control.

What are the Key Data Covered in this Type 2 Diabetes Market Research and Growth Report?

-

What is the expected growth of the Type 2 Diabetes Market between 2026 and 2030?

-

USD 59.90 billion, at a CAGR of 12.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Drug Class (Insulin, DPP-4 inhibitor, GLP-1 receptor agonists, SGLT-2 inhibitors, and Others), Distribution Channel (Retail pharmacies, Hospital pharmacies, and Online pharmacies), Delivery Mode (Oral, Injectable, and Continuous glucose monitoring (CGM)) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Integration of advanced medical devices and automated glycemic control, Escalating economic burden and reimbursement hurdles

-

-

Who are the major players in the Type 2 Diabetes Market?

-

Abbott Laboratories, AstraZeneca Plc, Bayer AG, Biocon Ltd., Boehringer Ingelheim GmbH, Dexcom Inc., Eli Lilly and Co., F. Hoffmann La Roche Ltd., Insulet Corp., Lupin Ltd., Medtronic Plc, Merck and Co. Inc., MicroPort Scientific Corp., Novartis AG, Pfizer Inc., Sanofi SA, Sun Pharmaceutical Industries, Takeda Pharmaceutical Ltd., Tandem Diabetes Care Inc. and Terumo Corp.

-

Market Research Insights

- Market dynamics are increasingly shaped by a move toward holistic metabolic disorder management, where treatment efficacy is measured by comprehensive health outcomes rather than just glycemic control. The adoption of value-based care models prioritizes therapies that deliver long-term clinical and economic advantages.

- For example, integrated systems combining continuous glucose monitoring with automated insulin delivery have demonstrated a 25% reduction in hospital readmissions for acute glycemic events. Concurrently, digital health platforms are enhancing patient adherence solutions, with some platforms boosting medication compliance by over 30%.

- This focus on real-world evidence and patient engagement is compelling providers to invest in technologies that facilitate decentralized healthcare and improve supply chain resilience for temperature-sensitive biologics.

We can help! Our analysts can customize this type 2 diabetes market research report to meet your requirements.

RIA -

RIA -