Enjoy complimentary customisation on priority with our Enterprise License!

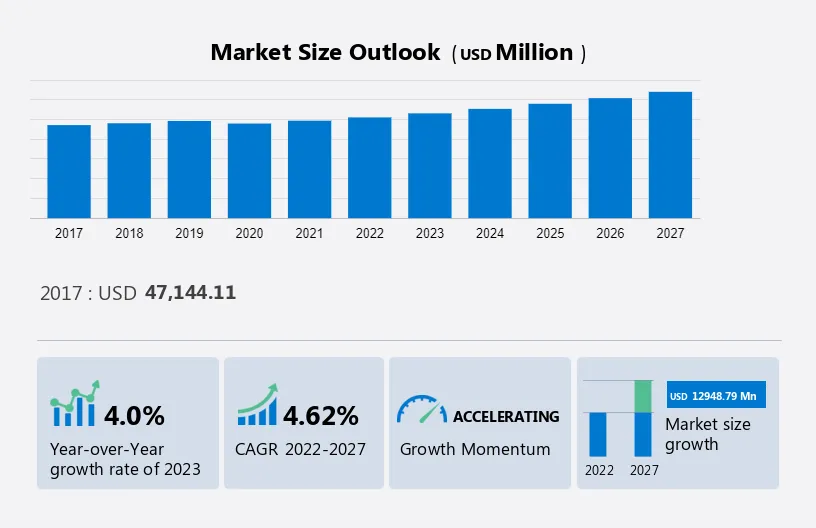

The Valves Market size is estimated to grow at a CAGR of 4.62% between 2022 and 2027 and the size of the market is forecast to increase by USD 12,948.79 million. The growth of the market depends on several factors, such as industrialization and infrastructure development, increased demand for oil and gas, and environmental regulations.

This report extensively covers market segmentation by end-user (chemicals and oil and gas industry, water and wastewater industry, power industry, mining and minerals industry, and others), type (gate, globe, ball, butterfly, and check and others), and geography (APAC, Europe, North America, Middle East and Africa, and South America). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

To learn more about this report, Download Report Sample

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Valves Market Customer Landscape

Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Industrialization and infrastructure development is the key factor driving the global valves market growth. Industrialization and infrastructure development efforts in emerging markets, especially in the Asia Pacific, the Middle East, and Africa, are driving the market. This includes the construction of new power plants, refineries, and pipelines that require many valves to regulate and control the flow of liquids and gases. Industrialization and infrastructure growth are key market drivers for the market. Increased industrialization and infrastructure-building activities, especially in growing countries such as the Asia Pacific, the Middle East and Africa, require many valves to control and regulate the flow of liquids and gases. Valves are critical components in several industries such as oil and gas, power generation, water treatment, and chemical processing.

Demand for valves is expected to increase as these economies expand and add infrastructure such as new pipelines, refineries, and power plants. Additionally, the growing need for valves in industrial applications is driving the development of new manufacturing techniques and increased spending on research and development. Valve manufacturers strive to develop new materials and techniques to increase the effectiveness and reliability of their valves. For example, the creation of smart valves that can be monitored and controlled remotely has gained popularity recently. This has allowed new players to enter the valve market, offering a range of innovative solutions to meet the growing valve needs of various industries. Hence, driving the growth of the market during the forecast period.

Increasing demand for industrial valves will fuel the global valves market growth. A major market trend in the market is the increasing demand for industrial valves. Industrial valves are used in oil and gas, chemical, power generation, water and wastewater treatment, and other fields. These valves help regulate the flow of fluids such as liquids, gases, and slurries and play an important role in many industrial processes.

The need for industrial valves is driven by the expansion of both industrialization and urbanization. The need for valves increases with the growing infrastructure built to support economic expansion. Also, as the world population grows, the need for resources such as energy and water is increasing, resulting in an increasing demand for faucets. The market is expected to increase due to the increasing demand in various sectors. The market is expected to grow during the forecast period, owing to increasing demand for industrial valves.

Intense competition among new and established players can majorly impede the growth of the market. There are many established and emerging competitors vying for dominance in the highly competitive market. Low barriers to entry, ease of production process, and increasing demand for valves in various industries are some of the factors fueling fierce competition in the market. One of the main issues facing the market is fierce competition. In a highly fragmented market, many players compete for market share. This competition can make it difficult for new entrants to establish a presence and for established companies to maintain market share.

Manufacturers are under pressure to differentiate their products and offer a unique value proposition to their customers as a result of intense competition. If manufacturers want to remain competitive, they must spend money on research and development to create new products and technologies that meet changing consumer expectations. To remain profitable in a highly competitive market, they must also focus on optimizing their manufacturing processes and reducing costs. To reach consumers and differentiate their products from those of their competitors, manufacturers must implement successful marketing techniques. Therefore, fierce competition between new and established players is likely to hamper the market's growth during the forecast period.

Vendors are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Alfa Laval AB: The company offers a wide range of valves, such as ball valves, butterfly valves, diaphragm valves, double seal valves, safety valves, and many more.

Baker Hughes Co: The company offers different types of valves, such as globe control valves, rotary control valves, safety valves, safety relief valves, and many more.

We also have detailed analyses of the market’s competitive landscape and offer information on 18 market vendors, including:

The report offers clients a deeper understanding of the market and its players through a combined qualitative and quantitative analysis of the vendors. The analysis classifies vendors into categories based on their business approach, including pure-play, category-focused, industry-focused, and diversified. Vendors are specially categorized into dominant, leading, strong, tentative, and weak to understand the dos and don’ts of business which in turn can help a client make the best decision.

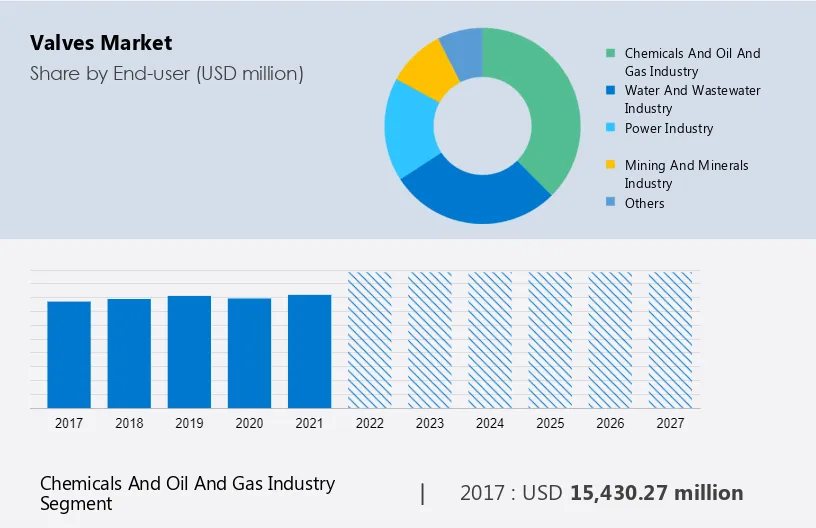

The chemicals and oil and gas industry segment will contribute a major share of the market, as this segment covers a wide range of applications such as refining, manufacturing, storage, and transportation of chemicals and oil and gas. The chemicals and oil and gas industry segment showed a gradual increase in market share with USD 15,430.27 million in 2017 and continued to grow until 2021. The chemicals, oil, and gas (COG) industry is one of the most important end users of the market. Valves are commonly used in these applications to control the flow of liquids and gases in pipelines, tanks, and reactors. They play a key role in ensuring the safe and efficient operation of these processes and are subject to stringent performance requirements and stringent regulations.

Get a Customised Report as per your requirements for FREE!

The COG industry requires valves that can withstand high pressures, high temperatures, and corrosive environments, as well as valves that can handle a wide variety of liquids and gases. As a result, the COG segment represents a significant opportunity for valve manufacturers and suppliers to offer customized solutions that meet the specific needs of this market. Demand for valves in the COG industry is driven by factors such as rising global energy consumption, increasing complexity of oil and gas reserves, and the need for advanced materials and technology to meet environmental and safety standards. These factors thus drive the growth of the COG segment of the market during the forecast period.

In the market, gate valves are considered one of the major market segments. Gate valves are used to regulate fluid flow in a variety of industries, including oil and gas, water treatment, and chemical processing. These valves can stop flow completely by having a flat plug that slides into the flow stream perpendicular to the direction of flow. Gate valves are often used in full-bore port applications to reduce pressure drop and fluid turbulence. Gate valves are also known for their superior durability and ability to close tightly, making them ideal for demanding industrial applications. A gate valve with a rising spindle allows movement. Non-rising stem gate valves, on the other hand, are inherently immovable, making them suitable for installation in tight spaces. Increasing demand for valves in the oil and gas, water and wastewater, and chemical processing industries contributes to the growth of the valve market. Therefore, the gate valve segment is expected to grow in the market during the forecast period.

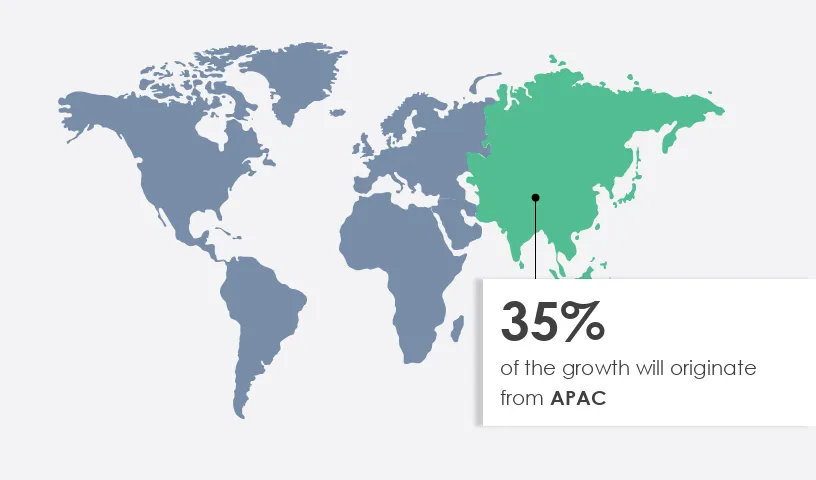

APAC is estimated to contribute 35% to the growth by 2027. Technavio’s analysts have elaborately explained the regional trends, drivers, and challenges that are expected to shape the market during the forecast period.

For more insights on the market share of various regions View PDF Sample now!

APAC has a sizeable growing market for valves. Valves are an important part of almost every industrial process and with the increasing industrialization and infrastructure development in the APAC region, the demand for valves is steadily increasing. Oil & Gas, Power Generation, Water & Wastewater, Chemicals & Pharmaceuticals are the key industries supporting the expansion of the valve market in APAC. The major players in this region's market are China, Japan, India, and South Korea, with China being the largest valve buyer as well as the largest producer in the region. The primary end-user of valves in the Asia-Pacific region, which accounts for the bulk of the market, is the oil and gas sector. Rising energy demand and the discovery of new oil and gas fields have increased the demand for valves in the oil and gas industry. The market in this region is highly competitive due to the presence of both foreign and domestic competitors. Although the industry is dominated by international players, regional companies are gradually gaining market share through aggressive pricing and customized product offerings. The market is expected to develop in the coming years due to increasing demand for valves in the APAC region, creating great opportunities for companies in the industry.

The COVID-19 pandemic has had multiple impacts on the valve market. An early impact of the pandemic was a decline in the market for valves, with many industrial activities halted or curtailed. As a result, the valve manufacturers' sales and profits declined. The market showed signs of recovery due to the need for valves in the healthcare and pharmaceutical sectors coupled with the progress of the pandemic. Valve manufacturers face many difficulties, including disruptions in logistics and supply chains, reduced end-user demand, and stoppages in production due to the pandemic. Cost-cutting measures taken by valve manufacturers, such as reducing labor and manufacturing costs and investing in new technologies to improve productivity and efficiency, have enabled them to adapt to changing market conditions. As the pandemic subsided and the recovery phase began, valve manufacturers found demand rebounding from many end-use industries, including oil and gas, water and wastewater treatment, and power generation. The growing market for valves in medical and pharmaceutical devices such as ventilators and oxygen concentrators has created new opportunities for valve manufacturers to diversify their product lines. During the forecast period, the market is expected to see increasing demand for valves from numerous end-user industries.

The valves market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

|

Valves Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

185 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.62% |

|

Market growth 2023-2027 |

USD 12,948.79 million |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

4.0 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 35% |

|

Key countries |

US, China, Japan, UK, and France |

|

Competitive landscape |

Leading Vendors, Market Positioning of Vendors, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Alfa Laval AB, Baker Hughes Co., Bray International Inc., Crane Holdings Co., Curtiss Wright Corp., Emerson Electric Co., Flowserve Corp., Forbes Marshall Pvt. Ltd., Honeywell International Inc., IMI Plc, KSB SE and Co. KGaA, Parker Hannifin Corp., SAMSON AG, Schlumberger Ltd., The Weir Group Plc, Trillium Flow Technologies, Valmet Corp., Valvitalia SpA, Watts Water Technologies Inc., and AVK Holding AS |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by End-user

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.