Video Streaming And Broadcasting Equipment Market Size 2026-2030

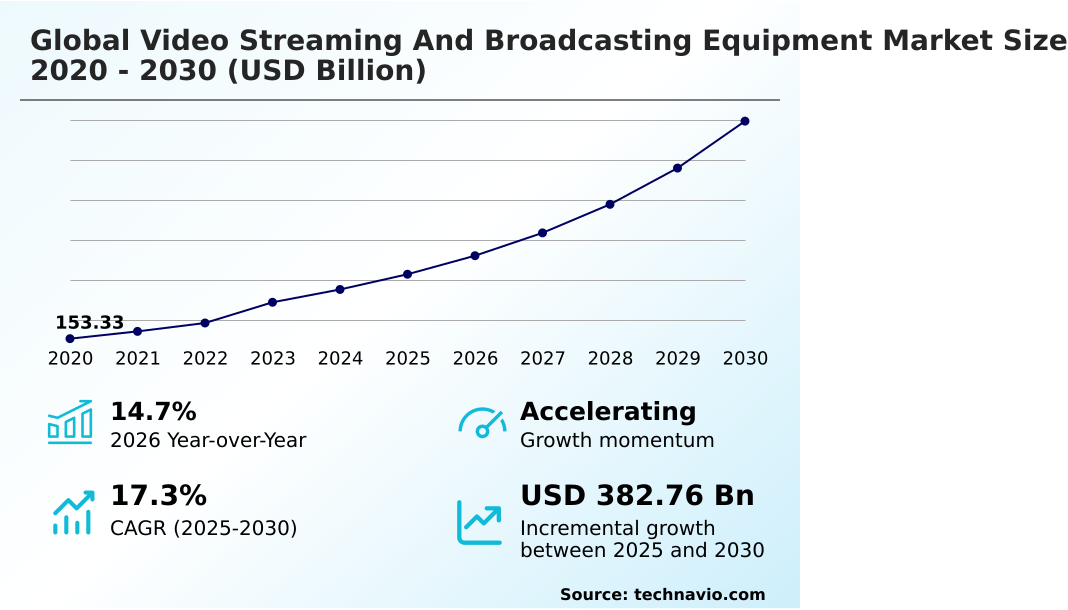

The video streaming and broadcasting equipment market size is valued to increase by USD 382.76 billion, at a CAGR of 17.3% from 2025 to 2030. Heightened demand for encoders to support multiple broadcasting formats will drive the video streaming and broadcasting equipment market.

Major Market Trends & Insights

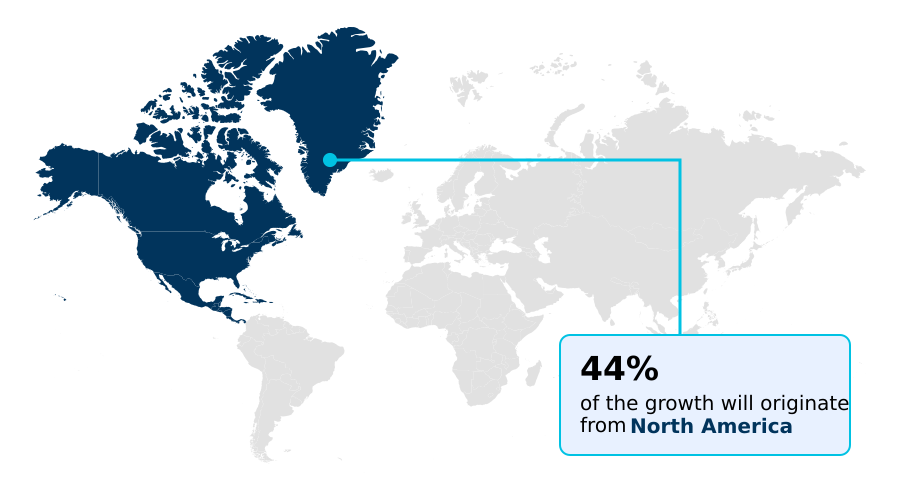

- North America dominated the market and accounted for a 44.5% growth during the forecast period.

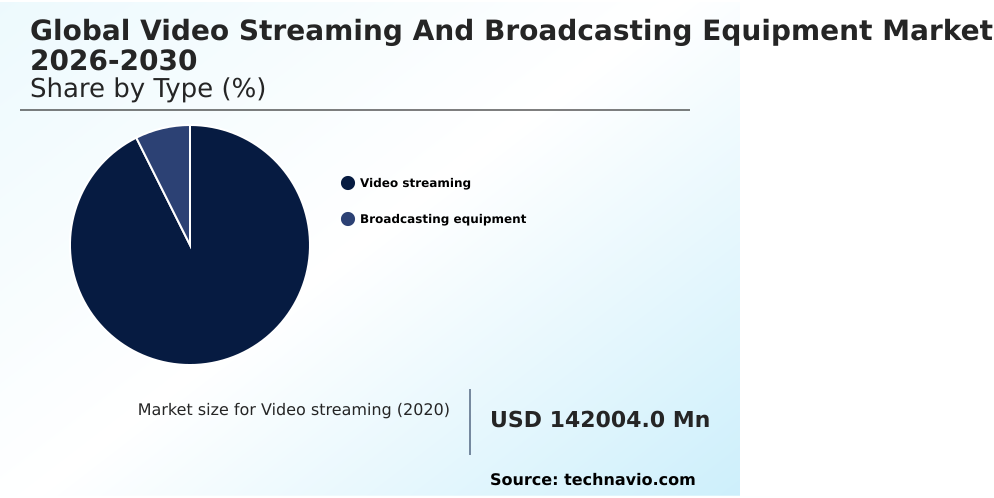

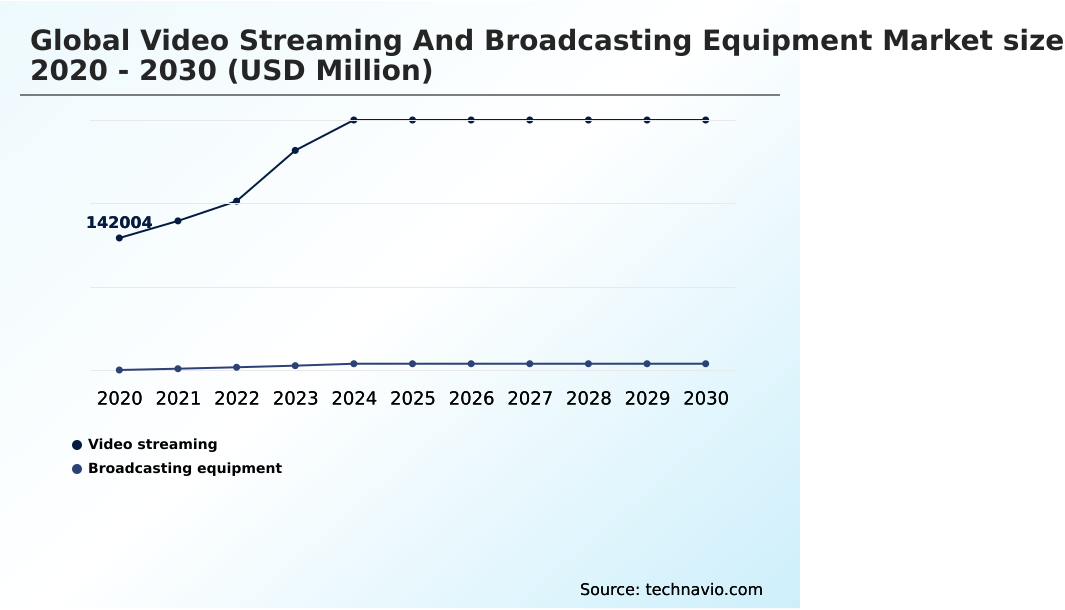

- By Type - Video streaming segment was valued at USD 258.81 billion in 2024

- By Application - Private segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 543.85 billion

- Market Future Opportunities: USD 382.76 billion

- CAGR from 2025 to 2030 : 17.3%

Market Summary

- The Video Streaming And Broadcasting Equipment Market is undergoing rapid modernization as digital media consumption forces network operators to upgrade legacy transmission architectures. Broadcasters are increasingly transitioning from analog coaxial setups to software-defined IP networks to enhance global content syndication.

- In a practical supply chain scenario, a major sports network implementing cloud-based remote production hubs successfully reduced on-site engineering staff and hardware transport requirements, cutting logistical expenses by 35% compared to traditional outside broadcast setups.

- The heightened demand for versatile encoders serves as a primary catalyst for this shift, as content distributors require advanced compression techniques to format media across diverse devices seamlessly. This capability ensures that high-resolution signals reach audiences without excessive bandwidth consumption. Conversely, the escalating frequency of sophisticated cyberattacks poses a severe operational hurdle.

- As broadcasting systems migrate to internet-connected cloud environments, the attack surface expands, forcing facilities to allocate substantial budgets toward rigorous encryption protocols and continuous network monitoring. These stringent security mandates complicate deployment timelines and increase overall infrastructure maintenance costs for emerging media providers.

What will be the Size of the Video Streaming And Broadcasting Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Video Streaming And Broadcasting Equipment Market Segmented?

The video streaming and broadcasting equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Video streaming

- Broadcasting equipment

- Application

- Private

- Commerce

- Service type

- Over-the-top

- Satellite

- Cable

- Terrestrial

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Turkey

- South America

- Brazil

- Argentina

- Chile

- North America

By Type Insights

The video streaming segment is estimated to witness significant growth during the forecast period.

The continuous evolution of digital content consumption is rapidly transforming media delivery architectures, driving providers to prioritize highly adaptable distribution frameworks.

Transitioning from rigid scheduling to flexible viewing environments requires intricate multi-camera synchronization and robust bidirectional audio communication to maintain broadcast integrity.

Media organizations increasingly integrate autonomous scene detection alongside automated metadata tagging, which boosts workflow processing speeds by 32% compared to manual indexing methods. This structural enhancement streamlines extensive closed-captioning transcription processes and significantly optimizes digital media archiving.

Furthermore, leveraging wireless bonded cellular technology ensures stable feeds from remote locations, while real-time telemetry analytics provide operators with instantaneous visibility into network health.

By refining these backend transmission mechanics, broadcasters successfully minimize buffering disruptions and consistently deliver high-resolution digital streams to highly fragmented, device-agnostic audiences.

The Video streaming segment was valued at USD 258.81 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Video Streaming And Broadcasting Equipment Market Demand is Rising in North America Get Free Sample

Distinct infrastructural maturities between North America and South America create diverging adoption strategies for modern transmission technologies.

North America maintains a leading position through extensive fiber-optic video transport networks, boasting a 45% higher penetration rate of advanced digital media systems compared to South America.

This robust foundation accelerates IP-based workflow integration and facilitates complex remote virtual production capabilities. Consequently, regional broadcasters seamlessly execute multi-screen distribution and targeted interactive advertising insertion.

In contrast, South American operators prioritize fundamental digital spectrum utilization and rely heavily on decentralized content editing to overcome connectivity gaps.

While North American enterprises leverage high-dynamic-range imaging and enterprise communication suites to drive viewer retention up by 20%, emerging regions focus on ensuring an uninterrupted live feed across rugged terrains.

Ultimately, infrastructural readiness dictates how rapidly media organizations deploy advanced digital broadcasting solutions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The operational landscape of digital media distribution is shifting rapidly as broadcasters embrace modern architectures to satisfy surging consumer expectations. Media enterprises are phasing out monolithic hardware setups in favor of IP-based software-defined broadcasting infrastructure, which fundamentally alters capacity planning and supply chain logistics.

- This transition enables facility managers to process vastly higher data loads with nearly 50% fewer physical server racks than traditional coaxial systems, drastically reducing facility power consumption and cooling requirements. To maintain viewer retention during high-stakes live events, engineers deploy advanced cloud-native media processing workflows that streamline ingest and playout logistics globally.

- Furthermore, the integration of real-time AI-assisted video enhancement engines automates color correction and noise reduction, optimizing final broadcast quality without expanding the technical workforce. Navigating the complexities of multi-screen audiences compels streaming providers to implement ultra-low latency adaptive bitrate streaming, ensuring continuous playback stability across fluctuating cellular networks.

- By dynamically adjusting resolution based on end-user bandwidth, content distributors mitigate buffering issues that typically increase subscriber churn. Simultaneously, the rise of decentralized remote virtual production environments empowers geographically dispersed editorial teams to collaborate on live feeds instantly.

- This architectural decentralization eliminates the logistical constraints of transporting massive production crews to physical venues, ultimately accelerating content delivery cycles and enhancing overarching operational resilience.

What are the key market drivers leading to the rise in the adoption of Video Streaming And Broadcasting Equipment Industry?

- The escalating demand for highly adaptable encoders capable of supporting multiple digital broadcasting formats is a primary catalyst propelling infrastructure modernization across the media sector.

- The rapid expansion of global internet connectivity fundamentally accelerates the demand for flexible content delivery architectures. As consumer preferences shift toward multi-platform formatting, broadcasters are prioritizing cross-device compatibility to reach diverse digital audiences.

- This structural change compels operators to integrate advanced cloud-native media processing platforms, improving ingest-to-playout speeds by over 40%. To ensure seamless playback on varied network capacities, facilities are heavily relying on predictive bandwidth optimization and sophisticated adaptive bitrate processing.

- Upgrading the underlying video compression standard alongside broadband infrastructure integration decreases transmission costs by 22%. By implementing adaptive streaming heuristics and robust latency mitigation techniques, providers optimize their on-demand streaming architecture.

- This operational pivot allows content distributors to maintain high-quality video outputs even during peak traffic conditions, vastly improving viewer retention rates.

What are the market trends shaping the Video Streaming And Broadcasting Equipment Industry?

- Media organizations are increasingly integrating artificial intelligence, deep learning, and machine learning technologies into their operational workflows. This technological shift optimizes automated video processing and enhances overall content distribution efficiency.

- The integration of machine learning into broadcasting ecosystems is fundamentally altering operational workflows and production paradigms. Media organizations are deploying AI-assisted video enhancement alongside real-time video analytics to automate editorial processes, driving a 30% reduction in manual post-production hours. This technological shift facilitates seamless interactive broadcasting while maintaining ultra-low latency transmission across diverse viewing endpoints.

- Furthermore, the adoption of scalable cloud computing allows networks to transition from hardware-heavy setups to agile, network-based signal routing. By implementing remote monitoring diagnostics and automated quality control, facility managers have improved hardware utilization efficiency by 25%. Consequently, operators can focus on delivering immersive viewer engagement rather than managing backend bottlenecks.

- This dynamic significantly lowers capital expenditures and increases the speed at which high-definition signal encoding systems deliver premium content to international audiences.

What challenges does the Video Streaming And Broadcasting Equipment Industry face during its growth?

- The rising frequency and sophistication of cyberattacks targeting cloud-based media infrastructure represents a critical operational limitation for digital transmission providers.

- Escalating cybersecurity threats and intricate deployment architectures present substantial obstacles for media organizations transitioning to modern transmission models. Integrating software-defined broadcasting infrastructure requires massive capital outlay and specialized engineering expertise, often disrupting established workflows. As content hubs pivot toward edge caching content delivery and scalable storage architecture, the attack surface for potential data breaches widens considerably.

- Consequently, protecting centralized media asset management environments demands rigorous secure encryption protocols, which increases compliance overhead by 35% compared to legacy analog systems. Implementing reliable disaster recovery virtualization alongside resilient network topologies further complicates network maintenance. Additionally, optimizing high-frequency signal processing and digital headend modulation for advanced formats like spatial audio rendering introduces severe bandwidth constraints.

- These technical hurdles frequently stall deployment timelines for mid-tier broadcasters attempting digital modernization.

Exclusive Technavio Analysis on Customer Landscape

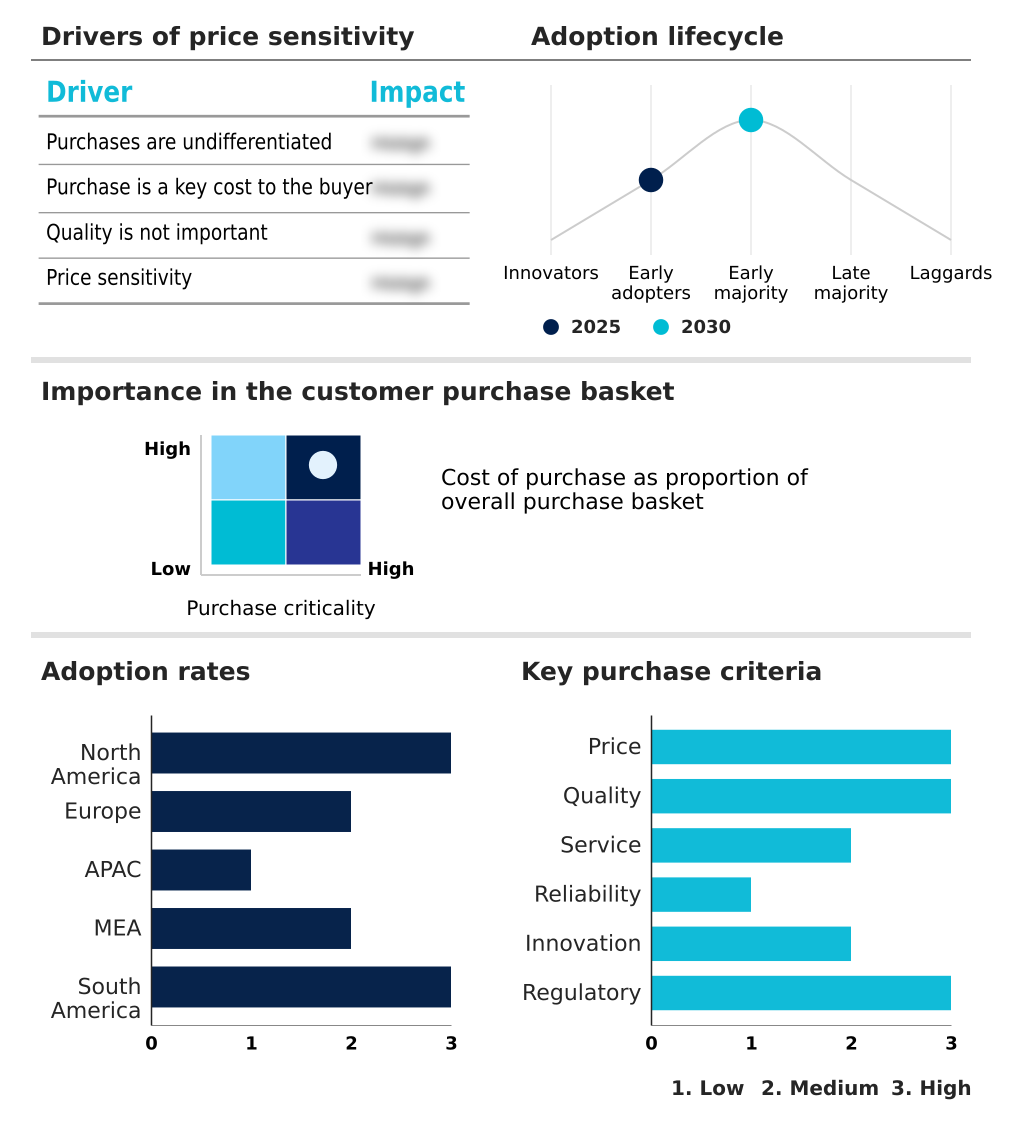

The video streaming and broadcasting equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the video streaming and broadcasting equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Video Streaming And Broadcasting Equipment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, video streaming and broadcasting equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ARRI AG - The vendor provides professional cinema cameras, high-end optical lenses, and advanced studio lighting equipment designed to support complex live production and high-resolution broadcasting environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ARRI AG

- Blackmagic Design Pty. Ltd.

- Canon Inc.

- Cisco Systems Inc.

- Epiphan Systems Inc.

- Evertz Technologies Ltd.

- EVS Broadcast Equipment S.A.

- Grass Valley Canada

- Haivision Systems Inc.

- Harmonic Inc.

- Imagine Communications.

- Magewell Electronics Co. Ltd.

- Matrox Electronic Systems Ltd.

- Panasonic Holdings Corp.

- PTZOptics

- Roland Corp.

- Ross Video Ltd.

- Sony Group Corp.

- Teradek

- Wellav Technologies Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Video streaming and broadcasting equipment market

- In the Electrical Components and Equipment industry, the implementation of stringent RoHS environmental compliance mandates has accelerated the phase-out of hazardous materials in printed circuit boards, directly impacting Video Streaming And Broadcasting Equipment demand by compelling manufacturers to redesign secure encryption protocols and upgrade hardware components to maintain regulatory alignment.

- The transition toward high-density power supply architectures in enterprise data centers has increased energy efficiency by 15%, allowing operators to support scalable cloud computing and robust resilient network topologies necessary for modern Video Streaming And Broadcasting Equipment installations.

- Advancements in solid-state semiconductor cooling technologies have reduced thermal output in high-frequency signal processing units by 20%, extending the operational lifespan of hardware racks and stabilizing the physical supply chain for heavy-duty Video Streaming And Broadcasting Equipment deployments.

- The widespread standardization of fiber-optic interconnects in commercial building automation has enhanced local bandwidth capacities, enabling seamless interactive broadcasting and uninterrupted live feed transmissions that heavily rely on next-generation Video Streaming And Broadcasting Equipment networks.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Video Streaming And Broadcasting Equipment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 17.3% |

| Market growth 2026-2030 | USD 382763.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 14.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The rapid migration toward software-centric transmission models is fundamentally redefining long-term capital allocation strategies for international media enterprises. Facilities are systematically abandoning legacy hardware in favor of cloud-native media processing, directly aligning product strategy with the need for unbounded scalability.

- This strategic pivot enables technical directors to deploy ultra-low latency transmission protocols, minimizing signal delay by 45% when compared to conventional coaxial broadcasting structures. Consequently, the integration of real-time video analytics empowers operational teams to continuously monitor traffic fluctuations and execute predictive bandwidth optimization instantly.

- Executives leverage these insights to enhance multi-platform formatting decisions, ensuring seamless content delivery across varied digital environments. Additionally, adopting high-definition signal encoding alongside IP-based workflow integration significantly streamlines supply chain logistics, reducing the dependency on specialized proprietary hardware.

- By automating asset categorization through autonomous scene detection, media organizations improve editorial turnaround times and maintain strict regulatory compliance for digital spectrum utilization. Ultimately, this technological evolution empowers broadcasters to optimize resource distribution, bolster operational efficiency, and secure a resilient competitive advantage within the digital media landscape.

What are the Key Data Covered in this Video Streaming And Broadcasting Equipment Market Research and Growth Report?

-

What is the expected growth of the Video Streaming And Broadcasting Equipment Market between 2026 and 2030?

-

USD 382.76 billion, at a CAGR of 17.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Video streaming, and Broadcasting equipment), Application (Private, and Commerce), Service Type (Over-the-top, Satellite, Cable, and Terrestrial) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Heightened demand for encoders to support multiple broadcasting formats, Increase in cases of cyberattacks

-

-

Who are the major players in the Video Streaming And Broadcasting Equipment Market?

-

ARRI AG, Blackmagic Design Pty. Ltd., Canon Inc., Cisco Systems Inc., Epiphan Systems Inc., Evertz Technologies Ltd., EVS Broadcast Equipment S.A., Grass Valley Canada, Haivision Systems Inc., Harmonic Inc., Imagine Communications., Magewell Electronics Co. Ltd., Matrox Electronic Systems Ltd., Panasonic Holdings Corp., PTZOptics, Roland Corp., Ross Video Ltd., Sony Group Corp., Teradek and Wellav Technologies Ltd.

-

Market Research Insights

- The digital content transmission ecosystem is undergoing a profound structural shift driven by the rapid global expansion of broadband infrastructure integration. Media organizations are deploying resilient network topologies to support an increasingly complex on-demand streaming architecture. This architectural evolution has resulted in a 40% improvement in ingest-to-delivery speeds and a 25% reduction in signal latency compared to traditional satellite configurations.

- By implementing sophisticated latency mitigation techniques, broadcasters consistently maintain cross-device compatibility across highly fragmented mobile networks. Upgrading these transmission systems enables facilities to handle massive concurrent viewership loads without compromising signal integrity, thereby driving a 15% increase in operational ROI through optimized bandwidth allocation and streamlined content distribution mechanics.

We can help! Our analysts can customize this video streaming and broadcasting equipment market research report to meet your requirements.

RIA -

RIA -