US Vodka Market Size 2025-2029

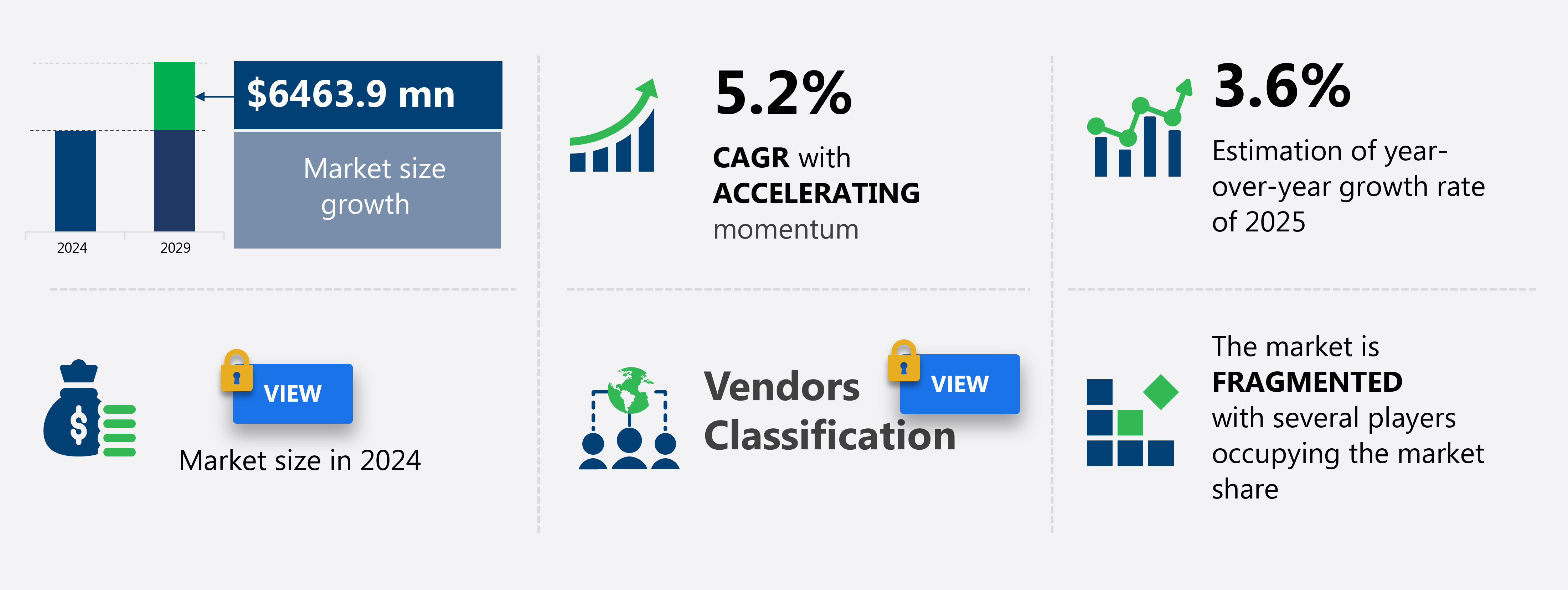

The vodka market in US size is forecast to increase by USD 6.46 billion at a CAGR of 5.2% between 2024 and 2029.

- The vodka market is experiencing significant growth, driven by several key trends. One notable trend is the increasing prominence of private-label brands, as consumers seek out affordable alternatives to premium offerings. Another trend is the rising demand for organic vodka, as health-conscious consumers look for beverage options free from additives and artificial ingredients.

- Additionally, the growing popularity of craft beer has led some breweries to expand their product lines to include vodka, offering unique and distinct flavors to the market. These trends are shaping the vodka market and providing opportunities for growth. However, challenges remain, including increasing competition and the need for innovation to differentiate products and meet evolving consumer preferences. Overall, the vodka market is poised for continued growth, driven by these trends and the adaptability of market players. Flavored vodkas, such as those infused with fruit flavors like cranberry, lime, raspberry, and citrus, are leading the market.

What will be the US Vodka Market Size During the Forecast Period?

- The vodka market has witnessed significant growth in recent years, with a focus on premiumization and innovation. Consumers are increasingly seeking out high-quality, authentic vodka experiences, leading to the rise of premium and high-end vodkas. This trend is evident in the growing popularity of flavored vodkas, which now account for a substantial share of the market. Flavored vodkas offer consumers a more diverse and exciting tasting experience, with fruit flavors such as blueberries and ruby red grapefruits being particular favorites. Vanilla and caramel flavors also continue to be popular choices, adding depth and complexity to cocktails. The wellness trend has also influenced the vodka market, with an increasing demand for gluten-free and organic vodkas.

- Consumers are increasingly gravitating toward vodkas crafted with high-quality ingredients and traditional distillation techniques to guarantee an authentic, pure taste. Bartenders and mixologists are leading the charge in this movement, experimenting with innovative flavors and mixing methods to create one-of-a-kind cocktails. The cocktail culture is flourishing, with bars, lounges, and even cocktail festivals showcasing an extensive range of vodka-based concoctions. Handcrafted vodkas, often produced in small batches at artisanal distilleries, are gaining traction for their personalized and authentic appeal, often featuring unique botanical infusions. The non-flavored vodka segment remains robust, with a focus on classic drinks and timeless cocktails.

- In the U.S. spirits market, the trend toward health-conscious vodka is rising, with a growing demand for low-calorie vodka, gluten-free vodka, and organic vodka. This shift aligns with the broader health and wellness movement, where consumers seek options that match their lifestyle. Vodka distribution channels such as supermarkets, bars, department stores, and direct-to-consumer sales are expanding to accommodate this demand.

- In conclusion, citrus-based cocktails continue to enjoy widespread popularity, offering a refreshing, zesty experience. Overall, the vodka industry remains dynamic and forward-thinking, with a strong focus on premiumization, authenticity, and innovation. Craft vodka growth is evident as consumers seek more refined, unique vodka experiences.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

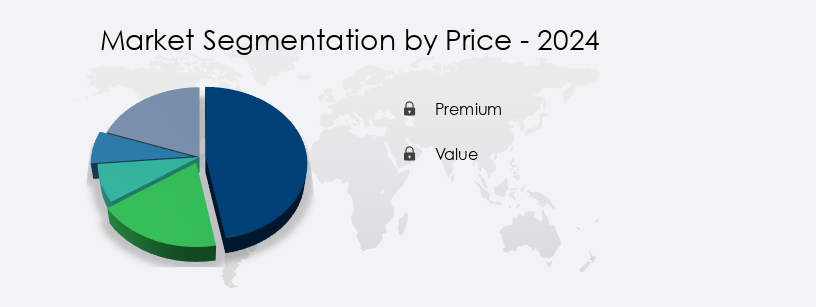

- Price

- Premium

- Value

- Distribution Channel

- On-trade

- Off-trade

- Product

- Unflavored

- Flavored

- Geography

- US

By Price Insights

- The premium segment is estimated to witness significant growth during the forecast period.

The premium vodka market in the US is expected to grow significantly in 2023, driven by the increasing consumer preference for high-quality ingredients in their alcoholic beverages. This segment includes premium, high-end premium, and super-premium vodkas, priced above USD 25. Factors such as new product launches and the addition of new flavors to existing lines are contributing to the growth of this segment. The US market, with its developed economy and high purchasing power, presents an attractive consumer base for premium vodka brands, particularly in on-trade distribution channels. Millennial consumers, who are increasingly influencing market trends, are a significant target demographic for players in the premium vodka market. The focus on cocktail culture and the rise of bars and lounges further boost the demand for premium vodkas.

Get a glance at the market report of share of various segments Request Free Sample

Market Dynamics

Our US Vodka Market researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of US Vodka Market?

The increasing prominence of private-label brands is the key driver of the market.

- The vodka market in the US is experiencing significant growth, driven by the increasing popularity of flavored vodkas and the rising demand for premium and high-quality vodkas among millennials. Retailers, particularly grocery stores, are capitalizing on this trend by introducing their own private-label vodka brands. These private labels offer consumers a more affordable option while maintaining the same high-quality standards as premium brands. Consumers are also showing a preference for gluten-free, organic, and non-GMO vodkas, which are being produced using traditional methods and handcrafted techniques.

- Furthermore, bartenders and mixologists are also playing a crucial role in the vodka market's growth by creating innovative cocktail recipes and promoting vodka cocktail culture in bars and lounges. Cocktail festivals and events are becoming increasingly popular, providing a platform for brands to showcase their offerings and engage with consumers. The wellness trend is also influencing the vodka market, with consumers seeking out low-alcohol content and non-flavored vodkas. Impurities are being minimized through the use of high-quality ingredients and distillation processes. The vodka market is expected to continue growing, with a focus on innovation, personalized botanical infusions, and low-alcohol beverages.

- In conclusion, consumers are becoming more health-conscious, and vodka brands are responding by offering a wider range of flavors and options to cater to this trend. Overall, the vodka market in the US is dynamic and diverse, with a strong focus on quality, innovation, and consumer preferences. Private-label vodkas are playing an essential role in this growth, offering consumers affordable options while maintaining the same high-quality standards as premium brands.

What are the market trends shaping the US Vodka Market?

Rising demand for organic vodka is the upcoming trend in the market.

- The vodka market in the US has witnessed a trend towards premiumization, with consumers seeking high-quality ingredients and traditional methods in their alcoholic beverages. This shift has led to the growth of premium and high-end vodka brands, as well as the popularity of flavored vodkas. Fruit flavors, such as cranberry, lime, raspberry, and citrus, have gained significant traction, while non-flavored vodka continues to hold a sizeable share of the market. Bartenders and mixologists have played a crucial role in driving this trend, with cocktail culture thriving in bars and lounges, cocktail festivals, and nightclubs.

- Additionally, the wellness trend has also influenced the vodka market, with consumers showing a preference for gluten-free and low-alcohol content vodkas. Organic vodka, made from organically cultivated raw materials, has gained popularity due to health consciousness and concerns about impurities in traditional grain-based vodkas. Fruit-based vodkas, such as those infused with blueberries, raspberries, and ruby red grapefruits, have also gained traction. IWSR Drinks reports that the organic infusions segment is expected to grow at a significant rate in the vodka market. Distilleries have emerged as key players in this segment, offering handcrafted and artisanal vodkas. The non-flavored segment is also expected to maintain its share of the market, with traditional drinks continuing to be popular.

- In conclusion, the vodka market in the US is witnessing a shift towards premiumization, with consumers seeking high-quality, organic, and flavored vodkas. The growing trend of health consciousness and the increasing popularity of cocktail culture have contributed to this shift, with bartenders and mixologists playing a crucial role in driving innovation and growth in the market.

What challenges does US Vodka Market face during the growth?

The growing popularity of craft beer is a key challenge affecting the market growth.

- The vodka market in the US is experiencing a shift towards premiumization, with consumers seeking high-quality ingredients and traditional methods in their alcohol choices. Premium vodkas and high-end brands are gaining popularity, as bartenders and mixologists incorporate these spirits into the cocktail culture at bars and lounges. Fruit flavors, such as cranberry, lime, raspberry, and citrus, are driving growth in the flavored vodka segment. Gluten-free and organic vodkas are also gaining traction, aligning with the wellness trend and health consciousness among millennials. Non-alcoholic and low-alcohol content beverages are another emerging trend, appealing to those who want to enjoy the vodka experience without the high alcohol content.

- However, handcrafted vodkas, organic infusions, and fruit-based vodkas are some of the popular offerings in this space. The distilleries producing these spirits are experimenting with various fruit flavors, including vanilla, caramel, blueberries, and ruby red grapefruits. Offline trading channels, such as liquor stores and supermarkets, remain the dominant sales channels for vodka, but online trading through blogging sites and alcohol delivery services is also gaining groun. IWSR Drinks reports that vodka remains the largest-selling spirit category in the US, with Smirnoff and Absolut being the leading brands. Brown Forman also holds a significant market share. Overall, the vodka market is expected to remain dynamic, with innovation and personalized botanical offerings continuing to drive growth.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Bacardi Ltd. - The company offers vodka through its brands GREY GOOSE, ERISTOFF, Stillhouse, and Ultimate Vodka.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bacardi and Co Ltd

- Becle SAB de CV

- Brown Forman Corp.

- Constellation Brands Inc.

- Davide Campari-Milano N.V.

- Diageo PLC

- E. and J. Gallo Winery

- Eastside Distilling Inc.

- Ethical Wine and Spirits Inc.

- Fifth Generation Inc.

- Globefill Inc.

- Grain and Barrel Spirits

- Novabev Group

- Pernod Ricard SA

- Phillips Distilling Co.

- Podlaska Wytwornia Wodek POLMOS SA

- Polmos Zyrardow Sp. ZOO

- Stoli Group S.ar.l.

- Suntory Holdings Ltd.

- William Grant and Sons Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Latest Market Development and News

- In December 2024, Constellation Brands announced the sale of its Svedka vodka brand to Sazerac, aiming to concentrate on its premium wine and spirits portfolio.

- In December 2024, Stoli Group USA filed for Chapter 11 bankruptcy protection, citing financial challenges such as decreased consumer demand post-pandemic, increased operational costs, inflation, a cyberattack, and a legal dispute over its vodka brand name with Russia.

- In December 2024, the U.S. vodka market experienced a 3% decline in spirits sales during the first seven months of the year, with vodka among the hardest hit categories.

- In December 2024, StateSide Urbancraft, a Philadelphia-based vodka company, was recognized as the 6th best cocktail vodka in the United States, highlighting its growing prominence in the market.

Research Analyst Overview

The vodka market has undergone significant transformations in recent years, with a shift towards premiumization, innovative flavors, and a focus on high-quality ingredients. This trend is driven by various factors, including the growing cocktail culture, the influence of bartenders and mixologists, and the increasing health consciousness of consumers. Premiumization has become a key trend in the vodka market, with consumers seeking out higher-end and artisanal brands. These premium vodkas are often produced using traditional methods and high-quality ingredients, resulting in a superior taste and smoother finish. The rise of high-end vodka has led to the emergence of new players in the market, offering unique and distinctive offerings to consumers. Another significant trend in the vodka market is the proliferation of flavored vodkas.

Furthermore, fruit flavors, such as cranberry, lime, raspberry, and citrus, have gained popularity among consumers, particularly millennials. These flavors are often used to create innovative cocktails and add a unique twist to traditional drinks. Vanilla and caramel are also popular choices, adding depth and complexity to the vodka's taste profile. Gluten-free and organic vodkas have also gained traction in the market, catering to consumers with specific dietary requirements and health consciousness. These vodkas are produced using natural ingredients and traditional methods, ensuring a pure and authentic taste. Bartenders and mixologists have played a crucial role in driving innovation in the vodka market. They have experimented with various flavors and ingredients, creating unique cocktails that have captured the imagination of consumers. Cocktail festivals and bars and lounges have become popular destinations for consumers looking to discover new and exciting vodka-based drinks. The wellness trend has also influenced the vodka market, with a growing demand for low-alcohol content and non-flavored vodkas.

In summary, these vodkas offer consumers a healthier alternative to traditional spirits, while still providing the taste and sophistication of vodka. The offline trading channel continues to dominate the vodka market, with hospitality venues such as bars and nightclubs being the primary outlets for vodka sales. However, the rise of e-commerce and blogging sites has opened up new opportunities for brands to reach consumers directly and build a loyal following. Grain-based vodkas remain the most popular choice among consumers, but fruit-based and handcrafted vodkas are gaining ground, offering unique and distinctive flavors that cater to the evolving preferences of consumers. In conclusion, the vodka market is undergoing a period of significant change, driven by the growing cocktail culture, the influence of bartenders and mixologists, and the increasing health consciousness of consumers. Premiumization, innovative flavors, and high-quality ingredients are key trends that are shaping the future of the vodka market.

|

US Vodka Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

159 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.2% |

|

Market growth 2025-2029 |

USD 6.46 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

3.6 |

|

Key countries |

US and North America |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -