White Chocolate Market Size 2024-2028

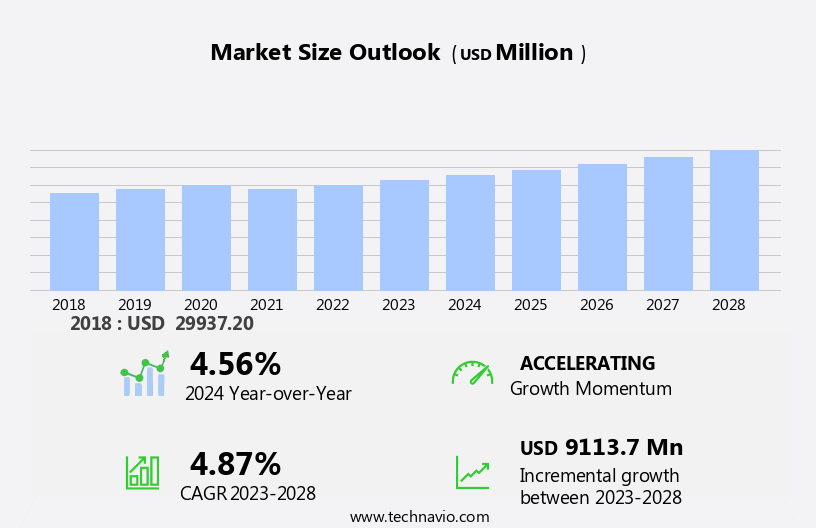

The white chocolate market size is forecast to increase by USD 9.11 billion at a CAGR of 4.87% between 2023 and 2028.

- White chocolate, a popular variation of chocolate, continues to capture the attention of consumers In the US and North America. The market is driven by several factors, including the increasing preference for premium chocolate offerings and the growing trend toward caramelized white chocolates. Additionally, the volatility of cocoa prices poses a challenge to the market. Chocolate is used in various applications, such as truffles, and cookies, and even as an ingredient in beverages like smoothies and coffee. In the confectionery industry, it is often used as an emulsifier in cosmetics and personal care products, as well as In the production of white chocolate bars and candies.

- Other applications include the use of white chocolate in baked goods, such as cakes and pastries, and In the creation of white chocolate-covered fruits and nuts. Chocolate is also finding its way into new applications, such as white chocolate wax for candles and white chocolate popcorn. With the growing popularity, convenience stores and supermarkets are stocking up on a wider range of white chocolate products, from buttery white chocolate spreads to orange-flavored white chocolate bars. Lecithin and vanilla are commonly used as emulsifiers in the production, while honey and other natural flavors are added to enhance the taste.

What will be the Size of the White Chocolate Market During the Forecast Period?

- The market encompasses a range of products, including truffles, bars, bulk, and various snack foods such as chips, cookies, popcorn, and beverages. This market experiences continuous growth due to increasing consumer preferences for indulgent treats and the "lipstick effect," which refers to the tendency for consumers to splurge on small luxuries during economic downturns. White chocolate's appeal stems from its unique taste profile, which is sweeter and creamier than dark chocolates. Its production involves the use of cocoa butter, sugar, milk products, vanilla, lecithin, and sometimes organic or natural ingredients to create a smooth texture and mild flavor. Innovative packaging and cost-effective ingredients have expanded white chocolate's reach beyond traditional chocolate retailers.

- Household care, lipstick, and health food stores, as well as coffee shops and premium chocolate outlets, now carry an extensive selection of these products. Consumers are increasingly drawn to the perceived health benefits, such as mood elevation, immunity boosting, digestion improvement, stress relief, and potential hypertension risk reduction. These health-conscious trends have led to the emergence of these chocolates as an ingredient in various food and beverage applications, further expanding the market's scope.

How is this White Chocolate Industry segmented and which is the largest segment?

The market report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- White chocolate bars

- White chocolate bulk

- White chocolate truffles

- Distribution Channel

- Offline

- Online

- Geography

- Europe

- Germany

- France

- North America

- Canada

- US

- APAC

- China

- South America

- Middle East and Africa

- Europe

By Product Insights

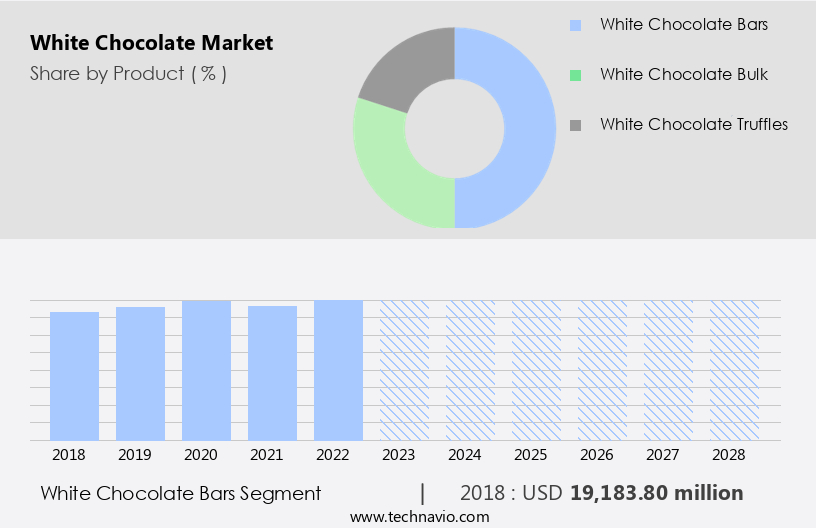

- The white chocolate bars segment is estimated to witness significant growth during the forecast period.

White chocolate bars, characterized by their creamy texture and mild sweetness, are primarily made from cocoa butter, sugar, and milk. Optional ingredients include natural and organic flavors such as vanilla, nuts, caramel, and fruit. Innovative packaging and cost-effective ingredients contribute to the market's growth. It is increasingly used in various sectors, including confectionery, household care, lipstick effect products, health food stores, coffee shops, and premium chocolates. Health benefits include mood elevation, immunity boosting, digestion improvement, and stress relief. Hypertension risk reduction is another potential health benefit. It is used in various forms, including truffles, bars, bulk, snack foods, and beverages.

Key players In the market include Nestle, Mondelez International, Mars, Barry Callebaut, and Arcor. Product innovation, such as the launch of vegan white chocolate variants and plant-based milk alternatives, continues to drive market growth.

Get a glance at the Industry report of share of various segments Request Free Sample

The white chocolate bars segment was valued at USD 19.18 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

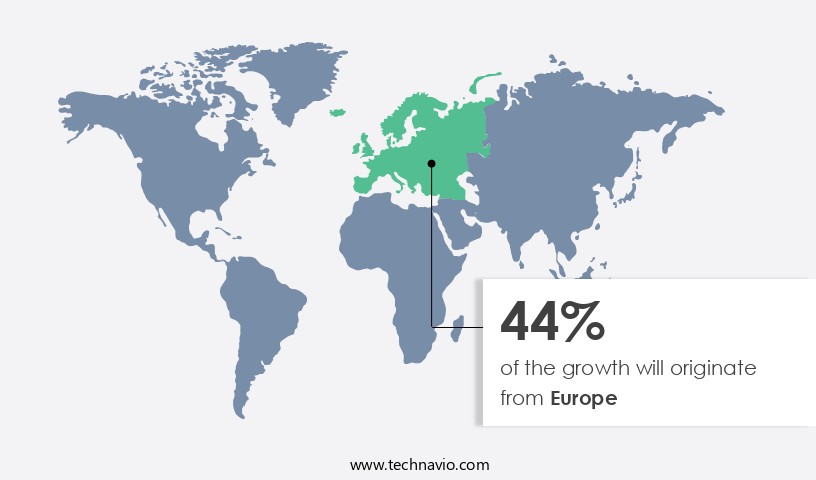

- Europe is estimated to contribute 44% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

Europe, known for its rich chocolate manufacturing tradition, experiences significant demand for premium chocolates, including white chocolates and organic variants. The European chocolate industry relies heavily on cocoa beans, leading to a growing interest in fine-flavored cocoa due to increasing health consciousness and obesity rates. companies focus on developing low-sugar chocolates, driving market growth through product innovation and launches. White chocolate, derived from cocoa butter, sugar, milk products, vanilla, lecithin, and sometimes natural ingredients, offers health benefits such as mood elevation, immunity boosting, digestion improvement, and stress relief. It is used in various applications, including confectionery, cosmetics, and personal care products, as a moisture barrier.

Further, the versatility extends to vegan variants, plant-based milk, and convenience foods like chips, cookies, popcorn, cupcakes, beverages, milkshakes, coffee, and smoothies. The European chocolate market is highly competitive and fragmented, with numerous players offering white chocolate truffles, bars, bulk, and snack foods. Key players include household care brands, lipstick effect markets like health food stores and coffee shops, and premium chocolate manufacturers.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of White Chocolate Industry?

Increasing premiumization of chocolates is the key driver of the market.

- White chocolate, derived from cocoa butter, sugar, milk products, and natural ingredients like vanilla and lecithin, is experiencing growing demand In the global market. Premium companies, such as Mars, Barry Callebaut, and Mondelez International, are differentiating their offerings by introducing innovative products and packaging. For example, Chocoladefabriken Lindt and Sprungli AG launched a new salted caramel truffle white chocolate in May 2020, featuring a silky caramel filling and a smooth milk chocolate texture. The appeal extends beyond confectionery. It is used in various industries, including household care, cosmetics, and beverages. The ability to act as a moisture barrier makes it an essential ingredient in cosmetic products.

- Vegan variants, made with plant-based milk, cater to the health-conscious consumer base. White chocolate's health benefits include mood elevation, immunity boosting, digestion improvement, and stress relief. Additionally, it may help reduce the risk of hypertension. These attributes contribute to its popularity In the health food sector and coffee shops. The versatility is evident in its application in various snack foods, such as chips, cookies, popcorns, and cupcakes. It is also used in beverages like milkshakes, coffee, and smoothies. Their premium image and higher profit margins make it an attractive offering for convenience stores and nongrocery retailers.

What are the market trends shaping the White Chocolate Industry?

Preference for caramelized white chocolates is the upcoming market trend.

- White chocolate, made from cocoa butter, sugar, milk products, and flavorings like vanilla, is gaining popularity In the confectionery market. Manufacturers are focusing on using organic and natural ingredients to cater to health-conscious consumers. Innovative packaging is another trend, making them more convenient for consumers, with offerings in sharing packs and individual servings. It is not just limited to desserts but is also used in household care, cosmetics, and personal care products for their moisture barrier properties. The "Lipstick Effect" is driving sales In these sectors. The health benefits, such as mood elevation, immunity boosting, digestion improvement, and stress relief, make it a preferred choice for health food stores, coffee shops, and premium chocolate consumers.

- Manufacturers are also introducing vegan variants using plant-based milk and lecithin. White chocolate truffles, bars, bulk, and snack foods like chips, cookies, popcorns, cupcakes, beverages, milkshakes, coffee, and smoothies are popular choices. The market is expected to grow due to these factors, offering opportunities for confectionery, cosmetics, and nongrocery retailers. Caramelized white chocolate, a recent innovation, adds depth to the flavor profile and opens up new possibilities for producers.

What challenges does the White Chocolate Industry face during its growth?

Unstable cocoa prices is a key challenge affecting the industry growth.

- White chocolate, derived primarily from cocoa butter, sugar, milk products, and vanilla, has gained popularity in various sectors due to its unique taste and versatility. The demand for organic and natural ingredients in white chocolate is on the rise, leading to innovative packaging and cost-effective production methods. They find applications not only in confectionery items like truffles, bars, and bulk sales but also in household care, lipstick effect products, health food stores, coffee shops, and premium chocolates. The market faces challenges due to the volatile prices of cocoa butter, a primary component. This volatility impacts the production costs for makers, making it difficult to estimate annual expenses.

- Despite this, the market continues to grow, driven by the health benefits associated with white chocolate, such as mood elevation, immunity boosting, digestion improvement, and stress relief. Additionally, it is used in various sectors, including cosmetics, personal care, and beverages, providing a moisture barrier and acting as a base for various products like caramelized white chocolate, sharing packs, and vegan variants made with plant-based milk.It is used in various applications, including snack foods like chips, cookies, popcorn, cupcakes, and beverages like milkshakes, coffee, and smoothies. It is also used in cosmetics, wax, nail enamel, oil, and other personal care products.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alfred Ritter GmbH and Co. KG

- AUGUST STORCK KG

- Barry Callebaut AG

- Cargill Inc.

- Carra Chocolates

- Chocoladefabriken Lindt and Sprungli AG

- Darrell Lea Confectionery Co. Pty Ltd.

- Ezaki Glico Co. Ltd.

- Ferrero International S.A.

- Fuji Oil Holdings Inc.

- ITC Ltd.

- Lotte Corp.

- Ludwig Weinrich GmbH and Co. KG

- MarieBelle

- Mars Inc.

- Molinos Rio de la Plata SA

- Mondelez International Inc.

- Nestle SA

- Nugali Chocolates

- Strauss Group Ltd.

- The Hershey Co.

- Unilever PLC

- Venchi SpA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

White chocolate, a beloved variation of the classic chocolate confection, has been gaining significant traction In the global confectionery market. This creamy, sweet treat, characterized by its lighter color and distinct flavor, is increasingly preferred by consumers seeking indulgent yet innovative sweet experiences. The market is driven by several key factors. Firstly, the growing demand for organic and natural ingredients is propelling the market forward. Consumers are increasingly conscious of the source and quality of their food, leading to a rise in demand made with premium, ethically-sourced ingredients. Another factor fueling the market is the trend towards innovative packaging.

Moreover, producers are investing in eye-catching, sustainable packaging solutions to differentiate their products and appeal to consumers. This not only enhances the visual appeal but also positions it as a premium, high-quality product. Cost-effective ingredients are also playing a role In the growth of the market. The use of cocoa butter, sugar, milk products, vanilla, lecithin, and other cost-effective ingredients enables manufacturers to produce them at a competitive price point, making them accessible to a wider consumer base. The versatility is another factor contributing to its popularity. It is used in a wide range of applications, from household care products and cosmetics to food and beverages.

Furthermore, in the food industry, it is used in various forms, including truffles, bars, bulk, snack foods, and baked goods such as cookies, cupcakes, and beverages like milkshakes and coffee. Their health benefits are also a significant market driver. It is believed to have mood-elevating properties, boost immunity, improve digestion, and provide stress relief. Additionally, it may help reduce the risk of hypertension, making it an attractive option for health-conscious consumers. The market is also witnessing the emergence of vegan and plant-based variants. This caters to the growing demand for ethical and sustainable food options, expanding the market's reach to a wider consumer base.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.87% |

|

Market Growth 2024-2028 |

USD 9.11 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.56 |

|

Key countries |

US, China, Germany, France, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the market growth of industry companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -