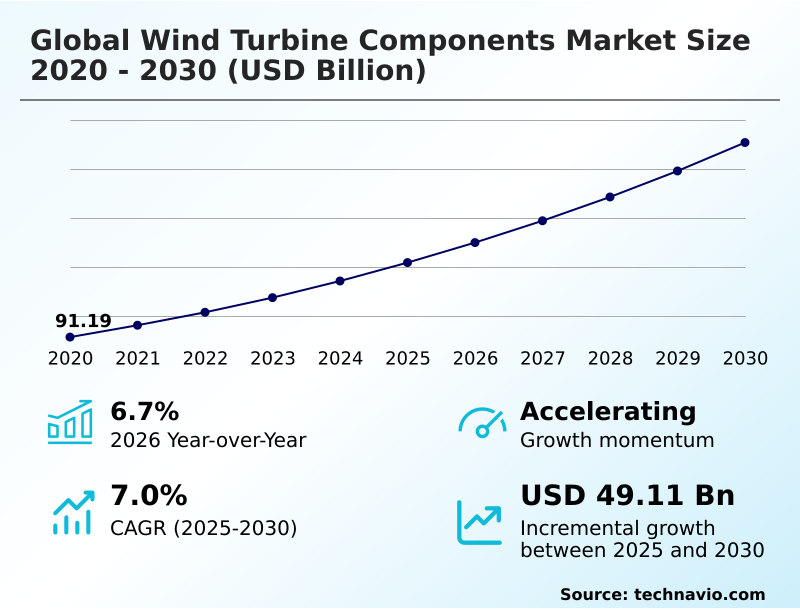

Wind Turbine Components Market Size 2026-2030

The wind turbine components market size is valued to increase by USD 49.11 billion, at a CAGR of 7% from 2025 to 2030. Rapid growth of global wind power industry will drive the wind turbine components market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 49.8% growth during the forecast period.

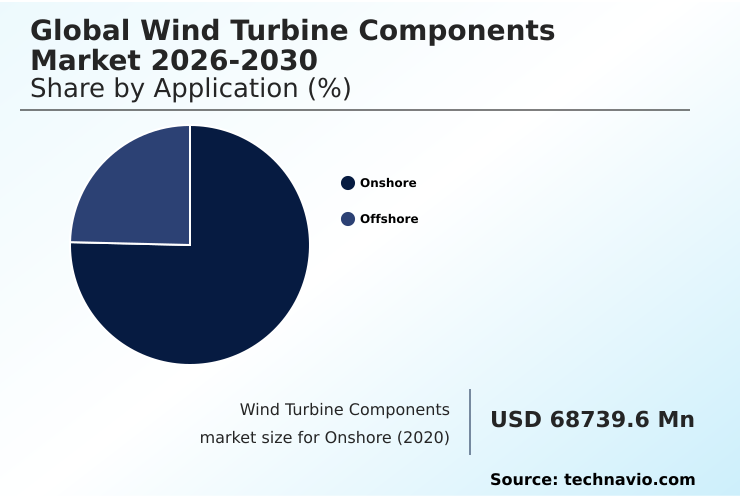

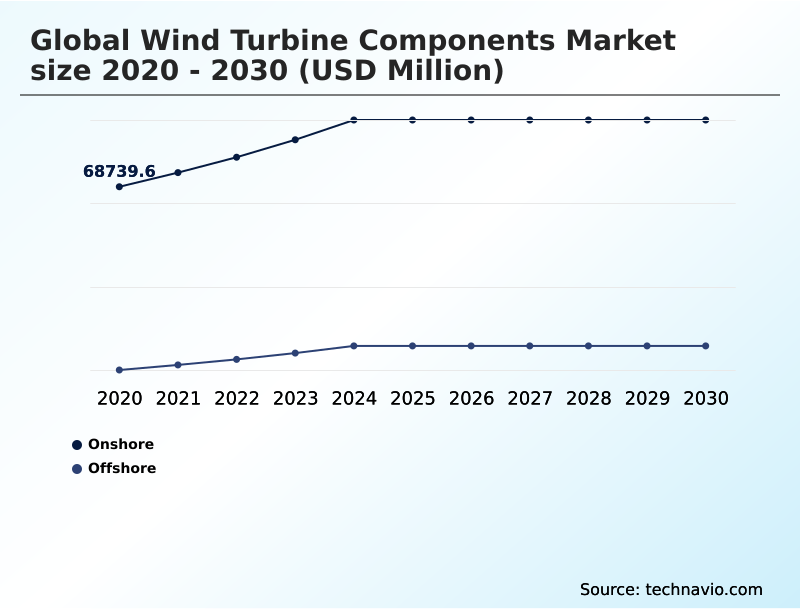

- By Application - Onshore segment was valued at USD 85.60 billion in 2024

- By Product - Wind turbine rotor blades segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 79.59 billion

- Market Future Opportunities: USD 49.11 billion

- CAGR from 2025 to 2030 : 7%

Market Summary

- The wind turbine components market is fundamental to the global energy transition, providing the essential hardware that converts wind into electrical power. This industry encompasses the design, manufacturing, and supply of parts ranging from massive wind turbine rotor blades and towers to intricate wind turbine gearboxes and power electronics.

- Key drivers include the rapid expansion of wind energy capacity, substantial investments in clean energy, and favorable government regulations promoting renewables. However, the sector faces considerable challenges, including material science complexities, such as the need for recyclable carbon-fiber-reinforced polymers, and the logistical hurdles of transporting oversized components.

- A critical business scenario involves manufacturers balancing the high cost of rare earth elements for direct-drive systems against the need for supply chain optimization. The trend towards larger, more powerful offshore turbines, requiring robust monopiles and floating platforms, is pushing engineering boundaries.

- Simultaneously, the integration of wind-solar hybrid plants with battery storage demands more sophisticated control systems and grid-forming inverters, underscoring the market's evolution toward creating resilient, high-performance energy ecosystems that can meet modern grid demands and sustainability goals.

What will be the Size of the Wind Turbine Components Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Wind Turbine Components Market Segmented?

The wind turbine components industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Onshore

- Offshore

- Product

- Wind turbine rotor blades

- Wind turbine gearboxes

- Wind turbine generators

- Wind turbine towers

- Others

- End-user

- Utility

- Commercial and industrial

- Residential

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- APAC

By Application Insights

The onshore segment is estimated to witness significant growth during the forecast period.

The onshore segment represents the most established application, focusing on the continuous refinement of mechanical parts for land-based terrains. Component manufacturing prioritizes the standardization of tubular steel towers and optimizing rotor diameters to suit diverse wind speeds.

The development of pitch drives and yaw systems is influenced by the need for cost reduction, operational longevity, and noise mitigation in populated areas.

Engineering efforts are directed toward creating modular tower designs and high-torque drivetrains for easier assembly, reducing project installation costs by over 15%.

The integration of advanced sensors and condition monitoring systems provides real-time data on structural components, supporting predictive maintenance strategies. This focus ensures high asset lifecycle management and minimal downtime across the operational fleet.

The Onshore segment was valued at USD 85.60 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 49.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Wind Turbine Components Market Demand is Rising in APAC Get Free Sample

The geographic landscape is undergoing a significant transformation, with APAC emerging as the primary growth engine, contributing nearly 50% of the incremental growth.

This expansion is driven by extensive onshore and offshore projects in China, supported by strong government initiatives and feed-in tariffs. In contrast, Europe’s mature market focuses on high-technology, including advanced power conversion systems and repowering projects to upgrade aging infrastructure.

North America is experiencing steady growth, supported by tax incentives that have spurred a 15% increase in domestic orders for wind turbine generators and control systems.

The development of high-power density generators and specialized composite materials is crucial for all regions.

This regional diversification, influenced by local content provisions and distinct energy targets, creates a complex but opportunity-rich environment for suppliers of pitch control mechanisms and other key hardware.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the wind turbine components market is marked by increasing specialization across its core segments. Onshore wind turbine component manufacturing continues to be driven by cost-efficiency and modularity, focusing on modular components for remote site assembly to streamline logistics.

- In contrast, the offshore sector is defined by the complex engineering challenges of offshore wind farm foundation design and the critical need for advanced corrosion protection for marine environments. The ongoing direct-drive vs geared drivetrain cost debate influences technological roadmaps, with decisions hinging on the impact of rare earth elements pricing and long-term maintenance projections.

- Sustainability is a growing concern, pushing for innovations in recyclable wind turbine blade materials and the adoption of a circular economy in the wind turbine industry. The rise of hybrid projects demands sophisticated wind-solar hybrid plant control systems to ensure grid stability with high renewable penetration.

- Consequently, high-capacity turbine predictive maintenance and structural health monitoring for turbine towers have become standard. The implementation of these digital solutions has been shown to reduce supply chain disruptions for spare parts by over 25% compared to reactive maintenance schedules, directly impacting operational planning and profitability.

What are the key market drivers leading to the rise in the adoption of Wind Turbine Components Industry?

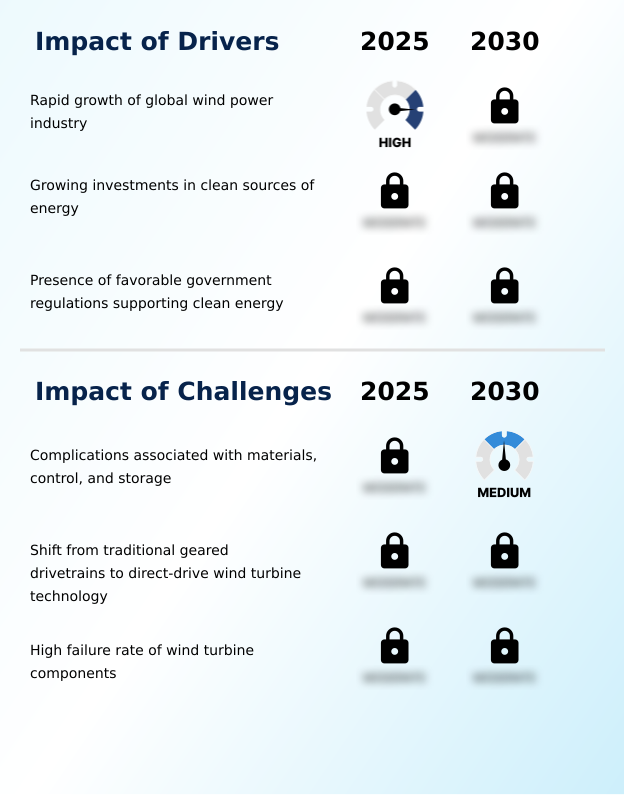

- The rapid growth of the global wind power industry is a key driver propelling expansion in the wind turbine components market.

- The market's expansion is fueled by the rapid growth of global wind power capacity, underpinned by strong government support and massive capital investment.

- Favorable regulations, including tax credits and power purchase agreements, have directly spurred a 15% increase in domestic orders for wind turbine towers and lattice towers in key regions.

- The influx of ESG-focused capital has been equally crucial, with dedicated credit facilities reducing the cost of debt for manufacturers of sub-station hardware by as much as two percentage points.

- This financial backing enables significant supply chain optimization and investment in new production facilities.

- The global push for decarbonization and the urgent need to replace fossil fuel plants ensure a massive, long-term order book, driving both mechanical stress analysis and innovation across the board.

What are the market trends shaping the Wind Turbine Components Industry?

- A key trend shaping the market is the consistently declining cost of wind power. This makes wind energy increasingly accessible and economically competitive against traditional power sources.

- Key trends are reshaping the market, led by the falling levelized cost of energy, which makes wind power highly competitive. This is driven by the development of larger, more powerful units requiring fewer subsea foundations, which improves the capacity factor by up to 20%.

- The move toward wind-solar hybrid plants, supported by advanced energy storage systems, is creating demand for hardware with enhanced grid-forming capability. These hybrid systems improve grid integration and can provide a more consistent power flow. Concurrently, the expansion into deep-water offshore wind is driving demand for super-turbines, some exceeding 20MW, which require specialized floating platforms and advanced corrosion-resistant coatings.

- This innovation in blade root sections and drive train peripherals enables energy yields over 30% higher than typical onshore sites.

What challenges does the Wind Turbine Components Industry face during its growth?

- Significant industry growth is challenged by complications associated with advanced materials, sophisticated control systems, and large-scale energy storage.

- Significant challenges constrain market growth, primarily related to materials, technology, and reliability. The reliance on advanced carbon-fiber-reinforced polymers and other composite materials for larger blades creates end-of-life recycling issues and heightens the need for circular economy models.

- The transition to direct-drive wind turbine technology introduces supply chain vulnerabilities, as the price of essential rare earth elements can surge by over 50% due to geopolitical factors. Furthermore, high failure rates of critical wind turbine components like gearboxes and main bearings, especially in harsh offshore environments, remain a major concern.

- These premature failures can lead to warranty claims that erode up to 10% of a project's profitability, highlighting the importance of rigorous aerodynamic load testing and quality control.

Exclusive Technavio Analysis on Customer Landscape

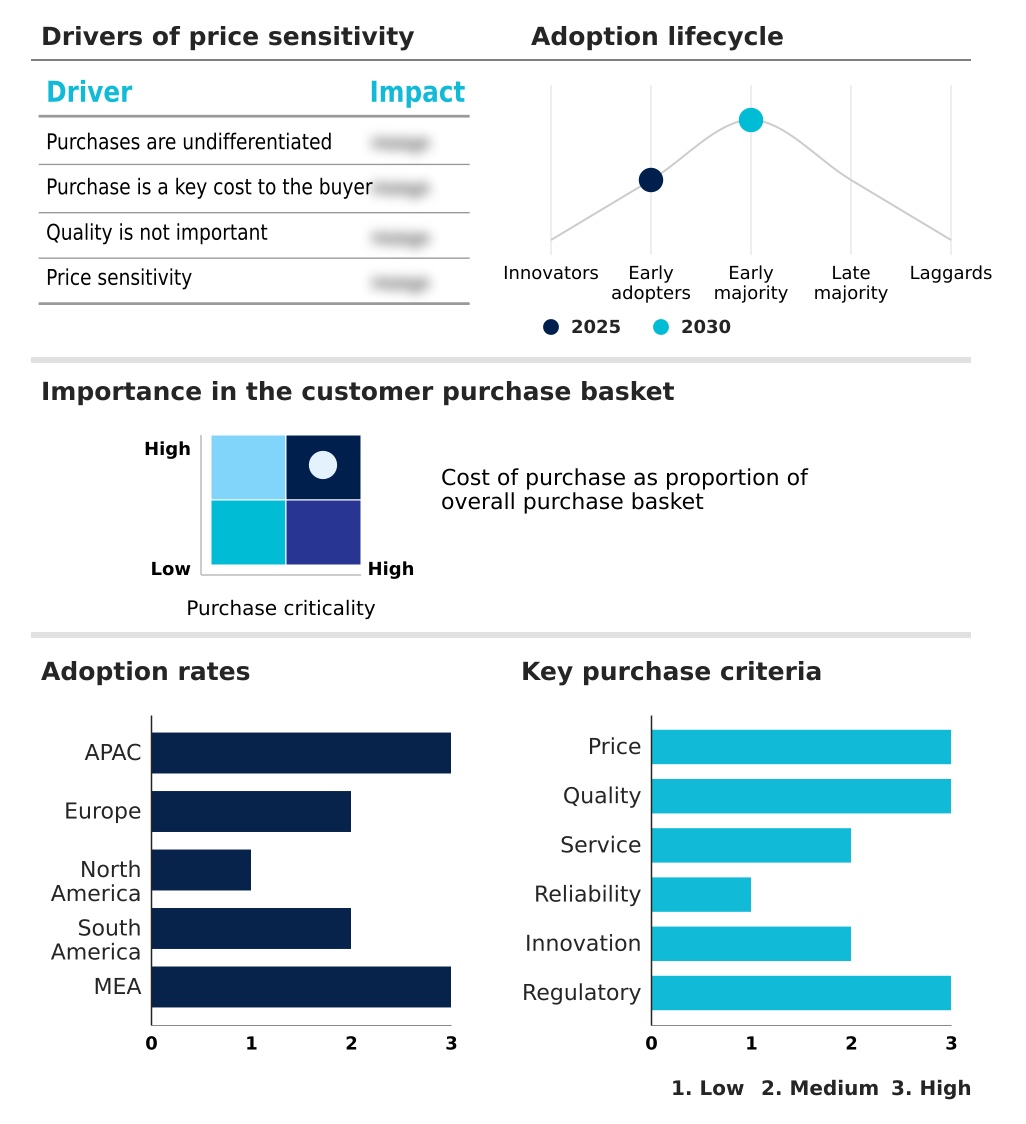

The wind turbine components market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wind turbine components market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Wind Turbine Components Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, wind turbine components market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

CS WIND Corp. - Offerings include a comprehensive range of wind turbine components, from structural towers and offshore substructures to integrated power solutions and drivetrain peripherals for renewable energy projects.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- CS WIND Corp.

- Dongfang Electric Corp. Ltd.

- EnBW Energie Baden Wurttemberg

- ENERCON GmbH

- Envision Group

- Flender GmbH

- GE Vernova Inc.

- Goldwind Science and Technology

- Gurit Holding AG

- ISHIBASHI Manufacturing Co

- LM Wind Power

- Max Bogl Wind AG

- Nanjing High Speed Gear

- Siemens Gamesa Renewable Energy

- Silbitz Group GmbH

- TPI Composites Inc.

- Vestas Wind Systems AS

- Wheels India Ltd.

- XEMC Darwind BV

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Wind turbine components market

- In August, 2024, a leading developer completed the world's largest wind-solar hybrid facility in North Africa, utilizing specialized control modules to demonstrate high technical synergy between variable renewable sources.

- In January, 2025, a major European grid operator implemented stringent new technical requirements for sub-station hardware, compelling suppliers in the market to redesign power electronics to manage rapid voltage fluctuations.

- In March, 2025, a prominent international wind developer reported a widespread structural defect in a specific series of generator bearings, triggering a global recall and a subsequent surge in demand for specialized maritime cranes and replacement parts.

- In May, 2025, a consortium of major investment banks announced a USD 50 billion credit facility for offshore wind infrastructure, which immediately spurred a wave of new contracts for subsea foundations and high-tension cables.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wind Turbine Components Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7% |

| Market growth 2026-2030 | USD 49109.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | China, India, Japan, South Korea, Vietnam, Indonesia, Germany, UK, France, Spain, Italy, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Egypt and Morocco |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The wind turbine components market is advancing through intense technological competition and a focus on lifecycle value. Core hardware such as wind turbine rotor blades, nacelle housing, and sophisticated wind turbine gearboxes are evolving to meet demands for higher capacity and reliability.

- The strategic shift toward direct-drive systems is a critical boardroom consideration, forcing a re-evaluation of supply chain dependencies on permanent magnets and rare earth elements versus investing in alternative technologies like doubly-fed induction generators.

- Advancements in material science, particularly with carbon-fiber-reinforced polymers, have enabled the creation of blades that are 10% longer while maintaining structural integrity, boosting the overall capacity factor. This push for innovation extends to power electronics and high-voltage control systems, which are essential for managing grid integration.

- The development of annular generators and robust main bearings underscores the industry's commitment to engineering excellence. Ultimately, success hinges on a manufacturer's ability to balance performance improvements with the economic realities of sourcing and production in a highly dynamic global landscape.

What are the Key Data Covered in this Wind Turbine Components Market Research and Growth Report?

-

What is the expected growth of the Wind Turbine Components Market between 2026 and 2030?

-

USD 49.11 billion, at a CAGR of 7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Onshore, and Offshore), Product (Wind turbine rotor blades, Wind turbine gearboxes, Wind turbine generators, Wind turbine towers, and Others), End-user (Utility, Commercial and industrial, and Residential) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rapid growth of global wind power industry, Complications associated with materials, control, and storage

-

-

Who are the major players in the Wind Turbine Components Market?

-

CS WIND Corp., Dongfang Electric Corp. Ltd., EnBW Energie Baden Wurttemberg, ENERCON GmbH, Envision Group, Flender GmbH, GE Vernova Inc., Goldwind Science and Technology, Gurit Holding AG, ISHIBASHI Manufacturing Co, LM Wind Power, Max Bogl Wind AG, Nanjing High Speed Gear, Siemens Gamesa Renewable Energy, Silbitz Group GmbH, TPI Composites Inc., Vestas Wind Systems AS, Wheels India Ltd., XEMC Darwind BV and ZF Friedrichshafen AG

-

Market Research Insights

- The market's dynamics are shaped by a strategic focus on improving operational efficiency and asset longevity. Innovations in remote sensing technology and a commitment to zero-defect performance are critical, with implementations of digital twins reducing unscheduled equipment downtime by an average of 20%.

- The industry-wide adoption of predictive maintenance protocols has enhanced material traceability and extended the lifespan of critical machinery, optimizing total cost of ownership. Furthermore, the emphasis on achieving dispatchable renewable energy through advanced energy storage systems has improved grid stability by over 15%, reinforcing the value proposition for utility-scale investments.

- This continuous drive for technical synergy and superior operational throughput defines the competitive landscape.

We can help! Our analysts can customize this wind turbine components market research report to meet your requirements.

RIA -

RIA -