Agricultural Films Market Size 2026-2030

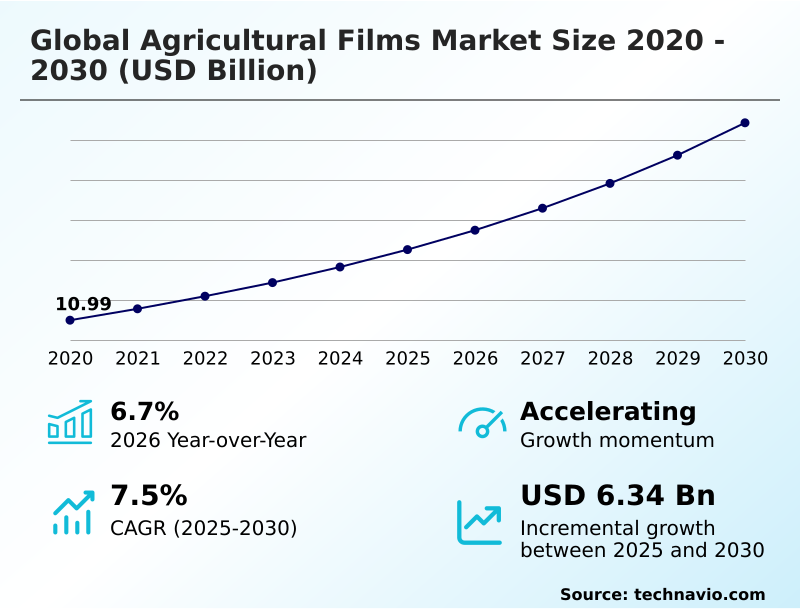

The Agricultural Films Market size was valued at USD 14.52 billion in 2025, growing at a CAGR of 7.5% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 75% growth during the forecast period.

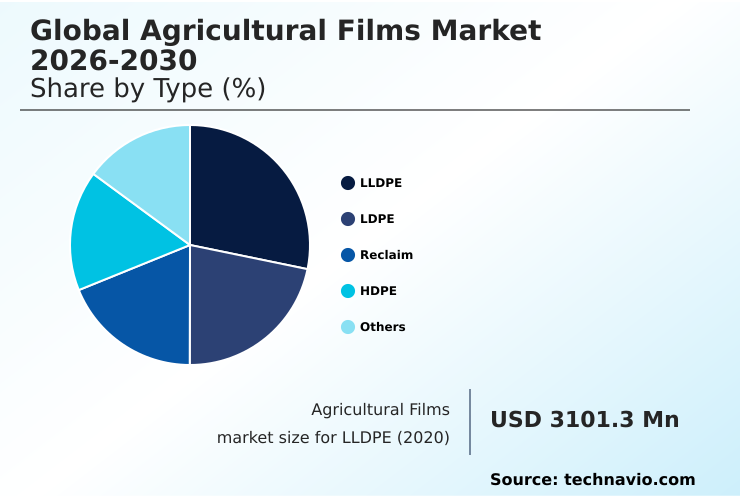

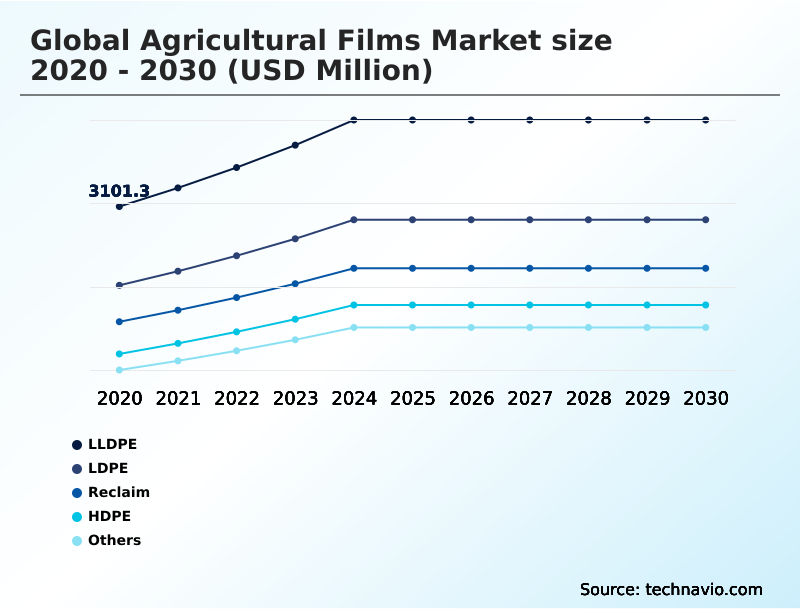

- By Type - LLDPE segment was valued at USD 3.88 billion in 2024

- By Application - Mulch films segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 9.87 billion

- Market Future Opportunities 2025-2030: USD 6.34 billion

- CAGR from 2025 to 2030 : 7.5%

Market Summary

- The agricultural films market is characterized by a strategic shift toward high-performance materials that directly enhance crop productivity and resource management. This evolution is driven by the urgent need to improve food security, with advanced films enabling farmers to achieve up to a 20% increase in water use efficiency through better soil moisture retention.

- A key driver is the adoption of multi-layer films, which offer superior durability and customized functionalities like photoselective light transmission. For instance, a produce grower might use a five-layer film with UV-blocking properties to reduce pest pressure by 15%, thereby lowering pesticide costs and improving crop quality. However, a significant challenge remains the environmental impact and disposal of conventional plastics.

- The high cost and performance variability of biodegradable alternatives hinder their widespread adoption, creating a complex operational dilemma for growers balancing agronomic benefits with sustainability mandates. This tension fuels continuous polymer science innovation.

What will be the Size of the Agricultural Films Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Agricultural Films Market Segmented?

The agricultural films industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- LLDPE

- LDPE

- Reclaim

- HDPE

- Others

- Application

- Mulch films

- Greenhouse films

- Silage films

- Product type

- Between 80-150 micron

- Up to 80 micron

- Above 150 micron

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Spain

- France

- Germany

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Turkey

- Rest of World (ROW)

- APAC

How is the Agricultural Films Market Segmented by Type?

The lldpe segment is estimated to witness significant growth during the forecast period.

The LLDPE segment of the agricultural films market is defined by superior mechanical properties, with adoption rates showing a 15% increase in applications requiring high durability.

This polymer, linear low-density polyethylene, enables downgauging technology, which reduces film thickness without compromising mechanical puncture resistance, a critical factor for silage wrap and high-performance mulch.

These films facilitate efficient mechanized film application, offering enhanced tensile strength compared to traditional LDPE. For instance, LLDPE-based silage films improve oxygen barrier properties by over 10% in multi-layer co-extrusions, ensuring optimal anaerobic silage fermentation and preserving feed quality.

The material’s compatibility with a UV stabilization package also extends its lifespan under intense solar radiation, making it a cornerstone of modern plasticulture techniques for crop protection strategies.

The LLDPE segment was valued at USD 3.88 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Agricultural Films market is rising in the leading region?

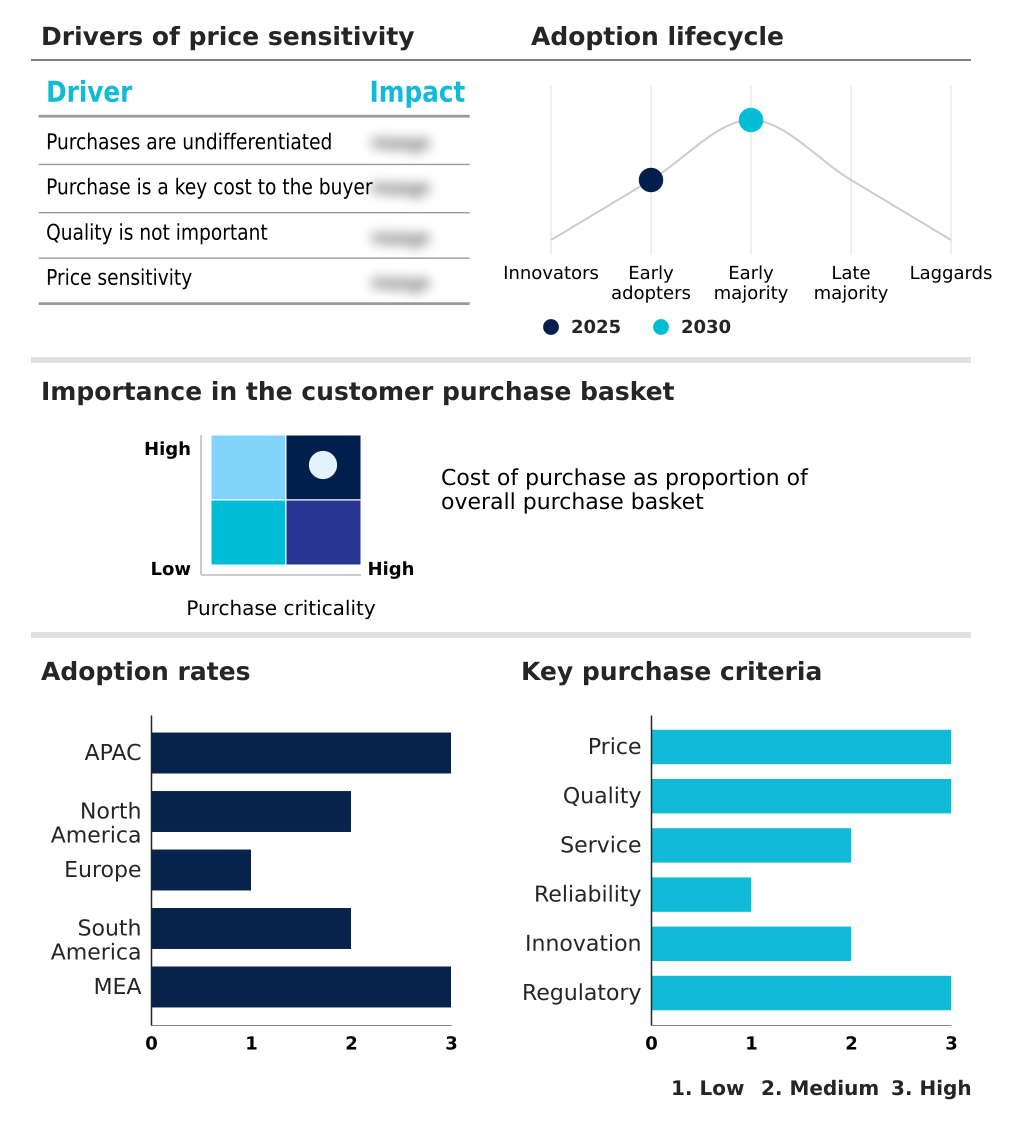

APAC is estimated to contribute 75% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Agricultural Films Market demand is rising in APAC Request Free Sample

The global agricultural films market exhibits significant geographic disparities, with APAC accounting for over 75% of the total market, a share more than seven times larger than that of North America.

This dominance is primarily driven by countries like China and India, whose markets were valued at approximately 4,511.1 million and 2,412.1 million respectively in 2025, reflecting intensive plasticulture techniques to ensure food security for vast populations.

In contrast, Europe's market growth, at 6.5%, is slower than North America's 7.9% expansion, influenced by stringent regulatory compliance frameworks mandating the use of soil-biodegradable polymers and materials with high post-consumer recyclate content.

This regulatory pressure directly impacts supply chain resilience, forcing European producers to invest heavily in circular economy principles, while producers in other regions may prioritize cost-efficiency and mechanical performance.

What are the key Drivers, Trends, and Challenges in the Agricultural Films Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Understanding the benefits of biodegradable mulch film is becoming essential for growers navigating stricter environmental regulations, as these materials can reduce end-of-life management costs by over 30% compared to conventional plastics. The decision-making process for farmers also involves evaluating lldpe vs ldpe silage film performance, where LLDPE's superior puncture resistance often justifies its higher initial cost by minimizing feed spoilage.

- In controlled environments, optimizing multi-layer greenhouse film light transmission is critical for maximizing photosynthesis and, consequently, crop yield. For instance, films that diffuse light can increase lower-canopy production by up to 15%.

- Specialized solutions are also crucial, as a uv stabilized film for desert agriculture must withstand extreme solar radiation, a factor that is directly linked to improving crop yield with reflective mulch. These reflective films can lower soil temperatures and deter certain pests, showcasing how film selection is a key component of modern, climate-resilient agriculture.

What are the key market drivers leading to the rise in the adoption of Agricultural Films Industry?

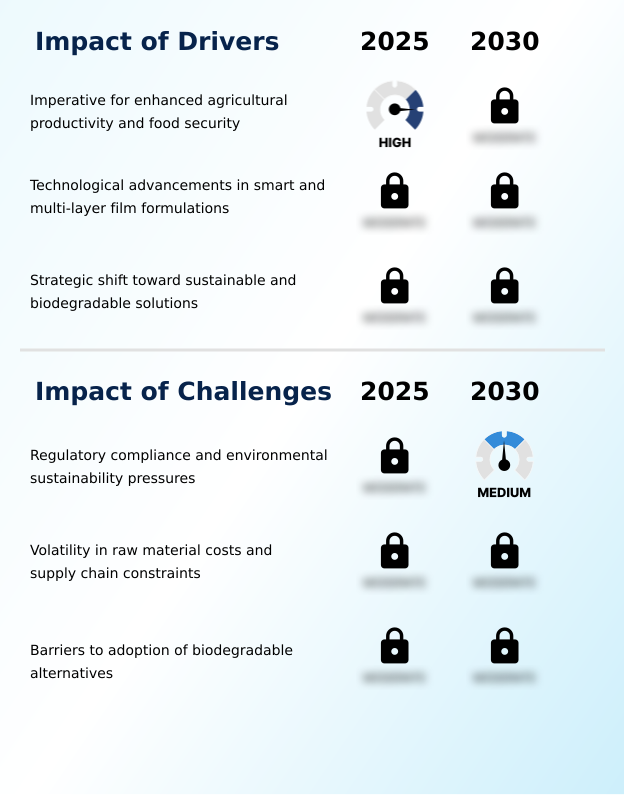

- The imperative for enhanced agricultural productivity and food security is the key driver for the agricultural films market.

- The primary driver for the agricultural films market is the escalating need for crop yield optimization to meet global food demand, with plasticulture techniques proven to increase yields by up to 30% in certain crops.

- This imperative is amplified by the need for greater water use efficiency, where mulch films can reduce soil water evaporation by more than 50%, a critical advantage in arid regions.

- Technological advancements in polymer science, particularly multi-layer extrusion, enable the creation of thinner, stronger films with specialized functions like controlled light diffusion. This downgauging technology reduces plastic usage per hectare, aligning with sustainable farming practices.

- The strategic shift toward biodegradable and recycled materials is also a significant driver, addressing environmental concerns and reducing labor costs associated with film disposal.

What are the market trends shaping the Agricultural Films Industry?

- The rapid commercialization of soil-biodegradable mulch films is an emerging trend, driven by environmental regulations and the operational need to reduce plastic residue in arable land.

- A dominant trend in the agricultural films market is the rapid commercialization of soil-biodegradable polymers, which can reduce on-farm plastic waste retrieval costs by up to 100%. This shift away from conventional plastics is accelerating due to regulations targeting microplastic pollution. Innovations in nanotechnology are also creating smart photoselective films that actively manage crop health.

- For instance, greenhouse films with UV-blocking nanoparticles can reduce insect pest populations by over 25% without chemical intervention. Furthermore, the institutionalization of circular economy principles is promoting the use of post-consumer recyclate (PCR) in film production.

- Advanced filtration technologies now allow for the creation of durable silage films containing high percentages of PCR, ensuring supply chain resilience while meeting sustainability goals.

What challenges does the Agricultural Films Industry face during its growth?

- Regulatory compliance and escalating environmental sustainability pressures are a key challenge affecting the growth of the agricultural films industry.

- A significant challenge for the agricultural films market is navigating complex and often unharmonized regulatory compliance frameworks, which can increase operational costs by over 15% for manufacturers. The volatility of feedstock costs, tied to fluctuating crude oil prices, poses another major constraint, as these price spikes are difficult to pass on to cost-sensitive farmers.

- This instability threatens supply chain resilience for essential materials like linear low-density polyethylene. Furthermore, the adoption of more sustainable alternatives faces hurdles; the price premium for soil-biodegradable polymers can be as high as 200% compared to conventional films. Performance inconsistencies, such as premature degradation in certain climates, also hinder widespread adoption and present a risk to crop protection strategies.

Exclusive Technavio Analysis on Customer Landscape

The agricultural films market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the agricultural films market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Agricultural Films Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, agricultural films market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ab Rani Plast Oy - Key offerings include advanced multi-layer films for agriculture and horticulture, such as specialized greenhouse covers, silage films, and mulch films designed for enhanced crop protection.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ab Rani Plast Oy

- Agriplast Tech India Pvt. Ltd.

- Amcor Plc

- Armando Alvarez Group

- BASF SE

- Coveris Management GmbH

- Dow Chemical Co.

- Exxon Mobil Corp.

- Ginegar Plastic Products Ltd.

- Henan Yinfeng Plastic Co Ltd.

- Industrial Development Co. sal

- Novamont S.p.A.

- PLASTIKA KRITIS SA

- POLIFILM GmbH

- RKW SE

- Sigma Plastics Group

- Tilak Polypack Pvt. Ltd.

- Trioplast Industrier AB

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Metal, Glass and Plastic Containers industry, the implementation of extended producer responsibility schemes for plastic packaging is accelerating the adoption of circular economy principles, directly pressuring the agricultural films market to increase the use of post-consumer recyclate and design films for improved end-of-life waste management.

- In the Metal, Glass and Plastic Containers industry, significant advancements in multi-layer extrusion technology, originally developed for flexible food packaging, are enabling the production of thinner, stronger agricultural films. This allows for downgauging, which enhances farm operational efficiency by reducing material consumption by up to 15% without sacrificing crucial oxygen barrier properties.

- In the Metal, Glass and Plastic Containers industry, persistent feedstock cost volatility, tied to crude oil and natural gas markets, is a major challenge. This instability drives innovation in the agricultural films sector toward alternative materials, such as soil-biodegradable polymers and bio-based resins, to ensure supply chain resilience and price stability.

- In the Metal, Glass and Plastic Containers industry, a rising consumer and regulatory focus on sustainable food production is creating demand for sustainable farming practices from the ground up. This shift directly impacts the agricultural films market by boosting demand for products that support water use efficiency, reduce chemical inputs, and align with organic certification standards.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Agricultural Films Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.5% |

| Market growth 2026-2030 | USD 6339.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Spain, France, Germany, Italy, UK, The Netherlands, Brazil, Argentina, Chile, South Africa, UAE, Turkey, Saudi Arabia and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The agricultural films market ecosystem is a complex value chain that begins with polymer science innovation from raw material suppliers providing resins like LLDPE and LDPE. Manufacturers then use technologies such as multi-layer extrusion to produce films, which must meet agronomic performance standards and increasingly stringent regulatory frameworks like EN 17033 for biodegradability.

- For instance, the mulch films segment holds over 45% of the market share, highlighting its importance. Distribution channels, including agricultural cooperatives and specialized dealers, are vital for reaching the fragmented end-user base of farmers. These end-users rely on films for crop yield optimization and resource management.

- The entire system is supported by research institutions that drive the development of new materials, such as soil-biodegradable polymers, and collection schemes that facilitate circular economy principles.

What are the Key Data Covered in this Agricultural Films Market Research and Growth Report?

-

What is the expected growth of the Agricultural Films Market between 2026 and 2030?

-

The Agricultural Films Market is expected to grow by USD 6.34 billion during 2026-2030, registering a CAGR of 7.5%. Year-over-year growth in 2026 is estimated at 6.7%%. This acceleration is shaped by imperative for enhanced agricultural productivity and food security, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (LLDPE, LDPE, Reclaim, HDPE, and Others), Application (Mulch films, Greenhouse films, and Silage films), Product Type (Between 80-150 micron, Up to 80 micron, and Above 150 micron) and Geography (APAC, North America, Europe, South America, Middle East and Africa). Among these, the LLDPE segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, South America and Middle East and Africa. APAC is estimated to contribute 75% to market growth during the forecast period. Country-level analysis includes China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Spain, France, Germany, Italy, UK, The Netherlands, Brazil, Argentina, Chile, South Africa, UAE, Turkey, Saudi Arabia and Israel, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is imperative for enhanced agricultural productivity and food security, which is accelerating investment and industry demand. The main challenge is regulatory compliance and environmental sustainability pressures, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Agricultural Films Market?

-

Key vendors include Ab Rani Plast Oy, Agriplast Tech India Pvt. Ltd., Amcor Plc, Armando Alvarez Group, BASF SE, Coveris Management GmbH, Dow Chemical Co., Exxon Mobil Corp., Ginegar Plastic Products Ltd., Henan Yinfeng Plastic Co Ltd., Industrial Development Co. sal, Novamont S.p.A., PLASTIKA KRITIS SA, POLIFILM GmbH, RKW SE, Sigma Plastics Group, Tilak Polypack Pvt. Ltd. and Trioplast Industrier AB. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the global agricultural films market, where APAC holds a 75% market share, is shaped by strategic innovation and regional expansion. Key vendors like RKW Group, Trioworld, and Armando Alvarez Group are focusing on developing high-performance, sustainable solutions to meet evolving regulatory standards and customer demands.

- For example, recent developments include the launch of advanced greenhouse films that improve light transmission by up to 10% and the introduction of silage sheets containing significant post-consumer recycled content. Companies such as Novamont are achieving milestones in biodegradable materials, securing certifications that validate their products for soil integration.

- These actions directly address the industry's primary challenge: balancing agricultural productivity with environmental stewardship, particularly concerning end-of-life plastic management.

We can help! Our analysts can customize this agricultural films market research report to meet your requirements.

RIA -

RIA -