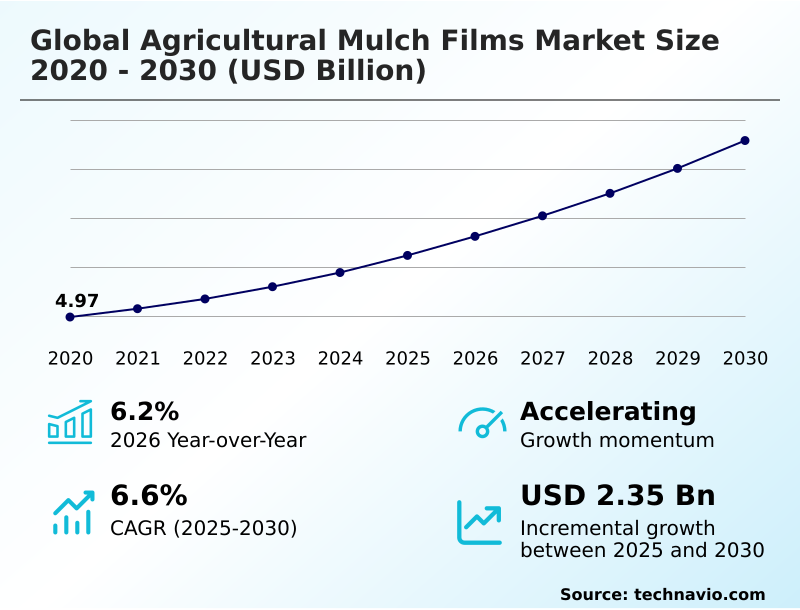

Agricultural Mulch Films Market Size 2026-2030

The agricultural mulch films market size is valued to increase by USD 2.35 billion, at a CAGR of 6.6% from 2025 to 2030. Accelerated transition toward biodegradable and soil-degradable film solutions will drive the agricultural mulch films market.

Major Market Trends & Insights

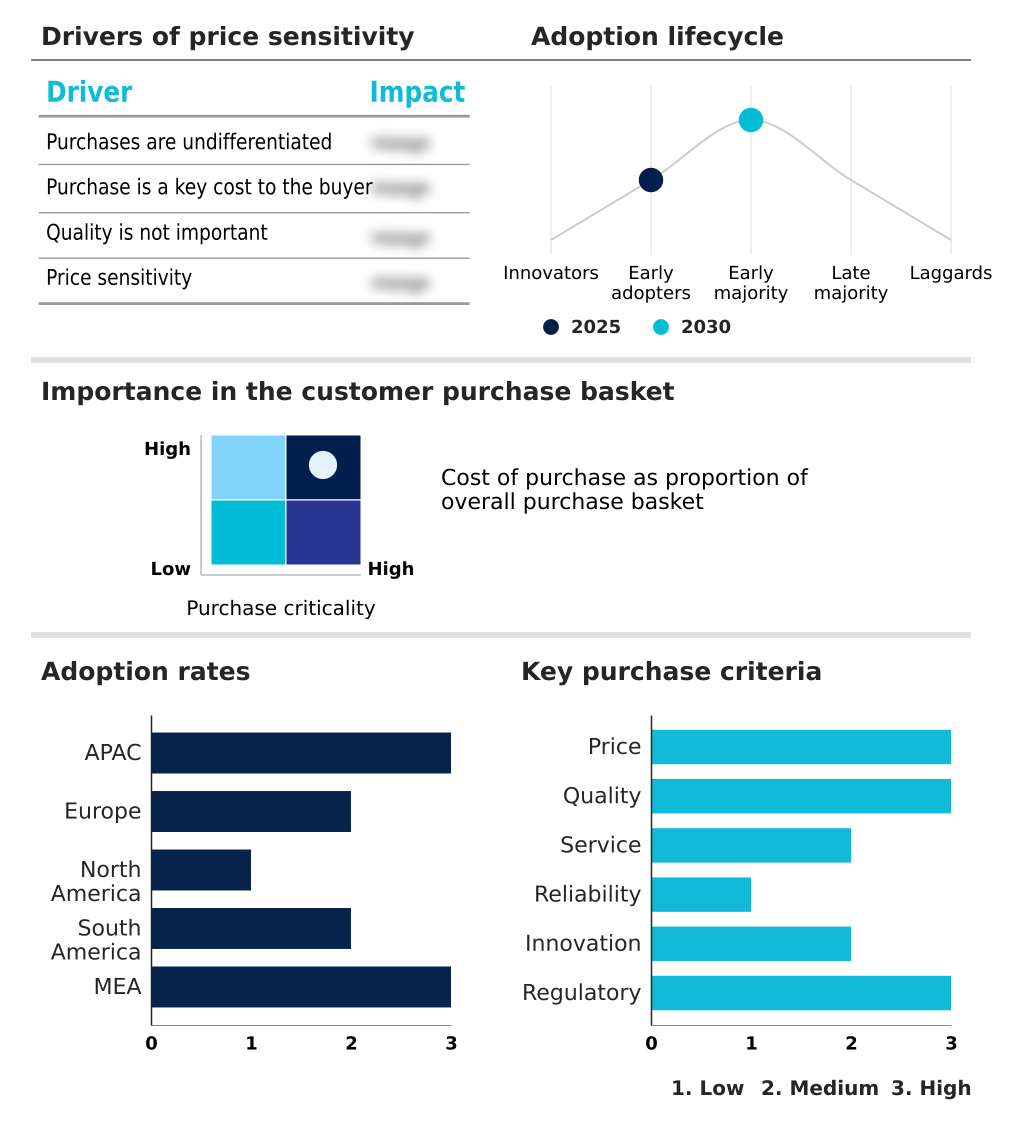

- APAC dominated the market and accounted for a 51.5% growth during the forecast period.

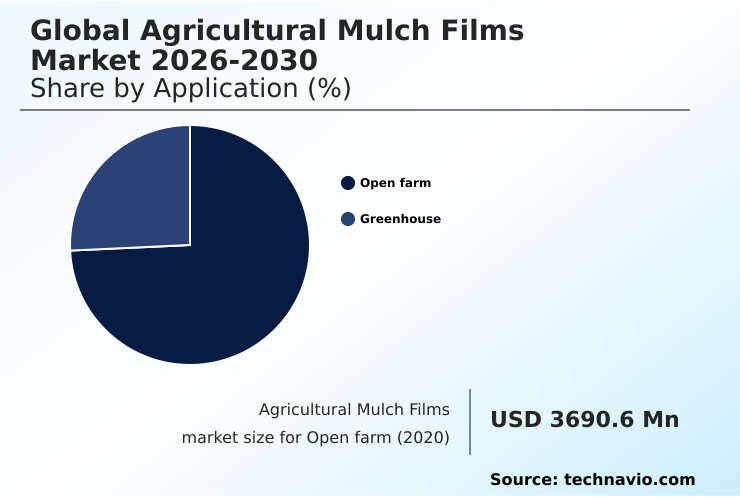

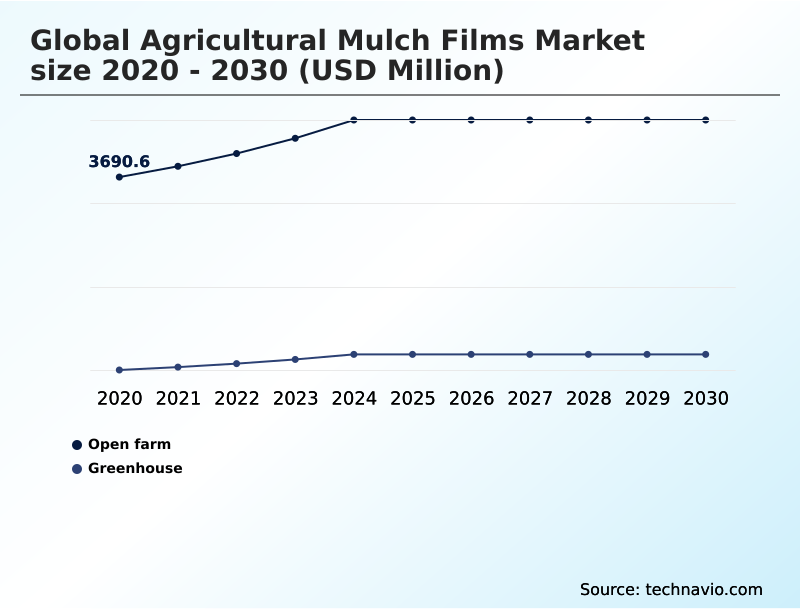

- By Application - Open farm segment was valued at USD 4.40 billion in 2024

- By Type - Conventional segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.61 billion

- Market Future Opportunities: USD 2.35 billion

- CAGR from 2025 to 2030 : 6.6%

Market Summary

- The agricultural mulch films market is undergoing a significant transformation, driven by the dual imperatives of enhancing food production efficiency and adopting sustainable farming practices. A key driver is the need to maximize yield per hectare amid shrinking arable land, which makes high-performance mulch films essential for conserving soil moisture retention and regulating root zone temperature.

- A dominant trend is the shift from conventional low-density polyethylene (ldpe) to soil-biodegradable polymers like polylactic acid (pla), spurred by stringent legislative frameworks aimed at reducing white pollution. Technological advancements in polymer chemistry are enabling the creation of multi-layer co-extrusion films with specialized functions, including photo-selective properties that influence crop morphogenesis and deter pests.

- However, the high agricultural input costs of these advanced materials and raw material price volatility present considerable challenges. For instance, a large-scale agricultural cooperative must weigh the immediate cost savings of conventional films against the long-term operational benefits and regulatory compliance of biodegradable alternatives, a decision that directly impacts its supply chain and environmental stewardship goals.

What will be the Size of the Agricultural Mulch Films Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Agricultural Mulch Films Market Segmented?

The agricultural mulch films industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Open farm

- Greenhouse

- Type

- Conventional

- Biodegradable

- Product type

- Black

- Transparent

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Israel

- Turkey

- Rest of World (ROW)

- APAC

By Application Insights

The open farm segment is estimated to witness significant growth during the forecast period.

The open farm segment, driven by extensive cultivation of broad-acre crops, prioritizes films offering high mechanical strength, durability, and cost-effectiveness. These films must withstand rigorous mechanical installation and environmental exposure.

Black mulch films dominate due to superior weed suppression mechanism and ability to warm the soil, extending growing seasons. However, the labor-intensive removal of conventional films is accelerating adoption of soil-biodegradable polymers that can be tilled directly into the soil.

For instance, the economic return from using these high-performance mulch films often results in yield increments exceeding 30%, a key factor for achieving yield per hectare optimization and ensuring economic viability in modern agriculture.

This shift underscores a broader move toward more efficient and sustainable farming practices.

The Open farm segment was valued at USD 4.40 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 51.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Agricultural Mulch Films Market Demand is Rising in APAC Get Free Sample

The global agricultural mulch films market landscape is led by APAC, which is projected to contribute 51.5% of the incremental growth. This dominance is driven by government initiatives in China and India aimed at modernizing agriculture and addressing environmental concerns.

In China, strict standards are being enforced to increase the recovery rate of agricultural plastic film to 85%, which is stimulating investment in mechanical recycling process technologies and promoting the use of post-consumer recyclate (pcr).

In Europe, the market is shaped by stringent environmental regulations and Extended Producer Responsibility (EPR) schemes, pushing manufacturers toward certified soil-biodegradable polymers and circular economy models.

These legislative frameworks are compelling a transition away from films made with linear low-density polyethylene (lldpe) to more sustainable alternatives, addressing the challenge of microplastic contamination and promoting long-term soil health management.

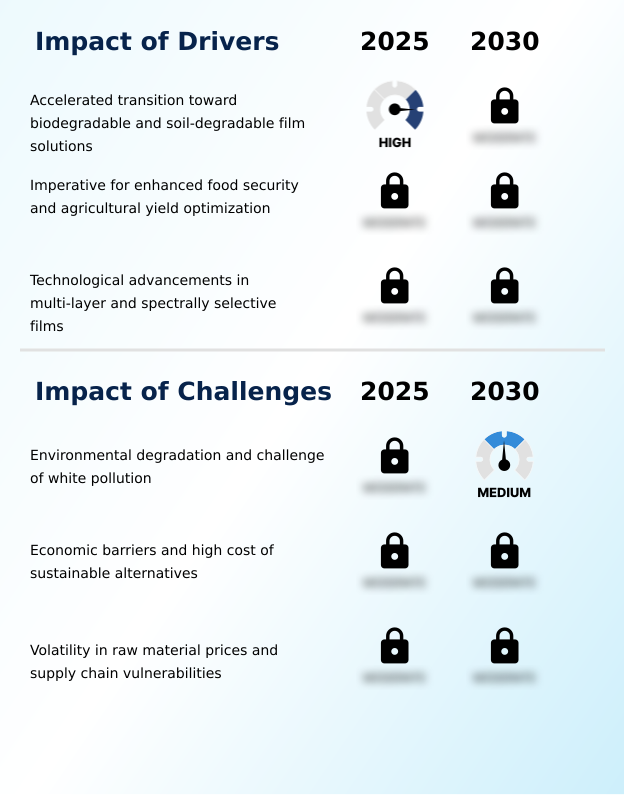

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the agricultural mulch films market increasingly involves a detailed cost analysis of photo-selective films versus conventional options. Understanding the benefits of biodegradable vs conventional mulch is critical, as is evaluating the impact of mulch film color on crops, which can enhance fruit quality with reflective films.

- The role of mulch in precision agriculture is expanding, with mulch film compatibility with drip irrigation becoming a standard for optimizing water use. For growers in arid regions, selecting the appropriate mulch film for water-scarce regions is a key determinant of success.

- Technological advancements are central to this evolution, with nanotechnology in ultra-thin mulch films enabling material reduction without sacrificing performance. Concurrently, there is a strong focus on the circular economy for agricultural plastics, with new technologies for recycling agricultural films being developed to tackle the challenges of mulch film disposal.

- Regulating soil temperature with mulch remains a primary function, but the use of multi-layer film for pest repellency is also gaining traction. Ensuring mulch film performance in greenhouse settings and preventing soil erosion with mulch films are additional considerations.

- The push for improving crop yield with black mulch continues, while adherence to standards for soil-biodegradable mulch is becoming mandatory in many regions. Ultimately, the economic viability of sustainable mulch films is improving, with advanced systems showing a nearly 25% greater return on investment compared to traditional methods over a three-year cycle due to reduced labor and disposal costs.

What are the key market drivers leading to the rise in the adoption of Agricultural Mulch Films Industry?

- The market's growth is significantly driven by the accelerated transition toward biodegradable and soil-degradable film solutions, spurred by environmental regulations and the need for sustainable farming practices.

- The market's expansion is propelled by the imperative for enhanced food security and agricultural yield optimization. The accelerated adoption of soil-biodegradable polymers is a primary driver, fueled by the need for sustainable farming practices.

- These advanced materials offer dual benefits, maintaining soil moisture and temperature while aligning with environmental stewardship goals. The integration with precision agriculture is critical, as smart mulch film solutions are being deployed to optimize yield in water-scarce regions.

- Pilot programs have demonstrated a 20% reduction in water usage while maintaining historical yield benchmarks.

- Furthermore, technological advancements in multi-layer and spectrally selective films, which actively manipulate the growing environment, are contributing to yield increments that often exceed 30%, ensuring economic viability for farmers.

What are the market trends shaping the Agricultural Mulch Films Industry?

- A key market trend is the emergence of nanotechnology-enhanced films. These advanced materials provide superior mechanical strength, enabling downgauging for reduced material use without performance loss.

- Key trends are reshaping the market, moving it toward sophisticated agronomic tools. The emergence of nanotechnology-enhanced films allows for significant downgauging technology, with some new polyethylene nanocomposite formulations enabling a 30% reduction in thickness without compromising tensile strength or soil moisture retention. This innovation allows for the creation of ultra-thin films that meet demands for cost-effective cultivation.

- Concurrently, the rise of multi-layer co-extrusion and photo-selective films is enabling precise manipulation of light to influence crop morphogenesis. Field trials with specific blue mulch films have demonstrated a 15% increase in cucumber yields. These advancements are integrating films into the digital farm ecosystem, enhancing food production efficiency.

What challenges does the Agricultural Mulch Films Industry face during its growth?

- A primary challenge affecting market growth is the environmental degradation caused by plastic residue accumulation, known as white pollution, which threatens long-term soil health and agricultural sustainability.

- The market faces significant hurdles, primarily the environmental impact of white pollution from the accumulation of plastic residues, which can reach contamination rates of over 50% by weight. This degradation of soil health has led to stringent legislative frameworks that threaten conventional product lines.

- While the transition to biodegradable alternatives offers a solution, their high cost remains a substantial barrier, with prices often two to three times higher than their polyethylene counterparts. This price differential, coupled with high agricultural input costs for other materials, slows adoption in price-sensitive regions.

- Additionally, the industry is highly susceptible to raw material price volatility and supply chain vulnerabilities, as disruptions in hydrocarbon processing or logistics can lead to sharp price spikes and inventory shortages during critical planting seasons.

Exclusive Technavio Analysis on Customer Landscape

The agricultural mulch films market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the agricultural mulch films market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Agricultural Mulch Films Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, agricultural mulch films market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

A.A. Politiv - The portfolio includes protective agricultural films, featuring high-barrier Totally Impermeable Films (TIF) and biodegradable options designed to optimize crop yields and support sustainable agriculture.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A.A. Politiv

- Ab Rani Plast Oy

- Achilles Corp.

- Armando Alvarez Group

- Barbier Group

- BASF SE

- Berry Global Inc.

- Daios Plastics S.A

- Dow Chemical Co.

- Exxon Mobil Corp.

- Imaflex Inc.

- Kingfa SCI. and TECH. Co. Ltd.

- Mitsubishi Chemical Grp.

- Novamont S.p.A.

- PLASTIKA KRITIS SA

- POLIFILM GmbH

- RKW SE

- SOTRAFA S.A

- Trioplast Industrier AB

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Agricultural mulch films market

- In August 2024, Berry Global Group Inc. initiated a strategic partnership with a major agricultural technology firm in North America to deploy smart mulch film solutions aimed at optimizing yield in water-scarce regions.

- In November 2024, the United Nations Environment Programme released a critical assessment on soil health, explicitly identifying agricultural plastics as a top-tier contaminant in global arable lands.

- In February 2025, Dow Inc. unveiled a novel resin formulation for ultra-thin, high-strength multi-layer mulch films, enabling a 30% reduction in thickness without compromising tear resistance.

- In March 2025, a comprehensive economic analysis by the Global Agricultural Economics Association revealed that high costs have stagnated adoption rates for biodegradable mulch films in emerging markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Agricultural Mulch Films Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 287 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.6% |

| Market growth 2026-2030 | USD 2346.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.2% |

| Key countries | China, India, Japan, Australia, South Korea, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, US, Canada, Mexico, Brazil, Argentina, Colombia, South Africa, Israel, Turkey, Saudi Arabia and UAE |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The agricultural mulch films market is evolving from a commodity-driven industry to one defined by advanced polymer chemistry and sustainability mandates. The development of films using polybutylene adipate terephthalate (pbat) and other soil-biodegradable polymers is reshaping product portfolios, forcing a strategic pivot away from conventional low-density polyethylene (ldpe).

- This transition is driven by the need to mitigate soil microbial diversity loss and address microplastic contamination. Innovations in resin formulation and multi-layer co-extrusion now allow for spectrally selective films that actively manage photosynthetically active radiation (par) and root zone temperature to influence crop morphogenesis. These technologies serve as powerful agronomic tools, offering enhanced crop protection benefits.

- For instance, new resin formulations have enabled the production of films that are up to 30% thinner, significantly reducing material consumption and aligning with circular economy models. Boardroom decisions now center on balancing investment in R&D for such high-performance films against the persistent demand for cost-effective cultivation solutions.

What are the Key Data Covered in this Agricultural Mulch Films Market Research and Growth Report?

-

What is the expected growth of the Agricultural Mulch Films Market between 2026 and 2030?

-

USD 2.35 billion, at a CAGR of 6.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Open farm, and Greenhouse), Type (Conventional, and Biodegradable), Product Type (Black, and Transparent) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerated transition toward biodegradable and soil-degradable film solutions, Environmental degradation and challenge of white pollution

-

-

Who are the major players in the Agricultural Mulch Films Market?

-

A.A. Politiv, Ab Rani Plast Oy, Achilles Corp., Armando Alvarez Group, Barbier Group, BASF SE, Berry Global Inc., Daios Plastics S.A, Dow Chemical Co., Exxon Mobil Corp., Imaflex Inc., Kingfa SCI. and TECH. Co. Ltd., Mitsubishi Chemical Grp., Novamont S.p.A., PLASTIKA KRITIS SA, POLIFILM GmbH, RKW SE, SOTRAFA S.A and Trioplast Industrier AB

-

Market Research Insights

- The agricultural mulch films market is defined by a dynamic shift toward advanced plasticulture solutions and sustainable inputs. The adoption of high-performance mulch films is accelerating, as they have been shown to reduce water usage by up to 20% in arid regions, a critical factor for resource efficiency.

- Precision agriculture integration is driving demand for smart mulch film solutions that are compatible with modern irrigation, enhancing crop protection benefits. This evolution from basic ground covers to sophisticated agronomic tools is evident in the development of films that optimize plant physiological processes.

- The market is also shaped by a push for circularity, with advanced collection programs successfully reclaiming over 10,000 tons of conventional film in a single fiscal year, reflecting robust industry responses to circular economy demands. This focus on both performance and sustainability is reshaping procurement strategies across the sector.

We can help! Our analysts can customize this agricultural mulch films market research report to meet your requirements.

RIA -

RIA -