Biodegradable Polymers Market Size 2025-2029

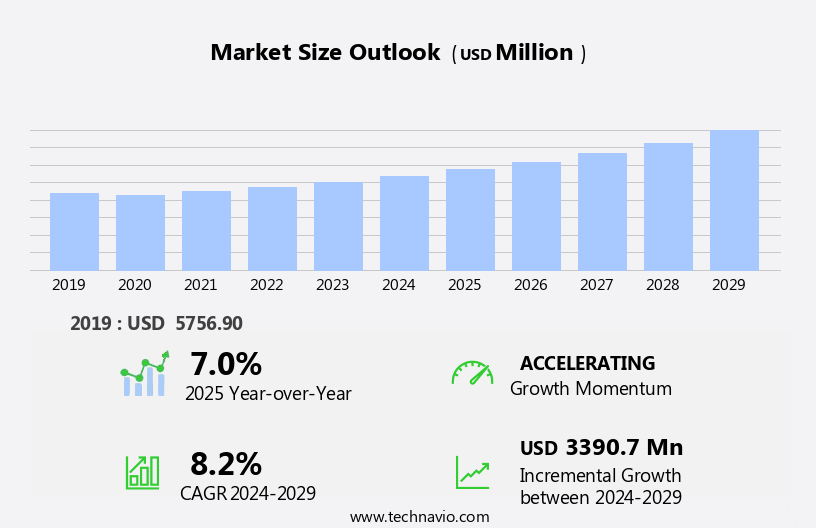

The biodegradable polymers market size is forecast to increase by USD 3.39 billion, at a CAGR of 8.2% between 2024 and 2029.

- The market is driven by the increasing global focus on environmental sustainability, leading to a rise in demand for eco-friendly alternatives to traditional plastics. Key players in this market, such as BASF SE, Corbion, and Novamont, are responding to this trend by launching innovative biodegradable polymer solutions. For instance, BASF SE's Ecoflex brand offers polylactide (PLA) for various applications, including packaging, while Corbion's Luminy PLA is used in food packaging and automotive industries. However, performance limitations pose a significant challenge to the market's growth. Biodegradable polymers often struggle to match the strength, durability, and cost-effectiveness of conventional plastics. Addressing these performance issues will require ongoing research and development efforts.

- Additionally, the market faces challenges related to scalability and affordability, as producing biodegradable polymers on a large scale can be complex and costly. Despite these challenges, the potential for biodegradable polymers to reduce plastic waste and minimize environmental impact makes them an attractive alternative for businesses seeking to align with sustainability initiatives. Companies that can successfully address performance limitations and scale up production will be well-positioned to capitalize on this growing market opportunity. Biodegradable plastics derived from renewable resources, like PLA and PBS, are gaining traction in various sectors, including food packaging and consumer goods.

What will be the Size of the Biodegradable Polymers Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market is experiencing significant growth, driven by increasing sustainability standards and consumer perception towards eco-friendly alternatives. The competitive landscape analysis reveals a diverse range of players, including those specializing in bio-based resins, such as polyvinyl chloride (PVC), polyamide (PA), polyethylene (PE), and polyester (PET). Government regulations are also playing a crucial role in boosting bioplastic adoption, particularly in industries like blow molding and injection molding. Bio-based colorants, lubricants, fillers, and processing technologies are key innovation areas, offering investment opportunities for businesses.

- However, market restraints include higher production costs compared to conventional plastics. The bioplastic market is segmented by industry applications and regions, with the future outlook showing promising growth in various sectors. Polypropylene (PP) and PVC are prominent traditional plastic markets facing increasing competition from bioplastics. The applications of bioplastics extend beyond packaging, with potential in textiles, automotive, and construction industries.

How is this Biodegradable Polymers Industry segmented?

The biodegradable polymers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Method

- Injection molding

- Extrusion

- Blow molding

- Thermoforming

- Others

- Industry Application

- Packaging

- Agriculture

- Biomedical

- Textiles

- Others

- Type

- PLA

- Starch-based polymers

- PHA

- PBS

- Others

- Geography

- North America

- US

- Europe

- Belgium

- France

- Germany

- The Netherlands

- APAC

- China

- Japan

- South Korea

- Thailand

- South America

- Brazil

- Rest of World (ROW)

- North America

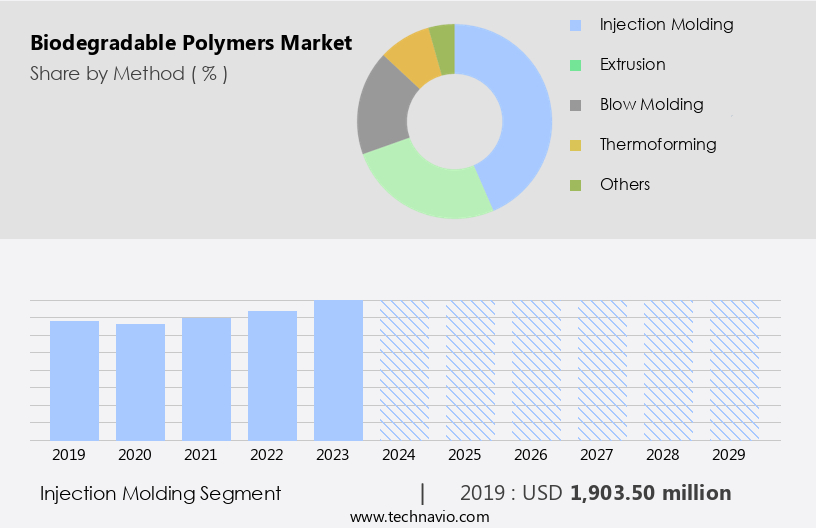

By Method Insights

The injection molding segment is estimated to witness significant growth during the forecast period. Injection molding is a prominent process in the market, known for producing complex, high-precision components at scale. This method involves injecting molten biodegradable polymer into a mold cavity, where it cools and solidifies into the desired shape. Suitable for high-volume production, injection molding ensures consistent quality and dimensional accuracy. Biodegradable polymers, such as polylactic acid (PLA) and polybutylene succinate (PBS), are frequently utilized due to their favorable flow characteristics and thermal behavior. These materials can be efficiently molded into intricate geometries, making them suitable for applications demanding both aesthetic and functional precision.

Biopolymer synthesis through microbial fermentation and polymer blends are key trends driving market growth. Biodegradable polymers offer improved mechanical properties, such as impact strength and flexural modulus, and can be recycled through mechanical, chemical, or composting processes. PLA, for instance, has a relatively low carbon footprint and is compostable under specific conditions, making it a popular choice for biodegradable bottles and films. PBS, on the other hand, exhibits excellent barrier properties, making it suitable for use in biodegradable bags and mulch films. Biodegradable coatings and bioplastic certification schemes ensure consumer trust and compliance with bioplastic standards.

The industry's focus on reducing waste, improving biodegradation rates, and enhancing the mechanical and thermal properties of biodegradable polymers is expected to further fuel market expansion.

The Injection molding segment was valued at USD 1.9 billion in 2019 and showed a gradual increase during the forecast period.

The Biodegradable Polymers Market is expanding with the integration of biobased fillers that enhance material strength while maintaining sustainability. The use of biobased lubricants improves processing efficiency in bioplastic processing, optimizing manufacturing techniques. Addressing bioplastic production costs is critical for wider adoption, with advancements reducing expenses and increasing feasibility. Detailed bioplastic market segmentation provides insights into demand across various sectors. The market's applications by industry include packaging, automotive, and healthcare, driving innovation and eco-friendly solutions. Regional demand variations influence applications by region, with Europe and North America leading in sustainability initiatives.

The Biodegradable Polymers Market is growing with increased focus on polyhydroxyalkanoates (PHAs), which offer eco-friendly alternatives in packaging and medical applications. Innovations in plant-based polymers drive sustainability, reducing reliance on traditional petrochemicals. Advanced chemical recycling methods enhance polymer recovery and reuse, minimizing environmental impact.

The circular economy concept is increasingly influencing the bioplastics industry, with a focus on reducing waste and promoting sustainable packaging. Innovations in bioplastics, such as biodegradable films and biodegradable plastics with enhanced oxygen permeability, are driving market expansion. Bioplastics in agriculture, particularly biodegradable mulch films, are also gaining attention due to their potential to reduce plastic waste and improve crop yields. In summary, the market is witnessing significant growth, driven by advancements in biopolymer synthesis, recycling technologies, and the increasing demand for sustainable packaging solutions. Injection molding remains a crucial processing method for manufacturing high-quality, biodegradable components, while PLA and PBS continue to dominate the market due to their favorable properties.

Regional Analysis

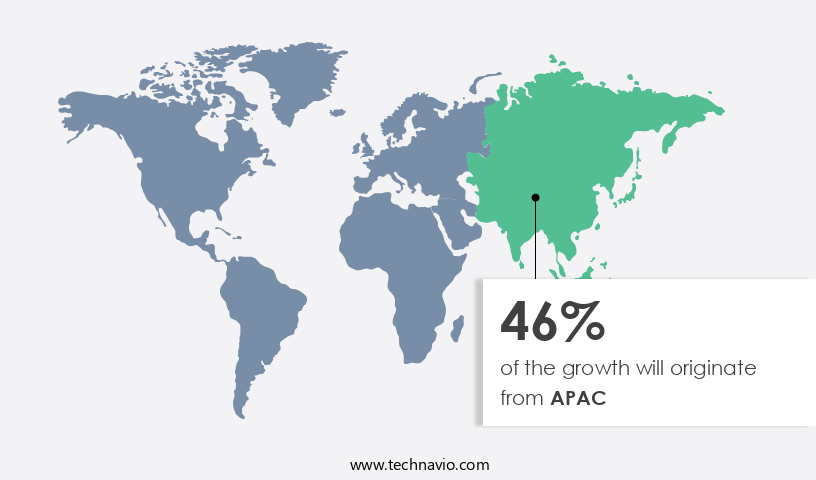

APAC is estimated to contribute 46% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The Asia-Pacific region is leading the global bioplastics market, driven by strategic initiatives and innovations in sustainable materials. India, in particular, is taking a prominent role in this transition. On October 16, 2024, India inaugurated its first Biopolymer Demonstration Facility in Jejuri, Pune, developed by Praj Industries. This facility focuses on producing biodegradable polylactic acid (PLA) bioplastics, supported by the national government. This initiative aligns with India's ambition to expand its bioeconomy, which reached a significant valuation milestone in 2023. The APAC market is witnessing a strong commitment to environmental stewardship, with several countries advancing policies and technologies to reduce plastic pollution and foster a circular economy.

Bio-based polymers, such as PLA, are gaining popularity due to their lower carbon footprint and biodegradable properties. These polymers are used in various applications, including food packaging, consumer goods, and biodegradable bottles. Innovations in biodegradable films, biodegradable coatings, and bioplastics in agriculture are also contributing to the market's evolution. The use of renewable resources in bioplastic production is a key trend, as is the focus on improving mechanical properties, such as impact strength, flexural modulus, and tensile strength, as well as thermal properties and barrier properties.

The market is also witnessing the emergence of chemical and mechanical recycling, composting, and compostability certification. ASTM D6400 and other bioplastic standards play a crucial role in ensuring product quality and consistency. The market's future looks promising, with ongoing research and development efforts aimed at enhancing the performance and sustainability of bioplastics. Polybutylene succinate (PBS) and other biodegradable polymers are expected to gain traction due to their unique properties and potential applications. Overall, the bioplastics market is an exciting and dynamic space, driven by a growing demand for sustainable alternatives to fossil-based plastics.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Biodegradable Polymers market drivers leading to the rise in the adoption of Industry?

- The increasing awareness and concern for environmental issues serve as the primary catalyst for market growth. The market is driven by growing environmental concerns over plastic waste and its long-term impact on ecosystems. In 2024, an estimated 220 million tonnes of plastic waste were generated worldwide, with around one-third, equivalent to 69.5 million tonnes, being mismanaged. This has led to significant pollution of land, marine, and atmospheric environments. The low global recycling rate, which remains at approximately 9 percent, exacerbates the issue, resulting in the accumulation of plastics in ecosystems where they persist for centuries. Biodegradable polymers offer a sustainable alternative to conventional plastics, with the ability to decompose naturally through mechanical recycling or composting.

- Two common biodegradable polymers are polybutylene succinate (PBS) and biodegradable films. PBS, with a melting point of 115-125°C, is a biodegradable aliphatic polyester derived from renewable resources. Biodegradable films, on the other hand, are used for various applications, including agricultural mulch films. Innovation in bioplastics continues to advance, with research focusing on improving the biodegradation rate and reducing the composting time of these materials. As businesses and consumers increasingly prioritize sustainability, the demand for biodegradable polymers in applications such as packaging is expected to grow.

What are the Biodegradable Polymers market trends shaping the Industry?

- The focus on new product launches is a prevailing market trend. It is essential for businesses to prioritize this area to stay competitive and innovative. The market is witnessing significant growth due to the increasing demand for eco-friendly and sustainable solutions. One key trend in this market is the development of high-performance biodegradable polymers that offer superior properties such as impact strength and oxygen permeability. Fiber reinforcement and bioplastic additives are being used to enhance the performance of biodegradable polymers, making them suitable for various applications, particularly in the packaging industry. Bioplastic recycling is another area of focus in the market. Companies are investing in research and development to create effective recycling solutions for bioplastics. Bio-based polymers, such as polylactic acid (PLA), are gaining popularity due to their biodegradability and reduced carbon footprint.

- These polymers are being used extensively in food packaging applications, where the need for sustainable and biodegradable solutions is high. Leading companies in the market are introducing innovative biodegradable polymer solutions to cater to the evolving demands of industries. For instance, Lubrizol Life Science Beauty recently launched Carbopol Fusion S-20, a sustainable and inherently biodegradable Carbopol polymer for skin cleansing and hair care applications. This rheology modifier is derived from renewable starch and is free from GMOs, ethylene oxide, and PEGs. It aligns with all 12 Principles of Green Chemistry and offers a low carbon footprint, making it a preferred choice for environmentally conscious consumers.

How does Biodegradable Polymers market face challenges during its growth?

- The market faces performance limitations, which pose a significant challenge to its broader adoption in various industries. Biodegradable polymers, derived from renewable resources, provide environmental benefits, but they often fail to match the mechanical and functional properties of conventional plastics like polyethylene and polypropylene. Biodegradable polymers such as polylactic acid (PLA) and bio-based composites, including compostable polymers and biodegradable coatings, exhibit lower tensile strength, reduced flexibility, and limited barrier properties. These deficiencies hinder their effectiveness in applications demanding durability, impact resistance, or long-term preservation, such as food packaging, automotive components, and medical devices. For instance, PLA, a widely used biodegradable polymer, is known for its brittleness and relatively low thermal resistance.

- The market's growth is also influenced by the increasing demand for biodegradable consumer goods, bioplastic certification, and bioplastic standards that support the circular economy. Despite these challenges, ongoing research and development efforts aim to improve the performance characteristics of biodegradable polymers, making them a viable alternative to conventional plastics. The market is expected to continue its growth trajectory due to the increasing demand for sustainable and eco-friendly solutions. Companies are focusing on developing high-performance biodegradable polymers and effective recycling solutions to cater to the evolving demands of various industries. The use of bio-based polymers, such as polylactic acid, is gaining popularity, particularly in the packaging industry. The market is expected to witness significant growth in the coming years, driven by the increasing awareness of sustainability and the need for eco-friendly solutions.

Exclusive Customer Landscape

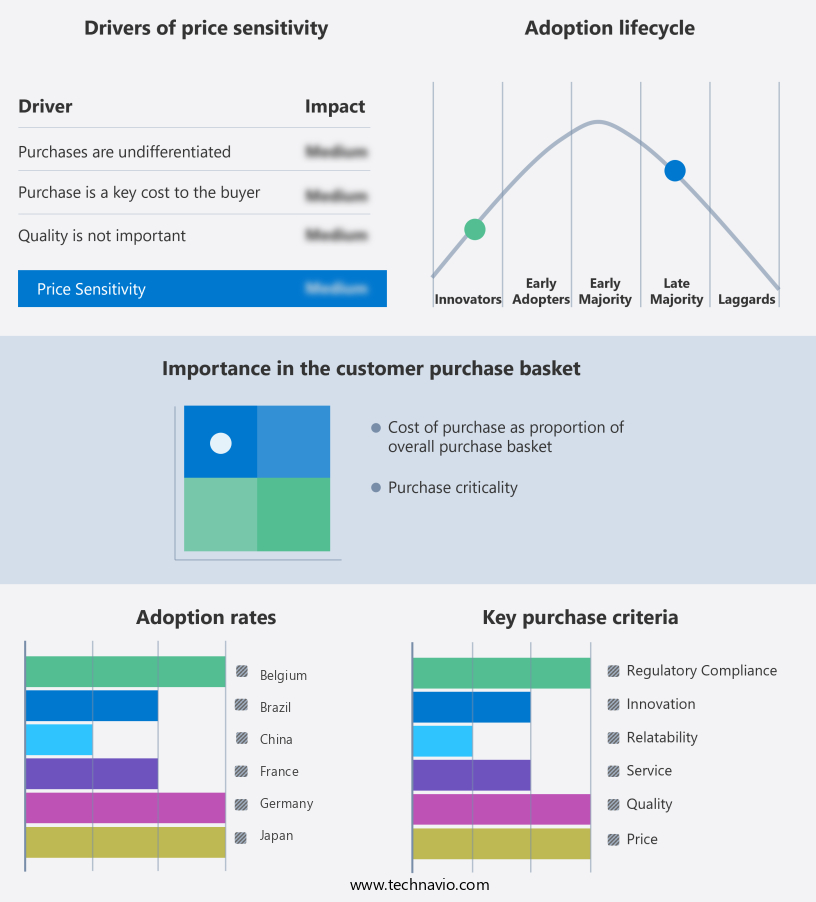

The biodegradable polymers market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the biodegradable polymers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, biodegradable polymers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BASF SE - The company specializes in the production and supply of biodegradable polymers, specifically ecoflex and ecovio.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BASF SE

- BioLogiQ Inc.

- Biome Bioplastics Ltd.

- Corbion N.V.

- DuPont de Nemours Inc.

- Evonik Industries AG

- Fkur Kunststoff GmbH

- Jiangmen Xinshuo New Materials Co. Ltd

- Kaneka Corp.

- LG Chem Ltd.

- Mitsubishi Chemical Group Corp.

- Mitsui Chemicals Inc.

- NatureWorks LLC

- Novamont S.p.A.

- Solvay SA

- Trinseo PLC

- Xiamen Changsu Industrial Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Biodegradable Polymers Market

- In January 2024, BASF SE, a leading chemical producer, announced the commercial production of its new biodegradable polymer, Ecoflex F, at its site in Ludwigshafen, Germany. This development marks a significant stride towards sustainable plastic solutions, as Ecoflex F can decompose in industrial composting facilities within six months (BASF SE, 2024).

- In March 2025, Danish biotech company Novozymes and American chemical company DuPont announced a strategic partnership to develop and commercialize biodegradable polymers using microbial enzymes. This collaboration aims to reduce plastic waste by enhancing the biodegradability of plastics, thereby addressing the growing environmental concerns (DuPont, 2025).

- In May 2024, LG Chem, a South Korean chemical company, secured a USD 100 million investment from SK Innovation to expand its biodegradable polymer production capacity. This investment will enable LG Chem to increase its market share and meet the rising demand for eco-friendly alternatives to traditional plastics (LG Chem, 2024).

Research Analyst Overview

The market continues to evolve, driven by the increasing demand for sustainable alternatives to traditional fossil fuel-based plastics. Biodegradable polymers, derived from renewable resources, offer numerous advantages such as reduced carbon footprint, biodegradability, and improved mechanical properties. Bioplastic additives play a crucial role in enhancing the performance of biodegradable polymers. Impact strength and fiber reinforcement are essential properties that can be enhanced through the addition of these additives. Bioplastic recycling is another area of focus, with chemical, mechanical, and composting methods being explored to extend the lifecycle of biodegradable polymers. Biodegradable plastics find extensive applications in various sectors, including food packaging, bioplastics in agriculture, and consumer goods.

Biodegradable bottles, biodegradable bags, and biodegradable coatings are some of the popular applications. Biopolymer synthesis techniques such as microbial fermentation and polymer blends are continually being innovated to improve production efficiency and reduce costs. Bioplastic market growth is driven by the increasing awareness of environmental issues and the need for sustainable solutions. Polylactic acid (PLA) and polyhydroxyalkanoates (PHA) are some of the commonly used bio-based polymers. Oxygen permeability and barrier properties are critical factors that determine the suitability of biodegradable polymers for various applications. Biodegradable polymers are subjected to various certification and standardization processes, including compostability certification, bioplastic certification, and environmental impact assessment.

The circular economy concept is gaining traction, with the focus on reducing waste and promoting the reuse and recycling of biodegradable polymers. Biodegradable polymers are finding increasing use in agriculture, particularly in mulch films and biodegradable coatings for seeds. The ongoing research and development in biopolymer synthesis and biodegradation technologies are expected to drive the growth of the market. The mechanical properties of biodegradable polymers, including tensile strength, flexural modulus, and melting point, are continually being optimized to meet the requirements of various applications. Biodegradable films are gaining popularity due to their excellent barrier properties and biodegradability. Innovation in bioplastics is a continuous process, with researchers exploring new methods for biopolymer synthesis, biodegradation, and recycling.

The future of biodegradable polymers looks promising, with the potential to replace fossil fuel-based plastics and contribute to a more sustainable future.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Biodegradable Polymers Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

253 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.2% |

|

Market growth 2025-2029 |

USD 3.39 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.0 |

|

Key countries |

China, US, Japan, Thailand, South Korea, France, Germany, Brazil, Belgium, and The Netherlands |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Biodegradable Polymers Market Research and Growth Report?

- CAGR of the Biodegradable Polymers industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the biodegradable polymers market growth of industry companies

We can help! Our analysts can customize this biodegradable polymers market research report to meet your requirements.

RIA -

RIA -