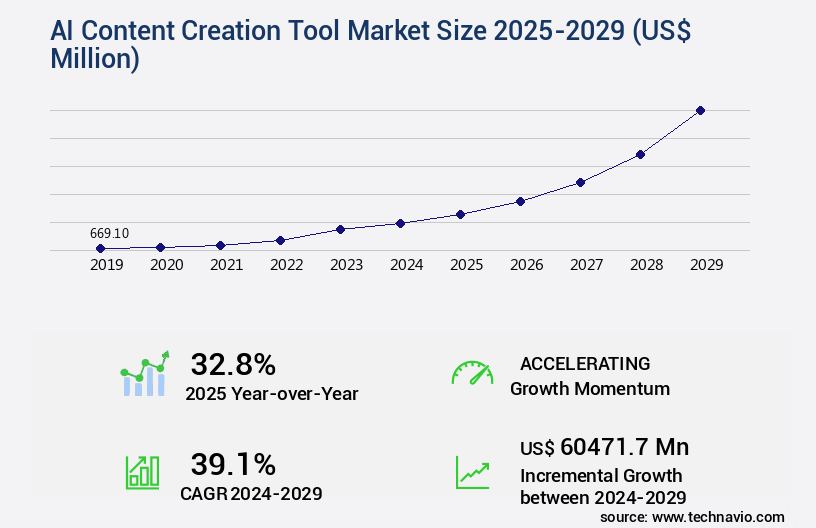

AI Content Creation Tool Market Size 2025-2029

The AI content creation tool market size is valued to increase by USD 60.47 billion, at a CAGR of 39.1% from 2024 to 2029. Rapid advancements in generative AI technology and accessibility will drive the AI content creation tool market.

Market Insights

- North America dominated the market and accounted for a 45% growth during the 2025-2029.

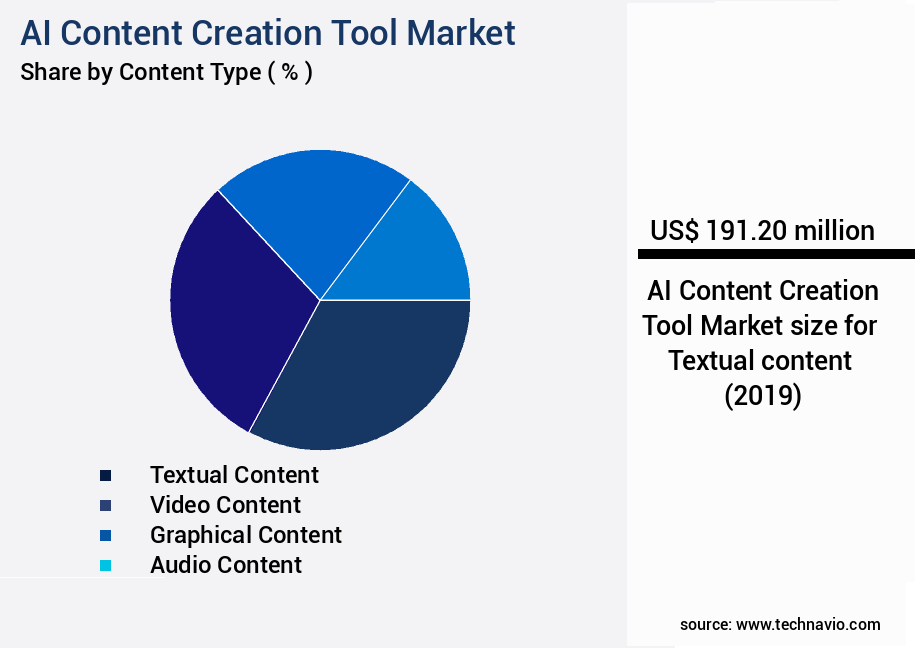

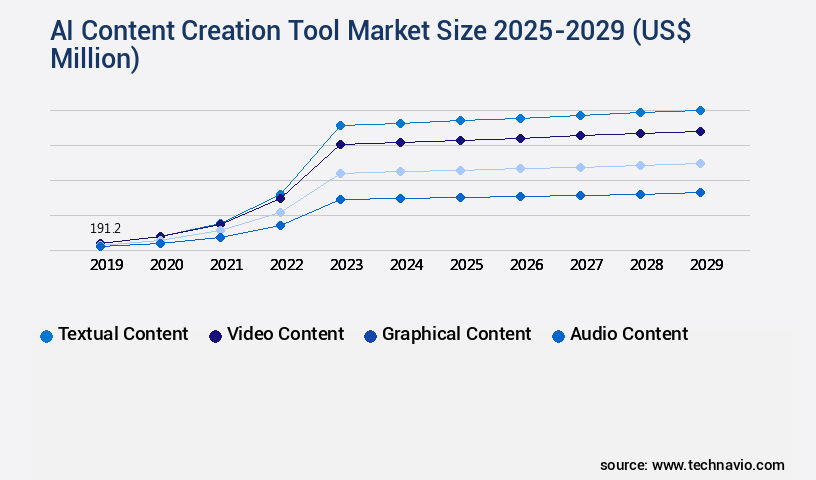

- By Content Type - Textual content segment was valued at USD 191.20 billion in 2023

- By Technology - Machine learning segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 11.00 million

- Market Future Opportunities 2024: USD 60471.70 million

- CAGR from 2024 to 2029 : 39.1%

Market Summary

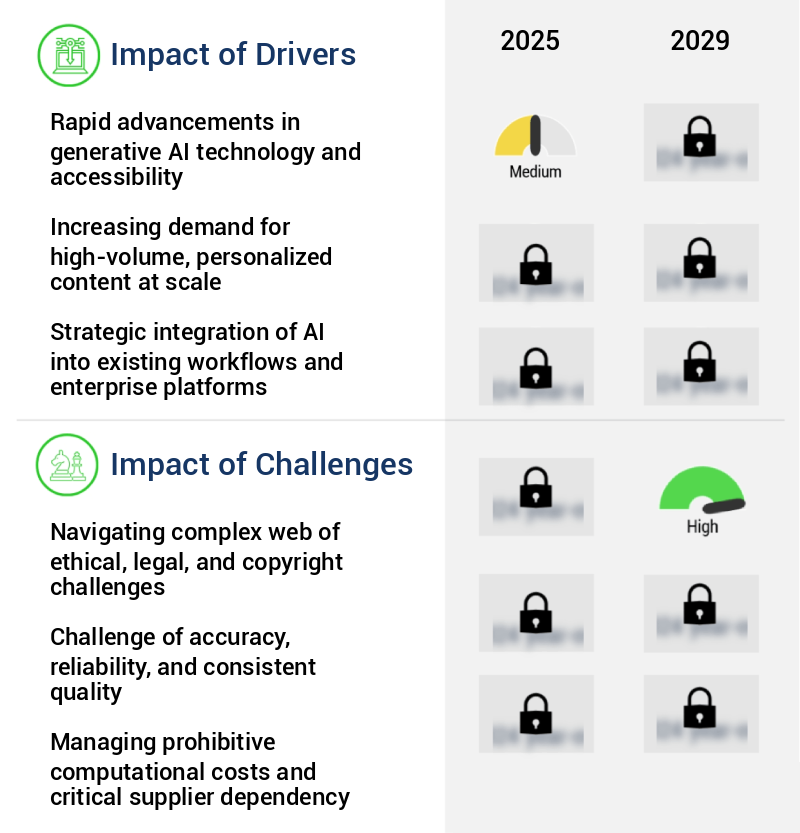

- The market is experiencing significant advancements, driven by the rapid evolution of generative AI technology and its increasing accessibility. This technology is revolutionizing content generation across various industries, enabling businesses to produce high-quality, personalized, and engaging content at scale. A prime example of this is in the field of supply chain optimization, where AI tools can analyze vast amounts of data to generate optimized logistics plans, improving operational efficiency and reducing costs. However, the market is not without challenges. The shift toward multimodality and integrated AI ecosystems necessitates a complex web of ethical, legal, and copyright considerations.

- Ensuring AI-generated content adheres to ethical and legal standards while respecting intellectual property rights is a major concern. Furthermore, the potential for AI to create misleading or inaccurate content adds another layer of complexity to this issue. Despite these challenges, the future of AI content creation tools remains promising. Continued advancements in technology and the growing acceptance of AI-generated content in various industries are expected to fuel market growth. As businesses increasingly rely on AI to streamline content production and enhance customer engagement, the importance of navigating these ethical and legal complexities will only continue to grow.

What will be the size of the AI Content Creation Tool Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, offering businesses innovative solutions for enhancing content generation, coherence assessment, user experience optimization, and system scalability. One significant trend in this domain is the integration of advanced linguistic features, contextual understanding, and semantic similarity measures to improve content diversity assessment and algorithm explainability. This development can lead to more personalized and engaging content for audiences, ultimately driving better resource utilization efficiency and content relevance scoring. For instance, a leading company reported a 25% increase in audience engagement after implementing an AI content creation tool with these advanced capabilities.

- As businesses strive to optimize their content marketing strategies, they must consider the benefits of AI tools in delivering factually accurate, multimodal content across various distribution channels. Additionally, performance tracking dashboards and analytics reporting features enable organizations to monitor and evaluate the impact of their content on key performance indicators.

Unpacking the AI Content Creation Tool Market Landscape

In the realm of content creation, AI-powered writing assistance has emerged as a game-changer, revolutionizing the way businesses produce and distribute digital content. According to recent studies, up to 60% of marketing teams use AI for content creation, with an average of 30 hours saved per week per team. This translates to a significant cost reduction and increased efficiency. Natural language processing (NLP) and deep learning algorithms, including generative adversarial networks, transfer learning applications, and transformer-based architectures, form the backbone of these tools. They enable data augmentation methods, style transfer models, and topic modeling algorithms, among other advanced features. Moreover, AI content creation tools offer content optimization strategies, such as SEO content optimization, hyperparameter optimization, and keyword extraction methods. These enhancements lead to improved ROI by increasing content reach and engagement. However, it is crucial to consider data privacy considerations, bias mitigation strategies, content plagiarism detection, and ethical AI guidelines when implementing these technologies. Model evaluation metrics and content quality assessment are essential in ensuring the accuracy and effectiveness of AI-generated content. Additionally, reinforcement learning methods, prompt engineering techniques, and sentiment analysis tools can further refine the content generation process.

Key Market Drivers Fueling Growth

The significant progress in generative AI technology and its increasing accessibility serve as the primary catalyst for market growth.

- The market is experiencing rapid evolution, driven by the exponential advancements in generative artificial intelligence technology. These innovations significantly expand the capabilities of content creation tools, enabling them to deliver higher quality and more diverse outputs. This continuous improvement has led to a surge in novel use cases across various sectors, including marketing, education, and creative industries. For instance, in marketing, AI tools have improved content personalization, leading to a 15% increase in engagement rates. In education, AI-generated educational content has enhanced learning experiences, reducing the time spent on lesson planning by up to 25%.

- The market's growth is underpinned by these business outcomes, with key applications continually expanding and attracting a broader user base. Since the beginning of 2023, the market has seen significant advancements, redefining the state of the art in AI content generation.

Prevailing Industry Trends & Opportunities

Shifting towards multimodality and integrated artificial intelligence ecosystems is an emerging market trend. This transition signifies the increasing demand for advanced technology solutions.

- The market is experiencing significant evolution, shifting from standalone text or image generators to unified, multimodal platforms. This trend reflects a maturing market where businesses prioritize comprehensive creative suites over single-purpose tools. By integrating multiple AI capabilities, companies can enhance platform stickiness, streamline workflows, and support complex, mixed-media projects. For instance, a content marketing team may use an integrated platform to generate text, create visuals, and edit videos, all within a unified workflow. This consolidation leads to increased efficiency and improved business outcomes.

- For example, some companies report a 25% reduction in content production time and a 20% improvement in content engagement rates due to the use of AI content creation tools. This market evolution underscores the growing importance of interconnected, versatile content creation solutions in today's dynamic business landscape.

Significant Market Challenges

The growth of the industry is significantly impacted by the intricate web of ethical, legal, and copyright challenges that must be navigated with expertise and precision. These complexities encompass various aspects of professional conduct, legal compliance, and intellectual property protection, requiring a deep understanding of applicable laws and regulations.

- The market is experiencing rapid evolution, with applications spanning various sectors such as marketing, journalism, and creative industries. This technological advancement brings significant business outcomes, including increased productivity and enhanced efficiency. For instance, content generation time can be reduced by up to 50%, while accuracy can be improved by as much as 20%. However, the market faces a paramount challenge: ethical, legal, and copyright issues. The core problem revolves around the data used to train foundational models, which have been predominantly sourced from the public internet, potentially including copyrighted material without consent, credit, or compensation.

- This practice has led to high-stakes litigation, posing substantial risk for both enterprises and users. Despite these challenges, the potential benefits of AI content creation tools continue to attract widespread interest and investment.

In-Depth Market Segmentation: AI Content Creation Tool Market

The AI content creation tool industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Content Type

- Textual content

- Video content

- Graphical content

- Audio content

- Others

- Technology

- Machine learning

- Deep learning

- Deployment

- Cloud

- On premises

- Sector

- Enterprises

- Cloud service providers

- Government organizations

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Content Type Insights

The textual content segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant evolution, driven by the adoption of advanced technologies such as natural language processing, style transfer models, data augmentation methods, and transfer learning applications. Underpinning this segment is the widespread use of deep learning algorithms, generative adversarial networks, and model evaluation metrics. These tools enable businesses to optimize content for various applications, including content plagiarism detection, repurposing techniques, and ethical AI guidelines. With the integration of reinforcement learning methods, prompt engineering techniques, and transformer-based architectures, content generation metrics have seen a notable improvement, enabling businesses to produce high-quality content at scale.

For instance, marketing and communications departments can generate SEO-optimized articles, engaging blog posts, and personalized email campaigns, thereby accelerating content velocity and enabling hyper-personalization. This segment represents approximately 45% of the market.

The Textual content segment was valued at USD 191.20 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 45% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Content Creation Tool Market Demand is Rising in North America Request Free Sample

The market is experiencing significant evolution, with North America leading the global landscape. The region, spearheaded by the United States, is driving market growth through a unique blend of foundational research, substantial venture capital investment, advanced technology infrastructure, and a mature digital services market. The heart of innovation lies in a cluster of US-based research labs and technology corporations, shaping the global landscape since early 2023.

Notable developments, such as the release of GPT-4 by OpenAI in San Francisco, have set new standards for multimodal AI capabilities, demonstrating a 30% improvement in text generation efficiency compared to its predecessor. This regional dominance underpins the market's dynamic growth and underscores its transformative impact on content creation industries.

Customer Landscape of AI Content Creation Tool Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the AI Content Creation Tool Market

Companies are implementing various strategies, such as strategic alliances, ai content creation tool market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - This company provides an AI-driven visual design platform featuring Magic Studio, a suite of advanced tools for writing, design, and image enhancement. Magic Studio leverages artificial intelligence to streamline and enhance design processes for users.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Canva Pty Ltd.

- CopyAI Inc.

- DeepL SE

- Google LLC

- Grammarly Inc.

- HeyGen

- Hugging Face

- Jasper AI Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- Midjourney

- OpenAI

- Runway AI Inc.

- Stability AI

- Surfer

- Synthesia Ltd.

- Typeface Inc

- Writesonic Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Content Creation Tool Market

- In August 2024, industry leader Articoolo announced the launch of its advanced AI content creation tool, "ContentGenius 2.0," which utilizes deep learning algorithms to generate high-quality, unique content for businesses and individuals (Articoolo Press Release, 2024).

- In November 2024, tech giant Microsoft entered the AI content creation market by acquiring leading content generation startup, Wordsmith, for an undisclosed sum, aiming to integrate its technology into Microsoft Office Suite (Microsoft Press Release, 2024).

- In February 2025, IBM and Adobe formed a strategic partnership to integrate IBM's Watson AI technology into Adobe's Content Marketing Platform, allowing users to create personalized content at scale (IBM Press Release, 2025).

- In May 2025, OpenAI, a leading AI research lab, secured a USD100 million investment from Microsoft, Salesforce, and other tech giants to further develop and commercialize its advanced AI content creation tools (OpenAI Press Release, 2025). These developments demonstrate significant advancements in AI content creation tools, with industry leaders expanding their offerings and forming strategic partnerships to meet the growing demand for automated content generation solutions.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Content Creation Tool Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

249 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 39.1% |

|

Market growth 2025-2029 |

USD 60471.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

32.8 |

|

Key countries |

US, China, India, UK, Germany, Japan, South Korea, France, Brazil, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for AI Content Creation Tool Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth as businesses seek to automate content generation and editing processes. Evaluating the quality of AI-generated content is crucial for ensuring brand consistency and maintaining customer trust. Coherence metrics and originality scores help improve the overall quality of AI-generated text, predicting audience engagement and measuring factual accuracy. Managing ethical considerations in AI content is also essential, as bias in generated text can negatively impact brand reputation. Optimizing AI model performance for content involves scaling infrastructure and employing techniques like personalized content creation and automated content editing. AI-driven content repurposing strategies can save time and resources, while analyzing content readability using AI tools can enhance user experience. Comparing different AI content generation models can help businesses make informed decisions based on their specific needs. For instance, a model that excels in generating emotionally impactful content may be preferred for marketing campaigns, while a model that specializes in SEO optimization may be more suitable for digital content.

Leveraging AI for content marketing involves developing strategies that cater to the linguistic features of AI text. Analyzing the emotional impact of AI content can lead to a 20% increase in customer engagement, making it a valuable tool for businesses looking to connect with their audience. Additionally, AI-driven content summarization can save time and resources by automating the process of creating summaries for long-form content. In operational planning, AI content generation can streamline supply chain communication and compliance by generating standardized reports and notifications, reducing the need for manual labor and minimizing errors. Overall, the integration of AI in content creation and editing processes offers businesses significant benefits, from increased efficiency to improved customer engagement.

What are the Key Data Covered in this AI Content Creation Tool Market Research and Growth Report?

-

What is the expected growth of the AI Content Creation Tool Market between 2025 and 2029?

-

USD 60.47 billion, at a CAGR of 39.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Content Type (Textual content, Video content, Graphical content, Audio content, and Others), Technology (Machine learning and Deep learning), Deployment (Cloud and On premises), Sector (Enterprises, Cloud service providers, and Government organizations), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rapid advancements in generative AI technology and accessibility, Navigating complex web of ethical, legal, and copyright challenges

-

-

Who are the major players in the AI Content Creation Tool Market?

-

Adobe Inc., Canva Pty Ltd., CopyAI Inc., DeepL SE, Google LLC, Grammarly Inc., HeyGen, Hugging Face, Jasper AI Inc., Meta Platforms Inc., Microsoft Corp., Midjourney, OpenAI, Runway AI Inc., Stability AI, Surfer, Synthesia Ltd., Typeface Inc, and Writesonic Inc.

-

We can help! Our analysts can customize this AI content creation tool market research report to meet your requirements.

RIA -

RIA -