Ai Gpu Orchestration Platforms Market Size and Growth Forecast 2026-2030

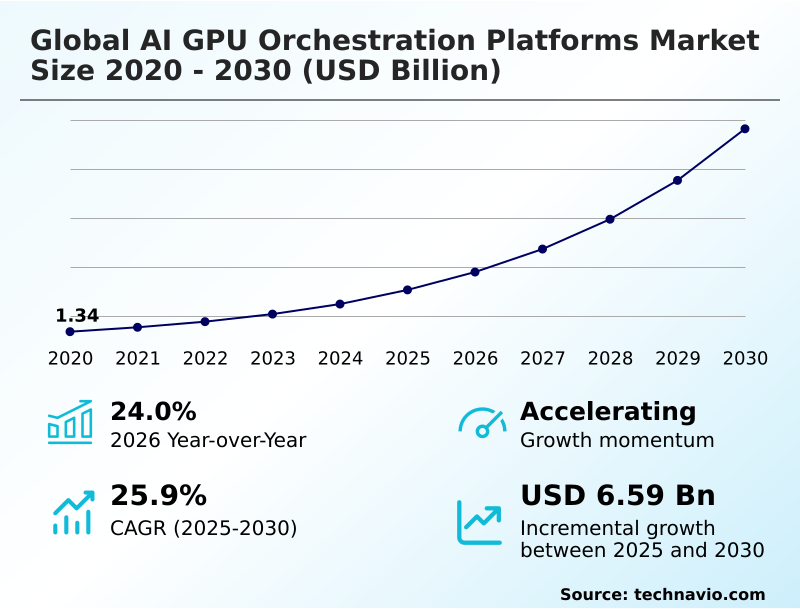

The Ai Gpu Orchestration Platforms Market size was valued at USD 3.05 billion in 2025 growing at a CAGR of 25.9% during the forecast period 2026-2030.

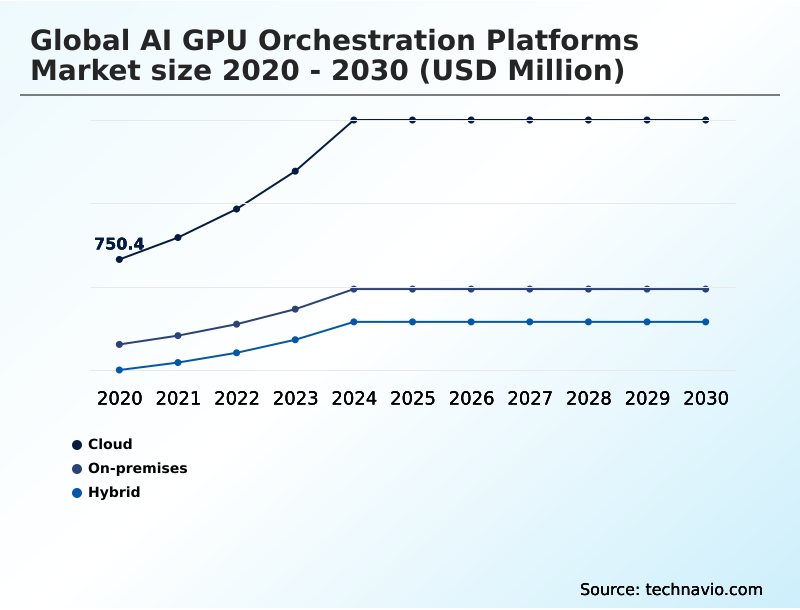

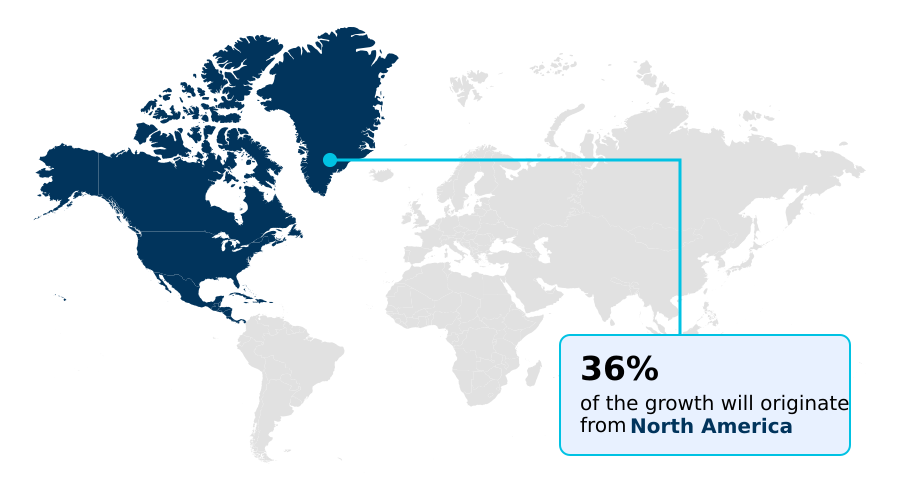

North America accounts for 36.3% of incremental growth during the forecast period. The Cloud segment by Deployment was valued at USD 1.40 billion in 2024, while the Tech companies segment holds the largest revenue share by End-user.

The market is projected to grow by USD 8.30 billion from 2020 to 2030, with USD 6.59 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Ai Gpu Orchestration Platforms Market Overview

The AI GPU orchestration platforms market is expanding as organizations seek to maximize the efficiency of computational resources, with North America leading incremental growth at 36.3% of the global opportunity. Demand is driven by the need for efficient GPU utilization in training and deploying complex models. This requires sophisticated job scheduling and resource allocation to manage generative AI workloads effectively. In practice, a financial services firm implementing an enterprise MLOps platform for algorithmic trading can use GPU partitioning to run hundreds of back-testing simulations concurrently on a shared cluster, reducing model validation cycles from days to hours. However, the market faces constraints from a severe talent deficit in skills related to machine learning infrastructure and distributed systems. This skills gap can impede the adoption of advanced tools for AI model lifecycle management, forcing some firms to rely on less optimal, manual processes for AI infrastructure management.

Drivers, Trends, and Challenges in the Ai Gpu Orchestration Platforms Market

Procurement decisions in the AI GPU orchestration platforms market are increasingly shaped by the need for managing multi-cloud GPU resources and achieving high GPU utilization rates. With the cloud segment representing a significantly larger share than on-premises deployments, enterprises are focused on optimizing the cost of AI training through sophisticated cost management for generative AI.

This involves not just acquiring compute power but implementing a hybrid cloud strategy for AI workloads that balances performance with expenditure. For example, an automotive manufacturer developing autonomous driving systems leverages platforms for orchestrating GPU resources for LLMs to run massive simulations. By using tools that simplify Kubernetes for data scientists, they can accelerate development cycles.

However, this process is constrained by security concerns, which drives the adoption of confidential computing in shared GPU clusters. The recent International Energy Agency guideline on reporting AI hardware power usage adds another layer of complexity, making energy efficient AI infrastructure management a key vendor qualification criterion and a central part of automating MLOps with GPU orchestration.

Migrating AI workloads across clouds remains a challenge, pushing vendors to improve tools for automated deployment of AI models.

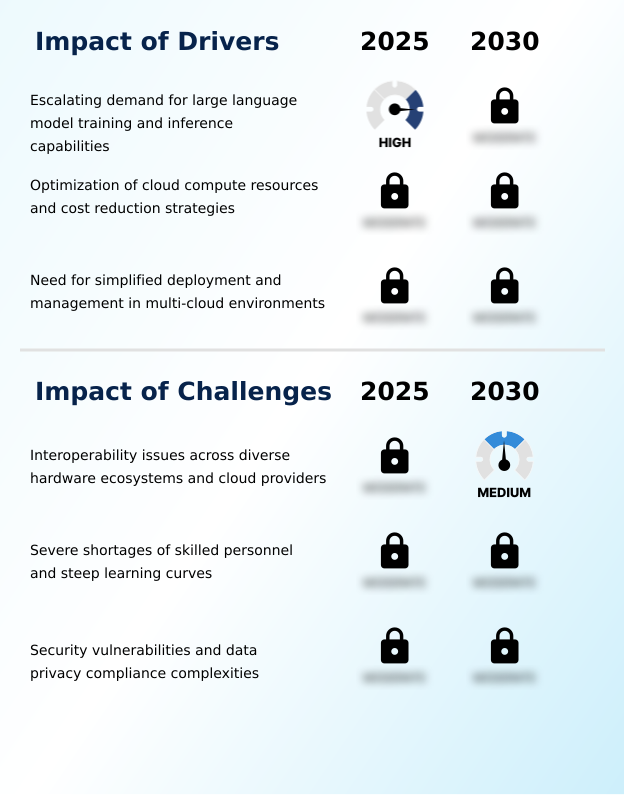

Primary Growth Driver: The escalating demand for training and inference capabilities for large language models is a primary driver for the AI GPU orchestration platforms market.

The primary force propelling the market is the escalating demand for computational power for large language model inference and training.

North America, contributing 36.32% of the market's incremental growth, exemplifies this trend as technology firms race to deploy sophisticated generative AI workloads. This demand necessitates solutions that enable efficient GPU utilization and scalable AI solutions.

Second, financial pressure to optimize cloud compute resources and reduce the total cost of ownership on expensive hardware drives adoption. Platforms offering fractional GPU sharing and automated resource provisioning allow enterprises to maximize hardware ROI.

Third, the complexity of modern multi-cloud and hybrid infrastructures makes a unified AI platform for AI model lifecycle management essential for simplifying deployment and ensuring operational consistency across environments.

Emerging Market Trend: The integration of edge computing with GPU orchestration platforms is emerging as a significant trend. This convergence addresses the need for real-time AI processing by reducing latency in industrial automation and autonomous systems.

Market evolution is characterized by the convergence of AI infrastructure management with decentralized architectures, reflecting a year-over-year growth of 24.0%. The integration of edge AI orchestration with centralized cluster management is critical for delivering real-time inference in applications like industrial automation. This requires platforms capable of managing heterogeneous hardware across a continuum of devices.

Another key development is the focus on sustainable operations, with energy-efficient scheduling becoming a standard feature to address environmental regulations and high operational costs. Advanced security protocols, including confidential computing for AI and zero-trust frameworks, are being implemented to protect sensitive data during processing, a crucial feature for securing multi-tenant AI environments in sectors like finance and healthcare.

This shift addresses the need for robust, secure, and efficient AI pipeline orchestration.

Key Industry Challenge: Interoperability issues across diverse hardware ecosystems and cloud providers present a key challenge affecting the growth of the AI GPU orchestration platforms industry.

Significant hurdles constrain the market, led by interoperability issues across a fragmented landscape of heterogeneous hardware and proprietary cloud APIs. This lack of standardization complicates AI workload migration and limits the effectiveness of a multi-cloud AI strategy.

A second major challenge is the severe shortage of skilled professionals with expertise in distributed systems and machine learning infrastructure, creating a steep learning curve for adoption. This talent deficit often prevents organizations from leveraging advanced features like confidential computing for AI. Finally, security vulnerabilities in multi-tenant environments and the complexities of data privacy compliance remain critical concerns.

The computational overhead required for robust security measures, such as securing multi-tenant AI environments, can degrade performance, presenting a difficult trade-off for enterprises seeking both efficiency and data protection.

Explore Full Market Dynamics Analysis Request Free Sample

Ai Gpu Orchestration Platforms Market Segmentation

The ai gpu orchestration platforms industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Deployment Segment Analysis

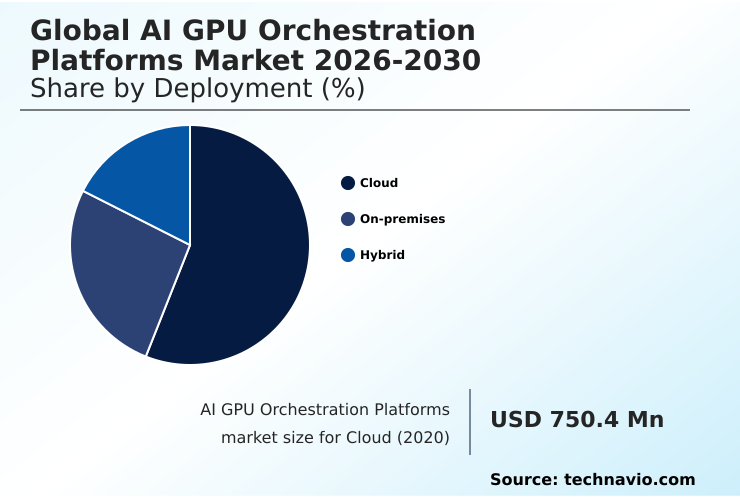

The cloud segment is estimated to witness significant growth during the forecast period.

The cloud deployment model dominates the AI GPU orchestration platforms market, accounting for over half of all deployments and exhibiting a year-over-year growth of 24.0%.

Enterprises are leveraging cloud environments for their inherent flexibility and the ability to employ dynamic scaling for variable AI workloads. This approach facilitates an operational expenditure model, crucial for managing the high costs of high-performance computing.

Cloud native AI/ML practices are becoming standard, with platforms providing serverless GPU computing and automated resource provisioning to minimize hardware idle time.

These solutions streamline AI workload migration and support complex multi-cloud AI strategy, integrating cost optimization algorithms to ensure financial efficiency and accelerate AI pipeline orchestration for faster time-to-market.

The Cloud segment was valued at USD 1.40 billion in 2024 and showed a gradual increase during the forecast period.

Ai Gpu Orchestration Platforms Market by Region: North America Leads with 36.3% Growth Share

North America is estimated to contribute 36.3% to the growth of the global market during the forecast period.

The geographic distribution of the AI GPU orchestration platforms market is led by North America, which accounts for 36.32% of incremental growth, driven by its concentration of hyperscale cloud providers and AI research hubs.

The region's advanced high-performance computing ecosystem provides an ideal environment for complex workload automation and MLOps integration.

APAC is the fastest-growing region, with a 27.2% CAGR, fueled by government-backed digital transformation initiatives and the expansion of domestic technology firms that require scalable AI solutions.

Europe, contributing 25.32% to growth, focuses on deployments that adhere to strict data sovereignty and energy efficiency standards, influencing the design of private AI cloud solutions.

This regional differentiation underscores the need for platforms capable of supporting both AI supercomputing scale and compliance with localized governance frameworks like the EU's proposed AI Act.

Customer Landscape Analysis for the Ai Gpu Orchestration Platforms Market

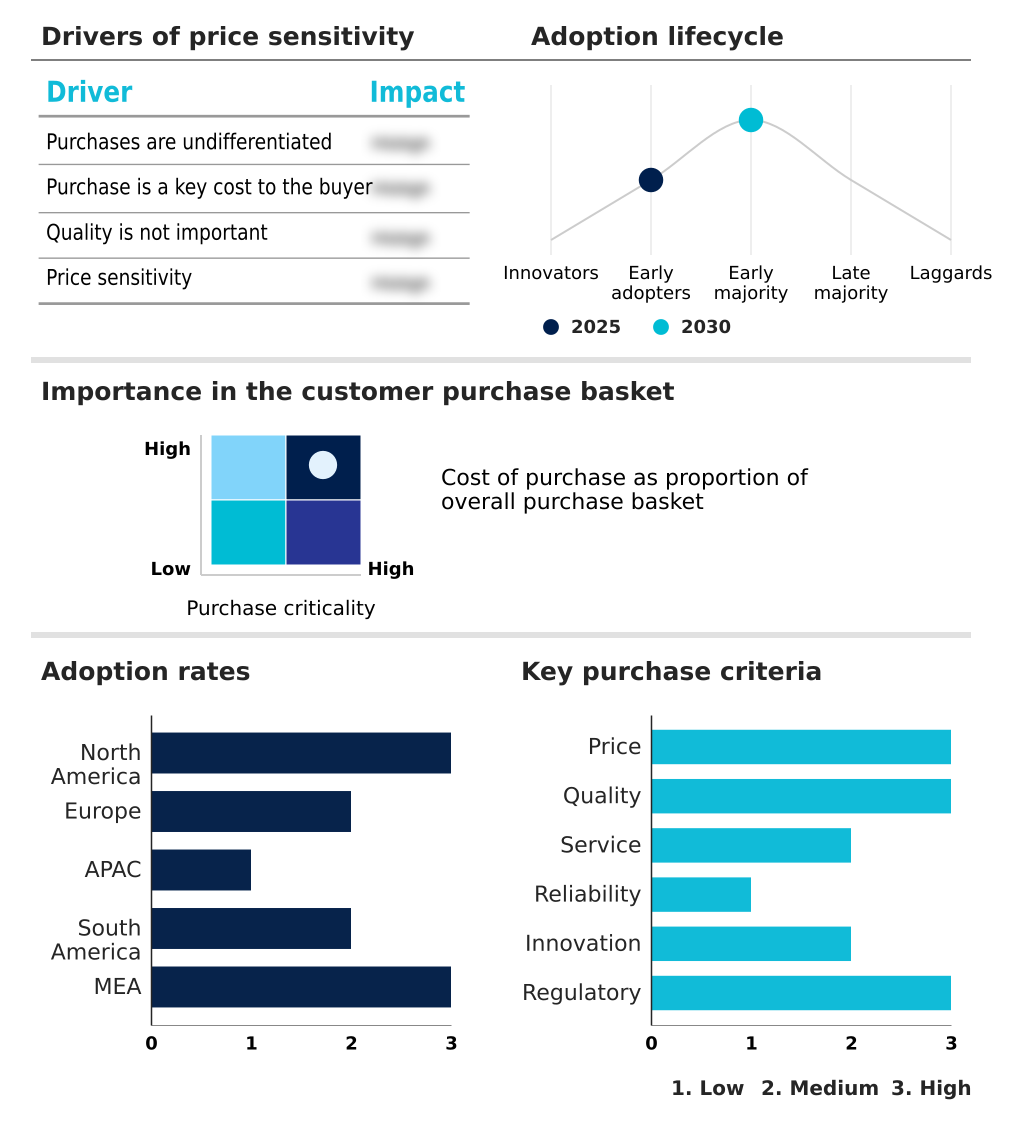

The ai gpu orchestration platforms market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai gpu orchestration platforms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Ai Gpu Orchestration Platforms Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the ai gpu orchestration platforms market industry.

Amazon.com Inc. - Key offerings feature platforms for managing and optimizing GPU resources for AI workloads, enabling efficient deployment from development through production across diverse and complex computing environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Anyscale Inc

- Broadcom Inc.

- ClearML Inc

- Databricks Inc.

- DigitalOcean Holdings Inc.

- Domino Data Lab Inc.

- Google LLC

- Hewlett Packard Enterprise Co.

- IBM Corp.

- Intel Corp.

- Lambda Labs, Inc.

- Lightning AI

- Microsoft Corp.

- NVIDIA Corp.

- Together AI

- VULTR

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Ai Gpu Orchestration Platforms Market

- In March 2025, CoreWeave announced a strategic agreement to provide AI infrastructure to OpenAI, aimed at expanding OpenAI's compute capacity for training and large-scale model deployment.

- In March 2025, CoreWeave announced an agreement to acquire Weights and Biases, a prominent AI developer platform, to create a more comprehensive, end-to-end solution for its purpose-built cloud offering.

- In March 2025, the International Energy Agency introduced a new regulatory guideline requiring major enterprise data centers to report hourly power consumption metrics tied to AI hardware usage.

- In November 2024, Huawei introduced Flex:AI, a new open-source software platform designed to enhance the utilization of its AI chipsets and provide high-performance training capabilities.

Research Analyst Overview: Ai Gpu Orchestration Platforms Market

Boardroom decisions regarding capital expenditure are now directly tied to AI infrastructure management, moving beyond hardware acquisition to focus on total cost of ownership. With North America representing 36.32% of incremental market growth, the primary challenge is maximizing return on substantial investments in high-performance computing.

This requires sophisticated resource allocation via container orchestration and GPU virtualization to enable dynamic scaling of deep learning frameworks. The adoption of confidential computing for AI is a critical response to data security mandates, allowing for multi-tenancy support without compromising sensitive workloads.

For instance, a global bank using a platform with GPU partitioning can isolate its fraud detection models from experimental trading algorithms running on the same cluster, adhering to strict compliance protocols.

Platforms must support heterogeneous hardware and provide advanced job scheduling and MLOps integration to streamline AI workload migration and facilitate automated model deployment, ultimately driving down operational costs and improving hardware utilization.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ai Gpu Orchestration Platforms Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 315 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 25.9% |

| Market growth 2026-2030 | USD 6589.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 24.0% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, Israel, UAE, South Africa and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Ai Gpu Orchestration Platforms Market: Key Questions Answered in This Report

-

What is the expected growth of the Ai Gpu Orchestration Platforms Market between 2026 and 2030?

-

The Ai Gpu Orchestration Platforms Market is expected to grow by USD 6.59 billion during 2026-2030, registering a CAGR of 25.9%. Year-over-year growth in 2026 is estimated at 24.0%%. This acceleration is shaped by escalating demand for large language model training and inference capabilities, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud, On-premises, and Hybrid), End-user (Tech companies, BFSI, Healthcare, Manufacturing, and Research and academia), Application (Workload orchestration, GPU scheduling and allocation, Cluster management, Multi-tenancy and governance, and Cost optimization) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Cloud segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 36.3% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, UK, Germany, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, Israel, UAE, South Africa and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is escalating demand for large language model training and inference capabilities, which is accelerating investment and industry demand. The main challenge is interoperability issues across diverse hardware ecosystems and cloud providers, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Ai Gpu Orchestration Platforms Market?

-

Key vendors include Amazon.com Inc., Anyscale Inc, Broadcom Inc., ClearML Inc, Databricks Inc., DigitalOcean Holdings Inc., Domino Data Lab Inc., Google LLC, Hewlett Packard Enterprise Co., IBM Corp., Intel Corp., Lambda Labs, Inc., Lightning AI, Microsoft Corp., NVIDIA Corp., Together AI and VULTR. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Ai Gpu Orchestration Platforms Market Research Insights

The dynamics of the AI GPU orchestration platforms market are influenced by the diverse needs of end-users and complex infrastructure strategies. Tech companies represent the largest end-user segment, with a 2024 market value approximately 30% higher than the BFSI sector, reflecting their aggressive investment in generative AI workloads.

This demand drives the need for computational resource optimization and scalable AI solutions. A key operational reality is managing workloads across disparate environments, which necessitates a cohesive multi-cloud AI strategy. For instance, a healthcare organization must balance the scalability of a public cloud with data residency rules, requiring a unified AI platform that can enforce strict governance.

The International Energy Agency's recent guidelines on power consumption reporting further pressure operators to adopt platforms offering energy-aware GPU resource scheduling, making efficient GPU utilization a critical performance metric.

We can help! Our analysts can customize this ai gpu orchestration platforms market research report to meet your requirements.

RIA -

RIA -