AI In Legal Document Automation Market Size 2025-2029

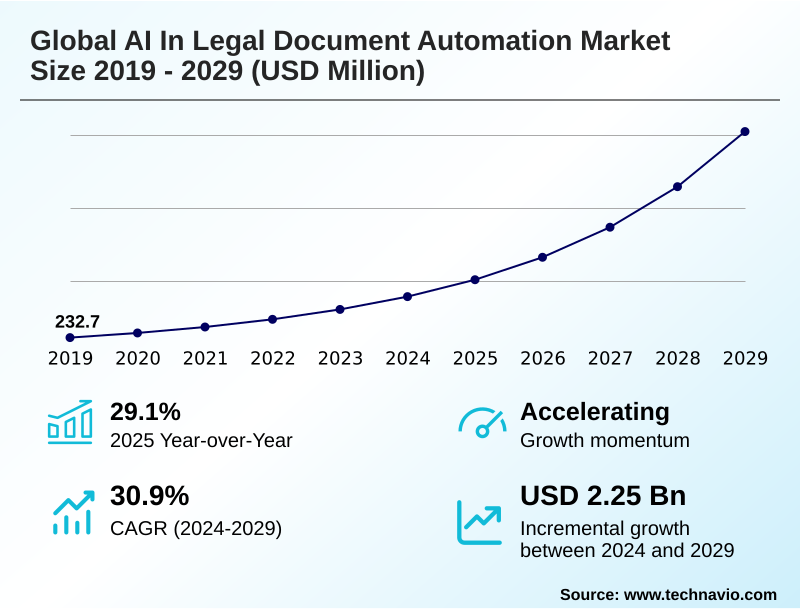

The ai in legal document automation market size is valued to increase by USD 2.25 billion, at a CAGR of 30.9% from 2024 to 2029. Increasing demand for efficiency and cost reduction will drive the ai in legal document automation market.

Major Market Trends & Insights

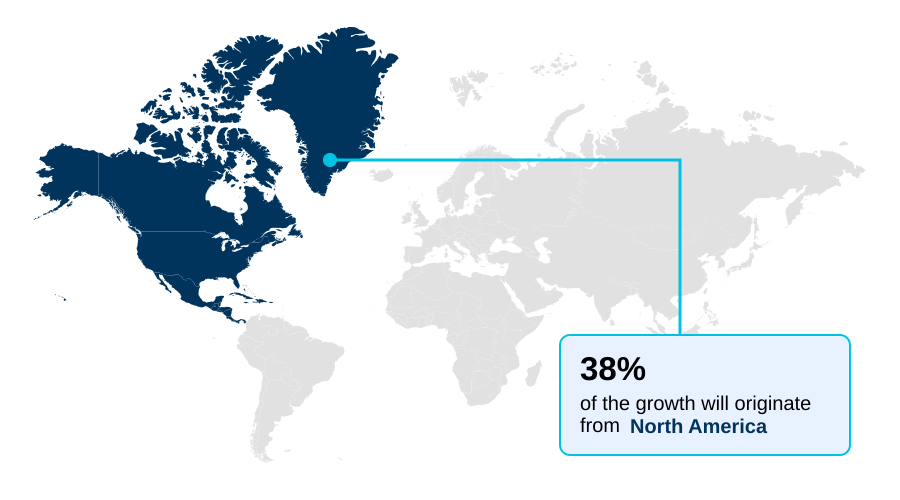

- North America dominated the market and accounted for a 37.9% growth during the forecast period.

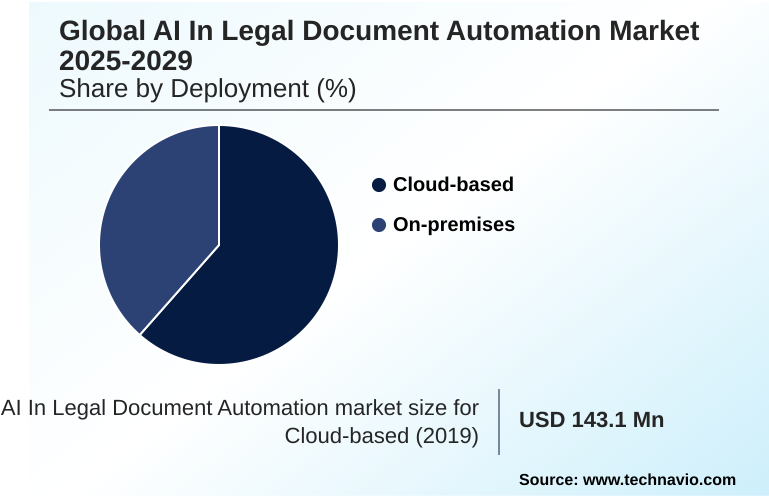

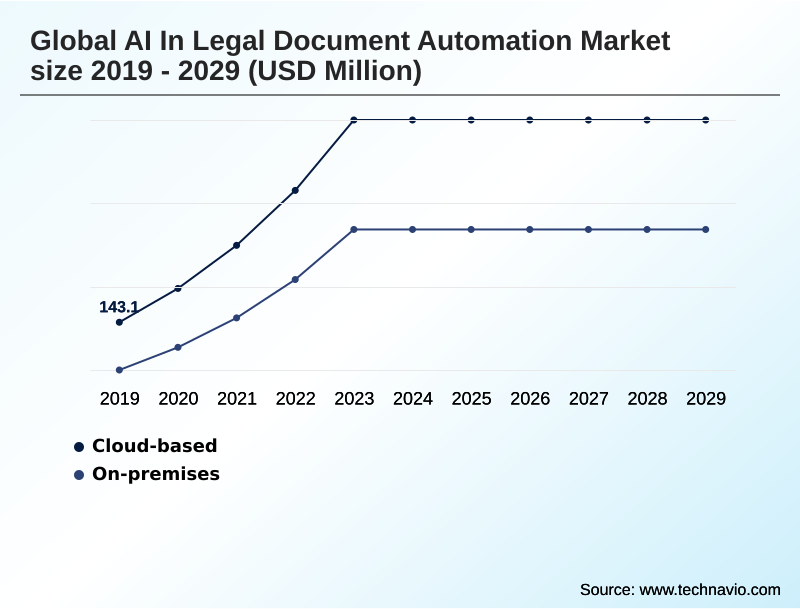

- By Deployment - Cloud-based segment was valued at USD 369.8 million in 2023

- By Application - Contract review segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.81 billion

- Market Future Opportunities: USD 2.25 billion

- CAGR from 2024 to 2029 : 30.9%

Market Summary

- The AI in legal document automation market is undergoing a significant transformation, driven by the increasing need for operational efficiency and cost reduction within the legal sector. This market revolves around the application of advanced technologies to streamline document-intensive workflows, from drafting and review to analysis and management.

- Key drivers include the growing complexity of global regulatory environments and continuous advancements in AI that enable more sophisticated and accurate document processing. For instance, in a large-scale mergers and acquisitions scenario, AI platforms can analyze thousands of contracts for due diligence in a fraction of the time required by a human team, identifying critical risks and non-standard clauses.

- This not only accelerates deal timelines but also enhances the precision of the legal review. However, the adoption of these technologies is met with challenges related to data security, the high cost of integration with legacy systems, and a shortage of legal professionals with the necessary technical skills.

- The market's trajectory is toward more specialized, user-friendly solutions that seamlessly integrate into existing legal practice ecosystems.

What will be the Size of the AI In Legal Document Automation Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Legal Document Automation Market Segmented?

The ai in legal document automation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Application

- Contract review

- Document drafting

- Legal research

- Others

- End-user

- Law firms

- Corporate departments

- Regulatory bodies

- Legal tech service providers

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- South Korea

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The cloud-based segment is defined by solutions delivered over the internet, offering scalability and accessibility that democratize advanced AI capabilities.

This model eliminates substantial upfront capital costs, replacing them with predictable subscription-based operational expenses, which is attractive for firms of all sizes. Cloud deployment facilitates superior workflow automation tools and remote collaboration, a critical advantage in modern distributed work environments.

For instance, some firms have achieved a 30% reduction in time spent on routine legal work by leveraging AI for initial contract review.

Utilizing AI-powered contract management and AI legal research tools, these platforms enable users to adjust capacity based on fluctuating workloads.

The focus is on secure AI for legal data, ensuring automatic updates for security and features, thus reducing the internal IT burden and enhancing overall efficiency.

The Cloud-based segment was valued at USD 369.8 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Legal Document Automation Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is led by North America, which is set to contribute approximately 38% of the market's incremental growth.

This is driven by high adoption rates in the United States and Canada, where a mature legal tech ecosystem and significant investment in advanced AI solutions prevail.

Meanwhile, the APAC region is projected to expand at the fastest rate, fueled by rapid digitalization and government initiatives in countries like China and Singapore.

Europe maintains a strong position with its complex regulatory environment, fostering demand for robust compliance solutions. Utilizing AI for due diligence and AI for regulatory changes is becoming standard practice.

These regions leverage legal document automation AI and legal clause analysis AI to manage intricate cross-border transactions, with a focus on expert system building to navigate diverse legal frameworks.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of AI in the legal sector is fundamentally reshaping operational paradigms. AI for automating contract review workflows is no longer a futuristic concept but a present-day tool that delivers measurable efficiency gains, with some platforms reducing manual review times by more than half.

- The advent of generative AI for drafting legal agreements further accelerates this transformation, allowing legal teams to produce high-quality first drafts rapidly. This directly addresses the impact of AI on legal research accuracy, as intelligent systems can sift through vast legal databases to find the most relevant precedents.

- Moreover, AI tools for corporate compliance monitoring provide a proactive approach to risk management, continuously scanning for regulatory changes. Despite these advantages, there are challenges of integrating AI in law firms, which often involve significant upfront investment and cultural shifts. Key considerations include the ROI of AI in corporate legal departments and securing sensitive data in AI legal platforms.

- Success hinges on a holistic strategy that includes training legal professionals for AI adoption and understanding the ethical considerations in legal AI deployment. Advanced applications like AI for intellectual property portfolio management and automating regulatory reporting with AI tools are becoming crucial for competitive advantage.

- Firms are also exploring AI-driven predictive analytics for litigation and using AI for e-discovery cost reduction to optimize resource allocation, especially in managing the high costs associated with M&A deals where AI-powered due diligence is invaluable.

What are the key market drivers leading to the rise in the adoption of AI In Legal Document Automation Industry?

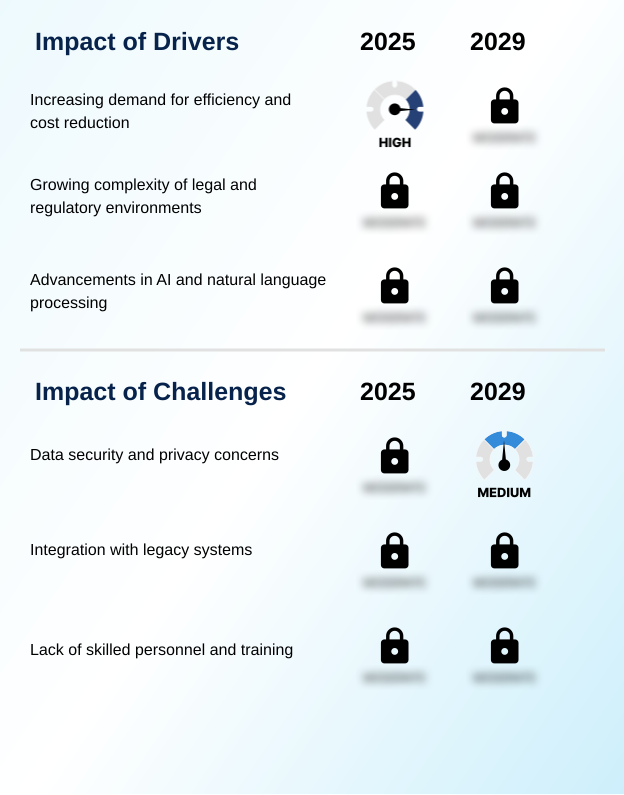

- The escalating demand within the legal sector for enhanced operational efficiency and significant cost reduction is a primary driver for market expansion.

- The escalating demand for efficiency and cost reduction is a primary driver, as traditional legal processes are notoriously labor-intensive.

- AI-powered document automation solutions, including AI-assisted contract review and automated contract drafting, directly address these issues by streamlining workflows and minimizing manual intervention.

- AI algorithms can review thousands of contracts in a fraction of the time, with implementations showing up to a 30% reduction in time spent on transactional legal work.

- Utilizing machine learning algorithms, these systems offer greater consistency and accuracy in identifying key clauses and potential risks. This acceleration of project completion frees up legal professionals to focus on higher-value advisory work.

- The drive for cost-efficiency is particularly relevant as clients demand more value, making adoption of e-discovery AI solutions and similar technologies a competitive necessity.

What are the market trends shaping the AI In Legal Document Automation Industry?

- The integration of generative AI is a paramount trend transforming legal workflows. It is actively reshaping how professionals approach document creation, review, and analysis.

- A paramount trend is the increasing integration of generative AI capabilities, which is transforming legal workflows by moving beyond analysis to active content creation. This evolution enables legal professionals to use AI-assisted document drafting to produce initial drafts of contracts and memos, accelerating document creation by over 40% in some use cases.

- AI for legal document review is also enhanced, as generative AI can summarize complex case law into concise, actionable insights. These automated legal memo generation and legal document summarization capabilities, powered by advanced generative AI models and semantic meaning analysis, allow legal teams to iterate on documents more rapidly.

- The benefits include substantial time savings and enhanced productivity, enabling a greater focus on strategic thinking and complex problem-solving as the technology becomes more legally nuanced.

What challenges does the AI In Legal Document Automation Industry face during its growth?

- Significant data security and privacy concerns, particularly regarding sensitive client information, represent a key challenge impacting the industry's growth.

- Profound data security and privacy concerns are a primary challenge, as legal documents contain highly sensitive and confidential information. The deployment of AI solutions, especially cloud-based platforms offering AI-powered compliance monitoring and legal workflow automation, raises critical questions about data protection. Surveys indicate that over 60% of legal professionals cite data security as their top concern, inhibiting faster adoption.

- Regulatory requirements like GDPR mandate robust data protection, and any perceived vulnerability can lead to significant penalties and loss of client trust. The challenge is intensified by the large volumes of data needed for training AI, which necessitates secure data anonymization and access controls.

- This makes the implementation of multi-agent AI platforms and other advanced tools a carefully considered process for legal organizations.

Exclusive Technavio Analysis on Customer Landscape

The ai in legal document automation market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in legal document automation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Legal Document Automation Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in legal document automation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ContractPod Technologies Ltd. - AI platforms enhance legal workflows with generative capabilities for contract lifecycle management, intelligent document processing, and automated compliance, ensuring greater operational precision.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ContractPod Technologies Ltd.

- Counsel AI Corp.

- CS Disco Inc.

- Everlaw Inc.

- Hebbia Inc.

- Ironclad Inc.

- Juro Ltd.

- Legalogic Ltd.

- LexisNexis Legal and Professional

- LinkSquares Inc.

- Litera

- Luminance Technologies Ltd.

- Neota Logic Inc.

- Reveal Data Corp.

- Robin AI Ltd.

- Themis Solutions Inc.

- Thomson Reuters Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in legal document automation market

- In September, 2024, a leading AI legal tech company announced a strategic partnership with a prominent financial services law firm to implement an AI-powered system for automating regulatory compliance checks on complex financial derivatives.

- In November, 2024, a legal tech startup specializing in real estate law launched an AI platform specifically designed to automate the review and drafting of commercial lease agreements, featuring modules tailored to property-specific regulations.

- In January, 2025, a major legal AI company integrated a new large language model into its document review platform, enabling the system to understand complex legal arguments and summarize lengthy case documents with human-like precision.

- In March, 2025, a major legal technology provider acquired a niche AI startup specializing in advanced e-discovery solutions, aiming to integrate its predictive coding technology to enhance its litigation support offerings.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Legal Document Automation Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 30.9% |

| Market growth 2025-2029 | USD 2251.0 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 29.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, South Korea, India, Australia, Indonesia, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in legal document automation market is characterized by continuous evolution, moving beyond simple task automation to become a strategic asset for legal operations. The core value proposition is the enhancement of efficiency and accuracy in document-intensive processes.

- This is particularly evident in the integration of sophisticated AI capabilities that can interpret complex legal language and generate nuanced legal content. For boardroom-level consideration, the adoption of these technologies represents a pivotal decision concerning capital allocation and long-term competitive strategy.

- A key trend to monitor is the development of vertical-specific AI solutions, which offer tailored functionalities for distinct practice areas like real estate or intellectual property law. This specialization provides deeper, more contextually relevant insights compared to general-purpose tools.

- Investing in such platforms can yield significant returns, with some organizations achieving a 30% reduction in document processing time, freeing up legal professionals to focus on high-value strategic counsel rather than repetitive administrative tasks.

What are the Key Data Covered in this AI In Legal Document Automation Market Research and Growth Report?

-

What is the expected growth of the AI In Legal Document Automation Market between 2025 and 2029?

-

USD 2.25 billion, at a CAGR of 30.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, and On-premises), Application (Contract review, Document drafting, legal research, and others), End-user (Law firms, Corporate departments, Regulatory bodies,and Legal tech service providers) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for efficiency and cost reduction, Data security and privacy concerns

-

-

Who are the major players in the AI In Legal Document Automation Market?

-

ContractPod Technologies Ltd., Counsel AI Corp., CS Disco Inc., Everlaw Inc., Hebbia Inc., Ironclad Inc., Juro Ltd., Legalogic Ltd., LexisNexis Legal and Professional, LinkSquares Inc., Litera, Luminance Technologies Ltd., Neota Logic Inc., Reveal Data Corp., Robin AI Ltd., Themis Solutions Inc. and Thomson Reuters Corp.

-

Market Research Insights

- The dynamics of the AI in legal document automation market are shaped by a convergence of technological innovation and evolving business needs. The primary impetus for adoption is the pursuit of efficiency; organizations report time reductions of over 30% on routine document review tasks.

- This drive is complemented by advancements that improve accuracy, with some platforms demonstrating a 15% lower error rate compared to manual processes. Trends show a clear shift toward vertical-specific solutions and the integration of generative AI, which moves beyond analysis to content creation.

- However, significant challenges persist, including data privacy concerns and the complexities of integrating modern AI with entrenched legacy systems. The competitive landscape is characterized by a mix of established legal tech giants and agile startups, all competing to offer more intuitive and powerful automation tools.

We can help! Our analysts can customize this ai in legal document automation market research report to meet your requirements.

RIA -

RIA -