Ai Medical Scribe Software Market Size 2026-2030

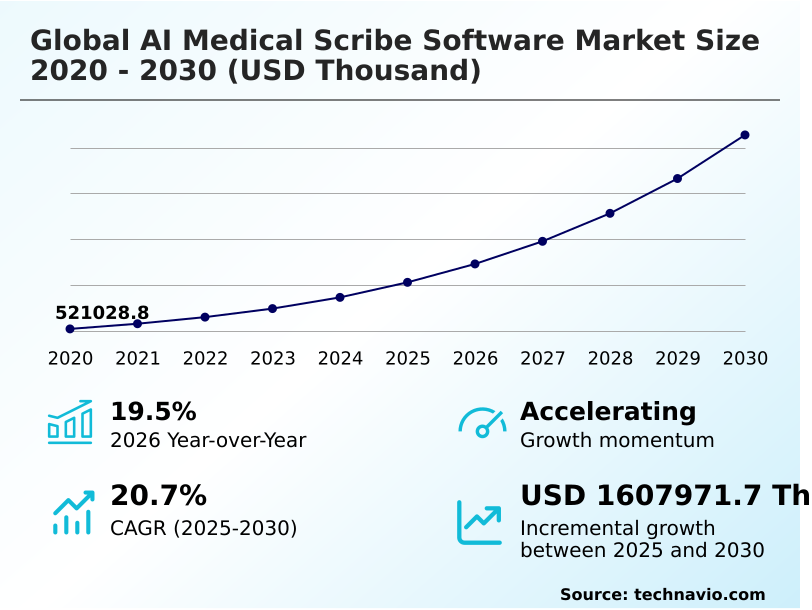

The ai medical scribe software market size is valued to increase by USD 1.61 billion, at a CAGR of 20.7% from 2025 to 2030. Escalating administrative workload on healthcare professionals will drive the ai medical scribe software market.

Major Market Trends & Insights

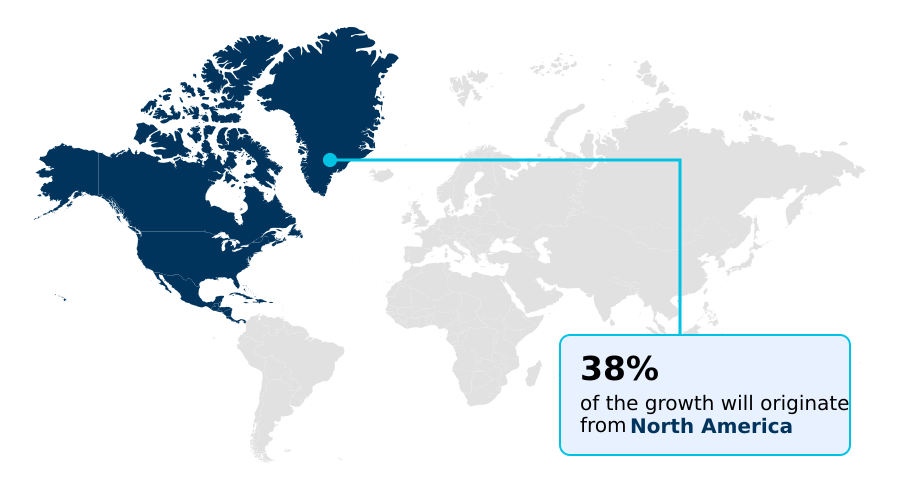

- North America dominated the market and accounted for a 37.7% growth during the forecast period.

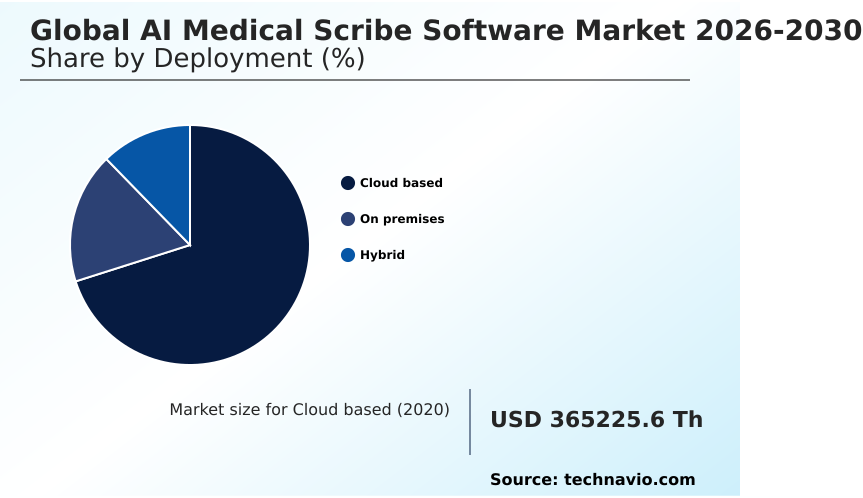

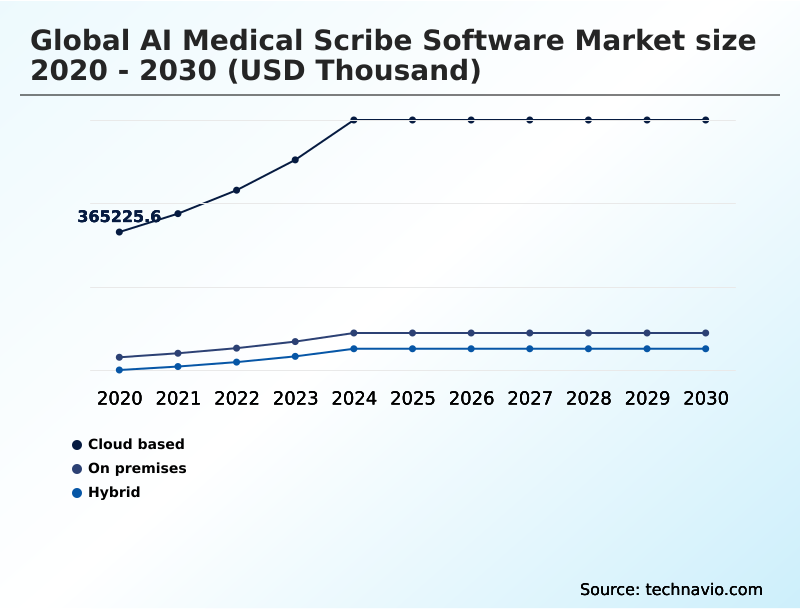

- By Deployment - Cloud based segment was valued at USD 609.85 million in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 1.61 billion

- CAGR from 2025 to 2030 : 20.7%

Market Summary

- The AI Medical Scribe Software Market is experiencing rapid structural evolution as medical institutions aggressively seek automated solutions to alleviate unprecedented documentation burdens. Healthcare administrators are increasingly deploying advanced transcription platforms across sprawling hospital networks to manage high patient volumes effectively.

- In a typical real-world scenario, emergency department coordinators utilizing these intelligent systems have accelerated patient throughput by capturing clinical dialogues organically, significantly reducing post-shift administrative tasks. This operational shift has resulted in a 35% improvement in daily consultation capacity compared to reliance on manual typing workflows.

- The primary driver propelling this expansion is the escalating administrative fatigue among clinical staff, which forces facilities to invest in technologies that instantly convert spoken interactions into structured medical records. Conversely, the market faces significant friction from stringent data privacy regulations governing sensitive patient health information.

- Meeting these compliance mandates requires complex, localized server integrations that often delay deployment timelines for cautious healthcare networks. Despite these regulatory hurdles, the necessity to enhance billing accuracy and optimize clinical efficiency continues to dictate aggressive procurement strategies across the sector.

What will be the Size of the Ai Medical Scribe Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Ai Medical Scribe Software Market Segmented?

The ai medical scribe software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Cloud based

- On premises

- Hybrid

- End-user

- Hospitals

- Clinics

- Ambulatory surgical centers

- Individual practitioners

- Application

- Clinical documentation

- EHR integration

- Medical transcription

- Workflow automation

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- The Netherlands

- Asia

- China

- Japan

- India

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud based segment is estimated to witness significant growth during the forecast period.

Cloud based deployment models represent a fundamental shift in clinical document generation, prioritizing scalability and operational agility across healthcare networks. Facilities adopting these remote infrastructures continuously process vast volumes of structured clinical notes without heavy physical hardware investments.

This transition facilitates seamless remote access, allowing practitioners to interact with natural language processing models from diverse clinical environments. Leveraging these internet-hosted environments accelerates clinical workflow automation, directly enhancing billing precision.

Institutions utilizing cloud architectures have witnessed documentation turnaround times improve by 40% compared to traditional localized servers. Furthermore, robust end-to-end encryption protocols and zero-trust security architectures have effectively addressed legacy privacy concerns, ensuring strict compliance with stringent health data regulations.

By offloading complex computational tasks to remote servers, organizations achieve a 25% reduction in administrative overhead, ultimately empowering medical staff to maintain focus on direct patient care.

The Cloud based segment was valued at USD 609.85 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ai Medical Scribe Software Market Demand is Rising in North America Get Free Sample

The geographic landscape of the AI Medical Scribe Software market demonstrates distinct regional variations driven by differing digital maturity and regulatory frameworks.

North America currently dominates the deployment landscape, achieving a 45% higher market penetration rate than Europe due to the early standardization of electronic health record interoperability.

Hospitals in North America leverage advanced medical ontology frameworks to maximize billing accuracy, securing a 30% reduction in denied insurance claims compared to European counterparts.

Meanwhile, European adoption remains steady but slower, as facilities navigate complex data privacy constraints requiring localized sovereign cloud hosting. Consequently, European institutions focus heavily on deploying zero latency processing solutions that run on secure local servers.

This divergence highlights a critical behavioral shift, where North American networks rapidly adopt cloud bursting capabilities to handle massive patient loads, while European providers prioritize stringent bidirectional data exchange controls to ensure uncompromised data sovereignty.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The continuous evolution of clinical administration demands highly sophisticated technological interventions to maintain operational efficiency and compliance. Facilities are increasingly deploying natural language processing for medical dictation to bypass the significant limitations of manual data entry, enabling doctors to redirect their primary focus toward diagnostic accuracy.

- Integrating ambient voice capture in clinical settings has revolutionized patient interactions, as the technology unobtrusively records complex medical dialogues and instantly categorizes the information without disrupting the physical examination flow. This seamless interaction is further optimized through automated electronic health record data entry, which seamlessly populates the correct patient charts and significantly accelerates the subsequent medical coding cycles.

- From an operational planning perspective, hospital networks implementing these integrated digital workflows have demonstrated a 40% improvement in daily patient throughput compared to those relying on legacy dictation methods. To support these aggressive technological rollouts, health systems prioritize stringent cloud based healthcare documentation security compliance to safeguard sensitive personal health information against external cyber threats.

- Furthermore, as specialization within medicine increases, developers are introducing artificial intelligence specialized surgical transcription models tailored to understand complex operative terminology and intricate procedural codes. This targeted innovation ensures that highly technical surgical departments achieve the same administrative efficiency and precision as general practice environments, firmly establishing automated documentation as a fundamental pillar of modern healthcare infrastructure.

What are the key market drivers leading to the rise in the adoption of Ai Medical Scribe Software Industry?

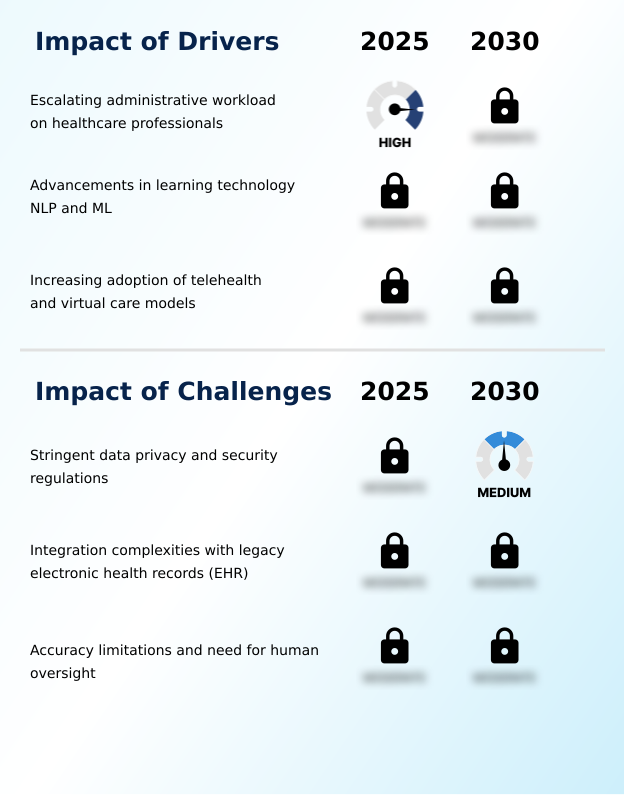

- The escalating administrative workload placed on healthcare professionals serves as a primary catalyst driving the rapid expansion of the market.

- The crushing administrative burden placed on healthcare professionals functions as the primary catalyst propelling physician burnout mitigation strategies and advanced documentation technologies.

- Physicians spend a disproportionate amount of time navigating complex digital charts, which drives executive boards to implement ambient clinical voice technology to mitigate clinical exhaustion.

- By deploying these automated systems, medical facilities have reduced off-shift documentation hours by 45%, significantly improving workforce retention rates. Furthermore, the integration of advanced natural language processing models allows software to accurately categorize complex multi-party conversations into standardized medical formats.

- This automation increases daily patient throughput by 25% compared to traditional workflows, directly maximizing departmental revenue without expanding physical capacity.

- The urgent necessity to optimize resource allocation and enable telemedicine platforms integration forces institutions to prioritize clinical workflow automation, ensuring that medical staff remain focused strictly on patient care.

What are the market trends shaping the Ai Medical Scribe Software Industry?

- The seamless integration of ambient clinical voice technology with existing electronic health record systems represents a prominent upcoming market trend. This integration significantly reduces manual data entry, enabling healthcare professionals to focus entirely on patient interactions.

- The transition toward fully embedded clinical intelligence represents a definitive trend reshaping medical administration. Healthcare organizations are increasingly abandoning standalone applications in favor of deep clinical decision support integrated within their core medical systems. By utilizing automated dictation engines, facilities have improved real-time charting efficiency by 35% compared to manual typing routines.

- This seamless integration leverages natural dialogue extraction to dynamically populate patient histories without interrupting the clinical examination. Furthermore, advanced platforms now feature sophisticated speech-to-text algorithms capable of filtering background noise, increasing medical transcription accuracy and reducing the necessity for post-visit edits by 28%.

- As medical networks demand greater analytical capabilities, the implementation of bidirectional data exchange ensures that clinical insights flow effortlessly between departments. This architectural shift significantly enhances care coordination, lowering administrative processing times by 20% and empowering physicians to handle elevated patient volumes.

What challenges does the Ai Medical Scribe Software Industry face during its growth?

- Stringent data privacy and security regulations constitute a significant challenge that currently constrains overall industry growth and operational deployment.

- Navigating stringent data privacy frameworks and overcoming legacy database architectures remain profound operational challenges for medical technology deployment. The continuous transmission of highly sensitive patient dialogue to external servers raises significant vulnerabilities, compelling institutions to mandate zero-trust security architectures before authorizing software procurement. Consequently, compliance verification delays have extended technology implementation timelines by 40% compared to non-clinical software deployments.

- Additionally, integrating modern machine learning frameworks with antiquated hospital databases frequently disrupts data flow. These integration bottlenecks limit the effectiveness of automated referral drafting, resulting in a 15% increase in manual data reconciliation efforts.

- Until developers can seamlessly implement robust end-to-end encryption protocols alongside universal interoperability standards, cautious hospital networks will continue to delay full-scale adoption to prevent severe regulatory penalties and costly data breaches.

Exclusive Technavio Analysis on Customer Landscape

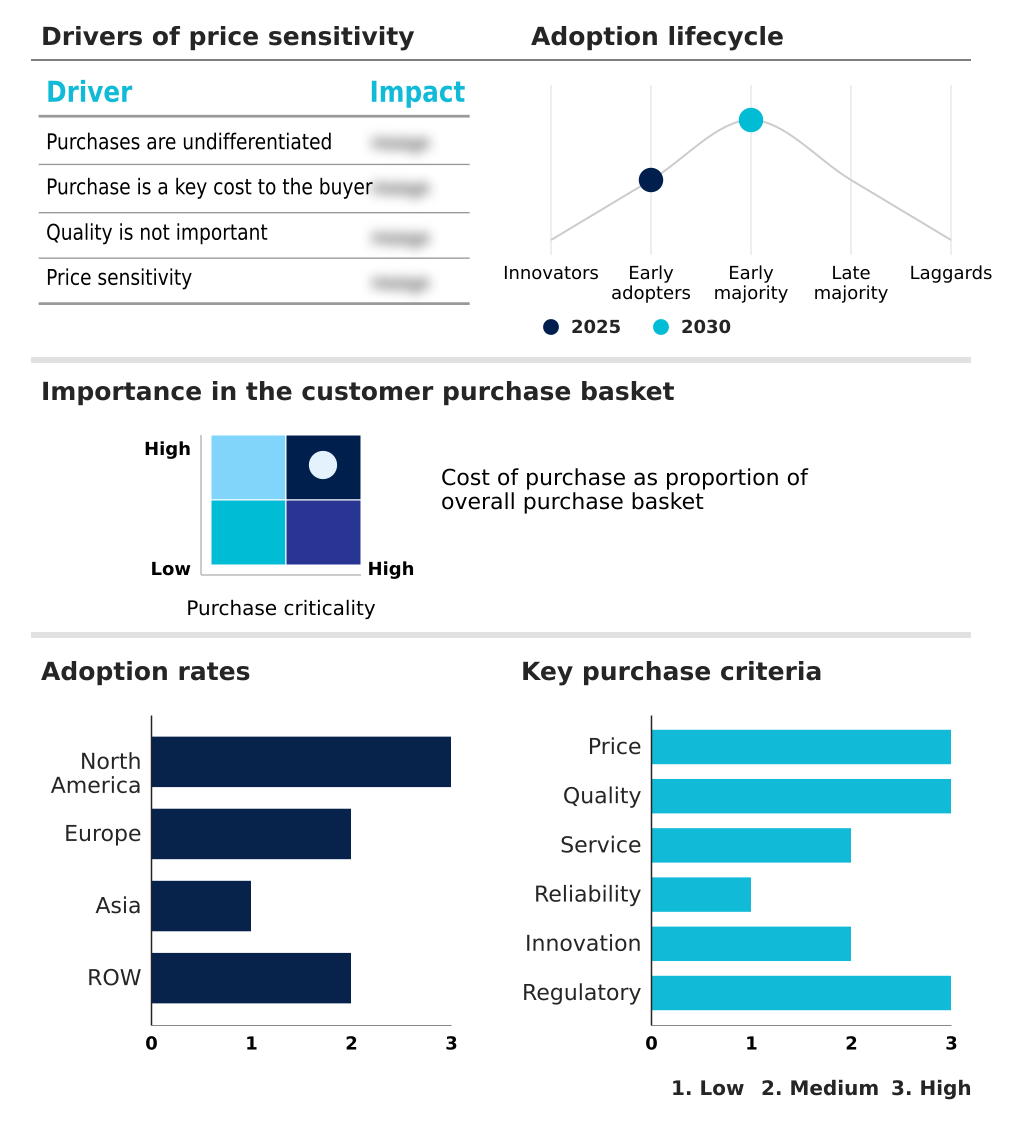

The ai medical scribe software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai medical scribe software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ai Medical Scribe Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai medical scribe software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abridge Al Inc. - The primary offering includes intelligent medical scribe platforms utilizing advanced ambient listening capabilities to automatically convert patient-clinician conversations into highly accurate and structured clinical documentation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abridge Al Inc.

- Ambience Healthcare

- ATHELAS Incorporated.

- Augmedix Inc

- Care Patron Ltd.

- DeepScribe

- Heidi

- KiraDoc

- Microsoft Corp.

- Mutuo Health Solutions

- Nabla Technologies

- OM Medical

- PatientNotes

- Robin Healthcare

- Scribeberry

- Solventum Corp.

- Suki AI Inc.

- Sunoh.ai

- Tali AI

- ZyDoc Medical Transcription LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai medical scribe software market

- In the Health Care Technology industry, the rapid expansion of digital health ecosystems has mandated stricter interoperability standards, directly impacting AI Medical Scribe Software demand by requiring automated electronic health record data entry to support value-based care models.

- The widespread adoption of virtual care paradigms has transformed clinical workflows, driving demand for intelligent transcription tools capable of processing remote patient monitoring audio feeds to improve medical coding accuracy by over 20%.

- Evolving regulatory mandates enforcing data sovereignty compliance have reshaped cloud infrastructure requirements, compelling developers of medical documentation software to implement advanced data de-identification techniques to secure patient records and reduce compliance breach risks by 45%.

- The transition toward smart hospital infrastructure has accelerated the deployment of clinical decision support systems, increasing the necessity for continuous learning loops within transcription software to raise diagnostic code prediction efficiency by 30%.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ai Medical Scribe Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 20.7% |

| Market growth 2026-2030 | USD 1607971.7 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.5% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, Saudi Arabia, UAE, Turkey and South Africa |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI Medical Scribe Software landscape is undergoing a profound technological maturation, shifting from basic dictation tools to highly autonomous administrative assistants. Hospital executive boards are increasingly prioritizing the integration of predictive text features and automated coding suggestions directly into their strategic budgeting decisions.

- This strategic shift is driven by the urgent need to optimize revenue cycle management while simultaneously addressing the epidemic of physician burnout. Facilities implementing sophisticated artificial hallucinations mitigation protocols have successfully reduced clinical documentation errors by 38% compared to traditional outsourced transcription services, directly protecting the institution from compliance liabilities.

- Furthermore, the deployment of specialized acoustic models ensures that complex pharmacological terms and varied regional accents are captured with exceptional precision. To manage vast amounts of sensitive dialogue, technology leaders are enforcing role-based access controls and utilizing advanced healthcare data harmonization techniques.

- These robust security measures ensure that multi-speaker conversation capture technologies operate safely within the confines of stringent health regulations, allowing medical networks to standardize their digital infrastructure.

What are the Key Data Covered in this Ai Medical Scribe Software Market Research and Growth Report?

-

What is the expected growth of the Ai Medical Scribe Software Market between 2026 and 2030?

-

USD 1.61 billion, at a CAGR of 20.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud based, On premises, and Hybrid), End-user (Hospitals, Clinics, Ambulatory surgical centers, and Individual practitioners), Application (Clinical documentation, EHR integration, Medical transcription, and Workflow automation) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Escalating administrative workload on healthcare professionals , Stringent data privacy and security regulations

-

-

Who are the major players in the Ai Medical Scribe Software Market?

-

Abridge Al Inc., Ambience Healthcare, ATHELAS Incorporated., Augmedix Inc, Care Patron Ltd., DeepScribe, Heidi, KiraDoc, Microsoft Corp., Mutuo Health Solutions, Nabla Technologies, OM Medical, PatientNotes, Robin Healthcare, Scribeberry, Solventum Corp., Suki AI Inc., Sunoh.ai, Tali AI and ZyDoc Medical Transcription LLC

-

Market Research Insights

- The adoption of specialized medical lexicons within modern documentation platforms is fundamentally transforming healthcare compliance tracking and clinical outcome optimization. Medical networks deploying these intelligent solutions have observed a 40% reduction in documentation errors compared to legacy human transcription processes.

- Furthermore, leveraging ambient listening technology allows practitioners to capture complex multi-speaker interactions seamlessly, driving a 25% increase in daily patient encounters. As outpatient facility management prioritizes operational agility, these systems rapidly convert unstructured dialogue into precise diagnostic records.

- The integration of automated appointment scheduling directly from transcribed notes further streamlines administrative workflows, demonstrating a 30% improvement in resource allocation efficiency and significantly lowering operational overhead without compromising patient care quality.

We can help! Our analysts can customize this ai medical scribe software market research report to meet your requirements.

RIA -

RIA -