Ai Model Optimization Tools Market Size and Growth Forecast 2026-2030

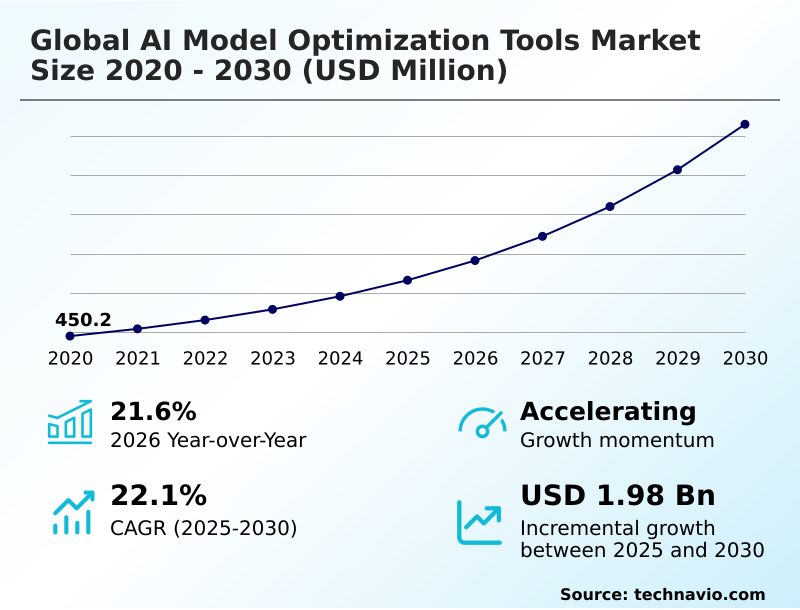

The Ai Model Optimization Tools Market size was valued at USD 1.16 billion in 2025 growing at a CAGR of 22.1% during the forecast period 2026-2030.

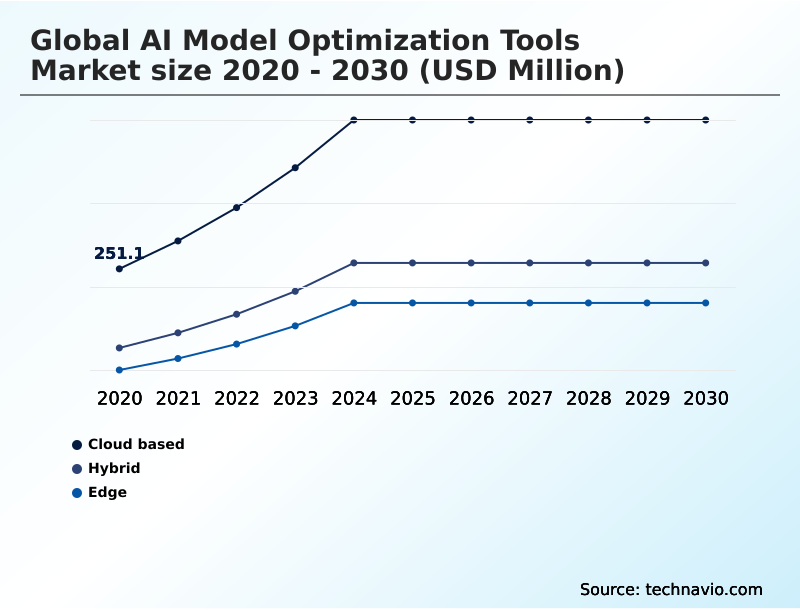

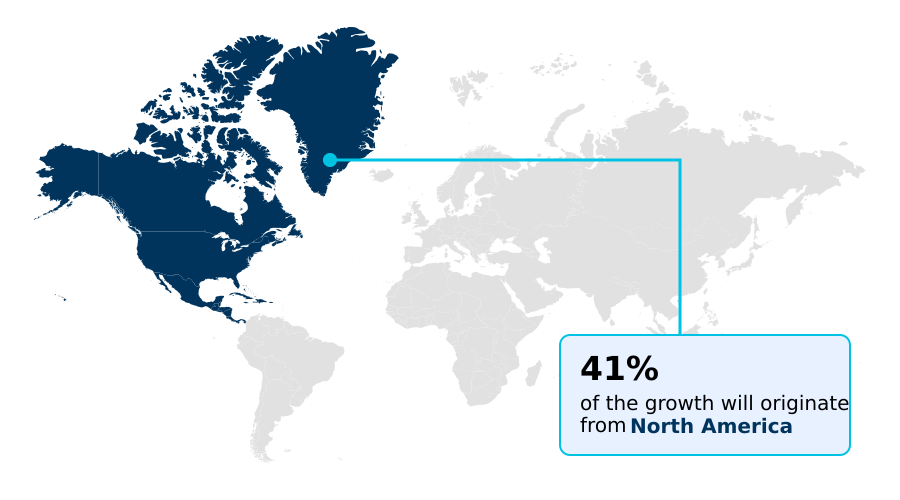

North America accounts for 40.6% of incremental growth during the forecast period. The Cloud based segment by Deployment was valued at USD 501.5 million in 2024, while the Generative AI segment holds the largest revenue share by Application.

The market is projected to grow by USD 2.70 billion from 2020 to 2030, with USD 1.98 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Ai Model Optimization Tools Market Overview

The AI model optimization tools market is expanding as organizations move beyond experimental AI to large-scale operational deployments, driven by the need to balance computational demand with budgetary and hardware constraints. This expansion is reflected in a year-over-year growth of 21.6%, with North America alone contributing to 40.6% of the market's incremental growth. Core techniques such as weight pruning and quantization are no longer optional but are strategic necessities for commercial viability, especially for complex large language models. For instance, an automotive plant implementing quality control with on-device AI deployment uses optimized computer vision models on its assembly line cameras. This hardware-aware optimization allows for real-time defect detection directly on edge devices, achieving latency reduction and eliminating the costs of cloud processing while ensuring high model fidelity. This shift underscores the industry's focus on embedding efficient, powerful AI into operational workflows, transforming raw data into actionable intelligence at the source and improving return on investment.

Drivers, Trends, and Challenges in the Ai Model Optimization Tools Market

Strategic decision-making in the AI model optimization tools market requires a thorough competitive analysis, as enterprises weigh the trade-offs between various techniques. The choice between Pytorch vs Tensorflow for model optimization often depends on the existing MLOps pipeline and the need for specific hardware integrations.

As organizations scale, the cost-benefit analysis of cloud AI optimization becomes critical, especially when dealing with large language models. The impact of hardware fragmentation on AI performance continues to be a central issue, pushing vendors to develop better cross-platform solutions.

Implementing continuous optimization in MLOps is becoming a best practice, but it introduces challenges in maintaining AI model fidelity, a concern highlighted in frameworks like the draft ISO AI Efficiency Framework. For instance, an automotive firm developing autonomous vehicles must balance aggressive model compression with the non-negotiable safety requirements, evaluating security implications.

The role of AI optimization in sustainable computing is also gaining prominence, as companies are now tasked with reporting the energy consumption of their AI workloads. The future of automated neural architecture search promises to alleviate some of these complexities by discovering optimal, hardware-specific model designs automatically.

The ability to measure AI model optimization ROI accurately will ultimately determine the technology's adoption rate across different industries.

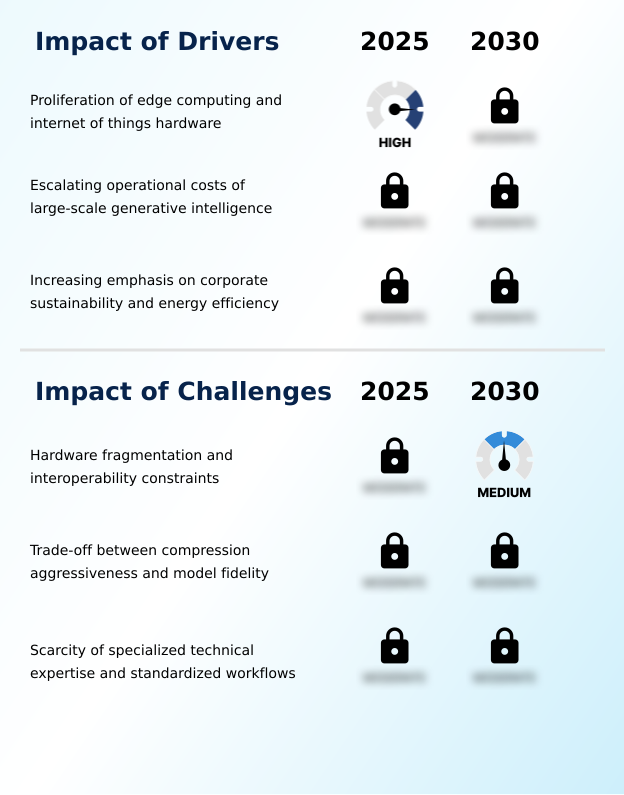

Primary Growth Driver: The proliferation of edge computing and Internet of Things hardware is a key driver for the market, creating demand for optimized AI models on resource-constrained devices.

The market is propelled by three interconnected forces that are making model optimization a strategic necessity.

First, the proliferation of edge computing and IoT hardware creates immense demand for lightweight models that can operate under strict power and memory constraints, driving techniques like structural pruning.

Second, the escalating operational costs of large-scale generative intelligence are forcing enterprises to adopt optimization to achieve commercial viability and manage inference cost reduction.

Finally, a growing emphasis on corporate sustainability and energy efficiency, in line with ESG mandates and regulations such as the EU Energy Efficiency Directive, is pushing organizations to minimize the carbon footprint of their data centers through power consumption optimization.

These drivers collectively shift optimization from a technical niche to a core business requirement.

Emerging Market Trend: The adoption of hardware-aware automated neural architecture search is emerging as a significant trend. This approach optimizes model efficiency for specific silicon, influencing deployment strategies across the industry.

Key trends are reshaping the deployment of artificial intelligence, driven by the need for greater efficiency and accessibility. The integration of continuous optimization within enterprise MLOps pipelines is becoming standard practice, ensuring that models remain efficient throughout their lifecycle.

This is complemented by the rise of hardware-aware automated neural architecture search, which automates the discovery of optimal model structures for specific hardware targets, from data center accelerators to edge devices. A significant shift is occurring toward ultra-low precision quantization, especially for generative intelligence, enabling massive models to run on consumer devices.

This trend toward on-device AI deployment is critical for applications requiring low latency and enhanced data privacy, fundamentally changing how users interact with AI.

Key Industry Challenge: Hardware fragmentation and interoperability constraints present a key challenge to industry growth, complicating cross-platform model deployment and increasing development overhead.

Despite strong drivers, the market faces significant structural challenges that temper growth. The primary obstacle is hardware fragmentation, where the diversity of silicon architectures necessitates bespoke optimization, increasing development costs and limiting model portability solutions. This creates significant cross-platform compatibility issues.

Another critical hurdle is the inherent trade-off between compression aggressiveness and model fidelity; overly aggressive quantization techniques can degrade performance, a risk that is unacceptable in high-stakes applications and a key focus of AI risk management.

Finally, a scarcity of specialized technical expertise, combining deep learning and low-level systems knowledge, creates a major bottleneck, hindering the widespread adoption of advanced optimization workflows and making AI deployment at scale difficult for many organizations.

Explore Full Market Dynamics Analysis Request Free Sample

Ai Model Optimization Tools Market Segmentation

The ai model optimization tools industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Deployment Segment Analysis

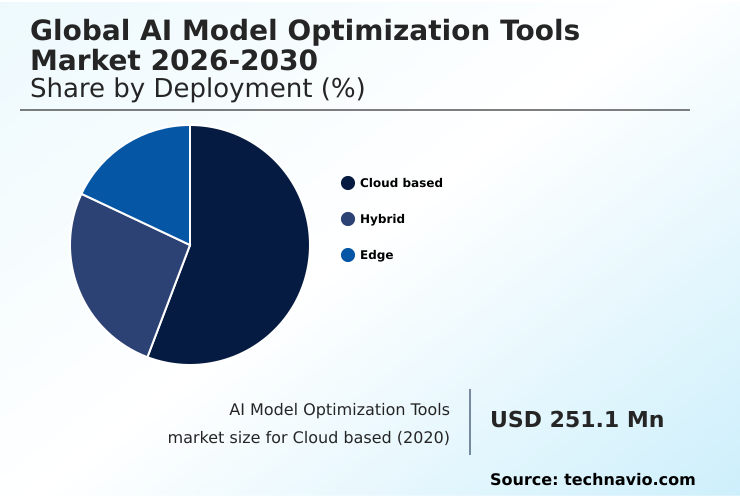

The cloud based segment is estimated to witness significant growth during the forecast period.

Cloud based deployment represents a primary segment of the AI model optimization tools market, as centralized data centers provide the vast computational resources necessary for large-scale training and refinement.

In this environment, optimization focuses on reducing the financial burden of high-end hardware utilization and increasing the throughput of complex machine learning models.

Cloud providers offer specialized toolchains to automate processes like knowledge distillation, enabling the creation of smaller, efficient models. This is particularly vital for managing inference cost reduction for generative AI inference.

With cloud based services projected to account for a significant share of the market, representing USD 597.9 million in 2025, the focus on AI accelerator utilization and model serving efficiency is paramount for achieving scalable enterprise AI strategy.

The Cloud based segment was valued at USD 501.5 million in 2024 and showed a gradual increase during the forecast period.

Ai Model Optimization Tools Market by Region: North America Leads with 40.6% Growth Share

North America is estimated to contribute 40.6% to the growth of the global market during the forecast period.

The geographic landscape is led by North America, which is projected to have a CAGR of 22.9% and holds a dominant market share due to its concentration of hyperscale data centers and foundational model developers.

This region focuses on inference cost reduction for cloud-based optimization.

In contrast, Europe, which accounts for 26.26% of the market opportunity, prioritizes AI regulatory compliance and green AI initiatives, driving demand for energy-efficient AI under frameworks like the EU AI Act.

APAC is the fastest-growing region, contributing 23.73% to market opportunity, with a strong emphasis on on-device AI deployment for mobile and consumer electronics, necessitating advanced model footprint reduction.

This regional diversity requires model portability solutions to address varying hardware and regulatory environments effectively.

Customer Landscape Analysis for the Ai Model Optimization Tools Market

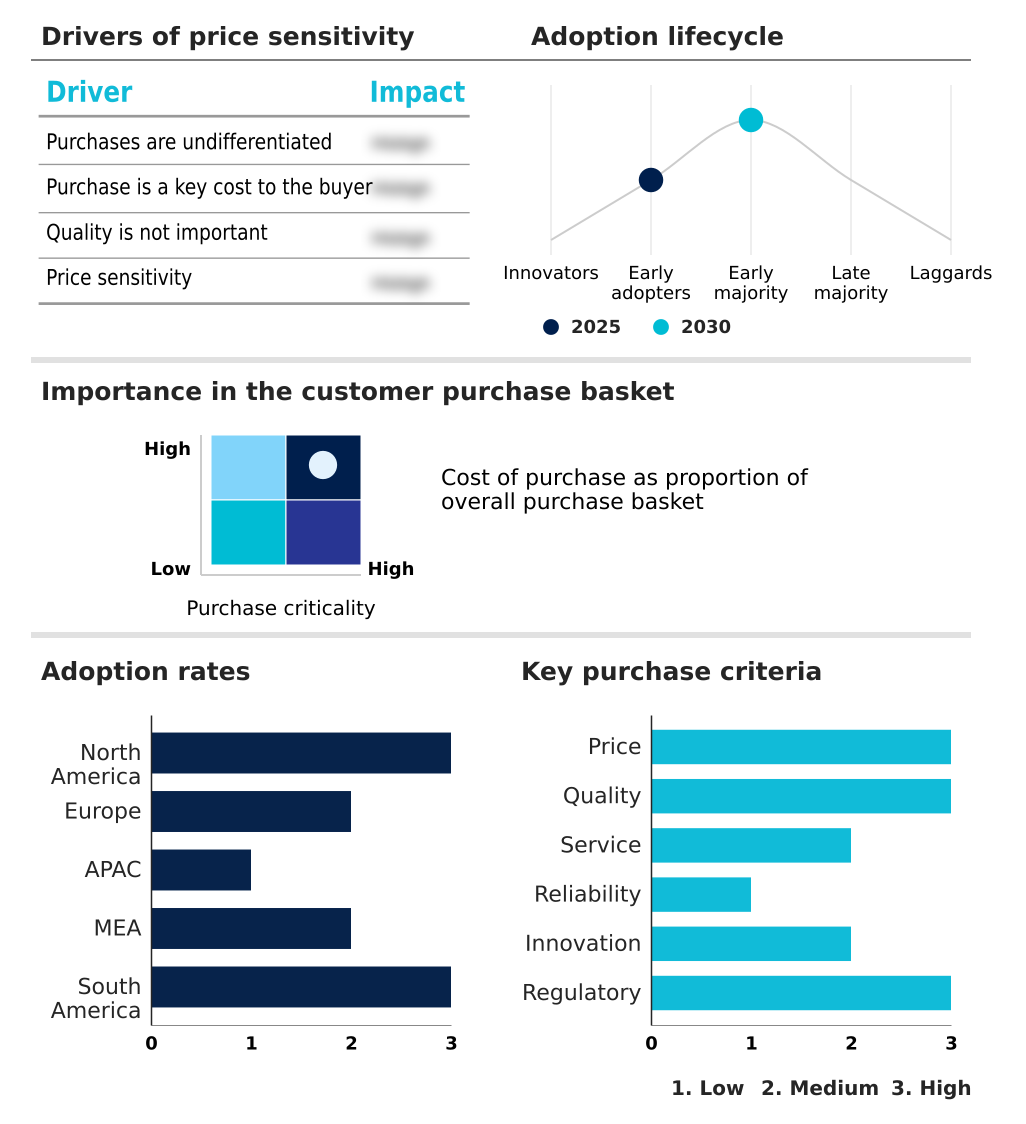

The ai model optimization tools market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai model optimization tools market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Ai Model Optimization Tools Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the ai model optimization tools market industry.

Advanced Micro Devices Inc. - Delivering AI model optimization through high-performance GPUs and an enabling software stack for efficient training and inference workloads across diverse AI applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Amazon.com Inc.

- Apple Inc.

- Arm Ltd.

- Baidu Inc.

- Blaize

- Cadence Design Systems Inc.

- Google LLC

- Hugging Face Inc.

- IBM Corp.

- Intel Corp.

- Latent AI Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Qualcomm Inc.

- Red Hat Inc.

- SAP SE

- Synopsys Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Ai Model Optimization Tools Market

- In August 2025, Meta Platforms released an enhanced version of the ExecuTorch framework, which introduced streamlined support for four-bit quantization across a wider range of mobile and embedded chipsets.

- In November 2025, Microsoft Corporation implemented a comprehensive energy-efficiency tracking system within the Azure AI model catalog, providing transparent metrics on the wattage consumed per inference task for various optimized architectures.

- In May 2025, Google Cloud integrated new hardware-aware optimization protocols into the Vertex AI platform which specifically target the latest generation of Tensor Processing Units.

- In May 2025, Arm Holdings introduced an updated version of the Ethos-U85 neural processing unit software suite, featuring hardware-native weight compression and automated pruning capabilities to reduce memory bandwidth for vision and voice tasks.

Research Analyst Overview: Ai Model Optimization Tools Market

The imperative to manage the escalating operational costs of large-scale generative intelligence is fundamentally reshaping enterprise IT strategy, making AI model optimization tools a central pillar of digital transformation. With the generative AI segment expanding rapidly, boardroom discussions now center on balancing capital expenditures on graphical processing units against the operational expenses of cloud services.

This requires a deep understanding of techniques like knowledge distillation and low-rank adaptation to ensure a positive return on investment. The technical trade-offs are significant; as highlighted in recent NIST reports, aggressive low-bit quantization can impact model fidelity, creating business risks that need careful management.

For procurement decision-makers, this translates to a complex evaluation of AI software stacks and AI accelerator hardware, moving beyond simple performance metrics to consider power consumption optimization and long-term sustainability. The goal is to achieve efficient model serving efficiency and latency reduction without compromising the accuracy needed for mission-critical real-time AI applications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ai Model Optimization Tools Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 318 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 22.1% |

| Market growth 2026-2030 | USD 1984.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 21.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, Israel, South Africa, Egypt, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Ai Model Optimization Tools Market: Key Questions Answered in This Report

-

What is the expected growth of the Ai Model Optimization Tools Market between 2026 and 2030?

-

The Ai Model Optimization Tools Market is expected to grow by USD 1.98 billion during 2026-2030, registering a CAGR of 22.1%. Year-over-year growth in 2026 is estimated at 21.6%%. This acceleration is shaped by proliferation of edge computing and internet of things hardware, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud based, Hybrid, and Edge), Application (Generative AI, Computer vision, NLP, and Others), End-user (IT and telecom, Automotive, Healthcare, BFSI, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America). Among these, the Cloud based segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, Middle East and Africa and South America. North America is estimated to contribute 40.6% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, Israel, South Africa, Egypt, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is proliferation of edge computing and internet of things hardware, which is accelerating investment and industry demand. The main challenge is hardware fragmentation and interoperability constraints, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Ai Model Optimization Tools Market?

-

Key vendors include Advanced Micro Devices Inc., Amazon.com Inc., Apple Inc., Arm Ltd., Baidu Inc., Blaize, Cadence Design Systems Inc., Google LLC, Hugging Face Inc., IBM Corp., Intel Corp., Latent AI Inc., Meta Platforms Inc., Microsoft Corp., NVIDIA Corp., Oracle Corp., Qualcomm Inc., Red Hat Inc., SAP SE and Synopsys Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Ai Model Optimization Tools Market Research Insights

Market dynamics are shaped by the dual pressures of performance demand and operational efficiency, with generative AI applications growing faster than computer vision. This necessitates sophisticated model performance benchmarking and adherence to emerging standards like the EU AI Act, which influences AI model governance.

Enterprises are increasingly adopting a hybrid cloud optimization strategy to balance security with scalability, particularly in regulated sectors like finance. For example, a bank might use a public cloud for model training but deploy a pruned and quantized version of the algorithm on-premises for real-time fraud detection, ensuring data privacy enhancement and compliance.

This approach addresses the total cost of ownership while supporting complex digital transformation projects, making AI deployment at scale a more achievable goal for risk-averse organizations.

We can help! Our analysts can customize this ai model optimization tools market research report to meet your requirements.

RIA -

RIA -