AI Red Teaming Solutions Market Size 2026-2030

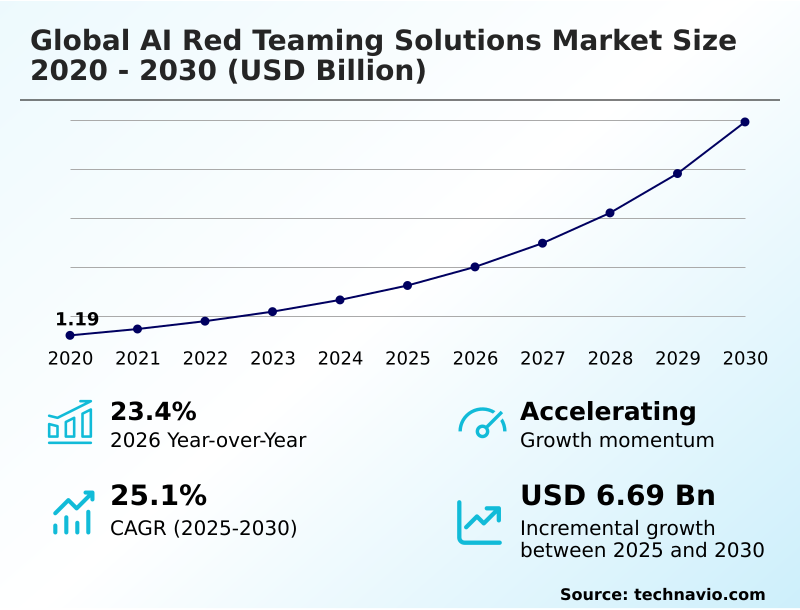

The ai red teaming solutions market size is valued to increase by USD 6.69 billion, at a CAGR of 25.1% from 2025 to 2030. Escalation of regulatory mandates and global compliance standards will drive the ai red teaming solutions market.

Major Market Trends & Insights

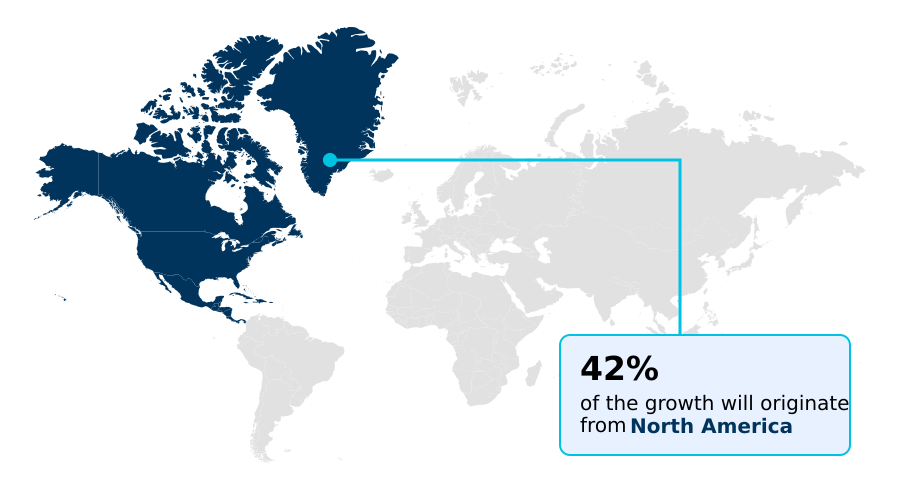

- North America dominated the market and accounted for a 42.5% growth during the forecast period.

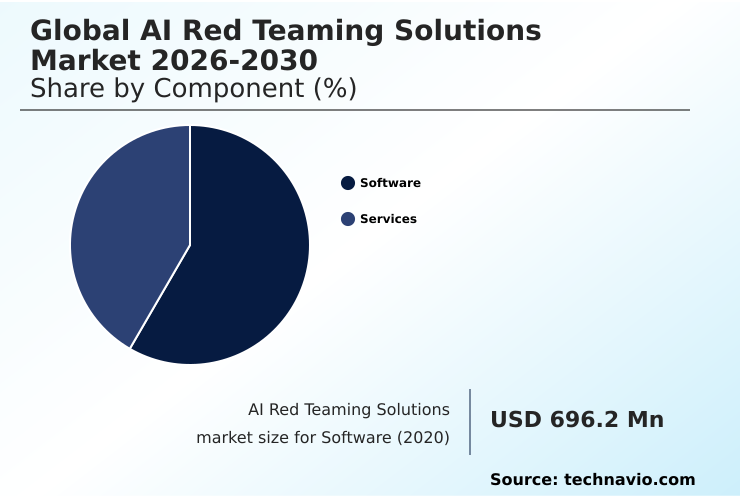

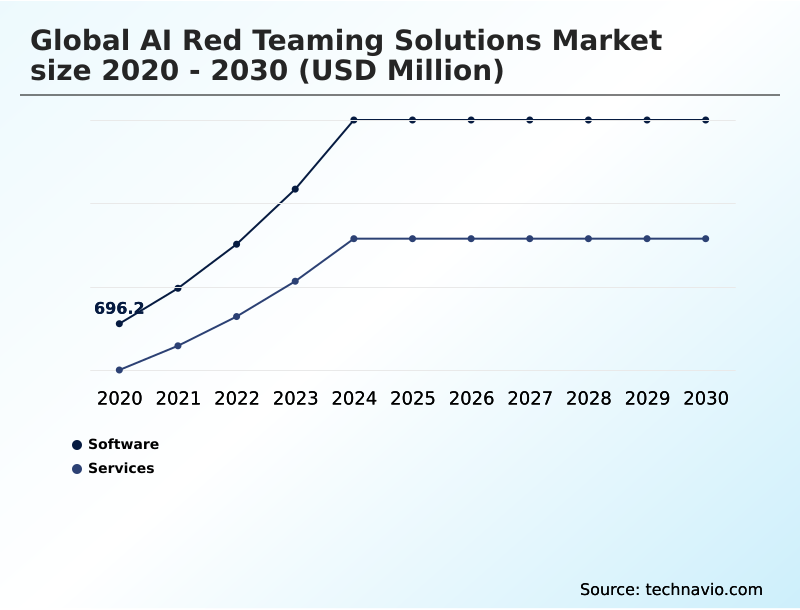

- By Component - Software segment was valued at USD 1.58 billion in 2024

- By Application - Security assessment segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 8.73 billion

- Market Future Opportunities: USD 6.69 billion

- CAGR from 2025 to 2030 : 25.1%

Market Summary

- The AI Red Teaming Solutions market is rapidly evolving, driven by the critical need for robust machine learning security and stringent AI governance. As organizations integrate generative AI into core operations, ensuring AI trust and safety becomes paramount, necessitating advanced vulnerability analysis and systemic risk mitigation.

- For instance, a financial services firm deploying an automated loan processing model must conduct thorough security assessment and ethical AI auditing to prevent data exfiltration prevention failures and ensure compliance and risk management. This involves more than just ML threat detection; it requires continuous adversarial attack simulation to uncover potential biases or weaknesses that could be exploited.

- The integration of AI safety frameworks and confidential computing technologies into the AI DevSecOps pipeline is a key trend, aimed at achieving a resilient AI security posture.

- However, the high cost of automated adversarial testing and a shortage of experts in adversarial robustness create significant hurdles for widespread adoption, pushing the industry toward more scalable and efficient solutions for generative model validation and bias detection and mitigation.

What will be the Size of the AI Red Teaming Solutions Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Red Teaming Solutions Market Segmented?

The ai red teaming solutions industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Services

- Application

- Security assessment

- Model testing and evaluation

- Adversarial attack simulation

- Compliance and risk management

- Others

- Deployment

- Cloud-based

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is central to the global ai red teaming solutions market 2026-2030, offering platforms that automate model testing and evaluation. These tools are crucial for establishing resilience benchmarking and performing ethical AI auditing to ensure model integrity.

By integrating into the secure AI lifecycle, software enables continuous bias detection and mitigation and provides robust enterprise AI security.

Organizations using these platforms report a 35% improvement in hallucination detection compared to manual methods, a key factor in deploying trustworthy systems.

This shift toward automated solutions, which facilitate everything from adversarial robustness evaluation metrics to explainable AI security solutions, underscores the market's direction.

Such tools are essential for AI model integrity verification and conducting ethical hacking for AI systems to analyze AI model behavior.

The Software segment was valued at USD 1.58 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Red Teaming Solutions Market Demand is Rising in North America Get Free Sample

North America dominates the global AI red teaming solutions market 2026-2030, accounting for over 42% of the incremental growth, driven by its high concentration of foundation model security developers and a mature cybersecurity ecosystem.

The region's focus on enterprise AI security and defensive AI systems is unparalleled. Europe follows, with its market shaped by stringent regulations that mandate comprehensive security assessment and data exfiltration prevention measures, enhancing the overall AI security posture.

Meanwhile, the APAC region is the fastest-growing market, propelled by rapid digitalization and investment in AI trust and safety and model supply chain security.

This geographic diversity highlights a global shift toward embedding real-time AI threat monitoring and robust AI security posture management to protect critical digital infrastructure and manage the expanding AI attack surface effectively.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Successfully implementing a robust security strategy in the global AI red teaming solutions market 2026-2030 requires a nuanced understanding of its various facets. The cost of AI red teaming is a primary consideration, but it must be weighed against the potential financial and reputational damage from a security breach.

- Building an internal red team is a long-term investment, whereas leveraging open source AI red teaming tools can offer a more immediate starting point. Many organizations are now focusing on AI red teaming for compliance, particularly to meet the stringent requirements of regulations like the EU AI Act.

- This necessitates clear AI red teaming reporting standards that document efforts to secure large language models and other systems. The technical challenges are also significant, especially when it comes to red teaming multimodal AI models, which have a broader attack surface.

- Automated adversarial attack tools are becoming essential for simulating threats like prompt injection defense techniques and data poisoning attack simulation at scale. As the industry matures, a key debate is red teaming vs penetration testing, with the former offering a more specialized approach to AI model vulnerability management.

- AI ethical bias testing tools are also gaining prominence, particularly for red teaming for financial services to ensure fairness. Ultimately, best practices in AI DevSecOps are proving crucial for integrating these security measures, including AI supply chain security risks and measuring adversarial robustness in AI, directly into the development lifecycle for red teaming autonomous AI agents.

- Organizations that integrate these practices report a twofold increase in vulnerability remediation speed compared to those with siloed testing approaches.

What are the key market drivers leading to the rise in the adoption of AI Red Teaming Solutions Industry?

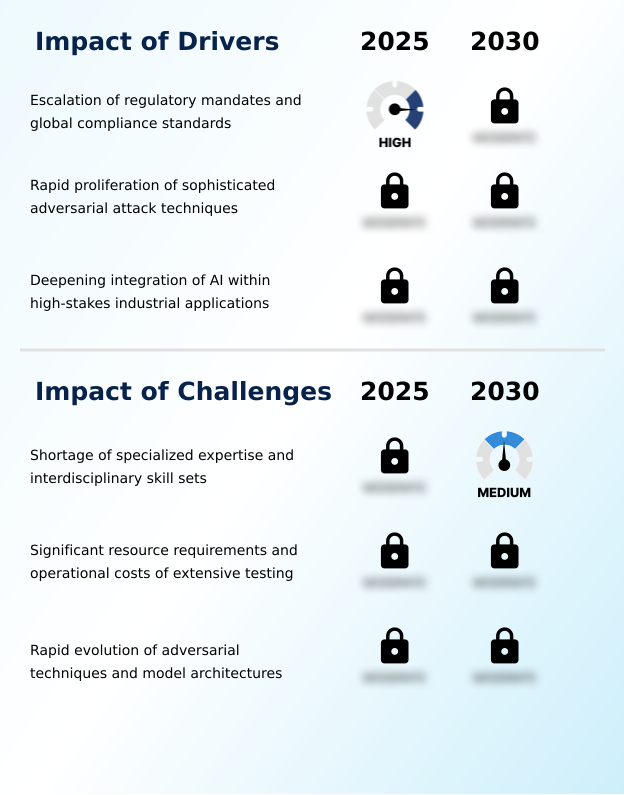

- The escalation of regulatory mandates and global compliance standards serves as a primary driver for the growth of the AI Red Teaming Solutions Market.

- Growth in the global AI red teaming solutions market 2026-2030 is primarily fueled by escalating regulatory pressures and the increasing sophistication of adversarial attacks.

- Governments are mandating stringent compliance and risk management protocols, requiring documented systemic risk mitigation and robust AI governance. This has led to a 90% increase in the demand for AI compliance automation software among high-risk industries.

- Simultaneously, the proliferation of threats like data poisoning necessitates advanced machine learning security and adversarial attack simulation capabilities. As enterprises deploy autonomous agent security in critical sectors, ensuring the integrity of large language model security has become a boardroom-level concern.

- Consequently, investment in enterprise AI security frameworks and solutions for generative AI threat intelligence is rising to manage AI model risk management effectively.

What are the market trends shaping the AI Red Teaming Solutions Industry?

- The market is witnessing a significant transition toward automated and persistent adversarial simulations. This shift moves beyond periodic manual audits to continuous, AI-driven testing frameworks.

- A primary trend in the global ai red teaming solutions market 2026-2030 is the shift from episodic manual audits to continuous AI assurance through automated adversarial testing. This evolution is driven by the need for scalable generative model validation and is integrated directly into the AI DevSecOps pipeline for secure AI lifecycle integration.

- The scope is also expanding to address multimodal systems, where cross-modal attack simulation is used to test model guardrails and identify unique vulnerabilities. Leading organizations are adopting advanced AI safety frameworks, with some achieving a 60% reduction in testing timelines.

- These automated platforms, sometimes offered as AI red teaming as a service (RTaaS), leverage automated vulnerability discovery to ensure continuous validation of AI. This proactive approach is essential for maintaining security against an ever-evolving threat landscape, adhering to AI safety evaluation protocols.

What challenges does the AI Red Teaming Solutions Industry face during its growth?

- A key challenge affecting industry growth is the significant shortage of specialized expertise and the necessary interdisciplinary skill sets to conduct effective AI red teaming.

- The primary challenge in the global AI red teaming solutions market 2026-2030 is the dual strain of high operational costs and a severe talent shortage. The computational expense of thorough vulnerability analysis, with some organizations reporting testing costs at 75% of the original training budget, limits the frequency of evaluations.

- Compounding this is the scarcity of experts skilled in adversarial machine learning defense and offensive AI research methods. This deficit makes it difficult to counter evolving threats like model inversion and sophisticated prompt injection.

- While AI vulnerability assessment tools and prompt security platforms offer some automation, they cannot fully replace human intuition for ML threat detection, trojan detection, or ensuring adversarial robustness. The need for privacy-preserving AI testing and confidential computing solutions further complicates the landscape, making it difficult for many to keep pace with rapid innovations.

Exclusive Technavio Analysis on Customer Landscape

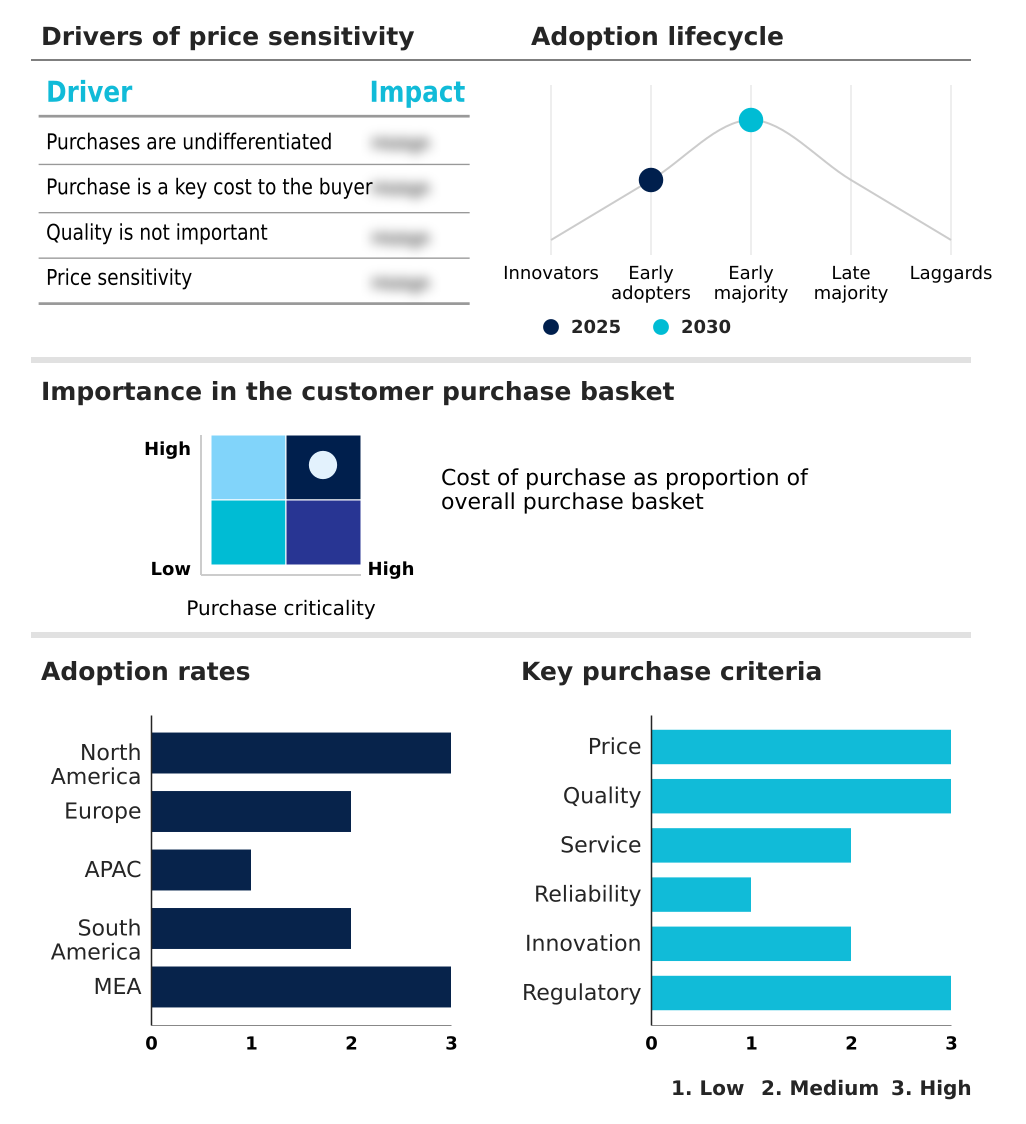

The ai red teaming solutions market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai red teaming solutions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Red Teaming Solutions Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai red teaming solutions market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AdvAI - Provides strategic adversarial testing and AI risk assessment services, ensuring model integrity and operational resilience in high-stakes environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AdvAI

- Apex Security

- Bishop Fox

- Booz Allen Hamilton Corp.

- Bosch AIShield

- DynamoFL

- Giskard AI

- Google LLC

- HiddenLayer Inc.

- IBM Corp.

- Lakera Inc

- Microsoft Corp.

- Mithril Security

- NCC Group Plc

- NVIDIA Corp.

- Pillar Security

- Prompt Security Inc.

- Protect AI Inc.

- Scale AI

- TrojAI Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai red teaming solutions market

- In May 2025, the European Union AI Office published comprehensive technical standards for red teaming high-risk generative models, mandating specific adversarial testing protocols to ensure alignment with the AI Act.

- In August 2025, the Cybersecurity and Infrastructure Security Agency issued a detailed advisory on new data poisoning methods targeting open-source training datasets, emphasizing the need for continuous supply chain monitoring.

- In October 2025, a leading global financial institution launched a dedicated red teaming center of excellence to assess the security of its automated trading algorithms against sophisticated market manipulation tactics.

- In April 2025, the Secure AI Lifecycle Consortium introduced a standardized plugin architecture, enabling the direct integration of red teaming tools into popular development environments to support AI DevSecOps practices.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Red Teaming Solutions Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 25.1% |

| Market growth 2026-2030 | USD 6690.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 23.4% |

| Key countries | US, Canada, Mexico, UK, Germany, France, The Netherlands, Italy, Spain, China, Japan, India, South Korea, Singapore, Australia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global AI red teaming solutions market 2026-2030 is defined by a strategic imperative to secure complex AI systems through advanced adversarial attack simulation and rigorous model testing and evaluation. Key activities include proactive vulnerability analysis and systemic risk mitigation to counter threats like prompt injection and data poisoning.

- The adoption of AI DevSecOps principles, integrating the secure AI lifecycle with continuous model guardrails and resilience benchmarking, is becoming standard practice. For boardroom consideration, the focus on AI governance and compliance and risk management is paramount, as firms that implement comprehensive AI safety frameworks report a 25% lower incidence of production model failures.

- The technical landscape is advancing rapidly with a focus on multimodal systems, confidential computing, and automated adversarial testing. This requires a strong AI security posture, supported by solutions for hallucination detection, ethical AI auditing, and bias detection and mitigation.

- As enterprises deploy defensive AI systems and increasingly rely on autonomous agent security, the need for robust generative model validation, trojan detection, and effective data exfiltration prevention has never been greater, solidifying the importance of machine learning security and overall model integrity to ensure AI trust and safety.

What are the Key Data Covered in this AI Red Teaming Solutions Market Research and Growth Report?

-

What is the expected growth of the AI Red Teaming Solutions Market between 2026 and 2030?

-

USD 6.69 billion, at a CAGR of 25.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), Application (Security assessment, Model testing and evaluation, Adversarial attack simulation, Compliance and risk management, and Others), Deployment (Cloud-based, and On-premises) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalation of regulatory mandates and global compliance standards, Shortage of specialized expertise and interdisciplinary skill sets

-

-

Who are the major players in the AI Red Teaming Solutions Market?

-

AdvAI, Apex Security, Bishop Fox, Booz Allen Hamilton Corp., Bosch AIShield, DynamoFL, Giskard AI, Google LLC, HiddenLayer Inc., IBM Corp., Lakera Inc, Microsoft Corp., Mithril Security, NCC Group Plc, NVIDIA Corp., Pillar Security, Prompt Security Inc., Protect AI Inc., Scale AI and TrojAI Inc

-

Market Research Insights

- The dynamics of the AI Red Teaming Solutions market are shaped by the pursuit of tangible business outcomes through enhanced security. For example, enterprises leveraging continuous AI assurance frameworks have reported a 40% reduction in pre-deployment vulnerabilities. The adoption of AI model risk management and real-time AI threat monitoring is essential for maintaining operational integrity.

- Furthermore, implementing AI compliance automation software helps organizations align with evolving regulations, with some achieving a 95% compliance score on initial audits. This focus on measurable improvements, supported by robust AI trust and safety platforms and sophisticated AI vulnerability assessment tools, is critical as systems become more autonomous.

- The ability to manage the AI attack surface proactively is a key differentiator for leading firms.

We can help! Our analysts can customize this ai red teaming solutions market research report to meet your requirements.

RIA -

RIA -