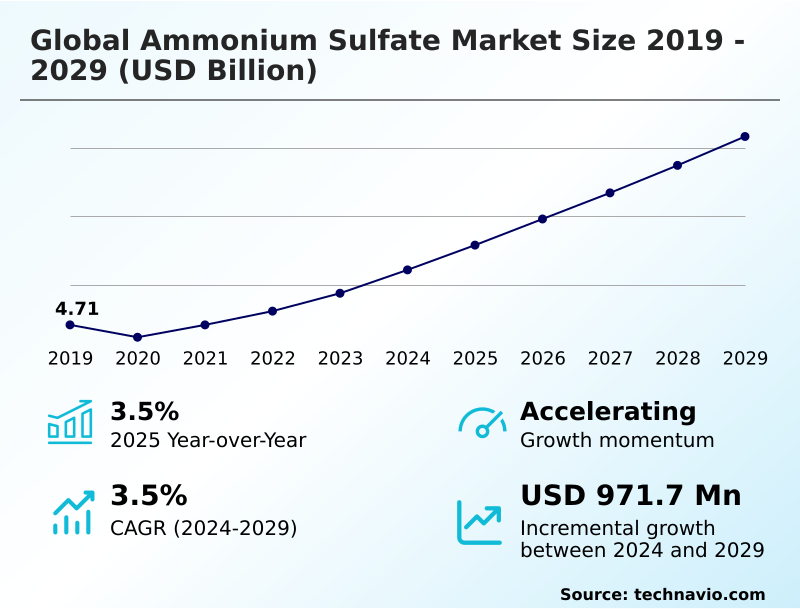

Ammonium Sulfate Market Size 2025-2029

The ammonium sulfate market size is valued to increase by USD 971.7 million, at a CAGR of 3.5% from 2024 to 2029. Growing global food demand will drive the ammonium sulfate market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 53.5% growth during the forecast period.

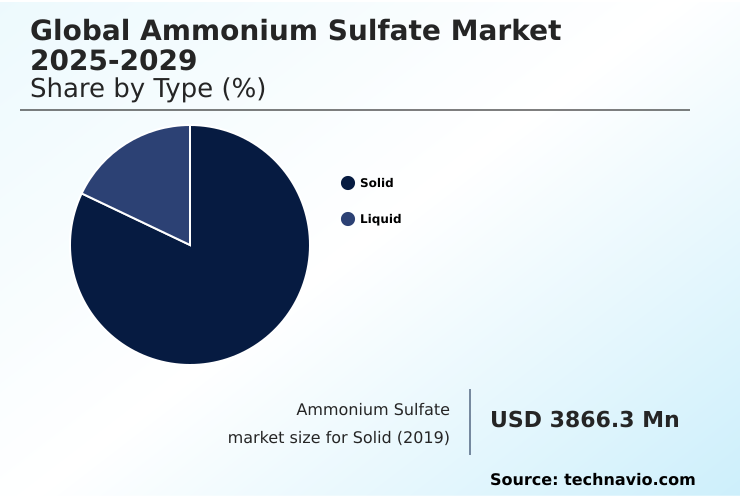

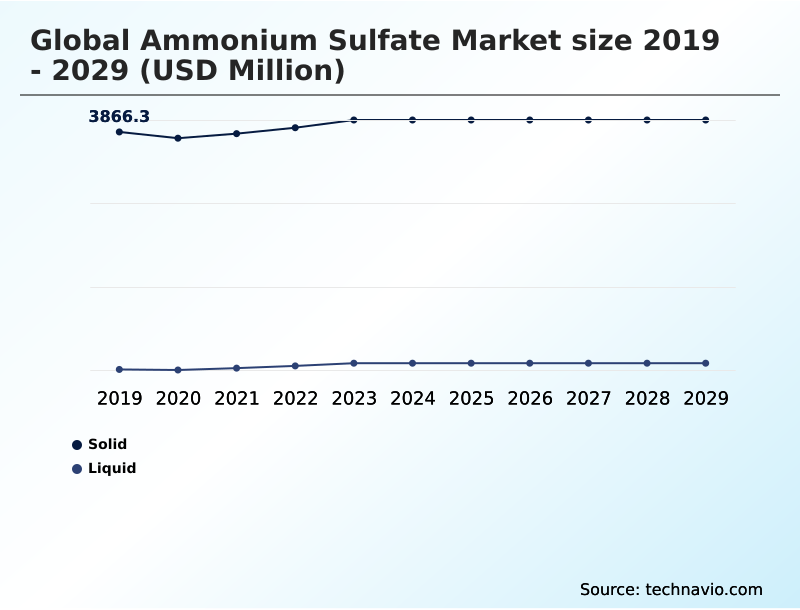

- By Type - Solid segment was valued at USD 4.02 billion in 2023

- By Application - Fertilizers segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.37 billion

- Market Future Opportunities: USD 971.7 million

- CAGR from 2024 to 2029 : 3.5%

Market Summary

- The ammonium sulfate market is shaped by a unique dual-supply structure, balancing byproduct streams from industrial manufacturing with on-purpose synthetic production. This dynamic creates distinct economic considerations for market participants. The primary demand driver remains the agricultural sector's unceasing need to improve crop yields through balanced nutrition, particularly by addressing widespread sulfur deficiencies in soil.

- As a fertilizer, it provides both nitrogen and sulfur in a plant-available form. Trends such as precision agriculture are increasing demand for high-solubility and liquid grades, while a growing emphasis on the circular economy enhances the value of byproduct material.

- For instance, a fertilizer blending company must navigate the supply-side complexities, where a slowdown in steel or chemical production could constrain the availability of cost-effective byproduct ammonium sulfate, forcing a pivot to potentially more expensive synthetic alternatives and impacting operational cost structures.

- Simultaneously, the market contends with intense competition from other nitrogen fertilizers and increasing regulatory scrutiny over nutrient management and environmental impact.

What will be the Size of the Ammonium Sulfate Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Ammonium Sulfate Market Segmented?

The ammonium sulfate industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Solid

- Liquid

- Application

- Fertilizers

- Food and feed additive

- Pharmaceuticals

- Water treatment

- Others

- Production area

- Synthetic production

- By-product production

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The solid segment is estimated to witness significant growth during the forecast period.

The solid segment, primarily comprising crystalline ammonium sulfate and granular ammonium sulfate, is central to the market's structure, driven by logistical efficiency in transport and storage.

As an agricultural grade fertilizer, its role in bulk blended fertilizer formulations is critical for improving nitrogen use efficiency and crop nutrient uptake.

The segment's stability is supported by byproduct fertilizer economics, where industrial byproduct valuation of material from sources like steel industry co-products makes it a cost-effective agricultural soil amendment.

This form accounts for over 81% of the total market volume, underscoring its dominance.

Beyond agriculture, industrial grade ammonium sulfate serves various sectors, while specialized forms are used as a food and feed grade additive, showcasing the material's versatility and strong position established through sound agronomic best practices.

The Solid segment was valued at USD 4.02 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 53.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ammonium Sulfate Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by APAC, which accounts for over 53% of the market's incremental growth, fueled by its vast agricultural sector and large-scale industrial byproduct capacity.

The region's growth rate of 4.2% significantly outpaces that of mature markets like North America and Europe. In these Western regions, demand is driven by advanced agricultural practices and the need for specialty products.

In contrast, South America, particularly Brazil, represents a high-growth market heavily reliant on imports to support its expanding cultivation of commodity crops. The soil acidification effect of the product is a key consideration in this region.

Industrial applications, including its use as a non-protein nitrogen source in animal feed or as a chemical intermediate for a pharmaceutical processing aid, also contribute to demand.

Strategic decisions are increasingly influenced by environmental, social, and governance (ESG) factors, impacting production and sourcing across all regions, including its use in water treatment chemistry and the chloramination process.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the ammonium sulfate market requires a nuanced understanding of both agricultural and industrial value chains. The debate over ammonium sulfate vs urea for corn is a recurring theme in agronomy, with choices influenced by soil type and the need for sulfur.

- Application methods also vary, with granular vs liquid ammonium sulfate application being a key consideration for farmers investing in precision agriculture. The market's supply side is complex; byproduct ammonium sulfate quality standards are critical for producers in the caprolactam and steel industries. Understanding the ammonium sulfate production from caprolactam is essential for forecasting supply.

- The price of ammonium sulfate per ton is closely watched, as it dictates the cost-effectiveness of byproduct fertilizers. From a use-case perspective, using ammonium sulfate in alkaline soils is a primary agricultural benefit, particularly for high sulfur crops.

- The ammonium sulfate supply chain logistics are a major factor in regional pricing, with firms that manage nutrient runoff from ammonium sulfate more effectively gaining a compliance advantage. This is crucial as regulatory limits on nitrogen fertilizer use become stricter.

- In industrial sectors, the role of ammonium sulfate in baking and its function as a fire retardant represent stable demand segments. The benefits of ammonium sulfate in fertigation are driving growth in the specialty agriculture sector. Further, the use of ammonium sulfate in pharmaceutical protein precipitation and for turfgrass management showcases its versatility.

- Proper blending of ammonium sulfate with other fertilizers and its role in water treatment disinfection highlight its importance beyond farming.

What are the key market drivers leading to the rise in the adoption of Ammonium Sulfate Industry?

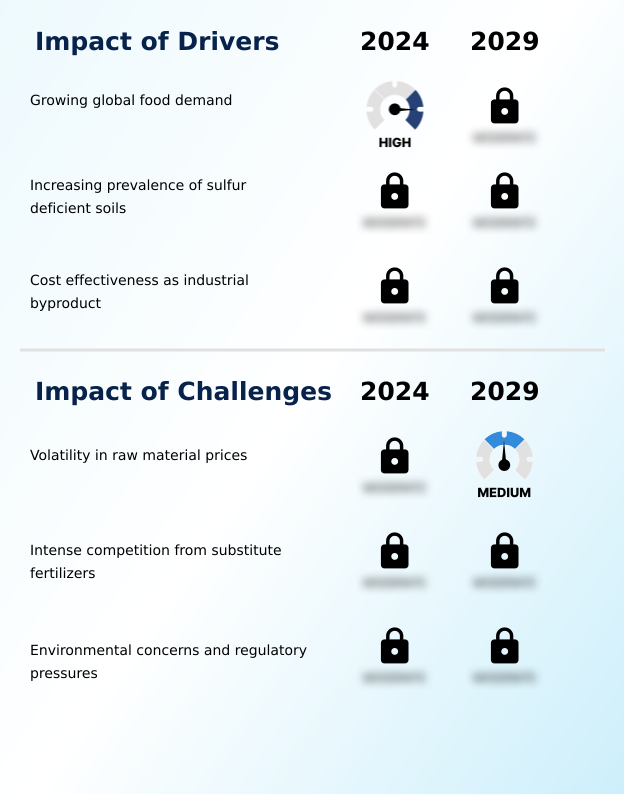

- The fundamental need to enhance agricultural productivity to meet growing global food demand serves as the primary driver for the market.

- Market growth is fundamentally driven by the dual imperatives of agricultural productivity and industrial sustainability.

- As a potent nitrogen and sulfur fertilizer, ammonium sulfate directly addresses the widespread issue of sulfur deficient soil correction, with balanced fertilization capable of boosting crop yields by 10-20% in affected areas.

- The product's high solubility fertilizer characteristics, providing both ammoniacal nitrogen and sulfate sulfur nutrient, make it ideal for modern farming. A major economic driver is its production as a caprolactam byproduct, a cornerstone of the circular economy in chemicals.

- This byproduct route, resulting from the beckmann rearrangement byproduct in caprolactam manufacturing, is significantly less energy-intensive than direct synthesis production.

- This inherent cost advantage makes it a preferred choice for alkaline soil treatment and enhances sulfur nutrition for crops, aligning economic benefits with environmental advantages.

What are the market trends shaping the Ammonium Sulfate Industry?

- A prominent trend is the agricultural industry's shift toward balanced fertilization, moving beyond primary macronutrients. This holistic approach emphasizes the critical role of secondary nutrients like sulfur for optimizing crop health and yield.

- Key market trends are driving a shift toward more sophisticated nutrient management. The adoption of precision agriculture application technologies, including variable rate technology (VRT), is boosting demand for high-quality liquid fertilizer solution and fertigation-grade soluble salt products. This approach enhances the delivery of plant available sulfur, with some systems improving nutrient placement efficiency by up to 25%.

- A robust nutrient management plan now frequently incorporates a soil pH regulator to optimize growing conditions. Furthermore, the push for sustainable agriculture inputs is increasing the use of advanced NPK+S formulation products and customized fertilizer blending, which can reduce nutrient waste by over 15%.

- The versatility of the product is also seen in its use as a foliar spray nutrient, offering another route for targeted fertigation systems and liquid fertilizer formulation.

What challenges does the Ammonium Sulfate Industry face during its growth?

- Significant price volatility in key raw materials, namely ammonia and sulfuric acid, presents a key challenge to market stability and producer profitability.

- The market faces significant headwinds from input cost instability and competitive pressures. The volatility in synthetic ammonia price and sulfuric acid cost directly impacts producers, with price swings of over 30% in a single quarter creating profound margin uncertainty. This raw material price volatility makes long-term planning difficult.

- Furthermore, intense fertilizer substitute competition, primarily from higher-nitrogen products, requires continuous value-based selling focused on the product's secondary nutrient benefits. On the regulatory front, concerns over nutrient runoff mitigation are leading to stricter environmental controls, such as the carbon border adjustment mechanism, which could increase compliance costs.

- Beyond agriculture, byproduct streams from coke oven gas purification and flue gas desulfurization product must meet quality standards for diverse applications, including as a water disinfectant agent, flame retardant composition, and even as a dough conditioner agent or yeast nutrient for baking.

Exclusive Technavio Analysis on Customer Landscape

The ammonium sulfate market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ammonium sulfate market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ammonium Sulfate Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ammonium sulfate market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arkema Group - Offerings center on versatile ammonium sulfate for agricultural nutrient management and diverse industrial processes, addressing both crop nutrition and technical chemical requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arkema Group

- BASF SE

- China Petrochemical Corp.

- Domo Chemicals GmbH

- DSM Firmenich AG

- Evonik Industries AG

- Honeywell International Inc.

- Indorama Ventures Public Co. Ltd.

- Lanxess AG

- Martin Midstream Partners L.P.

- Nutrien Ltd.

- Solvay SA

- Sumitomo Chemical Co. Ltd.

- Ube Corp.

- Yara International ASA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ammonium sulfate market

- In September, 2024, Evonik Industries AG announced the launch of a new high-purity, soluble-grade ammonium sulfate, specifically engineered for advanced fertigation systems in high-value horticulture, enhancing nutrient delivery precision.

- In November, 2024, Nutrien Ltd. completed the acquisition of a regional fertilizer blending and distribution company, expanding its logistical footprint to improve the supply of customized NPK+S formulations to key agricultural zones.

- In February, 2025, Lanxess AG reported the successful completion of a capacity expansion project at its European facility, increasing its output of byproduct ammonium sulfate by 15% to meet rising demand from the agricultural sector.

- In April, 2025, BASF SE entered into a strategic partnership with a green energy firm to pilot a new production process for low-carbon ammonium sulfate, utilizing green hydrogen to reduce the carbon footprint of synthetic ammonia feedstock.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ammonium Sulfate Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.5% |

| Market growth 2025-2029 | USD 971.7 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 3.5% |

| Key countries | China, India, Japan, Indonesia, South Korea, Australia, Germany, France, UK, The Netherlands, Spain, Italy, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ammonium sulfate market operates on a complex interplay between industrial symbiosis and agricultural necessity. Its production as a caprolactam byproduct or through coke oven gas purification underpins a significant portion of the global supply, offering a cost-effective agricultural grade fertilizer.

- Firms utilizing byproduct streams report a cost of goods sold that is on average 15-20% lower than those relying on synthetic production. This dual-source dynamic influences everything from supply chain stability to pricing. Agronomically, the product's value lies in delivering both ammoniacal nitrogen and sulfate sulfur nutrient, making it ideal for sulfur deficient soil correction and improving crop nutrient uptake.

- The plant available sulfur it contains enhances overall nitrogen use efficiency. The market is segmented into crystalline ammonium sulfate and granular ammonium sulfate for various applications, including as a key ingredient in NPK+S formulation for a nutrient management plan.

- Beyond the farm, it serves as an industrial grade ammonium sulfate in applications such as a flame retardant composition, a water disinfectant agent, and as a protein purification reagent via the salting out technique in biotech. It is also used as a dough conditioner agent and yeast nutrient for baking.

- The market's future hinges on balancing the economics of direct synthesis production against byproduct streams while promoting its benefits as a soil pH regulator and a component in high-solubility fertilizer solutions.

What are the Key Data Covered in this Ammonium Sulfate Market Research and Growth Report?

-

What is the expected growth of the Ammonium Sulfate Market between 2025 and 2029?

-

USD 971.7 million, at a CAGR of 3.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Solid, and Liquid), Application (Fertilizers, Food and feed additive, Pharmaceuticals, Water treatment, and Others), Production Area (Synthetic production, and By-product production) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing global food demand, Volatility in raw material prices

-

-

Who are the major players in the Ammonium Sulfate Market?

-

Arkema Group, BASF SE, China Petrochemical Corp., Domo Chemicals GmbH, DSM Firmenich AG, Evonik Industries AG, Honeywell International Inc., Indorama Ventures Public Co. Ltd., Lanxess AG, Martin Midstream Partners L.P., Nutrien Ltd., Solvay SA, Sumitomo Chemical Co. Ltd., Ube Corp. and Yara International ASA

-

Market Research Insights

- Market dynamics are defined by the pursuit of agricultural efficiency and sustainable industrial practices. The adoption of advanced agronomic practices leads to a greater emphasis on dual nutrient fertilizers that can correct specific soil deficiencies. This shift improves nutrient uptake by up to 15%, directly enhancing crop yields.

- The economics of byproduct production, a core component of the circular economy in chemicals, allows for a more competitive cost structure compared to purely synthetic routes. For instance, leveraging byproduct streams can reduce the overall energy intensity of fertilizer manufacturing by over 30%.

- However, the market is constrained by intense fertilizer substitute competition and significant raw material price volatility, which can impact producer margins and create pricing uncertainty for end-users. Firms must navigate these competing forces by emphasizing the agronomic value and cost-effectiveness of their products.

We can help! Our analysts can customize this ammonium sulfate market research report to meet your requirements.

RIA -

RIA -