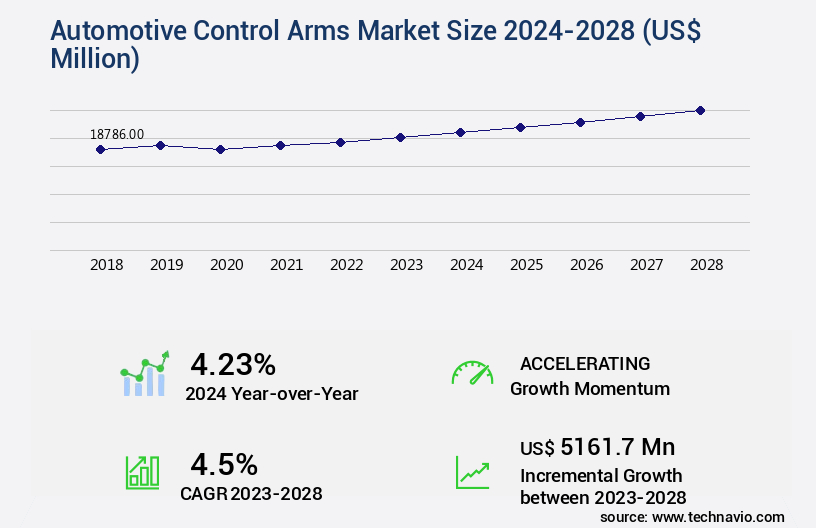

Automotive Control Arms Market Size 2024-2028

The automotive control arms market size is valued to increase USD 5.16 billion, at a CAGR of 4.5% from 2023 to 2028. Low cost of automotive control arms will drive the automotive control arms market.

Major Market Trends & Insights

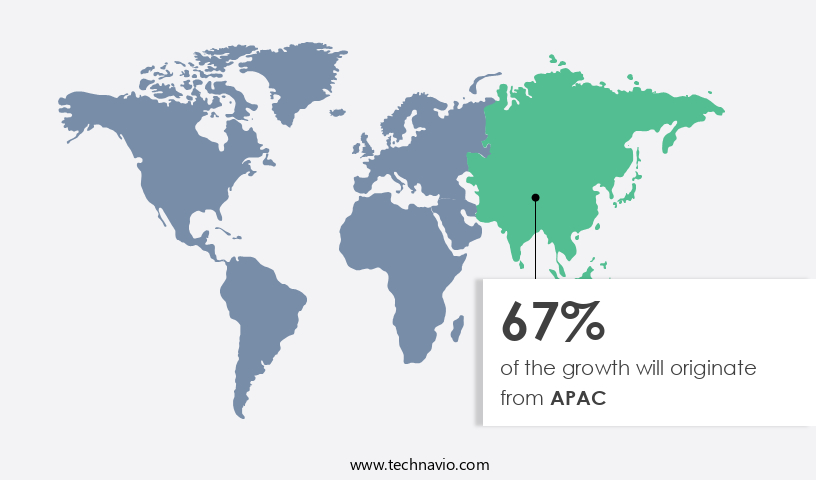

- APAC dominated the market and accounted for a 67% growth during the forecast period.

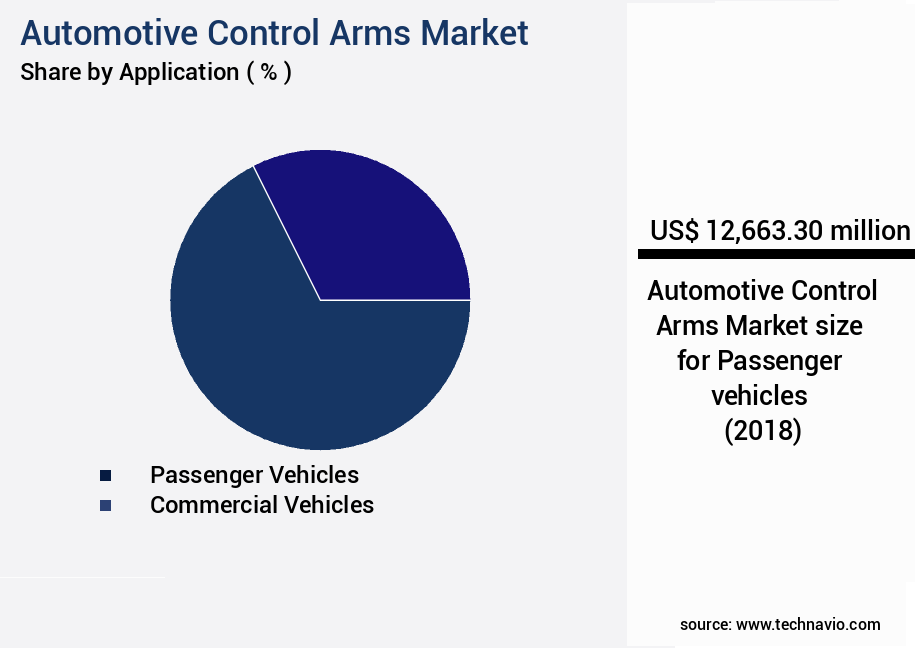

- By Application - Passenger vehicles segment was valued at USD 12.66 billion.

Market Size & Forecast

- Market Opportunities: USD 39.18 million

- Market Future Opportunities: USD 5161.70 million

- CAGR : 4.5%

Market Summary

- The market encompasses the production and distribution of control arms for various vehicle makes and models. Core technologies, such as the use of lightweight and energy-efficient materials in automotive suspension systems, are driving market growth. For instance, Magna International, a leading automotive supplier, reported a 12% increase in sales of suspension and steering components in 2020. However, challenges persist, including the rising cost of automotive control arms and the risk of faulty control arms leading to vehicle recalls.

- Regulations, such as the European Union's Regulation (EC) No. 764/2008 on the approval and market surveillance of vehicles and their trailers, continue to shape market dynamics. In 2021, The market is expected to witness significant expansion, with Asia Pacific emerging as a major growth region due to increasing vehicle production and sales in countries like China and India.

What will be the Size of the Automotive Control Arms Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Automotive Control Arms Market Segmented and what are the key trends of market segmentation?

The automotive control arms industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

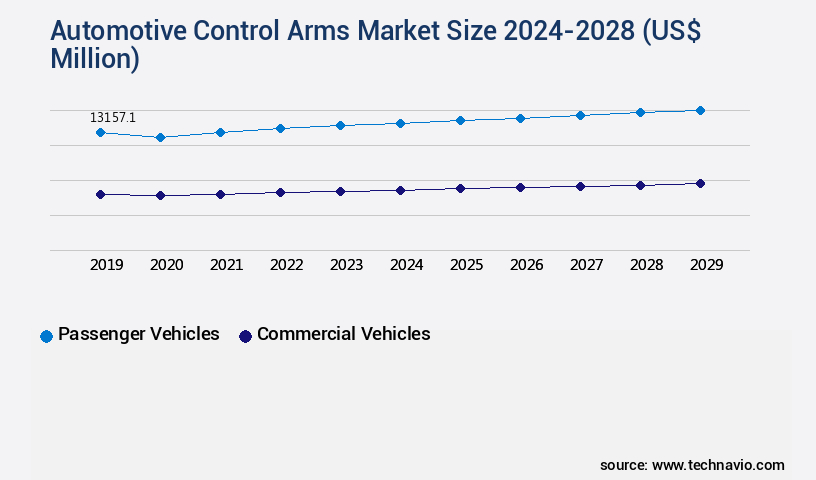

- Passenger vehicles

- Commercial vehicles

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Application Insights

The passenger vehicles segment is estimated to witness significant growth during the forecast period.

The market experiences significant growth, with passenger vehicles representing the largest market segment in 2023. This trend is driven by the increasing sales volume of passenger vehicles, particularly in emerging economies like China, India, and Southeast Asian nations. For instance, China's passenger car sales grew by 5.6% year-on-year (Y-O-Y) to 21.7 million units in 2023. Control arms are essential components in both front and rear suspension systems for passenger vehicles. Furthermore, the rising market share of mid-segment and luxury-segment sedans and SUVs contributes to the growth of the passenger vehicles segment. Regarding component design, safety standards and component lifespan are crucial factors.

Road handling and ball joint design significantly impact kinematic properties, vibration damping, and weight optimization. Control arm bushings, quality control, and dynamic response are essential aspects of suspension system design. Corrosion resistance, manufacturing processes, and NVH performance are key considerations for casting methods, lateral control arms, and steering knuckles. Impact absorption and braking system integration are essential for ensuring safety and optimal performance. Torque specifications and load capacity are essential factors in control arm design. Welding techniques and installation procedures are crucial for ensuring structural stiffness and component durability. Failure analysis, suspension geometry, control arm alignment, fatigue strength testing, and finite element analysis are essential for maintaining high-quality control and improving ride comfort.

In the future, the market is expected to grow further, with a focus on enhancing control arm performance, reducing weight, and improving NVH characteristics. Material science advancements and forging techniques will play a significant role in achieving these goals. Bushings material and component durability will continue to be essential factors in the market's evolution.

The Passenger vehicles segment was valued at USD 12.66 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 67% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Control Arms Market Demand is Rising in APAC Request Free Sample

The market in APAC is experiencing substantial expansion, fueled by the increasing sales volume of automobiles in countries like China, Japan, South Korea, and India. The economic advancements and enhanced purchasing power parity in these nations have led to a significant demand for both passenger and commercial vehicles. As a result, China, Japan, South Korea, India, and ASEAN countries are major contributors to the regional market's growth.

These factors collectively make the APAC the market a significant player in the global automotive industry.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global automotive control arm market is evolving with a focus on safety, performance, and efficiency in vehicle suspension systems. Material selection criteria and advanced material characterization are central to ensuring durability while reducing overall vehicle weight. Manufacturers are leveraging finite element modeling, topology optimization, and fatigue strength analysis methods to design control arms with improved stiffness, stability, and crash safety performance.

Weight reduction remains a major design priority. Optimized control arm geometry directly influences handling and vehicle dynamics, while improved NVH (noise, vibration, and harshness) performance enhances ride comfort. Integration with braking systems and other suspension components further improves stability and responsiveness.

On the manufacturing side, process optimization, tighter tolerances, and durability testing standards are essential to ensuring reliability and extended service life. Predictive simulations and service life analysis techniques enable engineers to reduce failures while maintaining cost efficiency.

With the rise of lightweight vehicle trends and electric vehicle adoption, OEMs are focusing on innovative control arm solutions that balance strength and flexibility. Enhanced manufacturing processes, bushing replacement procedures, and crash safety-oriented designs are shaping the next generation of suspension components.

As demand grows globally, the market is seeing strong adoption of advanced materials such as high-strength steel, aluminum alloys, and composites, ensuring improved efficiency, reduced emissions, and higher vehicle performance.

What are the key market drivers leading to the rise in the adoption of Automotive Control Arms Industry?

- The significant reduction in the cost of automotive control arms serves as the primary driving force behind the market's growth.

- The market is propelled by the economical ownership costs of these components, making them an attractive choice for inclusion in suspension systems found in a vast array of vehicles. Control arms, an integral element of a vehicle's suspension and steering systems, significantly contribute to enhancing passenger comfort. Primarily manufactured from fortified steel, these mechanical components do not incorporate electronics, thereby maintaining their cost-effectiveness.

- This affordability factor plays a pivotal role in their widespread adoption, making them a preferred choice for automakers and consumers alike. The continuous evolution of the automotive industry, with its focus on enhancing vehicle performance and passenger comfort, ensures a consistent demand for control arms.

What are the market trends shaping the Automotive Control Arms Industry?

- The increasing adoption of lightweight and energy-efficient materials in automotive suspension systems represents a significant market trend. This trend reflects the industry's focus on enhancing vehicle performance and fuel efficiency.

- The market is experiencing advancements in design and material innovation, enhancing vehicle comfort and reducing weight. companies are increasingly focusing on utilizing efficient, lightweight, and robust materials in automotive systems. The automotive industry, which has contributed significantly to environmental pollution, has faced increased scrutiny in recent years. Notably, powertrain, body, and exhaust systems have been under the microscope.

- Leading automotive Tier-1 suppliers are incorporating carbon-fiber reinforced thermoplastic (CFRP) and glass-fiber reinforced polymer (GFRP) into various suspension systems. These materials offer superior strength-to-weight ratios, contributing to weight reduction and improved performance. The market's evolution reflects the industry's commitment to innovation and sustainability.

What challenges does the Automotive Control Arms Industry face during its growth?

- The issue of faulty control arms resulting in vehicle recalls poses a significant challenge to the automotive industry's growth. This problem, which mandates costly remedies, can potentially damage a company's reputation and undermine consumer confidence. Therefore, ensuring the highest standards of manufacturing quality and rigorous testing procedures are essential to mitigate such risks and promote industry advancement within the given 100-word limit.

- Automotive control arms play a pivotal role in optimizing a vehicle's riding dynamics. However, their associated rubber bushings, which cushion the vehicle from road irregularities, are susceptible to wear and tear over time. This degradation can lead to inconsistent performance within the entire suspension system. Historically, such issues have necessitated costly vehicle recalls, prompting manufacturers to invest in addressing these concerns. Control arm rubber bushings serve as vital components, mitigating the impact of road imperfections on the vehicle. Damage to these bushings can adversely affect the driving experience. The continuous use of vehicles contributes to the degradation of these bushings, ultimately necessitating replacement.

- Manufacturers have responded to these challenges by exploring alternative materials and designs to improve the durability of control arm bushings. For instance, some have turned to polyurethane bushings, which offer enhanced strength and longevity compared to their rubber counterparts. This proactive approach not only mitigates the need for costly recalls but also enhances overall vehicle performance. In conclusion, the automotive control arm market is characterized by a focus on innovation and durability to address the challenges posed by wear and tear on rubber bushings. This ongoing evolution is essential to ensuring optimal vehicle performance and enhancing the driving experience.

Exclusive Technavio Analysis on Customer Landscape

The automotive control arms market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive control arms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Control Arms Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive control arms market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

A ONE Parts Co. Ltd. - The company specializes in manufacturing advanced automotive control arms, including the ASCA1001, ASCA1002, and ASCA1003 series. These innovative components enhance vehicle suspension performance and safety, contributing significantly to the automotive industry's technological advancements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A ONE Parts Co. Ltd.

- Alltech Automotive LLC

- American Axle and Manufacturing Holdings Inc.

- CCYS Hi Tech International Ltd

- CFS Machinery Co. Ltd.

- DRiV Inc.

- General Motors Co.

- Hyundai Motor Co.

- Iparts International Ltd.

- Lemdor Control Arm Co. Ltd.

- Marelli Holdings Co. Ltd.

- MZW Motor

- Nalbro Auto Parts Pvt. Ltd.

- RTS S.A.

- SIDEM NV

- Teknorot

- YOROZU Corp.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Control Arms Market

- In January 2024, Magna International, a leading automotive supplier, announced the launch of its new lightweight control arm design, named Magna Lightweight Control Arm System (MLCAS), which reduces vehicle weight by up to 20% and improves fuel efficiency (Magna International Press Release).

- In March 2024, ZF Friedrichshafen AG and Würth Elektronik, two prominent players in the automotive industry, entered into a strategic partnership to develop and produce electric vehicle (EV) control arms with integrated sensors and actuators (ZF Friedrichshafen AG Press Release).

- In April 2025, Continental AG, a leading automotive technology company, completed the acquisition of Vitesco Technologies AG, a major supplier of automotive components, including control arms, for €8.5 billion (Bloomberg News). This acquisition is expected to strengthen Continental's position in the market.

- In May 2025, the European Union announced the approval of new regulations for vehicle safety, including the mandatory installation of advanced driver assistance systems (ADAS) in all new passenger cars from 2026. Control arms are a crucial component in the implementation of these systems (European Commission Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Control Arms Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

146 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 5161.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

China, US, Japan, Germany, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is a critical component of suspension system design, ensuring road handling, safety standards, and NVH (Noise, Vibration, and Harshness) performance. This dynamic market is characterized by continuous innovation in component lifespan, vibration damping, and weight optimization. Ball joint design and kinematic properties play a pivotal role in control arm functionality. Manufacturers invest in advanced material science, casting methods, and forging techniques to enhance structural stiffness and dynamic response. Steering knuckles and control arm bushings undergo rigorous quality control processes to ensure optimal performance and durability. Control arms are integral to suspension geometry, impact absorption, and braking system integration.

- Lateral and longitudinal control arms are engineered to meet torque specifications and high load capacity requirements. The market emphasizes corrosion resistance and fatigue strength testing to improve component lifespan and reliability. Manufacturing processes, including welding techniques and installation procedures, are continually evolving to minimize production costs while maintaining high-quality standards. Finite element analysis and failure analysis are essential tools in suspension system design, ensuring optimal control arm alignment and vibration damping. The market is a competitive landscape, with manufacturers focusing on improving NVH performance, control arm bushings material, and steering knuckle design. The ongoing pursuit of lightweight materials and advanced manufacturing techniques underscores the industry's commitment to enhancing ride comfort and safety standards.

What are the Key Data Covered in this Automotive Control Arms Market Research and Growth Report?

-

What is the expected growth of the Automotive Control Arms Market between 2024 and 2028?

-

USD 5.16 billion, at a CAGR of 4.5%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (Passenger vehicles and Commercial vehicles) and Geography (APAC, Europe, North America, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Low cost of automotive control arms, Faulty control arms leading to vehicle recalls

-

-

Who are the major players in the Automotive Control Arms Market?

-

Key Companies A ONE Parts Co. Ltd., Alltech Automotive LLC, American Axle and Manufacturing Holdings Inc., CCYS Hi Tech International Ltd, CFS Machinery Co. Ltd., DRiV Inc., General Motors Co., Hyundai Motor Co., Iparts International Ltd., Lemdor Control Arm Co. Ltd., Marelli Holdings Co. Ltd., MZW Motor, Nalbro Auto Parts Pvt. Ltd., RTS S.A., SIDEM NV, Teknorot, YOROZU Corp., and ZF Friedrichshafen AG

-

Market Research Insights

- The market encompasses the design, manufacturing, and application of components that connect a vehicle's steering and suspension systems. These critical parts ensure vehicle stability, steering linkage, and optimal ride and handling performance. Control arms undergo rigorous testing to ensure compliance with industry standards, including durability testing, repair procedures, and compliance testing. Steel control arms, a common choice, offer high strength and durability, while aluminum control arms provide weight reduction and improved fuel efficiency. For instance, steel control arms can withstand fatigue life of over 10 million cycles, while aluminum control arms can endure up to 8 million cycles.

- Material selection, testing protocols, joint stiffness, and stress analysis are crucial factors in control arm design validation. Additionally, thermal management, maintenance intervals, and chassis design play significant roles in enhancing the service life of control arms. Polyurethane bushings and rubber bushings are common materials used in control arm mounts, offering varying degrees of flexibility and durability. Kinematic simulations and performance metrics are essential tools in the design and optimization of control arms, ensuring vehicle dynamics and wheel alignment are maintained throughout the vehicle's life cycle. Control arm manufacturers continually strive for cost optimization and design innovation to meet evolving market demands.

We can help! Our analysts can customize this automotive control arms market research report to meet your requirements.

RIA -

RIA -