Passenger Car Market Size 2024-2028

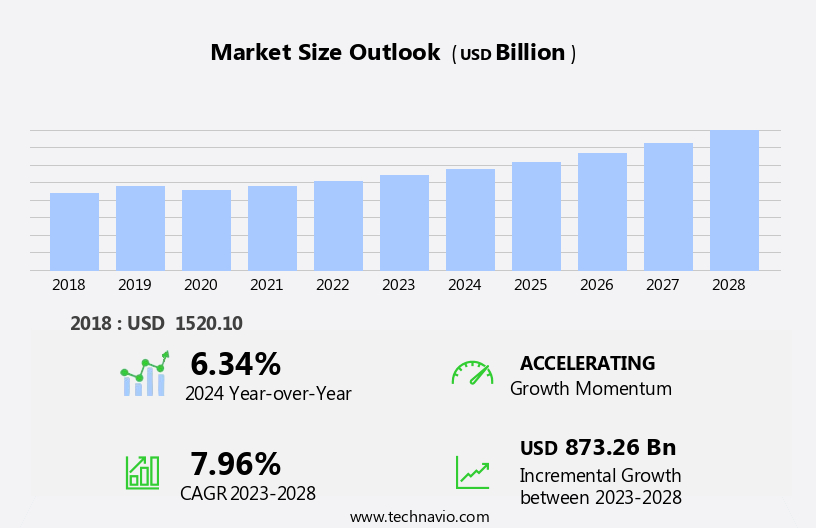

The passenger car market size is forecast to increase by USD 873.26 billion at a CAGR of 7.96% between 2023 and 2028.

- The market is experiencing significant shifts, driven by the increasing acceptance of electric vehicles (EVs) and the integration of advanced technologies such as 3D printing. The growing preference for sustainable transportation solutions is propelling the adoption of EVs, with governments and consumers alike recognizing their environmental benefits. This trend is expected to continue, as advancements in battery technology and charging infrastructure make EVs increasingly practical and convenient for everyday use. However, the market's growth potential is not without challenges. Regulatory hurdles, including stringent emissions standards and safety regulations, impact adoption and increase production costs. Furthermore, the semiconductor shortage is causing supply chain inconsistencies, leading to production delays and higher prices for automakers.

- To capitalize on market opportunities and navigate these challenges effectively, companies must stay informed of regulatory developments and invest in diversifying their semiconductor suppliers. Additionally, exploring collaborations with 3D printing technology providers can help streamline production processes and improve overall competitiveness in the market.

What will be the Size of the Passenger Car Market during the forecast period?

- The passenger vehicles industry in the US is experiencing dynamic shifts, with electric propulsion gaining traction among consumers. Middle-income groups are increasingly opting for sustainable mobility solutions, such as electric hatchbacks and compact SUVs, as lifestyle changes and environmental concerns become more prominent. The shift towards electric vehicles (EVs) is driven by various factors, including advancements in technology, charging infrastructure, and applicable taxes. Fuel prices and regulations continue to influence vehicle choices, with the European Union (EU) leading the way in implementing stringent emission norms. Raw material prices for Internal Combustion Engine (ICE) vehicles and the availability of affordable EV batteries further impact market trends.

- Sedans remain a popular choice, but their market share is dwindling as SUVs gain popularity. Technological developments, such as the Internet of Things (IoT) and EV charging stations, are transforming the industry. General Motors, Chrysler, Hyundai Kona Electric, and other companies are investing in R&D to cater to evolving consumer preferences. The US passenger vehicles industry is witnessing significant growth, particularly in the EV segment. Per capita income plays a crucial role in determining the affordability of various vehicle types. As sustainable practices become increasingly important, the industry is expected to continue adapting to meet the demands of the urban population.

How is this Passenger Car Industry segmented?

The passenger car industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- SUV

- Hatchback

- Sedan

- MPV

- Fuel Type

- ICE Vehicles

- Hybrid

- Electric

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

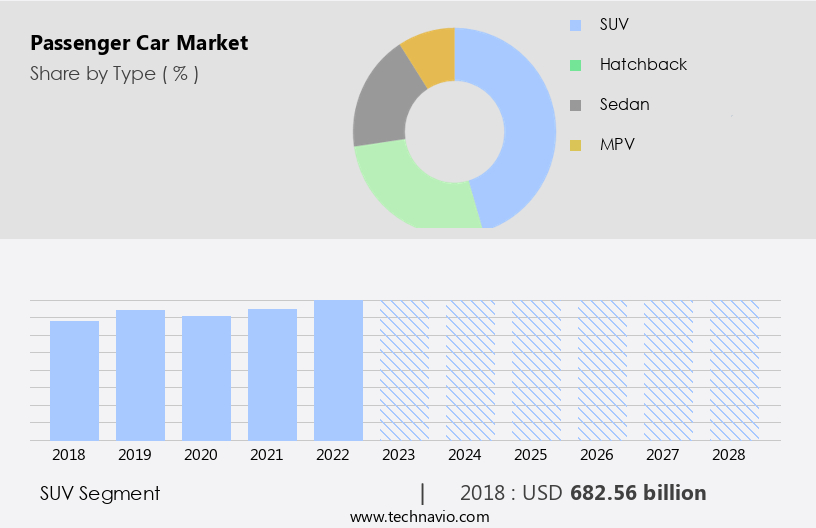

By Type Insights

The SUV segment is estimated to witness significant growth during the forecast period.

The market in the US is experiencing dynamic interplay between various entities, shaping its evolution. Combustion engines continue to dominate, offering power and flexibility, while fuel-efficient alternatives, including hybrid and electric vehicles, gain traction due to fuel price volatility and growing environmental concerns. Chrysler and General Motors, among others, innovate with personalized transportation solutions and enhanced features, catering to diverse consumer preferences. Emerging nations' increasing per capita income fuels overall market expansion, with compact SUVs and sedans popular choices for middle-income groups. Technological developments, such as the Internet of Things and advanced safety measures, add value, while regulations and economic challenges pose hurdles.

Electric vehicles (EVs) and electric vehicle batteries are at the forefront of innovation, with Hyundai Kona electric and Volvo's EV leading the charge. Alternative-fuel options, including diesel engines, face competition from EVs and hybrid vehicles. Urban population growth drives sales, with SUVs, hatchbacks, and sedans catering to various lifestyle changes and sustainable practices. Raw material prices and charging infrastructure development are crucial factors influencing the market landscape. The upward trend in sustainable mobility and applicable taxes shape consumer vehicle choices, making the passenger vehicles industry a dynamic and thriving market.

The SUV segment was valued at USD 682.56 billion in 2018 and showed a gradual increase during the forecast period.

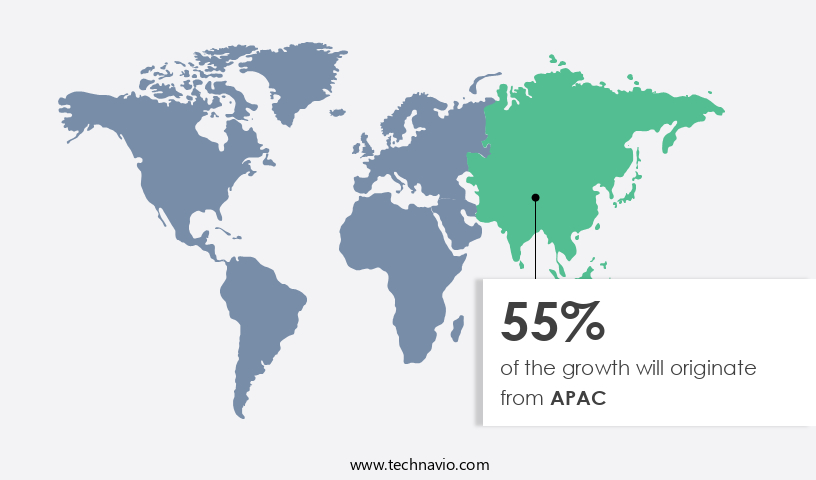

Regional Analysis

APAC is estimated to contribute 55% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth, driven by various factors. In APAC, the region leads in automobile production and sales, primarily due to the high demand in countries like China, Japan, South Korea, India, and Thailand. China, in particular, dominates the regional market with its vast production and sales numbers. The increasing preference for luxury vehicles in China, Japan, and South Korea further fuels market expansion. Emerging nations, including India and Southeast Asian countries, are poised to contribute substantially to the market's growth in the forecast period. Fuel efficiency and innovation are key trends shaping the market.

Combustion engines continue to be popular, but fuel price volatility has led to the increasing adoption of alternative-fuel options such as hybrids, diesels, and electric vehicles (EVs). Chrysler, General Motors, Hyundai, and Volvo are among the manufacturers investing in EVs and enhancing their offerings with advanced safety measures, Internet of Things connectivity, and personalized transportation features. Environmental concerns have become a significant factor influencing consumer preferences. As a result, sustainable vehicles, including EVs and sustainable mobility solutions, are gaining popularity. Technological developments, such as electric vehicle batteries and automatic transmissions, are driving the upward trend in the EV segment.

Special utility vehicles, compact SUVs, and sedans remain popular vehicle choices for various consumer segments, including middle-income groups. The market landscape is dynamic and thriving, with competition intensifying due to the dynamic interplay of economic challenges, regulations, raw material prices, and charging infrastructure development. Urban population growth and applicable taxes further impact market trends. Despite these challenges, the passenger vehicles industry remains a dynamic and exciting space, with ongoing innovation and lifestyle changes driving sustainable practices.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Passenger Car market drivers leading to the rise in the adoption of Industry?

- The increasing preference for electric vehicles (EVs) is the primary factor fueling market growth.

- The market is experiencing significant innovation, with a focus on fuel-efficient vehicles and advanced safety measures. Combustion engines are being replaced by electric passenger cars, driven by government initiatives to reduce air pollution and volatility in fuel prices. In emerging nations, incentives for electric vehicle (EV) manufacturing are boosting industry growth. EVs offer numerous benefits, including the absence of harmful emissions such as particulates, carbon monoxide, hydrocarbons, and volatile organic compounds.

- The Internet of Things (IoT) is playing a pivotal role in enhancing vehicle features, offering personalized transportation solutions. Compact SUVs are also gaining popularity due to their fuel efficiency and versatility. Overall market expansion is expected as buyers increasingly demand advanced safety measures and eco-friendly transportation options.

What are the Passenger Car market trends shaping the Industry?

- The increasing adoption of 3D printing technology in the automotive industry represents a significant market trend. Passenger cars are increasingly utilizing 3D printing for manufacturing components, leading to innovation and potential cost savings.

- The market is a dynamic and thriving industry, with consumer preferences increasingly leaning towards alternative-fuel options, such as electric vehicles (EVs). This trend is driven by environmental concerns and technological developments. For instance, Hyundai Kona electric and Volvo's EV are gaining popularity. EV charging stations are becoming more common, making it more convenient for consumers to make the switch. Hybrid vehicles and the gradual phase-out of diesel engines are also contributing to this shift. The market landscape is characterized by economic challenges, requiring continuous innovation and cost reduction. 3D printing, with its potential for customization, rapid prototyping, and reduced production time, is poised to revolutionize the industry.

- Personalized car components, such as custom dashboards and steering wheels, can be printed to cater to individual preferences. Complex geometries and intricate structures, previously difficult to manufacture, become feasible, leading to innovative car designs. On-demand manufacturing of spare parts using 3D printing reduces lead times and inventory costs.

How does Passenger Car market faces challenges face during its growth?

- The semiconductor shortage poses a significant challenge to the growth of the market, as this essential technology component is in high demand and limited in supply.

- The market is currently grappling with the repercussions of the semiconductor shortage, a critical issue affecting the production of vehicles worldwide. This scarcity of microchips, essential for various in-vehicle functions, has compelled automakers to reduce production, leading to a decrease in available cars for sale. The European Union (EU) has been particularly impacted, with the Association of European Vehicle Logistics reporting over 11 million vehicles lost to production cuts due to this crisis in 2021. This situation translates to significant revenue losses and disappointed customers for manufacturers. The semiconductor shortage, which originated in late 2020, has disrupted numerous industries, including automotive manufacturing, due to the vital role semiconductors play in modern vehicles, such as automatic transmissions, charging infrastructure for sustainable vehicles like Electric Vehicles (EVs) and Electric vehicle batteries, and other advanced features.

- The dynamic interplay between regulations, raw material prices, and technological challenges continues to shape the market, with competition intensifying as manufacturers strive to innovate and meet consumer demands for fuel efficiency, safety, and connectivity.

Exclusive Customer Landscape

The passenger car market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the passenger car market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, passenger car market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aston Martin Lagonda Ltd. - The luxury automobile manufacturer showcases an extensive range of passenger vehicles, including the DBX, DB12, DBS 770 Ultimate, DBS 770 Ultimate Volante, Vantage, and Valour models.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aston Martin Lagonda Ltd.

- BMW AG

- BYD Co. Ltd.

- Ford Motor Co.

- Geely Auto International Corp.

- General Motors Co.

- Great Wall Motor Co. Ltd.

- Honda Motor Co. Ltd.

- Hyundai Motor Co.

- Mahindra and Mahindra Ltd.

- Mazda Motor Corp.

- Mercedes Benz Group AG

- Renault SAS

- SAIC Motor Corp. Ltd.

- Stellantis NV

- Suzuki Motor Corp.

- Tata Motors Ltd.

- Tesla Inc.

- Toyota Motor Corp.

- Volkswagen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Passenger Car Market

- In February 2024, Volkswagen Group and Ford Motor Company announced a strategic partnership to develop commercial vehicles and autonomous vehicles together, aiming to save approximately USD3 billion in costs through the alliance (Volkswagen AG, 2024). This collaboration represents a significant shift in the market, as two major competitors join forces to improve their competitive positions in the rapidly evolving autonomous vehicle sector.

- In May 2025, Tesla, Inc. launched its Model Y compact SUV, marking the electric vehicle manufacturer's entry into the popular SUV segment (Tesla, Inc., 2025). With record-breaking pre-orders and strong demand, the Model Y has become a key player in the market, demonstrating the growing importance of electric vehicles and Tesla's continued dominance in the sector.

- In August 2024, Magna International, a leading automotive supplier, acquired a majority stake in Veoneer, a Swedish autonomous driving technology company, for approximately USD3.8 billion (Magna International, 2024). This strategic acquisition represents a significant investment in advanced technology and positions Magna as a key player in the development and deployment of autonomous driving systems in the market.

- In December 2025, the European Union passed new regulations requiring all new passenger cars to be fitted with emission reduction technology, such as particulate filters, from 2025 onwards (European Parliament, 2025). This regulatory initiative represents a significant shift towards cleaner, more sustainable transportation and is expected to drive demand for advanced emission reduction technologies in the market.

Research Analyst Overview

The market continues to evolve, driven by a dynamic interplay of various factors. One significant influence is the ongoing innovation in fuel-efficient technologies, as consumers seek to mitigate the impact of fuel price volatility. Combustion engines are being replaced by more efficient alternatives, such as hybrids and electric vehicles (EVs), which offer enhanced features and improved fuel economy. Chrysler, like other automakers, is responding to these trends by expanding its lineup of fuel-efficient vehicles. Personalized transportation solutions are also gaining traction in emerging nations, where the urban population is on the rise and per capita income is increasing.

This market landscape is further shaped by economic challenges, regulations, and raw material prices, which can significantly impact sales and segment growth. Technological developments, such as the Internet of Things (IoT), are transforming the passenger car industry. Advanced safety measures and sustainable mobility are becoming increasingly important to consumers, as environmental concerns grow. The upward trend towards electric vehicles (EVs) and sustainable vehicles is evident, with companies like Volvo introducing their EV offerings and the proliferation of EV charging stations. Competition in the market is fierce, with automakers vying to offer the most advanced propulsion systems, from traditional internal combustion engines (ICE) to alternative-fuel options like hybrids and EVs.

Special utility vehicles, such as compact SUVs, remain popular choices due to their versatility and appeal to middle-income groups. The passenger vehicles industry is a dynamic and thriving market, with continuous innovation and adaptation to changing consumer preferences and economic conditions. Fuel prices, applicable taxes, and lifestyle changes are all factors that influence vehicle choices, as consumers seek sustainable practices and environmentally-friendly options. The European Union (EU) and other regulatory bodies play a crucial role in shaping industry dynamics, as they implement regulations aimed at reducing emissions and promoting sustainable mobility. Despite these challenges, the market remains optimistic, as technological advancements and economic growth continue to drive demand for passenger cars.

The ongoing evolution of the industry is a testament to its resilience and adaptability, as it navigates the complex interplay of various factors and shapes the future of personalized transportation.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Passenger Car Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

184 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.96% |

|

Market growth 2024-2028 |

USD 873.26 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.34 |

|

Key countries |

US, China, India, Japan, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Passenger Car Market Research and Growth Report?

- CAGR of the Passenger Car industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the passenger car market growth of industry companies

We can help! Our analysts can customize this passenger car market research report to meet your requirements.

RIA -

RIA -