Automotive Inertial Measurement Unit (IMU) Sensors Market 2024-2028

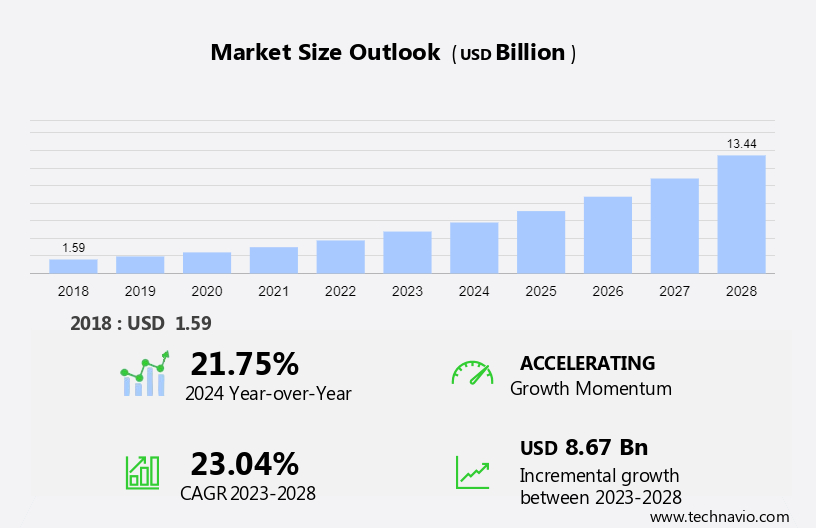

The automotive inertial measurement unit (IMU) sensors market size is forecast to increase by USD 8.67 billion, at a CAGR of 23.04% between 2023 and 2028. Several factors play a crucial role in market growth and forecasting, such as the reduction in the cost of IMU sensors due to economies of scale, the strong demand for IMU sensors from automotive applications, and the presence of stringent regulatory frameworks in automobile safety standards.

The market forecast report delves into the intricacies of the Automotive Inertial Measurement Unit Sensors Market, offering a detailed outlook on the industry. This comprehensive analysis segments the market by Application, encompassing passenger cars and commercial vehicles. Furthermore, the Product landscape is categorized into FOG-based IMUs and MEMS gyroscope-based IMUs. The report's extensive geographical coverage includes APAC, North America, Europe, South America, and Middle East and Africa.

In addition to these segments, the Automotive Airbag Electronic Control Unit (ECU) is another crucial component of the automotive sector that interacts with IMUs. The market analysis and report provide valuable insights into market size, historical data from 2018 to 2022, and future projections, all presented in terms of value in USD billion for each segment. The Automotive Airbag Electronic Control Unit (ECU) plays a vital role in deploying airbags in the event of a collision, and its integration with IMUs enhances the safety features of modern vehicles by providing real-time data on vehicle dynamics and impact forces

What will be the size of the Automotive Inertial Measurement Unit Sensors Market During the Forecast Period?

For More Highlights About this Report, Download Free Sample in a Minute

Automotive Inertial Measurement Unit Sensors Market: Key Drivers, Trends and Challenges

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Automotive Inertial Measurement Unit Sensors Market Driver

As per Automotive Inertial Measurement Unit Sensors Market Analysis,the robust demand for IMU (Inertial Measurement Unit) sensors in automotive applications is a key driver of Automotive Inertial Measurement Unit Sensors market growth. These sensors, including gyroscopes and accelerometers, are integral to ADAS (Advanced Driver Assistance Systems), which are designed to reduce human error while driving and mitigate accident risks. ADAS plays a particularly crucial role during long drives, where fatigue is a leading cause of accidents. Developed regions like North America and Europe are expected to dominate the ADAS market, boosting the growth of the global automotive IMU sensor market during the forecast period.

Furthermore, airbags, which are essential for ensuring occupant safety in the event of a crash, are operated by an airbag control unit that relies on various sensors, such as automotive IMU sensors. The increasing demand for airbags in vehicles is a significant factor driving the adoption of these sensors. As a result, this trend will positively impact the global automotive sensor market.

In addition to automotive applications, IMU sensors are pivotal in several other sectors, including aerospace, defense, consumer electronics, and robotics. In consumer electronics, sensors support functions such as motion tracking, stabilization, and navigation in smartphones, AR/VR systems, and drones. The rise of AI-powered autonomous vehicles, along with the increasing integration of IMU sensors in robotics, drones, and military systems, will further contribute to the market's expansion across various industries.

Automotive Inertial Measurement Unit Sensors Market Trends

The growing development of autonomous vehicles to increase IMU adoption is the primary trend shaping market growth. Leading automotive manufacturers like Mercedes-Benz and BMW are actively propelling the development of self-driving cars, driving significant market trends and analysis. The increasing acceptance of semi-autonomous vehicles is concurrently fueling the demand for automotive sensors. It is anticipated that self-driving or unmanned vehicles will boost the quantum of electronic content in future vehicles, which will aid in accessing large volumes of data to make better decisions while driving.

Furthermore, the growth in the global autonomous vehicle market is crucial for the growth in the global automotive inertial measurement unit sensors market. This is attributed to the adoption of automotive IMU sensors as an integral part of many systems used in automated vehicles. Thus, the advent of autonomous technology will boost the global automotive inertial measurement unit sensors market growth during the forecast period.

Automotive Inertial Measurement Unit Sensors Market Challenge

Improper tuning of IMU sensors impacting driving behavior is a challenge that affects market growth. Improper tuning of the autonomous car technology system can create problems in vehicles due to the electronic output from sensors (such as IMU sensors) positioned for chassis control. This can cause serious mishaps while driving. Consequently, electronic system manufacturers need to be wary of such consequences if they are to deliver as per the user's expectations. Even occasional faults in the system can have a deleterious effect on the adoption of sensors, which can also negatively impact the overall growth of the market.

Furthermore, multiple sets of calibrations (as required in the sensor fusion unit) increase the power consumption of the device. Good calibration is a prerequisite for sensor fusion and, preferably, without the need for additional hardware. This and the issue of sensor drift are expected to be some of the primary issues to impede market growth during the forecast period.

Automotive Inertial Measurement Unit Sensors Market Customer Landscape

The market research report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market research and growth report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Automotive Inertial Measurement Unit Sensors Market Customer Landscape

Who are the Major Automotive Inertial Measurement Unit Sensors Market Companies?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

- ACEINNA Inc.: The company offers intertial measurement unit sensors such as IMU330RA sensor that is designed for use in automotive level 3 and higher ADAS systems.

The research report also includes detailed analyses of the competitive landscape of the market and information about 17 market companies, including:

- Adafruit Industries LLC

- Advanced Navigation Pty Ltd.

- Continental AG

- Gladiator Technologies Inc.

- Honeywell International Inc.

- Hottinger Bruel and Kjaer GmbH

- ifm electronic gmbh

- Murata Manufacturing Co. Ltd.

- ON Semiconductor Corp.

- Robert Bosch GmbH

- Safran SA

- STMicroelectronics International N.V.

- TE Connectivity Ltd.

- Texas Instruments Inc.

- Thales Group

- VectorNav Technologies LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Latest Market Development and News

-

In December 2023, STMicroelectronics introduced the ASM330LHBG1, an automotive-grade 6-axis IMU sensor designed for advanced driver assistance systems (ADAS) and navigation applications. This sensor combines accelerometer and gyroscope functionalities to enhance vehicle safety and performance.

-

In November 2023, a comprehensive market analysis projected the automotive IMU sensors market to reach USD 27,243.96 million by 2032, growing at a compound annual growth rate (CAGR) of 19.96% from 2024 to 2032. This growth is driven by the increasing adoption of autonomous vehicles, electric vehicles, and advanced driver assistance systems (ADAS).

-

In January 2024, Technavio released a forecast indicating that the automotive IMU sensors market is expected to grow by USD 8.67 billion between 2023 and 2028, at a CAGR of 23.04%. This growth is attributed to the rising demand for IMU sensors in automotive applications, including passenger cars and commercial vehicles.

-

In February 2024, a market research report highlighted that the automotive IMU sensors market is projected to grow significantly at a CAGR of 8.4% during the forecast period from 2021 to 2028. This growth is driven by the increasing demand for car safety and driver assistance systems, such as autonomous driving and collision avoidance.

What is the Largest-Growing Segments in the Automotive Inertial Measurement Unit Sensors Market?

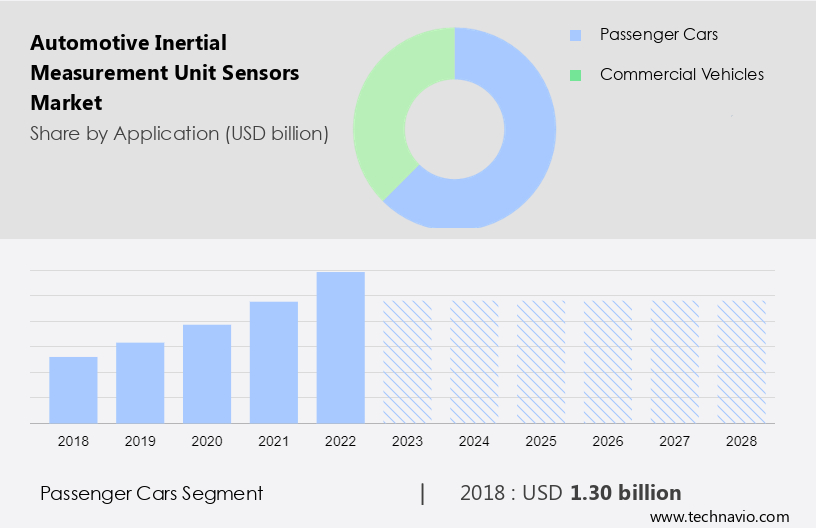

The passenger cars segment StartFragment is estimated to witness significant growth during the forecast period. The growing focus of the automotive OEMs toward offering advanced navigation systems and ADAS is fostering the adoption of IMU sensors in the passenger cars segment. Navigation systems are widely adopted due to the growing penetration of infotainment systems in passenger cars.

Get a glance at the market contribution of various segments Download the PDF Sample

The passenger cars segment StartFragment was the largest segment and was valued at USD 1.30 billion in 2018. In the past few years, growing concerns about safety among consumers have compelled automobile manufacturers to incorporate additional advanced safety features in vehicles, especially in entry-level vehicles. Furthermore, the growing focus of automotive OEMs on transitioning to fully autonomous vehicles is fostering the development of various sensor technologies that incorporate driver assistance systems for use during critical events. These developments will be a positive driver for the growth of the global automotive inertial measurement unit sensors market in this segment during the forecast period.

Which are the Key Regions for the Automotive Inertial Measurement Unit Sensors Market?

For more insights on the market share of various regions Download PDF Sample now!

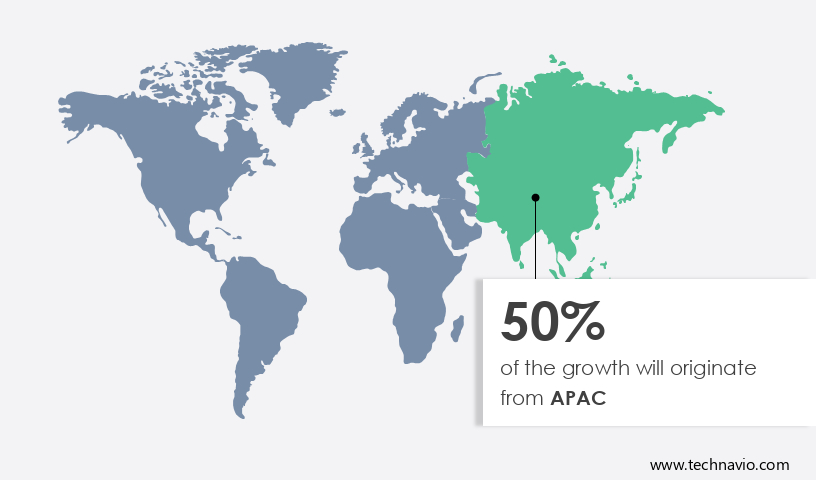

APAC is estimated to contribute 50% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. In APAC, China, India, and Japan are the prominent revenue-contributing countries in the automotive inertial measurement unit (IMU) sensors market. China, India, Japan, and South Korea are the dominant markets in APAC, where China leads the market, followed by Japan and India.

Furthermore, sensor companies are also attracted to markets in APAC. Some of these players have located their foundries to mark the beginning of a long-term presence in the region. Additionally, establishing a supplier base in APAC gives automotive OEMs significant cost benefits and also enables collaborative working models that may spark innovation in drivetrain technologies for future vehicles. Such developments are anticipated to expand the market for automotive IMU sensor manufacturers in APAC during the forecast period.

Segment Overview

The automotive inertial measurement unit sensors market report forecasts market growth analysis by revenue at global, regional & country levels and provides an analysis of the market growth and trends from 2018 to 2028.

- Application Outlook

- Passenger cars

- Commercial vehicles

- Product Outlook

- FOG-based IMUs

- MEMS gyroscope-based IMUs

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

|

Automotive Inertial Measurement Unit Sensors Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Market forecasting period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 23.04% |

|

Market Growth 2024-2028 |

USD 8.67 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

21.75 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 50% |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ACEINNA Inc., Adafruit Industries LLC, Advanced Navigation Pty Ltd., Continental AG, Gladiator Technologies Inc., Honeywell International Inc., Hottinger Bruel and Kjaer GmbH, ifm electronic gmbh, Murata Manufacturing Co. Ltd., ON Semiconductor Corp., Robert Bosch GmbH, Safran SA, STMicroelectronics International N.V., TE Connectivity Ltd., Texas Instruments Inc., Thales Group, and VectorNav Technologies LLC |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Automotive Inertial Measurement Unit Sensors Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the market between 2024 and 2028

- Precise estimation of the market size and its contribution to the market in focus to the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market across APAC, North America, Europe, South America, and the Middle East and Africa

- A thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -