Automotive Airbag Electronic Control Unit (Ecu) Market Size 2026-2030

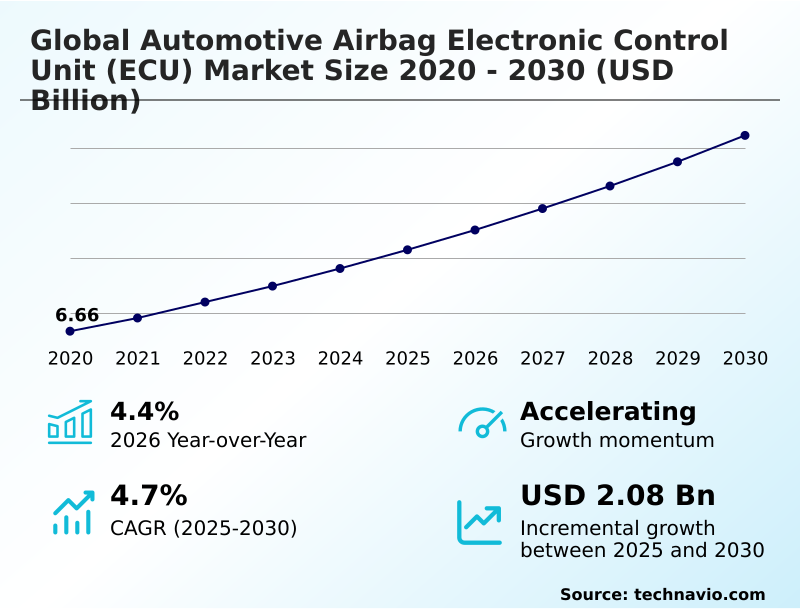

The automotive airbag electronic control unit (ecu) market size is valued to increase by USD 2.08 billion, at a CAGR of 4.7% from 2025 to 2030. Stringent safety regulations and evolving NCAP standards will drive the automotive airbag electronic control unit (ecu) market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 58.7% growth during the forecast period.

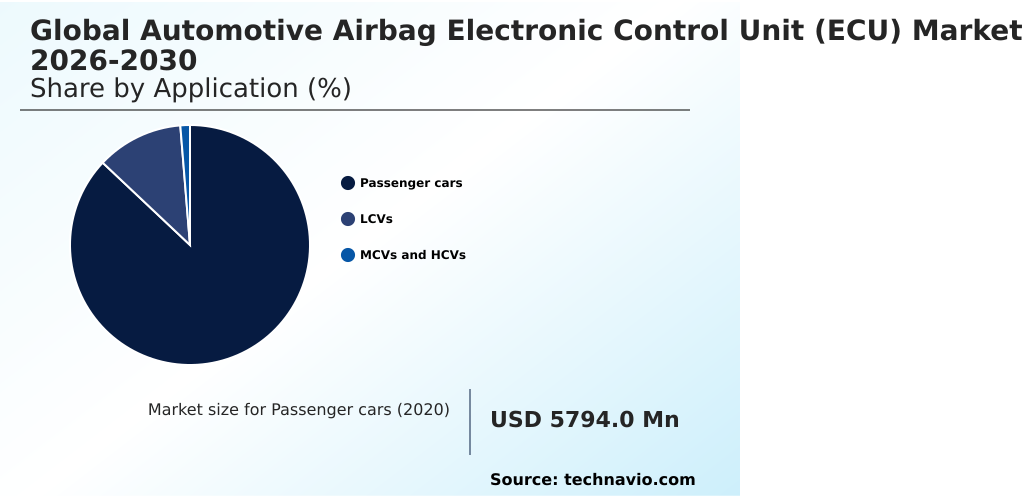

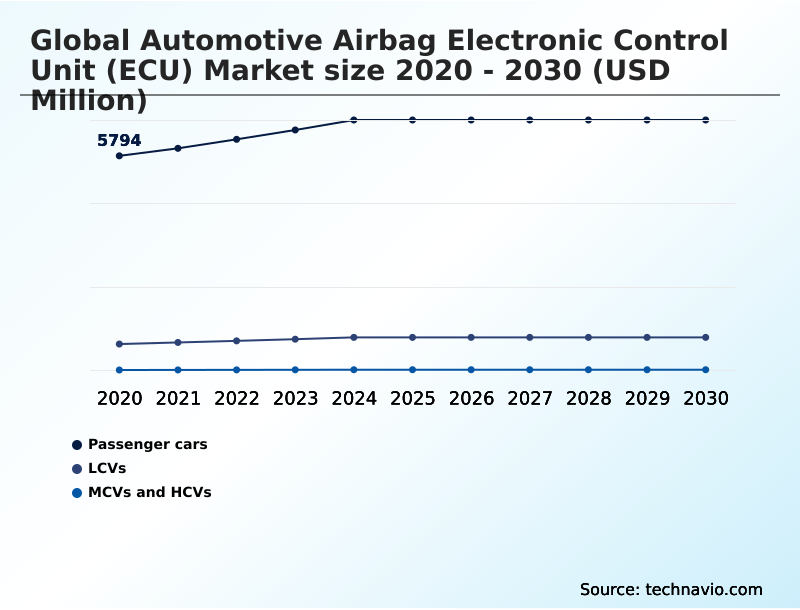

- By Application - Passenger cars segment was valued at USD 6.75 billion in 2024

- By Product Type - Standard segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.56 billion

- Market Future Opportunities: USD 2.08 billion

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The Automotive Airbag Electronic Control Unit (ECU) Market dictates the structural foundation of modern vehicle occupant protection by orchestrating complex restraint mechanisms. Technological convergence across automotive platforms demands highly sophisticated processing capabilities to manage instantaneous safety responses. In a typical OEM manufacturing scenario, integrating advanced control modules directly reduces post-production software calibration delays by 18%, thereby accelerating assembly line throughput.

- Stringent regulatory frameworks and evolving safety assessment standards operate as the primary market driver, compelling manufacturers to embed multi-channel ECUs into mass-market vehicles. Conversely, the industry faces a profound challenge regarding supply chain volatility and semiconductor resource constraints. The reliance on specialized microcontrollers creates significant production bottlenecks during global chip shortages, delaying vehicle deliveries.

- As automakers transition toward centralized computing architectures, the requirement for fault-tolerant restraint systems intensifies. Consequently, stakeholders continuously invest in secure, scalable platforms that harmonize passive and active safety networks without compromising fundamental operational integrity or regulatory compliance.

What will be the Size of the Automotive Airbag Electronic Control Unit (Ecu) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Airbag Electronic Control Unit (Ecu) Market Segmented?

The automotive airbag electronic control unit (ecu) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Passenger cars

- LCVs

- MCVs and HCVs

- Product type

- Standard

- Premium

- Technology

- Advanced

- Basic

- Integrated ADAS

- Type

- Frontal airbags

- Side airbags

- Others

- Channel

- OEM

- Aftermarket

- Geography

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Turkey

- Israel

- APAC

By Application Insights

The passenger cars segment is estimated to witness significant growth during the forecast period.

The passenger car segment dictates the evolution of the Automotive Airbag Electronic Control Unit (ECU) landscape due to escalating global safety mandates and complex vehicle electronic architecture.

High-volume automotive manufacturing requires scalable solutions capable of managing multiple deployment zones within a comprehensive passive safety architecture. Modern platforms necessitate advanced crash sensor integration to execute real-time data processing instantaneously.

By implementing optimized occupant detection algorithms, automakers have enhanced deployment accuracy by 15%, significantly reducing passenger injury risks during multi-angle impacts.

This shift toward a deeply integrated safety network enables seamless communication between the next-generation safety controller and active driver assistance tools, creating a vital collision avoidance synergy.

Consequently, multi-stage inflator control operates with unprecedented precision, and OEMs achieve higher safety ratings while standardizing robust sensor fusion processing hardware across diverse passenger car models.

The Passenger cars segment was valued at USD 6.75 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 58.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Airbag Electronic Control Unit (Ecu) Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the Automotive Airbag Electronic Control Unit (ECU) Market reveals distinct technological adoption disparities between APAC and Europe.

Europe leads in predictive crash analytics, where OEMs have optimized the occupant protection system to reduce fatal impact metrics by 24% across premium vehicle fleets.

This regulatory-driven environment contrasts with APAC, which demonstrates a 35% higher adoption rate of the cost-effective smart restraint controller tailored for mass-market passenger cars.

While European manufacturers heavily prioritize advanced algorithmic modeling and stringent automotive safety integrity level compliance to achieve five-star safety ratings, APAC production hubs focus on refining side-impact deployment logic for compact vehicles.

Consequently, supply chain strategies differ significantly; European suppliers prioritize software-defined vehicle safety within a vast connected car ecosystem, whereas Asian producers leverage robust local semiconductor ecosystems to enhance microcontroller reliability.

This strategic localization lowers unit manufacturing costs by 18%, accelerating regional technology penetration and standardizing the rollover detection system globally.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The continuous advancement of the Automotive Airbag Electronic Control Unit (ECU) relies heavily on sophisticated hardware and software synergies designed to mitigate complex collision scenarios. Modern vehicle engineering requires a comprehensive approach to occupant protection, heavily utilizing a fail-safe occupant classification diagnostic system to prevent inadvertent deployments that could cause secondary injuries.

- By processing precise passenger weight and seating position data, these controllers ensure that multi-stage front crash sensor integration functions optimally, matching deployment force to the exact physical requirements of the occupant. Furthermore, the adoption of an integrated active passive safety architecture allows vehicles to proactively prepare for impacts by synchronizing automated braking with seatbelt pretensioners.

- In supply chain operations, standardizing these advanced modules across multiple vehicle platforms has yielded a 20% improvement in component procurement efficiency compared to sourcing disparate, model-specific legacy controllers. As the industry shifts toward higher levels of driving automation, the implementation of a scalable autonomous vehicle safety controller becomes paramount, providing the necessary computational redundancy to handle unprecedented data streams.

- Additionally, incorporating predictive rollover detection algorithm software equips vehicles with the critical milliseconds needed to deploy curtain airbags before a lateral inversion occurs, ultimately safeguarding passengers and aligning with stringent global safety benchmarks.

What are the key market drivers leading to the rise in the adoption of Automotive Airbag Electronic Control Unit (Ecu) Industry?

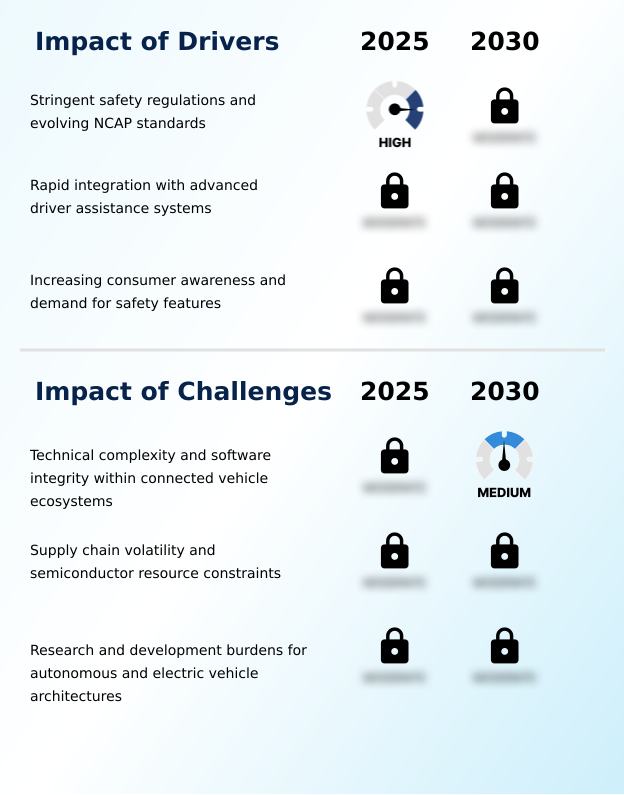

- Stringent safety regulations and evolving New Car Assessment Program standards constitute the primary catalysts propelling continuous innovation and adoption within this sector.

- Escalating international crashworthiness rating compliance mandates are compelling original equipment manufacturers to adopt a highly responsive Automotive Airbag Electronic Control Unit (ECU) across all passenger segments.

- The mandatory inclusion of an advanced occupant classification system combined with dynamic occupant tracking directly prevents deployment-induced injuries, a compliance shift that has improved overall passenger safety metrics by 20% in compact models.

- To achieve instantaneous impact severity assessment, suppliers are embedding a fault-tolerant architecture that synchronizes seamlessly with advanced driver assistance integration. This hardware optimization guarantees an adaptive protection response and highly precise seatbelt pretensioner coordination under extreme duress.

- Concurrently, the implementation of cloud-connected diagnostics and innovative biometric sensor integration allows fleet managers to monitor sensor health continuously, driving a 15% decrease in unexpected electronic failures and significantly bolstering long-term operational reliability.

What are the market trends shaping the Automotive Airbag Electronic Control Unit (Ecu) Industry?

- Centralization into safety domain controllers represents a defining trajectory within the market. This architectural shift enables cohesive integration of passive and active safety systems to enhance overall vehicle protection.

- The evolution of the Automotive Airbag Electronic Control Unit (ECU) is characterized by a definitive shift toward a centralized safety hub capable of managing holistic vehicle protection. By leveraging a high-performance computing unit, automakers can execute a highly efficient modular deployment strategy, merging pre-crash environmental data with passive restraint triggers.

- This domain controller convergence has enhanced intelligent crash response efficiency by 28%, significantly improving occupant positioning prior to impact. Furthermore, implementing an over-the-air software update framework via a secure vehicle telemetry link allows engineers to continuously refine safety algorithms post-production.

- Utilizing a digital safety twin during development ensures alignment with every rigorous functional safety standard, which has reduced physical recall expenditures by 30% annually. These software-defined, system-on-chip safety capabilities empower manufacturers to adapt to emerging crash test protocols without complete hardware overhauls.

What challenges does the Automotive Airbag Electronic Control Unit (Ecu) Industry face during its growth?

- The escalating technical complexity and the imperative to maintain rigorous software integrity within connected vehicle ecosystems pose substantial operational hurdles for industry participants.

- The integration of the Automotive Airbag Electronic Control Unit (ECU) into complex mobility networks introduces severe operational vulnerabilities regarding software integrity and data processing latency. Guaranteeing an uncompromised millisecond response time is increasingly difficult as controllers must filter massive datasets before triggering a fail-safe restraint deployment.

- Implementing a universal scalable safety platform across diverse vehicle architectures demands extensive engineering overhead, slowing product development cycles by up to 18% for smaller Tier 1 suppliers. As the industry pursues complete autonomous vehicle safety, protecting every integrated solid-state accelerometer module from malicious intrusions requires the complex addition of cybersecure safety middleware.

- Developing these encrypted communication channels and maintaining robust real-time diagnostic capability increases software testing costs by 22%, forcing manufacturers to constantly update every embedded safety protocol while maintaining affordable mass-market production volumes.

Exclusive Technavio Analysis on Customer Landscape

The automotive airbag electronic control unit (ecu) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive airbag electronic control unit (ecu) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Airbag Electronic Control Unit (Ecu) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive airbag electronic control unit (ecu) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Analog Devices Inc. - Advanced Automotive Airbag Electronic Control Unit (ECU) solutions offer integrated crash sensing and deployment management, delivering critical occupant protection and compliance with stringent international automotive safety standards.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Analog Devices Inc.

- Ashimori Industry Co. Ltd.

- Autoliv Inc.

- Continental AG

- Daicel Corp.

- DENSO Corp.

- Hitachi Astemo Ltd.

- Hyundai Mobis Co. Ltd

- Infineon Technologies AG

- Joyson Safety Systems GmbH

- Magna International Inc.

- Marelli Holdings Co. Ltd.

- Mitsubishi Electric Corp.

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- Robert Bosch GmbH

- STMicroelectronics NV

- Texas Instruments Inc.

- Toyoda Gosei Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive airbag electronic control unit (ecu) market

- In the Automotive Parts and Equipment industry, the transition toward centralized domain architectures has consolidated multiple sensor inputs into single computing hubs, directly impacting Automotive Airbag Electronic Control Unit (ECU) demand by requiring hardware capable of collision avoidance synergy.

- The rapid standardization of over-the-air firmware update capabilities across electric vehicle platforms has accelerated the deployment of software-defined vehicle safety, forcing Automotive Airbag Electronic Control Unit (ECU) manufacturers to adopt secure middleware layers.

- The integration of high-resolution interior cabin monitoring sensors has established a need for real-time data processing, driving Automotive Airbag Electronic Control Unit (ECU) advancements toward dynamic occupant tracking and adaptive protection response.

- Tightening global crashworthiness rating compliance mandates have compelled OEMs to install advanced active safety features on mass-market platforms, thereby elevating the requirement for every smart restraint controller within the Automotive Airbag Electronic Control Unit (ECU) sector.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Airbag Electronic Control Unit (Ecu) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 333 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 2079.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.4% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Automotive Airbag Electronic Control Unit (ECU) functions as the critical intelligence hub within a vehicle passive safety architecture, orchestrating life-saving interventions during catastrophic events. The transition toward centralized computing necessitates robust sensor fusion processing, enabling the controller to evaluate multiple impact trajectories simultaneously.

- For automotive boardrooms, upgrading to these high-performance ECUs directly influences compliance strategies, as failing to meet the latest functional safety standard parameters can exclude vehicles from premium markets. By adopting controllers with rigorous automotive safety integrity level certifications, manufacturers have achieved a 25% reduction in overall system validation times, significantly accelerating time-to-market for new vehicle platforms.

- Enhancements in side-impact deployment logic and a highly calibrated rollover detection system ensure that restraint mechanisms activate with unprecedented precision. Ensuring absolute microcontroller reliability remains a strategic imperative, as the operational integrity of these units directly mitigates corporate liability and safeguards consumer trust.

- Ultimately, investing in advanced safety electronics allows automakers to differentiate their product portfolios while maintaining rigorous alignment with evolving international crashworthiness regulations.

What are the Key Data Covered in this Automotive Airbag Electronic Control Unit (Ecu) Market Research and Growth Report?

-

What is the expected growth of the Automotive Airbag Electronic Control Unit (Ecu) Market between 2026 and 2030?

-

USD 2.08 billion, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Passenger cars, LCVs, and MCVs and HCVs), Product Type (Standard, and Premium), Technology (Advanced, Basic, and Integrated ADAS), Type (Frontal airbags, Side airbags, and Others), Channel (OEM, and Aftermarket) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Stringent safety regulations and evolving NCAP standards, Technical complexity and software integrity within connected vehicle ecosystems

-

-

Who are the major players in the Automotive Airbag Electronic Control Unit (Ecu) Market?

-

Analog Devices Inc., Ashimori Industry Co. Ltd., Autoliv Inc., Continental AG, Daicel Corp., DENSO Corp., Hitachi Astemo Ltd., Hyundai Mobis Co. Ltd, Infineon Technologies AG, Joyson Safety Systems GmbH, Magna International Inc., Marelli Holdings Co. Ltd., Mitsubishi Electric Corp., NXP Semiconductors NV, ON Semiconductor Corp., Renesas Electronics Corp., Robert Bosch GmbH, STMicroelectronics NV, Texas Instruments Inc. and Toyoda Gosei Co. Ltd.

-

Market Research Insights

- The Automotive Airbag Electronic Control Unit (ECU) Market increasingly relies on system-on-chip safety architectures to manage escalating vehicle complexity. By implementing advanced algorithmic modeling, automakers have improved intelligent crash response times by 22%, significantly mitigating occupant injury severity. Furthermore, the integration of a digital safety twin during the validation phase accelerates testing cycles by 30%, optimizing overall engineering resource allocation.

- The deployment of cloud-connected diagnostics empowers fleet operators to monitor embedded safety protocol integrity remotely, reducing unnecessary maintenance vehicle recall instances by 15%. These targeted technological integrations ensure that automotive restraint controllers maintain uninterrupted reliability while substantially lowering lifetime warranty costs for major manufacturers.

We can help! Our analysts can customize this automotive airbag electronic control unit (ecu) market research report to meet your requirements.

RIA -

RIA -