Automotive Junction Box Market Size 2025-2029

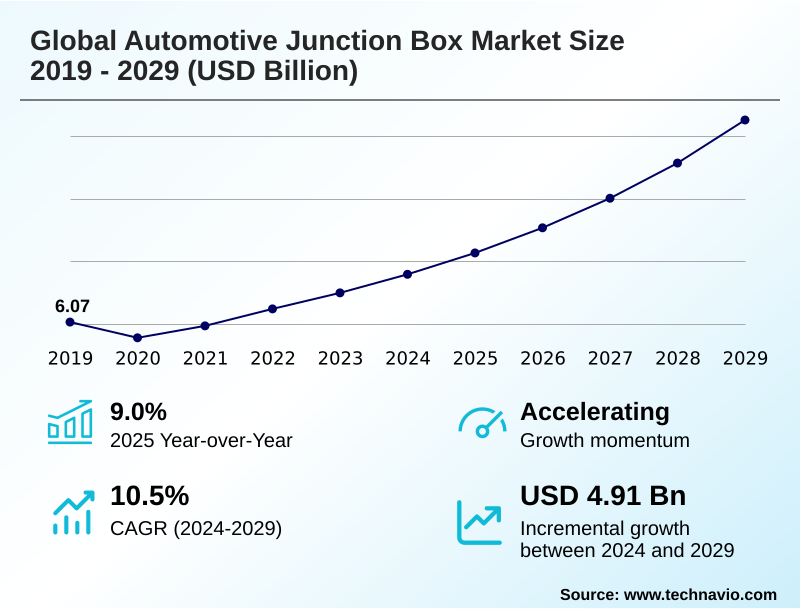

The automotive junction box market size is valued to increase by USD 4.91 billion, at a CAGR of 10.5% from 2024 to 2029. Penetration of hybrid and electric powertrains will drive the automotive junction box market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 56.5% growth during the forecast period.

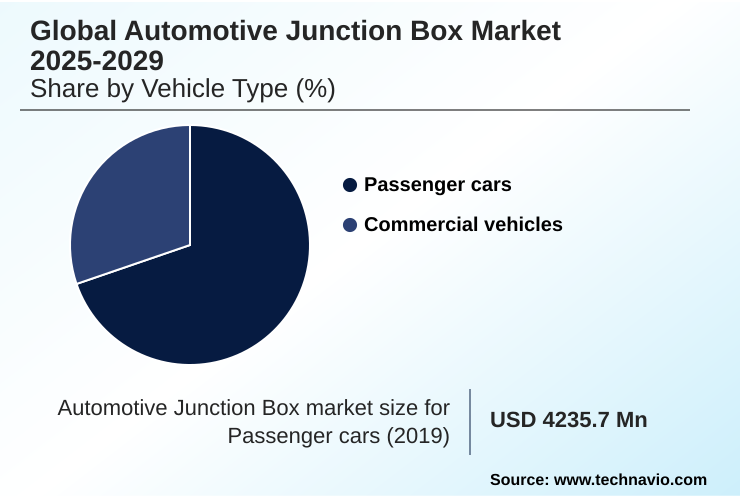

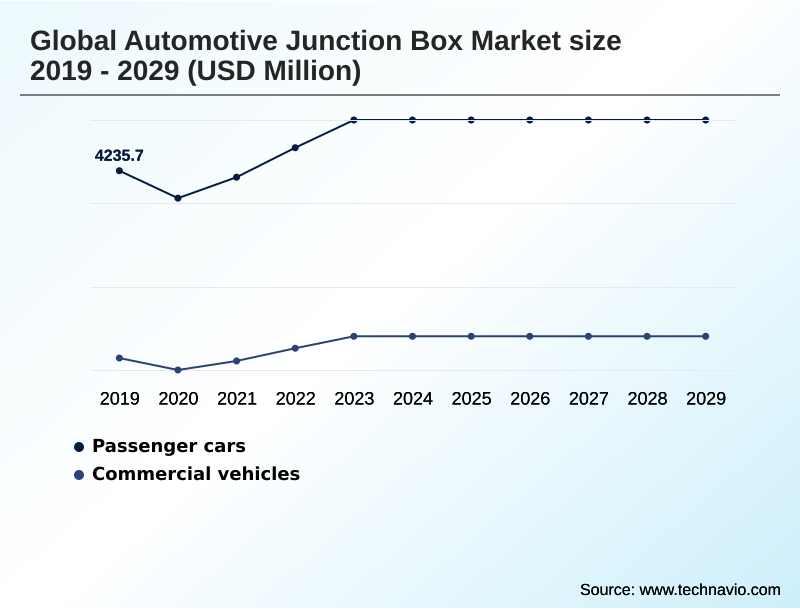

- By Vehicle Type - Passenger cars segment was valued at USD 4.89 billion in 2023

- By Technology - Smart junction box segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 6.42 billion

- Market Future Opportunities: USD 4.91 billion

- CAGR from 2024 to 2029 : 10.5%

Market Summary

- The automotive junction box market is transitioning from conventional fuse and relay centers to highly sophisticated electrical distribution systems. This evolution is driven by the inexorable rise of vehicle electrification and the increasing complexity of automotive electronics systems.

- A modern power distribution unit is no longer just a passive safety device; it is an intelligent hub responsible for high-current circuit management and seamless vehicle power distribution. In a typical business scenario, an automaker developing a new electric vehicle platform must optimize its entire vehicle electrical architecture.

- By implementing a zonal electrical architecture with multiple smart junction box modules, the company can significantly reduce the complexity and weight of its high-voltage wiring harness. This strategy not only improves manufacturing efficiency but also enhances the vehicle's overall performance and reliability.

- As vehicles become more connected and autonomous, the role of the power distribution module as a critical enabler of advanced functionalities will only intensify, making it a focal point for innovation in automotive power electronics and microcontroller-based technology.

What will be the Size of the Automotive Junction Box Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Junction Box Market Segmented?

The automotive junction box industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Vehicle type

- Passenger cars

- Commercial vehicles

- Technology

- Smart junction box

- Passive junction box

- Channel

- OEMs

- Aftermarket

- Geography

- APAC

- Japan

- China

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- APAC

By Vehicle Type Insights

The passenger cars segment is estimated to witness significant growth during the forecast period.

The passenger car segment is undergoing a significant transformation, driven by the dual trends of electrification and the proliferation of advanced electronic features.

The traditional reliance on a passive junction box is yielding to the adoption of the smart junction box, which is essential for managing the complex power requirements of modern vehicles.

As automakers integrate more advanced driver-assistance systems (ADAS), the demands on in-vehicle power management intensify. In response, designers are leveraging resettable poly switch devices and exploring zonal electrical architecture to streamline wiring and improve reliability.

The development of sophisticated thermal management solutions is critical, especially within electric vehicle powertrains.

This shift toward intelligent power distribution is not merely an upgrade; it is a fundamental redesign, with some integrated systems reducing the number of discrete components by over 30%, simplifying manufacturing and enhancing diagnostic capabilities in software-defined vehicle platforms.

The Passenger cars segment was valued at USD 4.89 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

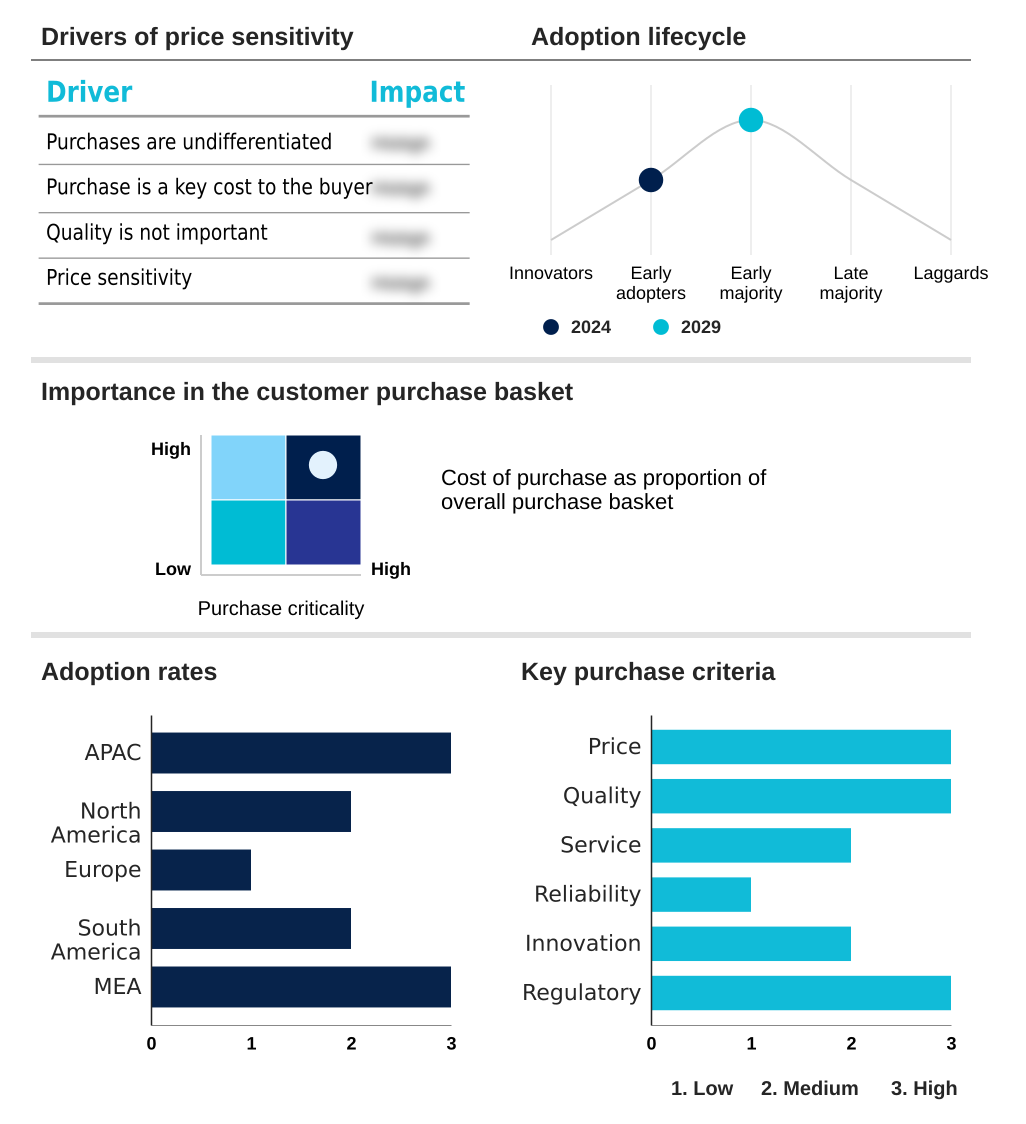

APAC is estimated to contribute 56.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Junction Box Market Demand is Rising in APAC Get Free Sample

The geographic landscape is defined by distinct regional dynamics and OEM sourcing strategy priorities.

APAC currently dominates, accounting for over 56% of the market's incremental growth, a direct result of its massive scale in electric vehicle production and a robust automotive manufacturing process for components like the high-voltage wiring harness.

This region's focus is on volume and cost-effective supply chain logistics.

In contrast, North America contributes nearly 23% of the growth, driven by demand for high-value, technologically advanced components such as the power distribution unit and battery disconnect unit, particularly for electric trucks and SUVs.

Europe's market is characterized by stringent automotive safety standards, pushing innovation in vehicle control unit integration and advanced power management solutions.

The dynamics of aftermarket replacement parts also vary, with mature markets demanding sophisticated replacements while emerging regions focus on basic component availability.

Market Dynamics

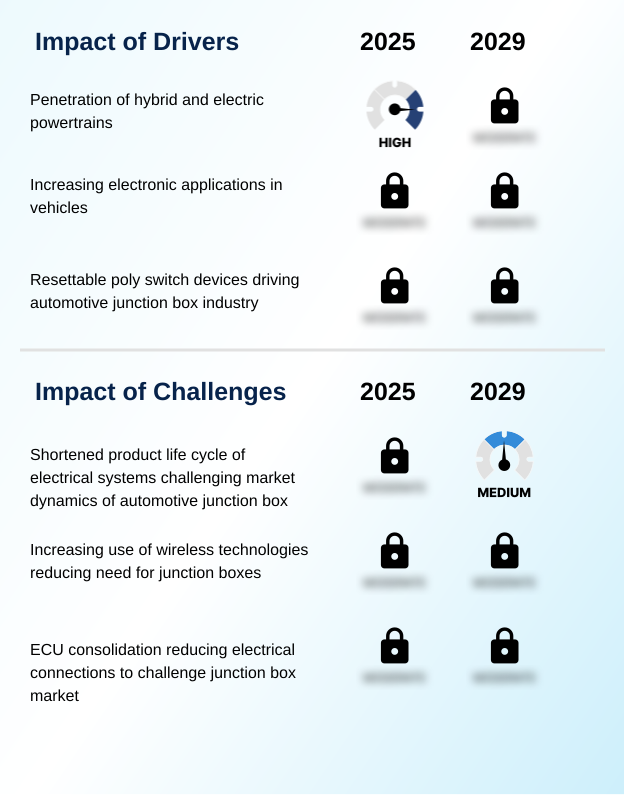

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A critical debate in modern vehicle design is the choice between a smart junction box vs passive junction box. While passive boxes offer simplicity, smart systems provide advanced diagnostics and reconfigurability, which is vital for complex electronics.

- The requirements for high-voltage junction box design for EVs are particularly stringent, demanding robust thermal management and safety mechanisms to handle immense power loads. Simultaneously, the impact of ECU consolidation on junction boxes is reshaping electrical architectures; as single controllers absorb more functions, the nature of power and data distribution shifts.

- This trend is a precursor to a full automotive zonal architecture power distribution model, where decentralized intelligent nodes replace a central box. The ultimate goal is achieving greater functional integration in power distribution units, which consolidates control, protection, and distribution into a single, optimized module.

- This integration offers significant operational benefits, with some analyses indicating it can reduce vehicle diagnostic and repair times by over 40% compared to traditional, distributed electrical systems, directly improving serviceability and lowering ownership costs.

What are the key market drivers leading to the rise in the adoption of Automotive Junction Box Industry?

- The increasing penetration of hybrid and electric powertrains is a key driver for the market's growth.

- The market's primary driver is the rapid pace of vehicle electrification, which necessitates a complete reimagining of vehicle power distribution.

- The transition to electric vehicle powertrains requires robust high-voltage junction box designs capable of high-current circuit management at levels exceeding 800 volts, a stark contrast to traditional 12-volt systems.

- This is compounded by the proliferation of automotive electronics systems, including advanced driver-assistance systems (ADAS) and sophisticated in-vehicle infotainment (IVI), which now account for up to 40% of a new vehicle's total cost.

- Adherence to evolving automotive safety standards is also compelling automakers to adopt more resilient and intelligent power architectures, further fueling demand for advanced power management solutions.

What are the market trends shaping the Automotive Junction Box Industry?

- The functional integration of junction boxes is an emerging market trend. This involves consolidating features from passive units with electronic module functionalities for enhanced performance.

- Key market trends are centered on the functional integration of the fuse and relay center into a single, intelligent solid-state smart junction box. This shift, driven by advanced microcontroller-based technology, allows for significant component miniaturization and simplifies complex automotive wiring systems. Innovations in automotive design engineering are leading to electrical component integration that reduces assembly weight by up to 15%.

- Furthermore, the use of lightweight wiring materials and heat-resistant composites is becoming standard practice to enhance efficiency and durability. This approach not only streamlines the manufacturing process but has been shown to reduce the number of individual power-switching components by over 25% in some platforms.

What challenges does the Automotive Junction Box Industry face during its growth?

- The shortened product life cycle of electrical systems presents a key challenge to the market dynamics of automotive junction boxes.

- Significant challenges are reshaping the competitive landscape, primarily stemming from deep architectural changes within the vehicle. The trend of ECU consolidation, where multiple controllers are replaced by a single, powerful automotive system-on-chip (SoC), is altering the traditional vehicle network topology and reducing the need for certain interconnect systems.

- This consolidation can eliminate up to 40% of physical ECUs, impacting the demand for associated wiring. Concurrently, the shortened automotive component lifecycle makes it difficult for suppliers to keep pace.

- For example, the 18-to-36-month development timeline for a new power distribution module directly conflicts with vehicle platform refreshes occurring every four to six years, creating immense pressure on automotive power electronics innovation and electrical system optimization.

Exclusive Technavio Analysis on Customer Landscape

The automotive junction box market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive junction box market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Junction Box Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive junction box market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amphenol Corp. - Key offerings center on advanced electrical distribution systems and smart junction boxes, engineered for modern vehicle electrification and complex power management requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amphenol Corp.

- Apparatebau Kirchheim-Teck GmbH

- Aptiv Plc

- BorgWarner Inc.

- Continental AG

- Dejini Systems

- Eaton Corp. Plc

- Fujikura Co. Ltd.

- Jenkin Electric Co.

- Lear Corp.

- Leoni AG

- M M Sankhla Electricals

- Motherson Group

- ON Semiconductor Corp.

- Sumitomo Electric Industries Ltd.

- TE Connectivity Ltd.

- Valeo SA

- Vitesco Technologies Group AG

- Yazaki Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive junction box market

- In May, 2025, Aptiv Plc announced a strategic partnership with a leading semiconductor firm to co-develop next-generation zonal controllers, integrating advanced processing with power distribution functionalities for software-defined vehicles.

- In February, 2025, Continental AG launched its new modular high-voltage junction box designed for 800-volt EV architectures, featuring enhanced thermal management and a 15% reduction in weight compared to previous models.

- In November, 2024, Lear Corp. confirmed a significant investment to expand its manufacturing facility in Mexico, aiming to increase production capacity for solid-state smart junction boxes by 40% to meet growing North American OEM demand.

- In August, 2024, Yazaki Corp. secured a major contract to supply its integrated power distribution units for a new line of all-electric commercial trucks, supporting the industry's transition to zero-emission logistics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Junction Box Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.5% |

| Market growth 2025-2029 | USD 4906.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 9.0% |

| Key countries | Japan, China, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive junction box market is undergoing a fundamental technological shift, moving beyond the traditional fuse and relay center to become a critical node in the vehicle's nervous system. Success for suppliers now hinges on mastering advanced automotive power electronics and microcontroller-based technology.

- The modern electrical distribution system, whether a centralized power distribution unit or a decentralized power distribution module, must handle sophisticated high-current circuit management for electric propulsion and autonomous systems. Integrating a battery disconnect unit into the high-voltage junction box is now a standard safety requirement.

- For boardroom strategy, the most pressing concern is the accelerated pace of innovation, with the average automotive component lifecycle shrinking from over eight years to just 4-6 years. This compression demands a complete overhaul of R&D cycles and supply chain agility to avoid obsolescence, compelling a strategic pivot toward modular and software-upgradable vehicle electrical architecture and automotive wiring systems.

- Mastery of the solid-state smart junction box and its role in a zonal electrical architecture is no longer optional but essential for survival.

What are the Key Data Covered in this Automotive Junction Box Market Research and Growth Report?

-

What is the expected growth of the Automotive Junction Box Market between 2025 and 2029?

-

USD 4.91 billion, at a CAGR of 10.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Vehicle Type (Passenger cars, and Commercial vehicles), Technology (Smart junction box, and Passive junction box), Channel (OEMs, and Aftermarket) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Penetration of hybrid and electric powertrains, Shortened product life cycle of electrical systems challenging market dynamics of automotive junction box

-

-

Who are the major players in the Automotive Junction Box Market?

-

Amphenol Corp., Apparatebau Kirchheim-Teck GmbH, Aptiv Plc, BorgWarner Inc., Continental AG, Dejini Systems, Eaton Corp. Plc, Fujikura Co. Ltd., Jenkin Electric Co., Lear Corp., Leoni AG, M M Sankhla Electricals, Motherson Group, ON Semiconductor Corp., Sumitomo Electric Industries Ltd., TE Connectivity Ltd., Valeo SA, Vitesco Technologies Group AG and Yazaki Corp.

-

Market Research Insights

- Market dynamics are increasingly shaped by the push for electrical system optimization and component miniaturization. The trend of ECU consolidation, facilitated by the adoption of powerful automotive system-on-chip (SoC) technology, is fundamentally altering vehicle network topology. This shift enables automakers to streamline designs and reduce wiring complexity.

- For instance, advanced thermal management solutions have been shown to improve the operational reliability of high-current components by over 20%, a critical factor in high-voltage applications. Concurrently, ongoing innovations in miniaturization have allowed for a 15% reduction in the physical footprint of power distribution modules, freeing up valuable space in increasingly crowded vehicle architectures.

- These advancements directly influence OEM sourcing strategy and design engineering priorities.

We can help! Our analysts can customize this automotive junction box market research report to meet your requirements.

RIA -

RIA -