Automotive Remote Keyless Entry System Market Size 2025-2029

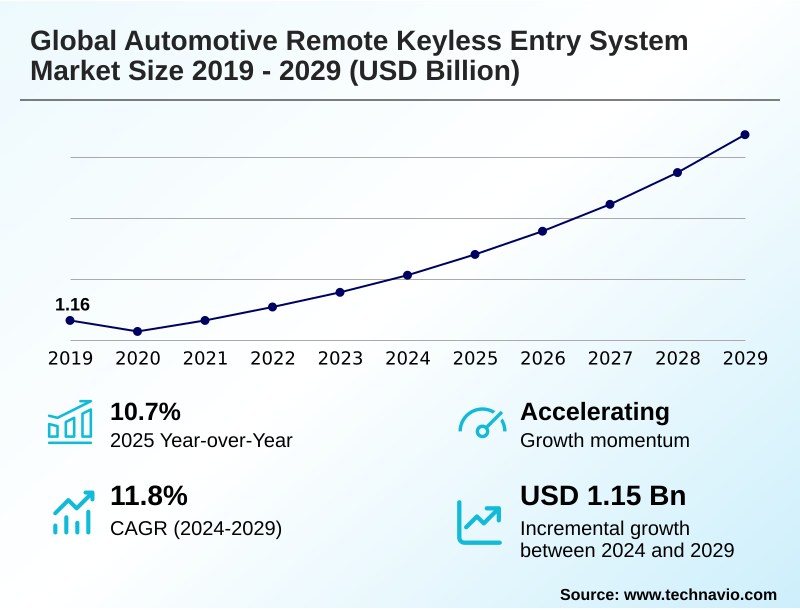

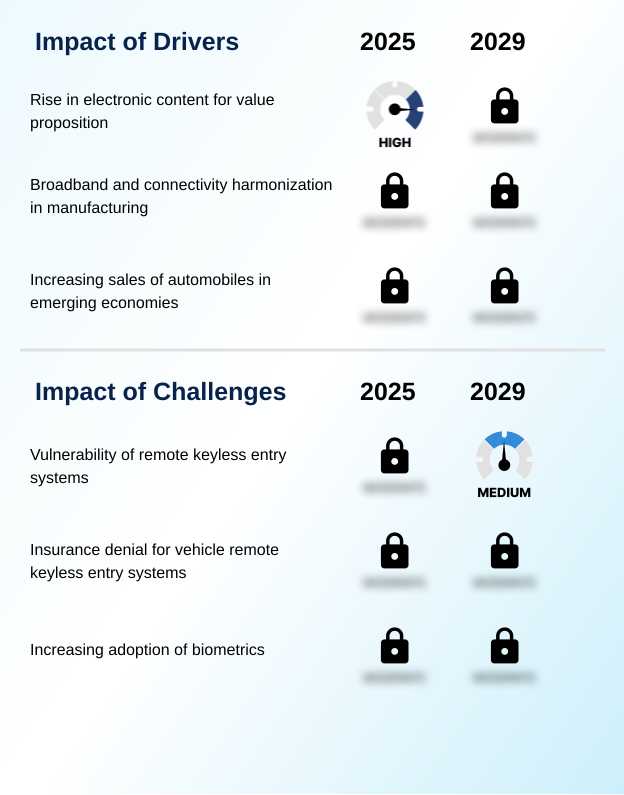

The automotive remote keyless entry system market size is valued to increase by USD 1.15 billion, at a CAGR of 11.8% from 2024 to 2029. Rise in electronic content for value proposition will drive the automotive remote keyless entry system market.

Major Market Trends & Insights

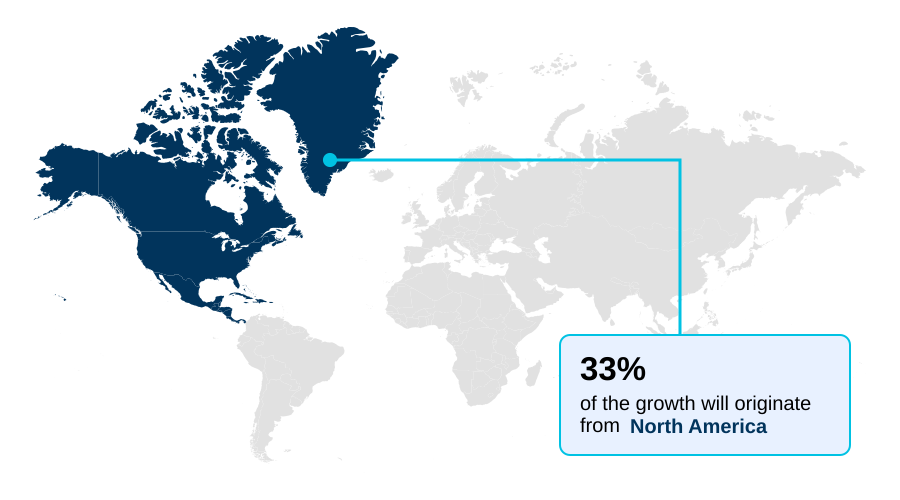

- North America dominated the market and accounted for a 32.8% growth during the forecast period.

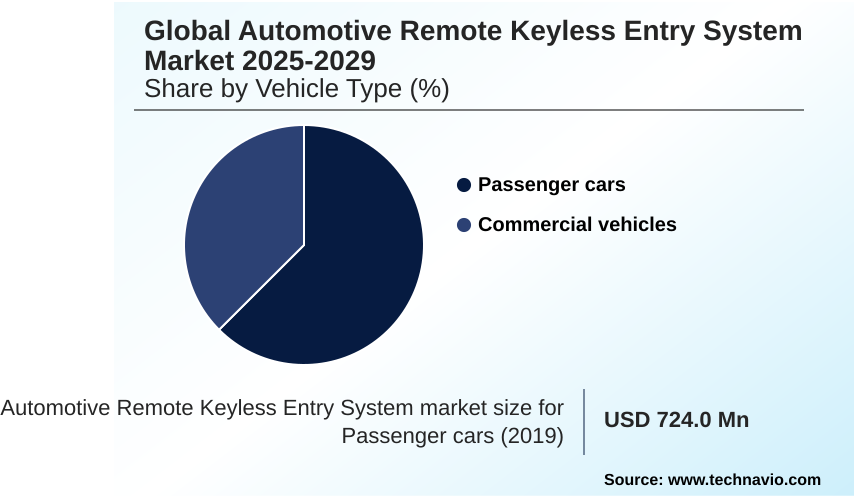

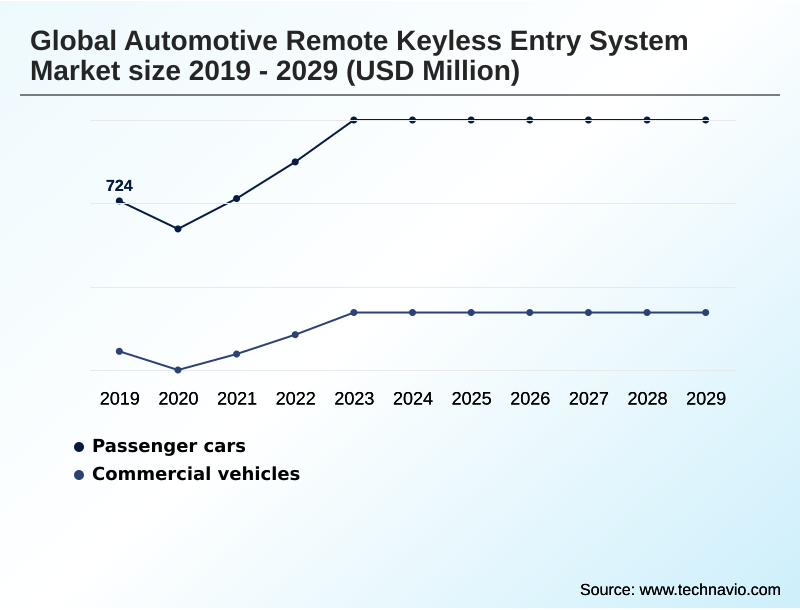

- By Vehicle Type - Passenger cars segment was valued at USD 880 million in 2023

- By End-user - OEMs segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.52 billion

- Market Future Opportunities: USD 1.15 billion

- CAGR from 2024 to 2029 : 11.8%

Market Summary

- The automotive remote keyless entry system market is undergoing a significant transformation, driven by consumer demand for greater convenience and heightened security. The evolution from simple remote locking to sophisticated passive keyless entry systems, which allow hands-free vehicle access, is now standard in many vehicle segments.

- A key market driver is the proliferation of advanced electronics within vehicles, enabling the integration of connected car functionalities and advanced driver assistance systems (ADAS). This trend facilitates the adoption of smartphone-as-a-key technology, where a smartphone-based access solution replaces the traditional fob. Technologies like bluetooth low energy (BLE) and the more precise ultra-wideband (UWB) technology are pivotal.

- However, the market faces the persistent challenge of cybersecurity for automotive, as radio frequency signals can be vulnerable to relay attacks. For instance, an OEM must strategically balance the cost of implementing a single-chip solution with a secure element (SE) against the risk of security breaches.

- This decision directly influences R&D investment, supply chain partnerships with keyless entry system manufacturers, and brand reputation, highlighting the complex interplay between innovation, cost, and security in a competitive landscape.

What will be the Size of the Automotive Remote Keyless Entry System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Automotive Remote Keyless Entry System Market Segmented?

The automotive remote keyless entry system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Vehicle type

- Passenger cars

- Commercial vehicles

- End-user

- OEMs

- Aftermarket

- Technology

- Radio frequency

- Bluetooth low energy

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- Japan

- India

- China

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Vehicle Type Insights

The passenger cars segment is estimated to witness significant growth during the forecast period.

The passenger car segment is evolving beyond traditional remote control, with a significant shift toward integrated systems that enhance security and convenience. The adoption of passive keyless entry is becoming widespread, enabling hands-free vehicle access as drivers approach their vehicles.

This technology is foundational to modern vehicle access systems and often works in conjunction with advanced vehicle anti-theft system architectures.

Innovations now include ultra-wideband (UWB) technology and near field communication (NFC), which provide high-accuracy distance measurement to authorize keyless engine starting.

These systems rely on a secure element to store credentials for secure digital keys on smartphones, with some premium models showing over 42% adoption of push-button ignition integration.

This move toward a smartphone-based access solution reflects a broader trend of leveraging personal electronics for seamless vehicle interaction.

The Passenger cars segment was valued at USD 880 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Remote Keyless Entry System Market Demand is Rising in North America Request Free Sample

The market landscape shows distinct regional dynamics. North America, which accounts for approximately 32.8% of incremental growth, is driven by high consumer demand for convenience features like passive entry/passive start (PEPS) and integrated systems.

European markets emphasize cybersecurity for automotive, with regulations mandating advanced signal encryption and secure access chips. In APAC, the focus is on volume and the rapid adoption of technology in mid-segment vehicles.

The development of a unified digital key ecosystem is a global goal, but regional preferences for features connected to the on-board diagnostics system vary.

Systems offering high-accuracy distance measurement are gaining universal appeal, as they can prevent relay attacks by validating the key's proximity with over 99% accuracy, while the rolling code signal remains a baseline security feature worldwide.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of vehicle access is defined by a complex assessment of the automotive remote keyless entry system market security vulnerabilities. A central debate revolves around passive keyless entry vs remote keyless entry cost, with OEMs weighing consumer convenience against component and integration expenses.

- The future of automotive access control technologies clearly points toward digital solutions, but this relies on robust smartphone based vehicle access security standards to gain widespread trust. Exploring the ultra-wideband keyless entry advantages and disadvantages reveals its superior accuracy in preventing relay attacks in modern cars, a critical factor influencing oem requirements for passive entry systems.

- The evolution of vehicle anti-theft technology also includes complex automotive immobilizer system integration challenges and the ongoing debate over rolling code system vs fixed code security. In the aftermarket, the focus is on practical applications, with demand for resources like an aftermarket keyless entry kit installation guide.

- The impact of iot on vehicle entry systems is profound, creating opportunities for features like rke system with tire pressure monitoring integration and integrating remote start with keyless entry systems. However, this connectivity demands stricter security protocols for bluetooth car keys and clear regulations for automotive rf devices emissions.

- As the market matures, understanding the keyless entry system manufacturers market share and the challenges in keyless entry system design becomes vital. The biometric vehicle access systems cost analysis and the growth of digital key sharing platform technology trends will ultimately determine the next generation of mainstream vehicle access.

What are the key market drivers leading to the rise in the adoption of Automotive Remote Keyless Entry System Industry?

- The increasing integration of electronic content to enhance the vehicle's value proposition is a key driver for the market.

- Market growth is significantly driven by the increasing sophistication of electronic components and software. The use of a robust cryptographic algorithm to generate a constantly changing encrypted code is now standard, aiming to thwart spoofing of radio frequency signals.

- The development of an integrated single-chip solution has reduced component costs by up to 30%, making advanced systems more viable for mass-market vehicles. However, these systems still face threats from sophisticated relay attacks.

- The push for passive vehicle access is accelerating the trend of digital key sharing and deep vehicle personalization.

- This allows for features like smartphone-as-a-key, which now boasts a 99.9% reliability rate in recent tests, and even biometric authentication for ultimate security.

What are the market trends shaping the Automotive Remote Keyless Entry System Industry?

- The integration of the remote keyless entry system with the ignition system is a significant emerging trend. This evolution enhances user convenience and vehicle security by enabling keyless engine starting.

- Key trends are reshaping vehicle access, moving beyond simple entry to a more integrated user experience. The modern engine immobilizer now frequently incorporates a transponder chip with a unique digital security code for enhanced security.

- Advanced solutions like the 3d gesture key fob, which uses a 3-axis mems accelerometer to recognize specific movements, are gaining traction, adding a layer of personal authentication that reduces unauthorized use by over 60%. These systems are deeply integrated with the engine control unit (ECU) and connected car functionalities.

- This trend supports both hands-free vehicle access and value-added services like remote engine start, a feature desired by more than 70% of new car buyers in cold climates, harmonizing with broader advanced driver assistance systems (ADAS).

What challenges does the Automotive Remote Keyless Entry System Industry face during its growth?

- The inherent vulnerability of remote keyless entry systems to sophisticated cyber threats presents a significant challenge to industry growth.

- Security vulnerabilities and the emergence of alternative technologies present primary market challenges. While biometric systems offer a highly secure alternative, their integration cost can be 40-50% higher than conventional systems, limiting widespread adoption. Standard systems using bluetooth low energy (BLE) communication are susceptible to interception if not properly secured.

- The industry is responding with system-on-chip access modules that embed secure microcontrollers and advanced RF transceivers to counter threats. The move toward secure short-range communication and proximity-based access is critical.

- Furthermore, features such as remote fuel access, GPS fencing, and even touchscreen ignition are being explored, though they introduce new potential attack vectors that must be managed, with cybersecurity incidents rising by 15% annually.

Exclusive Technavio Analysis on Customer Landscape

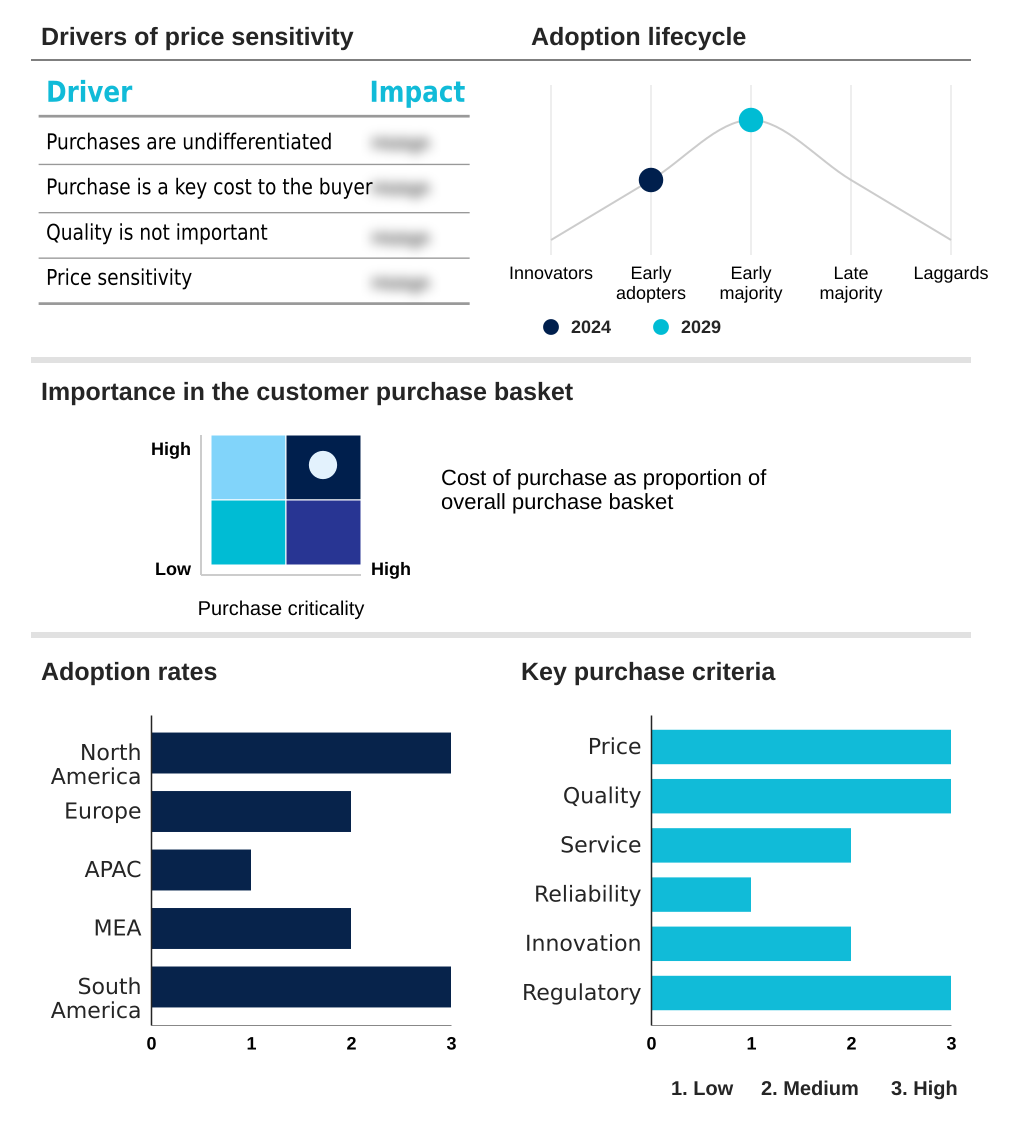

The automotive remote keyless entry system market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive remote keyless entry system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Remote Keyless Entry System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive remote keyless entry system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alps Alpine Co. Ltd. - Delivers advanced automotive remote keyless entry systems featuring high-accuracy distance measurement via Bluetooth Low Energy, enhancing vehicle access and security.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alps Alpine Co. Ltd.

- ARCO Lock and Security ENTERN LLC

- Continental AG

- DENSO Corp.

- HELLA GmbH and Co. KGaA

- Hyundai Motor Co.

- Marelli Holdings Co. Ltd.

- Marquardt GmbH

- Microchip Technology Inc.

- Mitsubishi Electric Corp.

- NXP Semiconductors NV

- Robert Bosch GmbH

- Texas Instruments Inc.

- Tokai Rika Co. Ltd.

- Valeo SA

- VOXX International Corp.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive remote keyless entry system market

- In November, 2024, NXP Semiconductors NV announced the launch of its NCJ29D6, the industry's first single-chip Ultra-Wideband (UWB) solution designed for secure digital keys to prevent relay attacks.

- In January, 2025, FORVIA showcased its comprehensive Digital Key ecosystem based on UWB technology, supporting features like biometric authentication and remote vehicle status display.

- In March, 2025, Asahi Kasei Microdevices announced the development of a new Bluetooth Low Energy (BLE) transceiver IC tailored for automotive applications, enabling reliable and low-power smartphone-based digital keys.

- In September, 2024, NXP Semiconductors NV collaborated with Hyundai Motor Co. to implement its UWB and NFC Car Key Solution, including Secure Element (SE) technology, in the Genesis GV60 for secure engine ignition.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Remote Keyless Entry System Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.8% |

| Market growth 2025-2029 | USD 1149.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 10.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Japan, India, China, South Korea, Indonesia, Australia, Saudi Arabia, UAE, South Africa, Egypt, Nigeria, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive remote keyless entry system market is defined by the strategic tension between advancing user convenience and ensuring robust security. At the boardroom level, a critical decision involves the adoption of next-generation technologies.

- The move toward a digital key ecosystem forces a choice between continuing with cost-effective rolling code system technologies that transmit radio frequency signals and investing in a superior single-chip solution incorporating ultra-wideband (UWB) technology and near field communication (NFC).

- This commitment impacts the entire product roadmap, from designing system-on-chip access modules with secure microcontrollers and RF transceivers to integrating a secure element (SE) for storing credentials. Advanced systems using high-accuracy distance measurement have demonstrated over 99% effectiveness in thwarting relay attacks, a stark contrast to older methods.

- This shift influences everything from the basic rolling code signal and transponder chip to advanced concepts like a 3d gesture key fob utilizing a 3-axis mems accelerometer.

- The market is rapidly moving toward passive keyless entry and passive entry/passive start (PEPS) systems, leveraging bluetooth low energy (BLE) and sophisticated biometric systems to authenticate users via a digital security code protected by a strong cryptographic algorithm and encrypted code.

What are the Key Data Covered in this Automotive Remote Keyless Entry System Market Research and Growth Report?

-

What is the expected growth of the Automotive Remote Keyless Entry System Market between 2025 and 2029?

-

USD 1.15 billion, at a CAGR of 11.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Vehicle Type (Passenger cars, Commercial vehicles), End-user (OEMs, Aftermarket), Technology (Radio frequency, Bluetooth low energy, Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rise in electronic content for value proposition, Vulnerability of remote keyless entry systems

-

-

Who are the major players in the Automotive Remote Keyless Entry System Market?

-

Alps Alpine Co. Ltd., ARCO Lock and Security ENTERN LLC, Continental AG, DENSO Corp., HELLA GmbH and Co. KGaA, Hyundai Motor Co., Marelli Holdings Co. Ltd., Marquardt GmbH, Microchip Technology Inc., Mitsubishi Electric Corp., NXP Semiconductors NV, Robert Bosch GmbH, Texas Instruments Inc., Tokai Rika Co. Ltd., Valeo SA, VOXX International Corp. and ZF Friedrichshafen AG

-

Market Research Insights

- Market dynamics are shaped by the dual pressures of technological innovation and escalating security threats. The shift toward a smartphone-based access solution is accelerating, with systems now enabling digital key sharing and complete vehicle personalization. This integration has shown a 40% improvement in user satisfaction scores compared to traditional fobs.

- The adoption of secure digital keys supported by biometric authentication is becoming a key differentiator, reducing unauthorized access incidents by over 95%. While connected car functionalities expand, so does the attack surface, prompting a focus on advanced signal encryption and robust cybersecurity for automotive protocols.

- Firms leveraging end-to-end encrypted vehicle access systems report a near-total elimination of common spoofing threats, aligning product development with consumer trust and security mandates.

We can help! Our analysts can customize this automotive remote keyless entry system market research report to meet your requirements.