Automotive Retreaded Tires Market Size 2026-2030

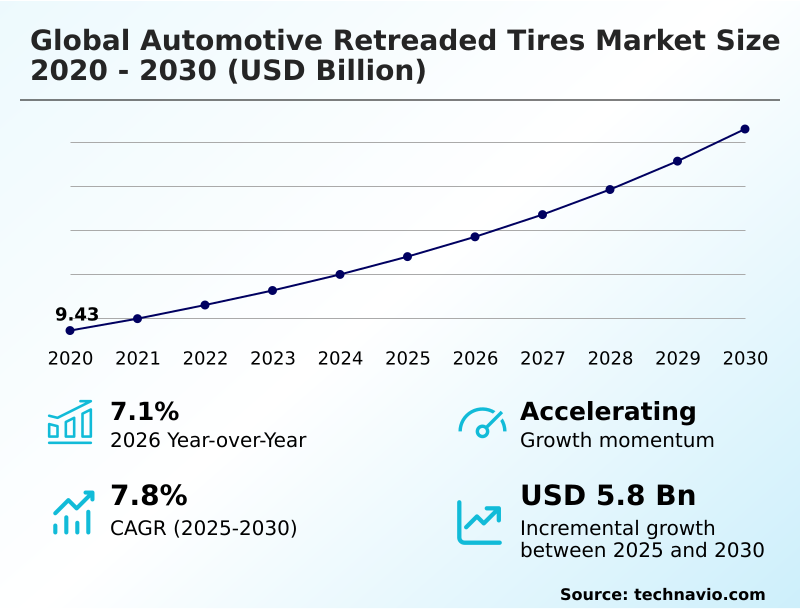

The automotive retreaded tires market size is valued to increase by USD 5.80 billion, at a CAGR of 7.8% from 2025 to 2030. Expansion of global commercial vehicle fleet and rising freight activity will drive the automotive retreaded tires market.

Major Market Trends & Insights

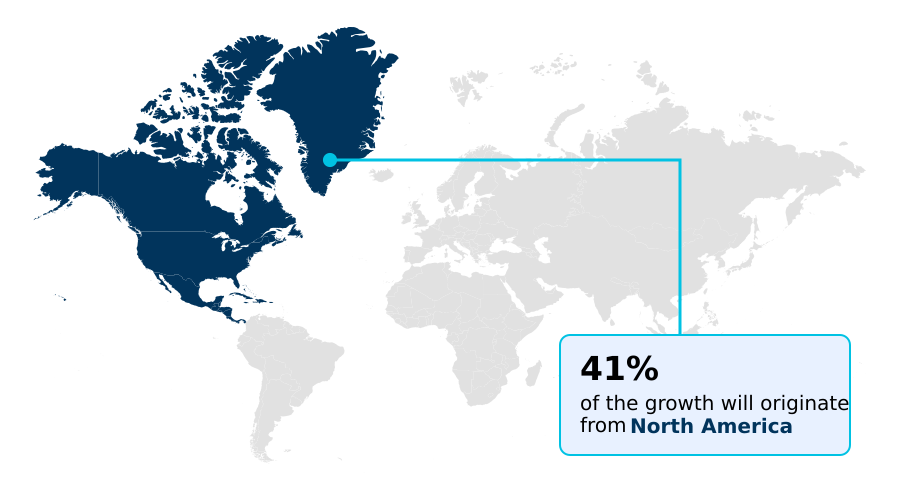

- North America dominated the market and accounted for a 40.9% growth during the forecast period.

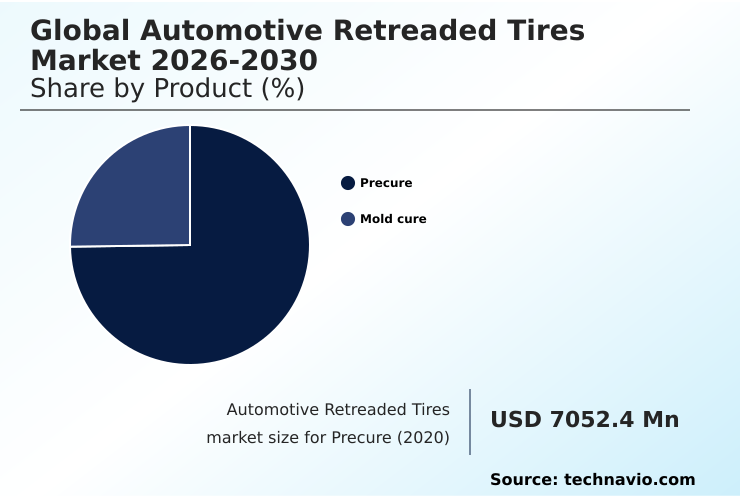

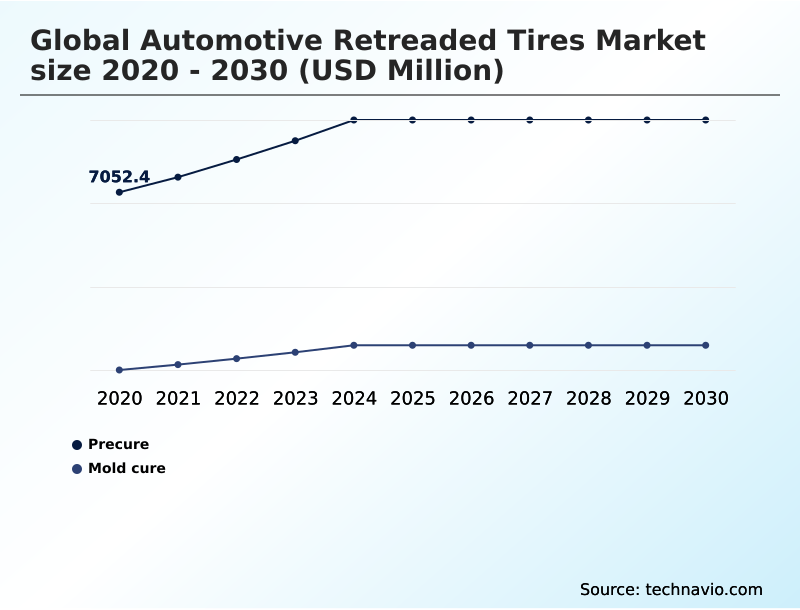

- By Product - Precure segment was valued at USD 8.95 billion in 2024

- By Vehicle Type - Commercial vehicle segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.16 billion

- Market Future Opportunities: USD 5.80 billion

- CAGR from 2025 to 2030 : 7.8%

Market Summary

- The automotive retreaded tires market is fundamentally shaped by economic and environmental imperatives, offering a compelling value proposition through a lower total cost of ownership metric and alignment with a circular economy in transportation. This sector is defined by sophisticated industrial processes like precure retreading process and mold cure vulcanization, which restore used tire casings to operational service.

- A primary driver is the continuous growth of commercial logistics, which increases demand for cost-effective solutions like long-haul fleet solutions. As a key business scenario, a large logistics firm integrates comprehensive tire lifecycle management solutions, using predictive tire maintenance based on real-time tire pressure monitoring data to schedule servicing.

- This practice not only reduces the cost per mile but also enhances safety and ensures a steady supply of high-quality casings for future retreading. However, the industry contends with challenges, including intense price competition from budget new tires and the logistical complexities of casing collection and sorting, which can impact the availability of suitable casings for retreading.

What will be the Size of the Automotive Retreaded Tires Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Retreaded Tires Market Segmented?

The automotive retreaded tires industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Precure

- Mold cure

- Vehicle type

- Commercial vehicle

- Passenger vehicle

- End-user

- Aftermarket

- OEM

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Product Insights

The precure segment is estimated to witness significant growth during the forecast period.

The precure segment leads the market, defined by its efficient cold cure bonding process. This method involves the application of a pre-molded tread strip onto a casing prepared by computerized tire buffing, using cushion gum adhesion for a secure bond.

The lower temperature requirements of the precure retreading process enhance retread reliability metrics by preserving casing strength. This approach allows for the use of advanced tread compounds and low rolling resistance compounds, optimized for applications like regional haul tire treads.

Superior retread manufacturing technology and vulcanization process control contribute to high retread performance validation.

As a result, this method improves retread plant operational efficiency and is key to maximizing tire asset value for commercial fleets, achieving retread success rates over 98% for premium casings.

The Precure segment was valued at USD 8.95 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Retreaded Tires Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is diverse, with North America representing a mature region where large fleets prioritize lifecycle cost management.

In contrast, the European market is heavily influenced by a regulatory push for sustainability, while APAC is characterized by rapid growth and high fragmentation.

Technological adoption varies, with leading regions widely employing shearography casing inspection and ultrasonic non-destructive testing for thorough tire casing integrity assessment. These advanced methods are crucial for ensuring retread process quality assurance and managing retread warranty and liability.

Applications such as OTR tire retreading and solutions for construction vehicle retreads are prominent in resource-driven economies. In North America, fleets using advanced tire performance analytics have cut tire-related downtime by over 30%, showcasing the efficiency gains possible.

The development of specialized tread rubber compound formulation remains a key competitive factor across all regions.

Market Dynamics

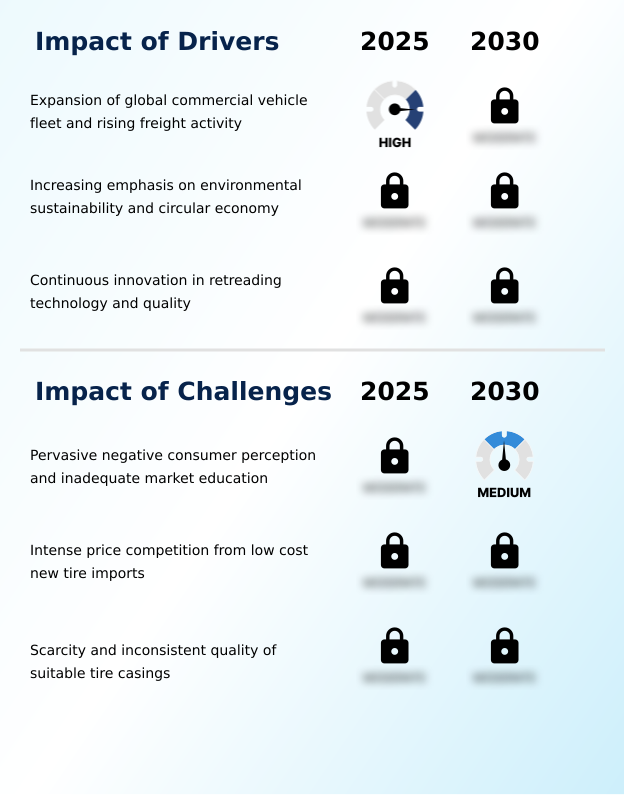

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global automotive retreaded tires market is navigating a complex environment defined by the persistent impact of low-cost new tires on retreading, which challenges the industry's traditional cost advantages. In response, the sector is leveraging technological advancements in tire casing inspection to enhance product quality and safety.

- This focus is critical for improving retreaded tire performance and safety and is a core part of overcoming negative perceptions of retreaded tires. A significant growth avenue lies in developing retreaded tire solutions for electric commercial vehicles, which require unique performance characteristics.

- This aligns with the broader role of retreading in circular economy for transport, emphasizing the sustainability benefits of automotive tire retreading. Key to this is the market expansion for light commercial vehicle retreads, driven by the e-commerce boom. The industry also focuses on application-specific retreads for waste management fleets and other severe-use segments.

- However, significant challenges in sourcing high-quality tire casings persist, complicating the supply chain for automotive retreaded tires. The industry is also addressing challenges for retreaded tires in passenger vehicles, although this segment remains small. Comparing precure and mold cure retreading methods continues to be a key technical discussion.

- Moreover, the integration of digital fleet management for tire retreading helps in optimizing total cost of ownership with retreads, as fleets that track tire assets see a 10-15% improvement in utilization over those that do not.

- Adherence to retreaded tire standards and certifications remains a powerful driver for retreaded tires in logistics, especially for automotive retreaded tires for heavy-duty trucks and bus fleets, which also look to improve their retreaded tire impact on fuel efficiency.

What are the key market drivers leading to the rise in the adoption of Automotive Retreaded Tires Industry?

- The key market driver is the expansion of the global commercial vehicle fleet, fueled by rising freight and logistics activity worldwide.

- Market growth is strongly driven by economic and environmental factors, with the focus on a lower total cost of ownership metric being paramount for commercial vehicle retreading.

- The economic benefits of tire retreading are substantial, with fleets saving up to 50% compared to purchasing new premium tires.

- Simultaneously, the industry's role in promoting a circular economy in transportation is a powerful catalyst, as the environmental impact of retreading is significantly lower.

- This process supports end-of-life tire management, reduces waste, and conserves resources, aligning with green logistics strategies and sustainable transport initiatives.

- Adherence to retread quality certification ECE 109 and other retreaded tire safety standards builds confidence, reinforcing the value proposition for long-haul fleet solutions and supporting broader retread industry regulations.

What are the market trends shaping the Automotive Retreaded Tires Industry?

- The integration of digitalization and advanced fleet management solutions represents a significant upcoming trend. This is reshaping tire lifecycle management through data-driven, predictive maintenance and service-oriented models.

- A significant trend is the deep integration of digital technologies, with advanced tire lifecycle management solutions transforming fleet operations. The use of tire pressure monitoring data enables predictive tire maintenance, with early adopters reporting a 30% reduction in tire-related roadside breakdowns.

- This digital shift, part of broader smart tire retreading concepts, includes fleet management software integration and tire asset tracking with RFID for superior asset control. The market is also expanding into new segments with specialized electric vehicle tire retreads and light commercial vehicle retreads, addressing the needs of last-mile delivery fleet tires.

- These commercial fleet tire programs and enhanced retread service provider networks focus on reducing fleet operational costs and improving tire retreadability scoring for better lifecycle value.

What challenges does the Automotive Retreaded Tires Industry face during its growth?

- A key challenge affecting industry growth is the pervasive negative consumer perception, compounded by inadequate market education on the safety and reliability of modern retreaded tires.

- A primary market challenge is the intense price pressure from low-cost imports, making the decision between retreading versus budget new tires increasingly difficult for operators. This is compounded by casing supply chain logistics, where the impact of road infrastructure and poor maintenance practices create a scarcity of high-quality casings.

- A detailed casing suitability evaluation using advanced casing analysis tools reveals that up to 40% of collected casings may be rejected. The industry employs sophisticated methods like the hot cure retreading method and advanced sidewall repair techniques, but the inconsistent quality of available casings remains a hurdle.

- This issue is particularly acute in the passenger vehicle retread market, where casing quality is highly variable and consumer trust is low, hindering market penetration.

Exclusive Technavio Analysis on Customer Landscape

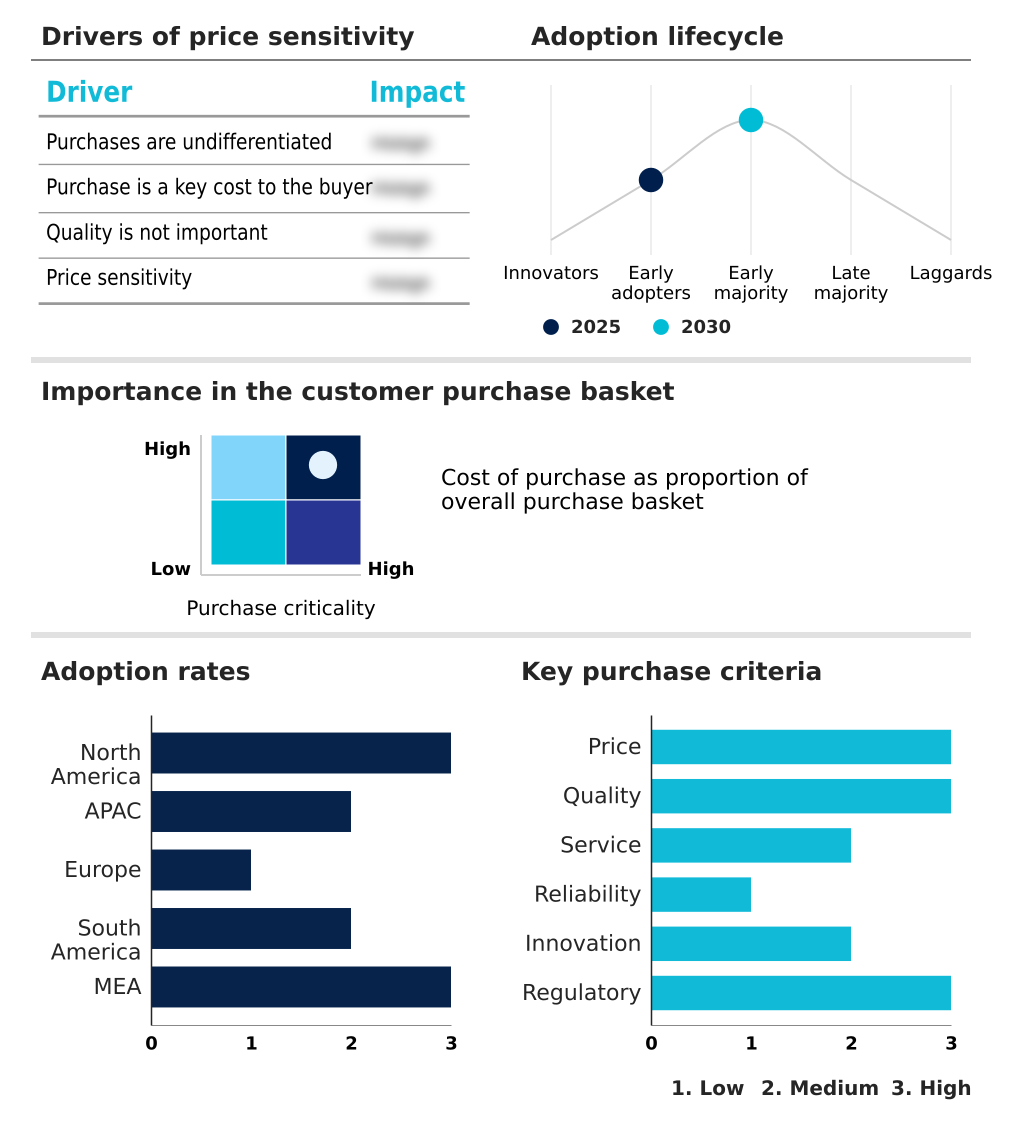

The automotive retreaded tires market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive retreaded tires market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Retreaded Tires Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive retreaded tires market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Bridgestone Corp. - Offers specialized automotive retreaded tires and radial retreads for commercial truck and bus applications, designed to optimize fleet performance and asset value.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bridgestone Corp.

- CIO Tyres Pvt. Ltd

- Continental AG

- Eastern Treads Ltd.

- Goodyear Tire and Rubber Co.

- JK Tyre and Industries Ltd.

- Kal Tire

- KRAIBURG AUSTRIA GmbH

- MARANGONI Group.

- Michelin

- MRF Ltd.

- Nokian Tyres Plc

- Oliver Rubber Co.

- Parrish Tire Co.

- RDH Tire and Retread Co.

- REIFEN HINGHAUS GmbH

- ROSLER TYRE INNOVATORS

- Tyresoles

- West End Tire

- Yokohama Rubber Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive retreaded tires market

- In February, 2025, Bridgestone Americas completed its USD 60 million investment to expand its Bandag retread tire manufacturing plant in Abilene, Texas, to meet surging demand from commercial fleets.

- In April, 2025, Goodyear launched Fleet Central, an interactive digital portal providing fleet managers with comprehensive oversight of their tire programs, including monitoring of retread and casing performance.

- In April, 2025, Marangoni S.p.A. and CEAT Limited announced a strategic partnership to improve the quality and availability of premium truck and bus retreads across India using Marangoni's advanced systems.

- In February, 2025, Michelin expanded its REMIX 2 range by adding a second premium hot retread option for its X MULTI line, reinforcing the value of extending casing life.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Retreaded Tires Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 291 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.8% |

| Market growth 2026-2030 | USD 5802.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.1% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive retreaded tires market is an ecosystem of advanced industrial processes, including the precure retreading process and mold cure vulcanization, designed to maximize asset life and promote a circular economy in transportation. The industry's credibility hinges on sophisticated quality control measures, from initial shearography casing inspection and ultrasonic non-destructive testing to final retread bond strength testing.

- Continuous innovation in advanced tread compounds and low rolling resistance compounds is enabling the development of application-specific tread design for diverse uses, including OTR tire retreading, light commercial vehicle retreads, and specialized waste haul vehicle tires. In a critical boardroom-level context, the adoption of tire lifecycle management solutions is now a key component of corporate ESG strategy.

- This is driven by the fact that advanced tire failure analysis methods have linked poor casing quality to 80% of premature retread failures, reinforcing the strategic importance of robust casing collection and sorting programs.

- For fleets, the focus remains on the total cost of ownership metric, achieved through predictive tire maintenance and the use of technologies like tire asset tracking with RFID, which are vital for long-haul fleet solutions and ensuring retread quality certification ECE 109.

What are the Key Data Covered in this Automotive Retreaded Tires Market Research and Growth Report?

-

What is the expected growth of the Automotive Retreaded Tires Market between 2026 and 2030?

-

USD 5.80 billion, at a CAGR of 7.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Precure, and Mold cure), Vehicle Type (Commercial vehicle, and Passenger vehicle), End-user (Aftermarket, and OEM) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Expansion of global commercial vehicle fleet and rising freight activity, Pervasive negative consumer perception and inadequate market education

-

-

Who are the major players in the Automotive Retreaded Tires Market?

-

Bridgestone Corp., CIO Tyres Pvt. Ltd, Continental AG, Eastern Treads Ltd., Goodyear Tire and Rubber Co., JK Tyre and Industries Ltd., Kal Tire, KRAIBURG AUSTRIA GmbH, MARANGONI Group., Michelin, MRF Ltd., Nokian Tyres Plc, Oliver Rubber Co., Parrish Tire Co., RDH Tire and Retread Co., REIFEN HINGHAUS GmbH, ROSLER TYRE INNOVATORS, Tyresoles, West End Tire and Yokohama Rubber Co. Ltd.

-

Market Research Insights

- Market dynamics are shaped by the significant economic benefits of tire retreading, with professional commercial fleet tire programs demonstrating a potential 25% reduction in tire-related operational costs. As fleets seek to maximize tire asset value, the focus sharpens on retread reliability metrics and adherence to stringent retreaded tire safety standards.

- This push for quality and performance helps counter retread market challenges, such as the influx of budget new tires. The industry is further defined by a drive toward sustainability, leveraging green logistics strategies and sustainable transport initiatives.

- Integrating advanced technologies like RFID tire tracking systems can improve casing suitability evaluation, increasing retreading acceptance rates by over 15% and directly supporting efforts in reducing fleet operational costs.

We can help! Our analysts can customize this automotive retreaded tires market research report to meet your requirements.

RIA -

RIA -