Enjoy complimentary customisation on priority with our Enterprise License!

The automotive ultracapacitor market size is forecast to increase by USD 165.09 million, at a CAGR of 15.2% between 2022 and 2027. The market's expansion is influenced by various factors, with notable contributions from the burgeoning electric vehicle (EV) automotive industry, escalating governmental backing, and the shift from rechargeable batteries to ultracapacitors in EVs. The rapid growth of the EV automotive sector has created a surge in demand for advanced energy storage solutions, driving the adoption of ultracapacitors. Government initiatives and policies promoting sustainable transportation and clean energy have further propelled market growth by incentivizing the adoption of ultracapacitor technology. The transition from traditional rechargeable batteries to ultracapacitors offers several advantages, including rapid charging, longer lifespan, and improved energy efficiency, making them a preferred choice for EV manufacturers and consumers alike. These factors collectively contribute to the dynamic growth and evolution of the ultracapacitor market within the electric vehicle industry.

To learn more about this report, Download Report Sample

This report extensively covers market segmentation by type (double-layered capacitors, pseudo capacitors, and hybrid capacitors), application (brake regeneration, start-stop operation, and active suspension), and geography (APAC, Europe, North America, South America, and Middle East and Africa). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

The Market is driven by the increasing demand for electric energy solutions in the automobile market, particularly in EVs (Electric Vehicles) and hybrid cars. Factors such as fuel efficiency, reduced greenhouse gas emissions, and the growth of the global electric car market are key drivers. Trends include the rising adoption of ultracapacitors and supercapacitors for their high power density and extended lifecycle, contributing to improved energy efficiency. Challenges lie in optimizing electrostatic charge separation and ensuring seamless integration with renewable energy solutions amidst the shift towards electrification of vehicles. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The growing EV automotive industry is a key factor driving the growth of the global market. The EV automotive industry consists of many companies that design, develop, manufacture, and sell various types of vehicles, such as Hybrid electric vehicles, plug-in hybrid electric vehicles, and battery electric vehicles. Due to the increasing turnover, it has experienced significant growth worldwide.

According to the International Energy Agency (IEA), globally, the number of electric cars by the end of 2021 was about 16.5 million, triple the amount in 2018. Such development will positively influence the demand for automotive ultracapacitors, which, in turn, will drive the growth of the market in focus during the forecast period.

Increasing focus on advanced ultracapacitors is the primary trend in the global market growth. Recent technological advances have led to the development of fiber-based ultracapacitors that can be used to power portable electrical devices and other small electronic devices. Fiber-based ultracapacitors such as 6.3 Wh/mm3 carbon-based capacitors have the highest storage capacity. Fiber-based materials offer access to a significant surface area and are highly conductive. The large surface area is said to increase the energy storage capacity of these capacitors.

Moreover, like all capacitors, these flexible ultracapacitors can charge and release energy much faster than batteries. They are expected to be integrated into the clothing of soldiers and wearable medical or communication devices used on battlefields. Such development is expected to propel the demand for ultracapacitors in the automotive industry, which, in turn, will boost the growth of the market in focus during the forecast period.

The high-cost burden is a major challenge to the global market growth. The cost of incorporation of ultracapacitors in an electric car ranges from USD 2,000 to USD 10,000 per kWh. On the other hand, batteries for electric cars cost between USD200 and USD1,000 per kWh. Ultracapacitors are almost ten times more expensive than the available substitutes. However, the cost of ultracapacitors is expected to decline in the near future with significant investments in research and development (R&D).

Customers are hesitant to adopt ultracapacitors as the market has very few suppliers. Moreover, ultracapacitors have not been tested in many applications. This discourages potential customers from taking risks and investing in these devices. Such factors will negatively impact the market in focus during the forecast period.

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Market Customer Landscape

companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

CAP-XX Ltd.- The company offers automotive ultracapacitors such as CAP-XX supercapacitors. Also, The company offers a wide range of products such as Murata supercaps, prismatic ultra-thin supercaps, cylindrical supercaps, and others.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The Market is driven by the need for electric energy storage solutions in various sectors, especially commercial cars and passenger cars. The RBS (Regenerative Braking System), a key feature in electric and hybrid vehicles, underscores the demand for efficient energy recovery devices. Ultracapacitors and supercapacitors emerge as pivotal technologies, offering high power density and extended lifecycle benefits. These energy storage devices, including automotive ultracapacitors and electric double-layer capacitors (ELDC), are integral to enhancing fuel efficiency and reducing greenhouse gas emissions. As the automotive industry continues its electrification journey, the demand for renewable energy solutions and improved energy efficiency through ultracapacitors remains on the rise.

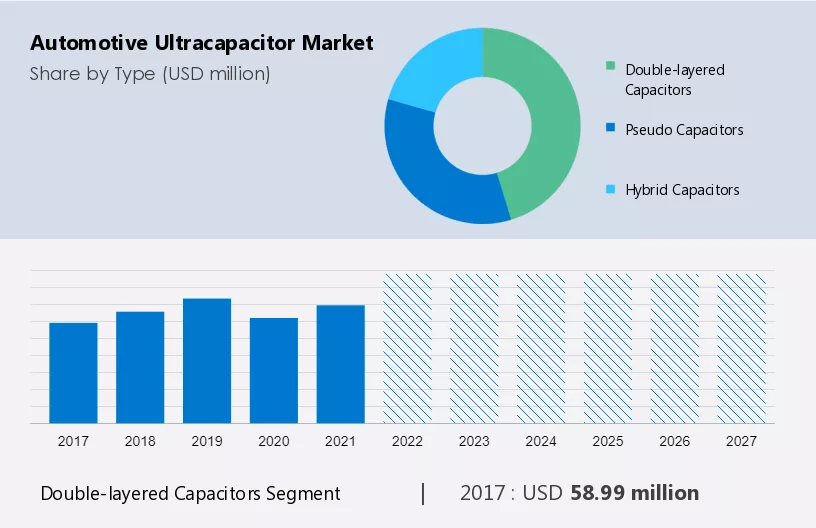

The market share growth by the double-layered capacitors segment will be significant during the forecast period. The double-layered capacitors or electric double-layered capacitors (EDLCs) segment dominated the market in focus by type in 2022 in terms of market size. EDLCs have the energy storage properties of batteries and the power discharge characteristics of capacitors.

Get a glance at the market contribution of various segments Request a PDF Sample

The double-layered capacitors were valued at USD 58.99 million in 2017 and continue to grow by 2021. The main reason for the EDLCs segment is the growing demand for compact and energy-efficient storage devices in end-user segments such as EVs and transportation. The use of regenerative braking systems in cars and buses will be a significant step, with EDLCs absorbing all the kinetic energy from automobiles and storing it for later use. The advent of start and stop systems, which shut down the engine and stop internal combustion, will help conserve power and reduce emissions from cars. The demand for EDLCs is expected to increase with the rising number of vehicles adopting this technology, which in turn will propel the market in focus during the forecast period.

For more insights on the market share of various regions Request PDF Sample now!

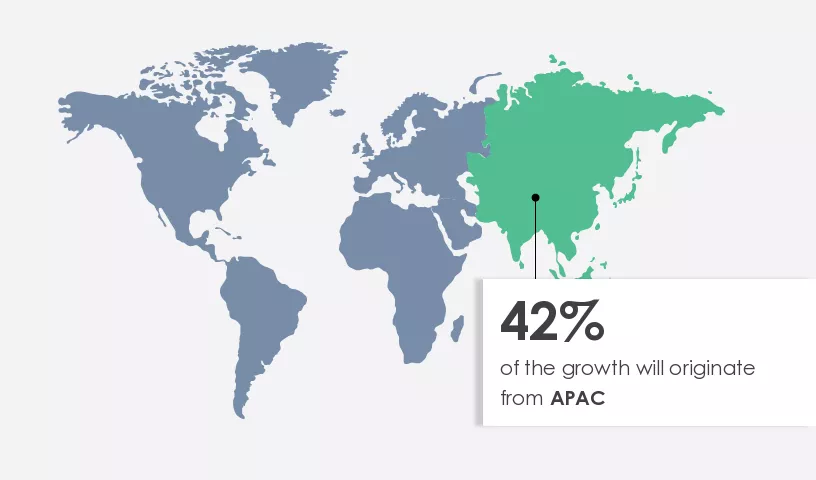

APAC is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. Promising economic growth potential in emerging countries (such as China and India) and government initiatives are expected to drive the regional market in focus during the forecast period. The adoption of electric vehicles is increasing in China, Japan, and India. In APAC, China is the leading country in terms of the inventory of electric vehicles, followed by India. The governments of India and China are supportive of the adoption of electric vehicles. The mandate for new energy vehicles (NEVs) in China has increased the adoption of EVs across the country. Such favorable government initiatives undertaken by governments are boosting the demand for ECVs from fleet owners in APAC and, in turn, are anticipated to propel the market in the region during the forecast period.

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Million" for the period 2023 to 2027, as well as historical data from 2017 to 2021 for the following segments

The Market is propelled by the global shift towards sustainable energy, catalyzed by concerns over greenhouse gas emissions and the increasing demand for energy-efficient solutions in the electric vehicle (EV) and hybrid car segments. As the automotive industry leans towards electrification and green technologies, ultracapacitors emerge as pivotal components, offering high power density, extended lifecycle, and quick charging times. This market witnesses advancements in electrochemical energy storage devices like ultracapacitors and electric double-layer capacitors (ELDC), driving efficiency and performance in vehicles. The market for automotive supercapacitors is driven by technological advancements in energy storage solutions, particularly in the context of renewable energy storage systems (ESS). As telecommunications and data processing technologies continue to evolve, ultracapacitors find applications in electronic circuits and frequency characteristics, contributing to enhanced efficiency and performance in propulsion systems. Overall, the Automotive Ultracapacitor Market is poised for growth, fueled by advancements in energy storage technology, increasing EV adoption, and the demand for energy-efficient and sustainable transportation solutions.

Moreover, Original Equipment Manufacturers (OEMs) like Morand eTechnology are at the forefront, developing energy storage solutions and hybrid systems that utilize ultracapacitors to provide bursts of power and complement renewable energy storage systems (ESS). The integration of ultracapacitors into control systems and power electronics further enhances their role in both passenger cars and commercial vehicles, contributing significantly to the transformation of the automotive landscape towards sustainable and efficient propulsion technologies. The Market is experiencing a surge in demand due to the rapid growth of the electric vehicles (EVs) and hybrid cars segments within the automobile market. With a strong emphasis on fuel efficiency and sustainability, the market for ultracapacitors is thriving as they play a crucial role in enhancing energy recovery through stop-start and regenerative braking systems (RBS). These systems enable efficient energy storage and electrostatic charge separation, making them essential components in the electrification of vehicles and the transition from internal combustion engine (ICE) vehicles to battery-powered electric vehicles (EVs) and plug-in electric vehicles.

Furthermore, ultracapacitors are characterized by their high energy density, quick charging times, and suitability for hybrid systems and mild hybrid setups. They complement renewable energy solutions and grid infrastructure, contributing to a more sustainable automotive sector. Their role in EV fast charging is particularly noteworthy, with automotive supercapacitors and electric double-layer capacitors (ELDC) being instrumental in achieving rapid charging capabilities. As technological advancements continue to improve energy storage solutions, ultracapacitors stand out for their efficiency, reliability, and compatibility with various propulsion types in both passenger cars and commercial vehicles. This trend underscores the pivotal role of ultracapacitors in shaping the future of automotive propulsion and energy management systems.

In addition, the Market is witnessing significant growth driven by the increasing adoption of EVs (Electric Vehicles) worldwide. As the global electric car market expands, the demand for ultracapacitors in both passenger cars and commercial vehicles is on the rise. One of the key technologies fueling this growth is the Regenerative Braking System (RBS), which allows for efficient energy recovery during braking. Ultracapacitors, also known as electric double-layer capacitors (ELDC), play a crucial role in energy storage solutions for vehicles, especially in EV fast charging scenarios. Their ability to store and discharge electrical energy rapidly makes them ideal for supporting hybrid vehicles and mild hybrid systems. The market landscape depends on ICE vehicle, electric vehicles (EV), ultracapacitors in EV fast charging, technological advancement, energy storage solution, hybrid system, renewable energy storage system (ESS), passenger car, commercial vehicle, propulsion type, Energy recovery device, automotive supercapacitor, electric double-layer capacitor (ELDC), energy storage device. Moreover, ultracapacitors exhibit superior performance compared to traditional batteries like lithium-ion, offering extended lifecycle, higher power density, and faster charging capabilities.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 15.52% |

|

Market growth 2023-2027 |

USD 165.09 million |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

14.4 |

|

Regional analysis |

APAC, Europe, North America, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 42% |

|

Key countries |

US, China, Japan, India, and Germany |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

CAP XX Ltd., Cornell Dubilier Electronics Inc., Eaton Corp. Plc, GODI India Pvt. Ltd., Kyocera Corp., LICAP Technologies Inc., LS MTRON Ltd., Nippon Chemi Con Corp., Panasonic Holdings Corp., Shanghai Aowei Technology Development Co. Ltd., Skeleton Technologies GmbH, SPEL TECHNOLOGIES PVT. LTD., Systematic Power Manufacturing LLC, TAIYO YUDEN Co. Ltd., TDK Corp., UCAP Power Inc., VINATech Co. Ltd., Yageo Corp., Yunasko Ltd., and Zoxcell Ltd. |

|

Market dynamics |

Parent market analysis, market forecast, market research and growth, market growth analysis, Market forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by Application

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.