Aviation Test Equipment Market Size 2024-2028

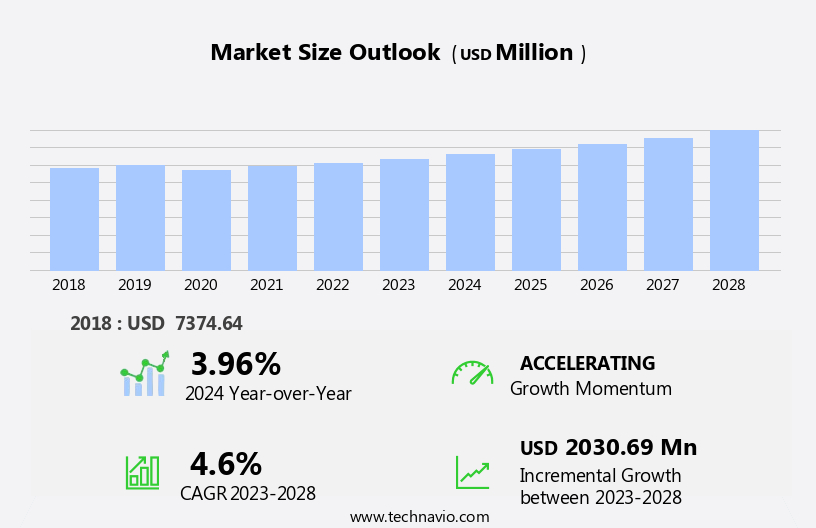

The aviation test equipment market size is forecast to increase by USD 2.03 billion at a CAGR of 4.6% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing demand for aircraft testing activities. With the opening of new aircraft testing labs and the expansion of existing ones, the market is poised for continued expansion. However, this growth comes with challenges, primarily the shortage of skilled workforce for aircraft components testing. This labor shortage may hinder market growth if not addressed through training programs or outsourcing solutions. To capitalize on this market opportunity, companies must focus on innovation and efficiency in their test equipment offerings, as well as invest in workforce development to meet the growing demand for skilled labor.

- By staying abreast of the latest trends and addressing the challenges head-on, companies can effectively navigate this dynamic market and position themselves for long-term success.

What will be the Size of the Aviation Test Equipment Market during the forecast period?

- The market encompasses a range of instruments and systems used to evaluate the performance and compliance of aircraft and weapon systems. Key components of this market include pressure probes, temperature sensors, strain gauges, potentiometers, current transducers, and voltage measurement devices. These tools play a critical role in ensuring the safety and efficiency of aircraft by measuring various parameters such as component temperatures, pressure distribution, electrical power, and cargo temperature. The market is driven by the growing demand for advanced testing solutions in the aviation and defense industries to support qualification, calibration, and separation assurance. Software-adaptable solutions are increasingly popular due to their flexibility and ability to accommodate changing testing requirements.

- Hydraulic systems and weapon systems also require specialized test equipment for proper evaluation and maintenance. Overall, the market is expected to experience steady growth due to the continuous evolution of aircraft technology and the increasing importance of safety and reliability in the aviation and defense sectors.

How is this Aviation Test Equipment Industry segmented?

The aviation test equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Commercial

- Military

- Type

- Electric

- Hydraulic

- Pneumatic

- Geography

- North America

- US

- Canada

- Europe

- Russia

- UK

- APAC

- China

- South America

- Middle East and Africa

- North America

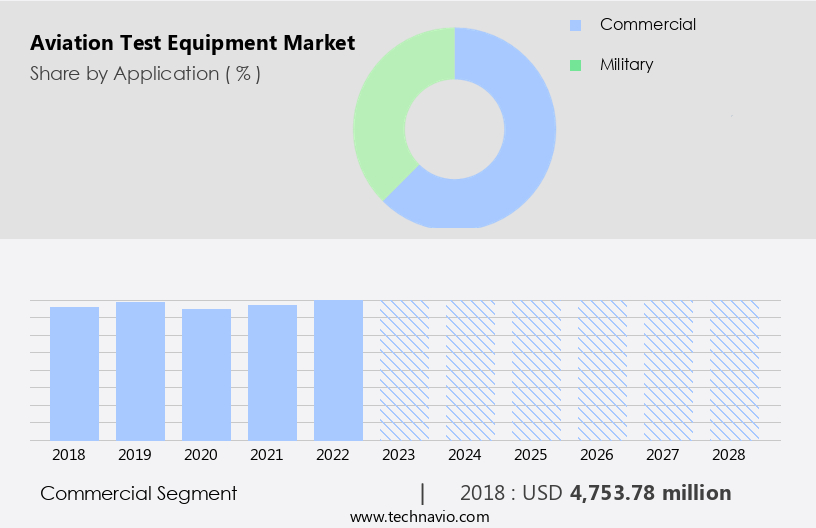

By Application Insights

The commercial segment is estimated to witness significant growth during the forecast period.

The commercial segment of the market is experiencing significant growth due to the expanding commercial aviation sector. The increasing demand for air travel is driving this growth. According to the International Air Transport Association (IATA), North American carriers reported a 28.3% annual traffic increase in 2023 compared to 2022. Total air traffic globally in 2023 rose 36.9% compared to 2022. This growth is attributed to various factors, including the use of advanced technologies in aviation, such as composite materials, automation, cyber protection, and ML (Machine Learning) in avionics. Additionally, military expenditure on aviation technology continues to be a significant contributor to the market.

The aviation industry's focus on ensuring separation assurance, weather conditions monitoring, and no-fault-found (NFF) analysis is also driving the demand for test equipment. The market encompasses various types of equipment, including power test equipment, pneumatic test equipment, hydraulic test equipment, pressure probes, potentiometers, and temperature sensors, among others. These instruments are used for calibration, inspection, data collection, and evaluation of aircraft components, engines, and systems. The market also includes software-adaptable solutions, such as model-based definition (MBD), which enable the integration of test data with digital mockups of aircraft designs. Furthermore, the use of aviation data buses, communication systems, and radar technology in test equipment enhances their functionality and accuracy.

Overall, The market is expected to continue its growth trajectory, driven by the increasing demand for efficient and reliable testing solutions in the aviation industry.

Get a glance at the market report of share of various segments Request Free Sample

The Commercial segment was valued at USD 4.75 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

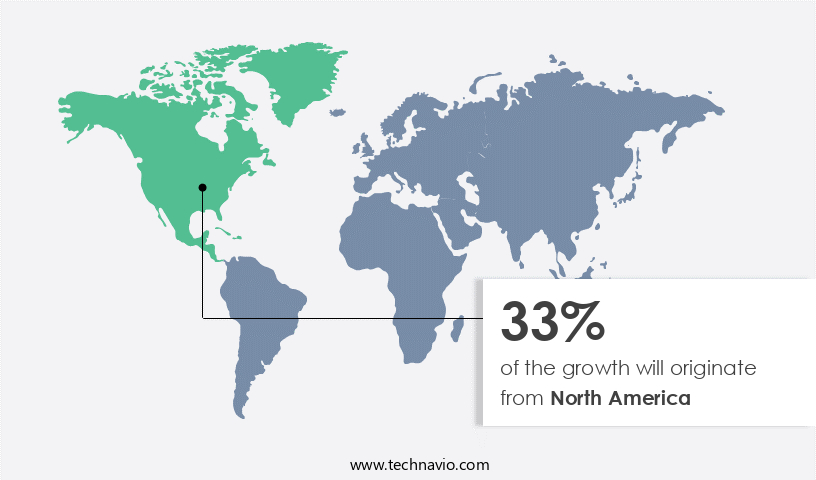

North America is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The North American the market is poised for expansion due to the heightened emphasis on ensuring safety and quality in the aviation industry. Key players in this sector, including Boeing, Embraer, and Bombardier, are prioritizing fault detection, product inspection, and calibration to maintain the highest standards. Additionally, the importance of regular maintenance and testing for military and commercial aircraft is driving demand for advanced aviation test equipment. This growth can be attributed to the integration of automation, cyber protection, and data collection systems in aviation devices, such as engines, avionics, and communication systems. Furthermore, the adoption of technologies like Machine Learning (ML), pressure probes, potentiometers, and temperature sensors is enhancing the capabilities of aviation test equipment.

The market is also witnessing the emergence of software-adaptable solutions, including pneumatic, hydraulic, and electrical power test equipment, as well as radar surveillance mechanisms and fiber optics. The Federal Aviation Administration (FAA) and the defense industry are significant contributors to the market, with a focus on ensuring separation assurance, weather conditions monitoring, and mid-air collision avoidance. Overall, the North American the market is expected to experience significant growth due to the increasing demand for advanced testing solutions in the aviation industry.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Aviation Test Equipment Industry?

- Increasing aircraft testing activities is the key driver of the market.

- The global aerospace testing market is experiencing significant growth due to the increasing production of aircraft, technological advancements, and regulatory requirements. As new aircraft are developed, existing systems are upgraded, or modifications are made, extensive testing is necessary to ensure safety, reliability, and compliance with evolving standards. This demand encompasses a range of testing parameters, from avionics to structural integrity, creating a sustained and growing market for aerospace testing services worldwide. Recent developments in aircraft testing include The Boeing Company's announcement in April 2023 to expand its ecoDemonstrator flight testing program using a 787-10 Dreamliner.

- This initiative involves partnerships with four countries to test the operational efficiency of the aircraft, further emphasizing the importance of rigorous testing in the aviation industry.

What are the market trends shaping the Aviation Test Equipment Industry?

- Opening of new aircraft testing labs is the upcoming market trend.

- The market experiences growth due to the establishment of new testing facilities. These advanced laboratories, equipped with modern technologies, broaden the aerospace industry's testing capabilities. With an expanding network of testing labs, aircraft manufacturers can benefit from specialized services, expediting the testing process for individual components, systems, and complete aircraft. This advanced testing infrastructure facilitates shorter development cycles, adherence to stringent regulations, and fosters innovations in aviation technology.

- The availability of extensive testing solutions caters to the increasing demand for efficient and comprehensive testing services, thereby fueling the expansion of the market.

What challenges does the Aviation Test Equipment Industry face during its growth?

- Shortage of skilled workforce for aircraft components testing is a key challenge affecting the industry growth.

- The market faces a significant challenge due to the shortage of skilled labor in the aerospace industry. The complex nature of testing aircraft components necessitates a workforce with specialized expertise in areas such as avionics, materials science, aerodynamics, and structural engineering. Keeping up with the continuous evolution of aircraft technologies requires a workforce that can adapt quickly. However, the availability of workers with up-to-date knowledge and training for testing advanced aerospace technologies is limited. For instance, there is a scarcity of avionics engineers capable of testing sophisticated avionic systems.

- This shortage is particularly evident when developing and validating the intricate electronic systems found in modern aircraft. The demand for such expertise is increasing as the aerospace industry advances technologically. Consequently, addressing this labor shortage is crucial for the growth and success of the market.

Exclusive Customer Landscape

The aviation test equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aviation test equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, aviation test equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - The company specializes in providing advanced aviation test solutions, encompassing equipment for inspecting intricate internal components and tools dedicated to assessing hydraulic and pneumatic systems' performance. These solutions cater to the rigorous demands of the aviation industry, ensuring optimal functionality and safety.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- AMETEK Inc.

- ATEQ AVIATION

- BAE Systems Plc

- Cobham Ltd.

- Curtiss Wright Corp.

- dSPACE GmbH

- General Electric Co.

- Honeywell International Inc.

- L3Harris Technologies Inc.

- Leonardo DRS

- Lockheed Martin Corp.

- Moog Inc.

- Northrop Grumman Corp.

- Rolls Royce Holdings Plc

- RTX Corp.

- Safran SA

- Textron Inc.

- Thales Group

- The Boeing Co

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The aviation industry continues to evolve, driven by advancements in technology and the increasing demand for efficient and safe air travel. A key component of this industry's growth is the development and utilization of aviation test equipment. This equipment plays a crucial role in ensuring the performance and safety of manned and unmanned aircraft, as well as various aerospace applications. Aviation test equipment encompasses a wide range of instruments and systems designed to evaluate various aircraft components and systems. These tools are essential for the aviation industry, as they enable the testing and certification of new aircraft designs, the maintenance of existing fleets, and the implementation of new technologies.

One area of significant focus in aviation test equipment is separation assurance. With the increasing number of aircraft in the skies, ensuring adequate distance between them is crucial for safety. Test equipment is used to verify the performance of collision avoidance systems and radar surveillance mechanisms, ensuring mid-air collisions are minimized. Another critical application for aviation test equipment is in the defense industry. Military expenditure on advanced aircraft and weapon systems necessitates rigorous testing to ensure their effectiveness and reliability. Test equipment is used to evaluate the performance of engines, hydraulic systems, and other critical components, as well as to test weapon systems and cyber protection measures.

Composite materials have become increasingly common in the aviation industry due to their lightweight and high-strength properties. Test equipment is used to evaluate the performance of these materials under various conditions, including pressure distribution, temperature, and stress. Automation is another trend driving the market. Software-adaptable solutions and model-based definition (MBD) are being used to streamline testing processes and improve efficiency. These solutions enable the automation of test procedures, reducing the need for manual intervention and minimizing errors. The use of aviation test equipment extends beyond the testing of aircraft components and systems. It is also used in applications such as aerial photography, mapping, and weather conditions monitoring.

For instance, test equipment is used to calibrate cameras and temperature sensors, ensuring accurate data collection for various applications. The aviation industry's reliance on technology continues to grow, with the integration of communication systems, avionics, and data collection systems. Test equipment is used to evaluate the performance of these systems, ensuring they meet the required standards and are free from faults. In , aviation test equipment plays a vital role in the aviation industry, enabling the testing and certification of new aircraft designs, the maintenance of existing fleets, and the implementation of new technologies. The market for aviation test equipment is expected to grow as the industry continues to evolve and embrace new technologies.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2024-2028 |

USD 2030.69 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.96 |

|

Key countries |

US, Canada, China, Russia, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Aviation Test Equipment Market Research and Growth Report?

- CAGR of the Aviation Test Equipment industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the aviation test equipment market growth of industry companies

We can help! Our analysts can customize this aviation test equipment market research report to meet your requirements.

RIA -

RIA -